Global MDI, TDI, and Polyurethane Market Research Report - Segmentation By Application (Flexible Foams, Rigid Foams, Paints & Coatings, Elastomers, Adhesives & Sealants, Others (PUD, RIM, Binders)), End Use Industry, and Region (North America, Europe, Asia Pacific, Latin America, Middle east and Africa) - Industry From 2026 to 2034

Global MDI, TDI, and Polyurethane Market Report Summary

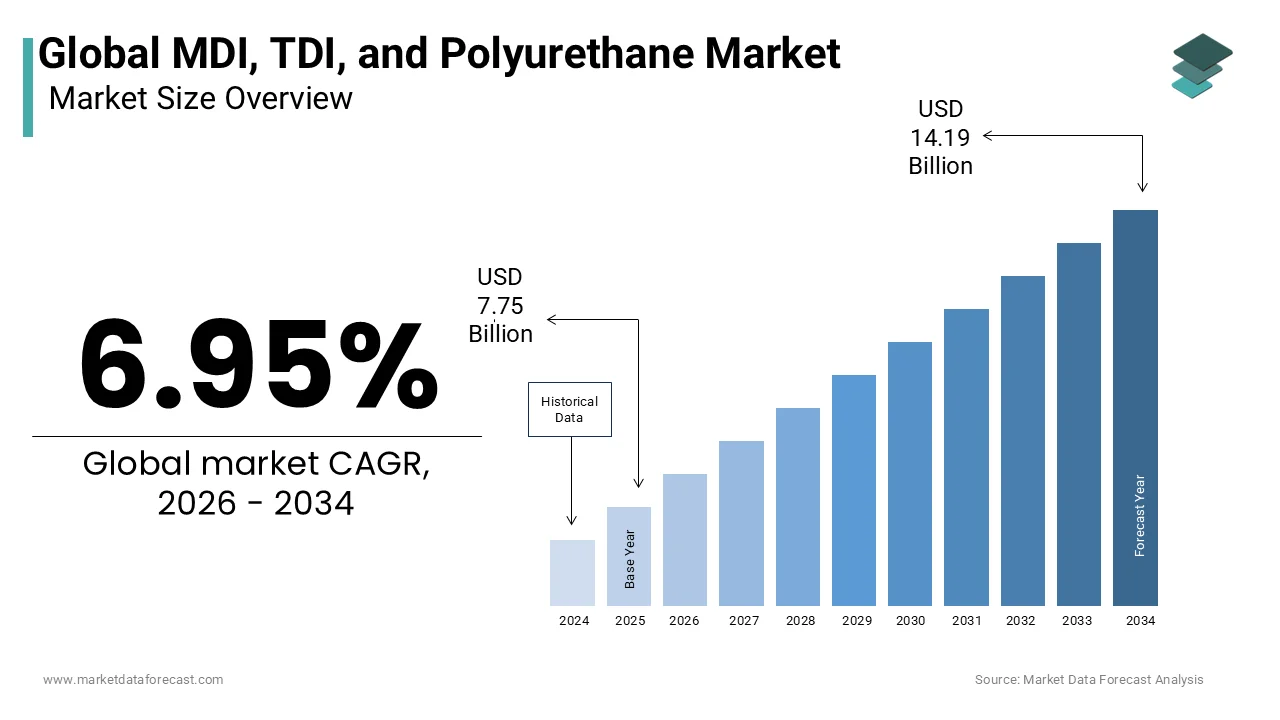

The global MDI, TDI, and polyurethane market was valued at USD 7.75 billion in 2025, is estimated to reach USD 8.29 billion in 2026, and is projected to reach USD 14.19 billion by 2034, growing at a CAGR of 6.95% during the forecast period. Market growth is driven by increasing demand for lightweight and durable materials, rising construction and automotive activities, and expanding industrial applications. MDI, TDI, and polyurethane materials are widely used in insulation, furniture, automotive interiors, coatings, adhesives, and foams due to their flexibility, durability, and thermal efficiency. The growing focus on energy efficient construction and industrial manufacturing is further supporting strong market expansion globally.

Key Market Trends

- Rising demand for lightweight and high performance materials is driving market growth.

- Increasing applications in construction, automotive, and furniture industries are boosting demand.

- Growing use of polyurethane foams for insulation and cushioning is supporting market expansion.

- Expansion of industrial manufacturing and infrastructure projects is enhancing product adoption.

- Innovation in sustainable and energy efficient polyurethane technologies is influencing market development.

Segmental Insights

- Based on application, the rigid foams segment accounted for 31.3% of the global MDI, TDI, and polyurethane market share in 2025. This dominance is attributed to extensive use in insulation materials, refrigeration systems, and construction applications.

- Based on end use industry, the construction segment held 36.9% of the global market share in 2025, driven by rising demand for insulation, sealants, coatings, and energy efficient building materials.

Regional Insights

- The global MDI, TDI, and polyurethane market is experiencing strong growth across regions, supported by rapid industrialization and urban development.

- Asia Pacific was the leading contributor in 2025 and is expected to maintain its dominant position during the forecast period, driven by large scale infrastructure development, expanding manufacturing industries, and urbanization across China, India, and Southeast Asia.

Competitive Landscape

The global MDI, TDI, and polyurethane market is highly competitive, with key players focusing on production expansion, advanced material technologies, and sustainable product innovation to strengthen their market position. Companies are investing in energy efficient polyurethane solutions, specialty formulations, and strategic collaborations. Prominent players in the global MDI, TDI, and polyurethane market include BASF SE, Dow, Covestro AG, Huntsman International LLC, Era Polymers Pty Ltd, Shandong INOV Polyurethane Co., Ltd, Kuwait Polyurethane Industries W.L.L, Wanhua Chemical Group Co. Ltd, Tosoh Corporation, and Yantai Shunda Polyurethane Co. Ltd.

Global MDI, TDI, and Polyurethane Market Size

The global MDI, TDI, and polyurethane market size was valued at USD 7.75 billion in 2025 and is projected to reach USD 14.19 billion by 2034 from USD 8.29 billion in 2026, growing at a CAGR of 6.95%.

Methylene diphenyl diisocyanate and toluene diisocyanate serve as the fundamental chemical building blocks for the production of polyurethane materials which are versatile polymers used across a vast array of industrial and consumer applications. These isocyanates react with polyols to form polyurethanes that can be engineered into rigid foams, flexible foams, coatings, adhesives, sealants, and elastomers. The unique ability to tailor the physical properties of polyurethanes makes them indispensable in sectors ranging from construction and automotive to furniture and appliances. According to the International Isocyanate Institute, global production capacity for MDI exceeds 9 million metric tons annually reflecting the massive scale of this chemical industry. As per the European Chemical Industry Council, the chemicals sector in the European Union directly employs approximately 1.2 million people and generates significant economic value through downstream products like polyurethanes. In the construction sector, polyurethane foams are critical for insulation due to their superior thermal resistance properties. As per the United States Department of Energy, building insulation can reduce energy consumption for heating and cooling by up to 20% and this indicates the functional importance of these materials. The automotive industry also relies heavily on polyurethane for lightweight components that improve fuel efficiency. The interdependence between isocyanate production and downstream manufacturing creates a complex supply chain that is sensitive to raw material availability and regulatory frameworks. This intricate network ensures that developments in the MDI and TDI markets have far reaching implications for multiple end use industries globally.

MARKET DRIVERS

Surging Demand for Energy Efficient Building Insulation

Surging demand for energy efficient building insulation drives the expansion of the global MDI and polyurethane market significantly as governments and consumers prioritize sustainability. Rigid polyurethane foam derived from MDI is one of the most effective insulation materials available offering high thermal resistance per unit thickness. This efficiency is crucial for meeting stringent energy performance standards in new constructions and retrofitting projects. According to the International Energy Agency, buildings and the construction sector combined are responsible for 30% of total global final energy consumption and 27% of total energy sector emissions. The European Union Energy Performance of Buildings Directive mandates that all new buildings be nearly zero energy by 2030 which accelerates the adoption of high performance insulation materials. MDI based foams provide superior air sealing capabilities reducing heat loss and lowering heating and cooling costs for homeowners and businesses. As per the US Environmental Protection Agency, homeowners can save an average of 15% on heating and cooling costs by air sealing their homes and adding insulation in attics and floors. The renovation wave initiative in Europe aims to double annual energy renovation rates in the next decade creating substantial demand for insulation materials. Additionally, the durability and moisture resistance of polyurethane foam extend the lifespan of building envelopes. These factors combined with regulatory incentives and growing awareness of climate change ensure a robust and sustained demand for MDI in the construction insulation sector.

Growth in the Automotive Industry for Lightweighting Applications

Growth in the automotive industry for lightweighting applications substantially fuels the requirement for TDI and MDI based polyurethanes, which is further contributing to the expansion of the global MDI and polyurethane market. Automakers are under increasing pressure to reduce vehicle weight to improve fuel efficiency and meet emission standards particularly with the rise of electric vehicles where battery range is critical. Polyurethane materials are used in seating systems, interior trim, bumpers, and structural components due to their high strength to weight ratio and design flexibility. According to the International Organization of Motor Vehicle Manufacturers, global vehicle production reached approximately 93.5 million units in 2023 indicating a strong base for material consumption. The shift towards electric vehicles is particularly significant as each electric car requires specialized lightweight materials to offset the heavy weight of battery packs. As per the International Council on Clean Transportation, reducing vehicle mass by 10% can improve fuel efficiency by 6% to 8% for conventional vehicles and extend range for electric vehicles. Polyurethane composites and foams offer a viable solution for achieving these weight reductions without compromising safety or comfort. Furthermore, the versatility of polyurethane allows for the integration of complex shapes and functions into single components reducing assembly time and costs. The ongoing expansion of automotive manufacturing in emerging markets such as Asia Pacific and Latin America further amplifies the demand for these advanced materials. Consequently, the automotive sector remains a pivotal driver for the growth of the isocyanate and polyurethane markets.

MARKET RESTRAINTS

Stringent Environmental and Health Regulations on Isocyanates

Stringent environmental and health regulations on isocyanates are hampering the expansion of the MDI and TDI market due to their potential hazards. Isocyanates are known respiratory sensitizers and can cause severe asthma and other lung issues if not handled properly during manufacturing and application. Regulatory bodies worldwide have imposed strict exposure limits and handling requirements to protect workers and consumers. According to the European Chemicals Agency, isocyanates are subject to a restriction under the REACH regulation requiring mandatory training for industrial and professional users before handling these substances. The Occupational Safety and Health Administration in the United States has established permissible exposure limits for both MDI and TDI which necessitate expensive engineering controls and personal protective equipment in industrial settings. These compliance costs increase operational expenses for manufacturers and downstream users potentially limiting market growth. As per the World Health Organization, occupational asthma remains one of the most frequently reported work related lung diseases in industrialized countries and isocyanates are a leading cause of this condition. Additionally, some regions are exploring bans or severe restrictions on certain isocyanate applications in consumer products. The need for continuous monitoring and training adds to the administrative burden for companies. While essential for safety, these regulatory pressures can slow down innovation and adoption in price sensitive segments. Manufacturers must invest heavily in safer handling technologies and alternative formulations to mitigate these risks which can impact profitability and market dynamics.

Volatility in Raw Material Prices and Supply Chain Disruptions

Volatility in raw material prices and supply chain disruptions create financial instability for the MDI TDI and polyurethane market. The production of isocyanates relies heavily on crude oil derivatives such as benzene and natural gas which are subject to significant price fluctuations due to geopolitical tensions and market dynamics. According to the International Energy Agency, oil prices remained highly volatile in recent years with annual average price swings often exceeding 20% to 30%. Benzene, a key precursor for both MDI and TDI, is directly linked to oil prices making it difficult for producers to maintain stable pricing strategies. Additionally, the energy intensive nature of isocyanate production means that spikes in natural gas prices further exacerbate cost pressures. As per the American Chemistry Council, chemical manufacturers continue to experience significant supply chain and logistics challenges including delays in transit and higher freight costs. Logistics bottlenecks and port congestion can delay the delivery of raw materials and finished products affecting customer satisfaction and inventory management. Smaller players in the market may struggle to absorb these cost increases leading to consolidation or exit. The unpredictability of input costs complicates long term planning and investment decisions for manufacturers. Furthermore, trade policies and tariffs can introduce additional barriers and costs affecting global supply chains. This economic uncertainty forces companies to adopt flexible sourcing strategies and hedge against commodity risks but ultimately constrains market growth and profitability in the short to medium term.

MARKET OPPORTUNITIES

Development of Bio Based and Circular Polyurethane Solutions

Development of bio based and circular polyurethane solutions is a lucrative opportunity for market growth. Consumers and industries are increasingly seeking sustainable alternatives to fossil fuel based materials to reduce carbon footprints and support circular economy principles. Manufacturers are innovating by incorporating bio based polyols derived from renewable sources such as soybean, castor oil, and waste biomass into polyurethane formulations. According to the European Bioplastics Association, global bioplastics production capacity is set to increase significantly as demand for more sustainable plastic products continues to grow. Additionally, chemical recycling technologies are being developed to break down post-consumer polyurethane waste into original raw materials such as isocyanates and polyols for reuse. As per the Ellen MacArthur Foundation, a circular economy for plastics could reduce the annual volume of plastics entering our oceans by 80% and reduce greenhouse gas emissions by 25% by 2040. Companies that successfully commercialize bio based and recycled polyurethanes can capture value from the growing demand for green products in construction, automotive, and furniture sectors. Certification schemes and eco labels further enhance the market appeal of these sustainable solutions. Government incentives for sustainable manufacturing and waste reduction also support this transition. By investing in research and development for bio based feedstocks and recycling processes, isocyanate producers can future proof their businesses against resource scarcity and regulatory pressures. This strategic shift not only addresses environmental concerns but also opens new revenue streams and strengthens brand reputation in an increasingly eco conscious market.

Expansion into Emerging Economies with Growing Infrastructure

Expansion into emerging economies with growing infrastructure and industrial bases offers significant growth potential for MDI, TDI and polyurethane market. Regions such as Asia Pacific, Latin America, and Africa are experiencing rapid urbanization and industrialization which drives demand for construction materials, automobiles, and consumer goods. In these markets, the penetration of polyurethane applications is still relatively low compared to developed regions indicating substantial room for growth. According to the World Bank, developing countries will need to invest around 4.5% of their gross domestic product to achieve the Sustainable Development Goals while staying within the limits of a warming climate. The rising middle class in countries like India, China, and Brazil is increasing demand for comfortable housing, appliances, and vehicles all of which utilize polyurethane products. As per the United Nations, the global urban population is projected to reach 6.7 billion by 2050 with much of the growth concentrated in developing regions. Local manufacturing setups or strategic partnerships with regional distributors can facilitate market penetration and ensure supply chain reliability. Additionally, the adoption of international building codes and energy efficiency standards in these regions is gradually increasing the use of high performance insulation materials. By tailoring product offerings to meet the specific needs and economic constraints of these developing regions, isocyanate manufacturers can diversify their revenue streams. This geographic expansion reduces dependence on mature saturated markets in Europe and North America and positions companies for long term sustainable growth.

MARKET CHALLENGES

Intense Competition from Alternative Materials and Technologies

Intense competition from alternative materials and technologies is one of the major challenge to the growth of the global MDI, TDI and polyurethane market. In various applications, polyurethanes face competition from other polymers such as polystyrene, polyethylene, and natural fibers which may offer lower costs or perceived environmental benefits. For instance, in packaging and disposable products, biodegradable plastics and paper based alternatives are gaining traction due to consumer preference for sustainable options. According to the European Bioplastics Association, the global market for bioplastics is expected to grow as the industry seeks to replace traditional fossil based plastics. In the construction sector, mineral wool and fiberglass remain strong competitors to polyurethane foam for insulation due to their non-combustible nature and lower initial cost. As per the North American Insulation Manufacturers Association, fiberglass and mineral wool products continue to hold a massive share of the insulation market due to their long standing use and fire safety profiles. Additionally, advancements in material science are leading to the development of new composite materials that offer superior performance characteristics in specific applications. The automotive industry is exploring aluminum and carbon fiber composites for lightweighting which can replace polyurethane components. These alternatives often benefit from established supply chains and recycling infrastructure. To remain competitive, polyurethane manufacturers must continuously innovate to improve performance, reduce costs, and enhance sustainability. However, the relentless advancement of competing materials requires constant investment in research and development. This competitive pressure can erode market share and margins forcing companies to defend their territory through product differentiation and targeted marketing efforts.

Complexity in Recycling and Waste Management of Polyurethanes

Complexity in recycling and waste management of polyurethanes creates environmental and logistical challenges for the global market. Unlike thermoplastics, polyurethanes are thermoset materials that do not melt upon heating making them difficult to recycle using conventional methods. Most post-consumer polyurethane waste ends up in landfills or is incinerated which contradicts the growing emphasis on circular economy principles. According to the European Environment Agency, roughly 25% of all plastic waste in the European Union was recycled in 2022 and thermoset plastics like polyurethane represent a significant challenge within the unrecycled portion. The lack of efficient recycling infrastructure and standardized collection systems further complicates waste management efforts. Chemical recycling technologies such as glycolysis and hydrolysis are being developed but are not yet commercially viable at large scale due to high costs and technical complexities. As per the American Chemistry Council, the chemical industry is aggressively exploring advanced recycling technologies to convert post use plastics back into their basic chemical components for new products. Regulatory pressures are increasing with governments implementing extended producer responsibility schemes that hold manufacturers accountable for end of life management. This imposes additional financial and operational burdens on companies. Developing effective recycling solutions requires collaboration across the value chain including manufacturers, converters, consumers, and waste management firms. Until scalable and cost effective recycling methods are established, the industry faces reputational risks and potential regulatory restrictions. Addressing this challenge is critical for the long term sustainability and social license to operate for the MDI TDI and polyurethane market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.95% |

| Segments Covered | By Application, End-use Industry, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europ, Asia Pacific, Latin America, Middle East and Africa. |

| Market Leaders Profiled | BASF SE, Dow, Covestro AG, Huntsman International LLC, Era Polymers Pty Ltd, Shandong INOV Polyurethane Co., Ltd, Kuwait Polyurethane Industries W.L.L, Wanhua Chemical Group Co.Ltd, Tosoh Corporation, Yantai Shunda Polyurethane Co.Ltd., and Others |

SEGMENTAL ANALYSIS

By Application Insights

The rigid foams segment commanded for the highest share of 31.3% of the global market in 2025. The growth of the rigid foams segment in the global market can be credited to the unparalleled energy efficiency provided by rigid polyurethane foam which has the lowest thermal conductivity among common insulation materials. This property is essential for meeting stringent global energy conservation standards in residential and commercial buildings. According to the International Energy Agency, the buildings and construction sector is responsible for over 30% of global final energy consumption and approximately 27% of total energy sector emissions. The European Union Energy Performance of Buildings Directive mandates that all new buildings be nearly zero energy by 2030 driving widespread adoption of rigid foam insulation panels. Additionally, the appliance industry relies heavily on rigid foams for refrigerator and freezer insulation to improve energy ratings. As per the United States Department of Energy, homeowners can save up to 20% on heating and cooling costs by properly sealing and insulating their homes. The durability and moisture resistance of rigid foams further enhance their appeal in harsh climates. The ongoing renovation wave in Europe and infrastructure development in Asia Pacific ensure sustained demand. These factors combined with regulatory support for green building practices solidify the leading position of rigid foams in the polyurethane application landscape.

On the other end, the polyurethane elastomers segment is anticipated to record a promising CAGR of 6.2% over the forecast period in the global market due to their versatility and superior mechanical properties in automotive and industrial applications. These materials offer a unique combination of high abrasion resistance, flexibility, and load bearing capacity which makes them ideal for demanding environments. The automotive sector is a key contributor to this growth as manufacturers seek lightweight materials to improve fuel efficiency and extend the range of electric vehicles. According to the International Organization of Motor Vehicle Manufacturers, global vehicle production showed resilience with over 93 million vehicles produced in 2023. As per the International Council on Clean Transportation, reducing vehicle mass by 10% can improve fuel efficiency by 6% to 8% highlighting the strategic importance of lightweight elastomers. Additionally, the industrial sector utilizes polyurethane elastomers for conveyor belts, rollers, and mining equipment due to their durability and resistance to wear and tear. The expansion of mining activities in Latin America and Africa further boosts demand. As per the World Bank, global demand for minerals and metals is expected to grow by nearly 500% by 2050 to meet the needs of clean energy technologies. The ability to tailor the hardness and elasticity of elastomers for specific applications allows for innovation in product design. This adaptability coupled with the trend towards durable and high performance materials ensures that the elastomer segment experiences rapid growth compared to other application areas.

By End Use Industry Insights

The construction segment led the market with 36.9% of the global market share in 2025. The dominance of construction segment in the global market the MDI TDI and polyurethane market is attributed to the extensive use of rigid foams for insulation and flexible foams for sealants and adhesives. The global push for energy efficient buildings is the primary catalyst for this dominance as polyurethane insulation offers superior thermal performance compared to traditional materials. Governments worldwide are implementing strict building codes to reduce carbon emissions from the built environment. According to the United Nations Environment Programme, the building and construction sector is responsible for 37% of global energy related $CO_2$ emissions. The European Union Renovation Wave strategy aims to double the annual energy renovation rate of buildings by 2030 which directly increases the demand for high performance insulation materials like polyurethane. In North America, the Infrastructure Investment and Jobs Act allocates significant funds for building upgrades and energy efficiency improvements. As per the US Census Bureau, total construction spending in the United States was estimated at a seasonally adjusted annual rate of over 2 trillion dollars in 2023. Polyurethane sprays and panels are preferred for their ability to create air tight seals preventing heat loss and improving indoor comfort. The growth of urbanization in Asia Pacific also drives new construction activities where modern building standards increasingly incorporate advanced insulation technologies. The durability and long term energy savings provided by polyurethane products make them a cost effective choice for developers and homeowners. Consequently, the construction industry remains the cornerstone of demand for MDI and TDI based products ensuring its leading market position.

However, the automotive segment is growing exponentially and is estimated to register a CAGR of 6.1% during the forecast period in the global market due to the transition to electric vehicles and the need for lightweighting. Polyurethane materials are extensively used in seating, interiors, bumpers, and structural components due to their ability to reduce weight without compromising safety or comfort. The shift towards electric mobility is particularly significant as battery electric vehicles require weight reduction to offset the heavy mass of battery packs and extend driving range. According to the International Energy Agency, global electric car sales reached 14 million in 2023 representing a substantial increase from previous years. As per the International Council on Clean Transportation, lightweighting remains a critical technological pathway for achieving ambitious fuel economy and $CO_2$ reduction targets. Polyurethane composites and foams offer a high strength to weight ratio making them ideal for replacing heavier metal parts. Additionally, consumer demand for enhanced comfort and noise reduction in vehicles drives the use of polyurethane in acoustic insulation and seating systems. The expansion of automotive manufacturing in emerging markets such as India and Southeast Asia further contributes to growth. As per the Society of Indian Automobile Manufacturers, the Indian auto industry is currently the third largest in the world and experienced strong growth in passenger vehicle sales recently. The continuous innovation in polyurethane formulations to meet specific automotive requirements such as flame retardancy and durability supports the rapid expansion of this segment in the global market.

REGIONAL ANALYSIS

Asia Pacific MDI TDI and Polyurethane Market Analysis

Asia Pacific dominated the market in 2025 and is likely to maintain its dominant position in the global MDI and TDI market as the region continues its rapid path of industrialization and urban expansion in China, India, and Southeast Asia. The region is the largest producer and consumer of polyurethane products due to its massive construction, automotive, and furniture sectors. According to the Asian Development Bank, developing Asia will need to invest 1.7 trillion dollars per year in infrastructure until 2030 to maintain growth momentum and adapt to climate change. China remains the largest market within the region supported by its extensive chemical manufacturing base and growing domestic consumption. The Chinese government initiatives such as the 14th Five Year Plan emphasize green building and energy efficiency which boosts the adoption of polyurethane insulation. As per the National Bureau of Statistics of China, the nation invested 11 trillion yuan in fixed assets related to infrastructure during 2023. India is also emerging as a key growth engine with initiatives like Housing for All driving residential construction. The automotive industry in Asia Pacific is expanding rapidly with major global manufacturers establishing production hubs in the region. As per the International Organization of Motor Vehicle Manufacturers, China remains the world’s largest vehicle producer accounting for approximately 32% of global production. The rising middle class and increasing disposable incomes are driving demand for consumer goods such as furniture and appliances which utilize flexible and rigid foams. The availability of raw materials and competitive labor costs further strengthen the regional market position.

Europe MDI TDI and Polyurethane Market Analysis

Europe is likely to lead the global transition toward a circular polyurethane economy as strict environmental mandates and sustainability goals drive high value technological innovation. Europe is a leader in the development of sustainable and energy efficient polyurethane solutions driven by policies such as the European Green Deal. According to the European Commission, the Renovation Wave strategy aims to double renovation rates in the next ten years to ensure higher energy and resource efficiency. Germany, France, and Italy are the largest markets within the region supported by robust construction and automotive industries. The European automotive sector is undergoing a significant transformation towards electric mobility which increases the demand for lightweight polyurethane components. As per the European Automobile Manufacturers Association, the market share of battery electric cars in the European Union reached 14.6% in 2023. The region is also a hub for research and development with companies investing in bio based and recyclable polyurethane technologies. Strict regulations on volatile organic compounds and hazardous substances drive innovation in safer and more sustainable formulations. As per the European Chemicals Agency, chemical legislation like REACH ensures a high level of protection for human health and the environment. Despite slower growth rates compared to emerging markets, Europe remains a critical region for high value added polyurethane products and technological advancements. The emphasis on circular economy and sustainability ensures that European manufacturers remain at the forefront of innovation.

North America MDI TDI and Polyurethane Market Analysis

North America is likely to see robust growth in high performance polyurethane applications as government incentives for energy efficiency and the resurgence of domestic manufacturing stimulate demand. The region has a well established coatings and plastics industry with a focus on high performance and energy efficient products. According to the American Chemistry Council, the United States chemical industry is a 639 billion dollar enterprise that supports nearly 25% of the nation’s gross domestic product. The construction sector benefits from infrastructure investments and a strong housing market. As per the US Census Bureau, total construction spending in the United States reached a record high seasonally adjusted annual rate of 2.1 trillion dollars at the end of 2023. The automotive industry is also a key driver with the shift towards electric vehicles creating new opportunities for lightweight polyurethane applications. The Inflation Reduction Act in the United States provides tax credits for energy efficient home improvements which boosts the adoption of polyurethane insulation. As per the Department of Energy, the residential sector in the United States consumes about 21% of the country’s total energy. Canada also contributes to market growth with its own energy efficiency programs and construction activities. The region is characterized by high awareness of sustainability and energy conservation which supports the demand for high quality polyurethane products. Innovation in recycling and bio based materials is also gaining traction in North America. The presence of major chemical companies ensures a competitive and dynamic market environment.

Latin America MDI TDI and Polyurethane Market Analysis

Latin America is likely to experience steady market expansion as the region focuses on housing modernization and strengthens its role as a key manufacturing hub for global automotive and appliance supply chains. The region's market is driven by growing construction activities and an expanding automotive sector. According to the Economic Commission for Latin America and the Caribbean, the region’s gross domestic product is projected to grow moderately as countries focus on stabilizing their economies. Brazil is the largest market in the region with a strong demand for polyurethane in furniture and bedding due to its large population and urbanization trends. The Mexican manufacturing sector, particularly automotive and appliances, drives demand for industrial polyurethane applications. As per the Brazilian Institute of Geography and Statistics, the construction industry in Brazil showed a slight growth recently after years of fluctuation. Price sensitivity is a key factor in the region leading to a preference for cost effective solutions. Local manufacturers are expanding production capacities to meet domestic demand and reduce reliance on imports. Environmental regulations are gradually becoming stricter influencing the adoption of newer technologies. The region offers growth opportunities for international players looking to expand their footprint. Urbanization and population growth are driving demand for residential and commercial buildings. The expansion of the middle class is also increasing consumption of consumer goods such as mattresses and sofas. These factors contribute to the steady growth of the polyurethane market in Latin America.

Middle East and Africa MDI TDI and Polyurethane Market Analysis

The Middle East and Africa is likely to emerge as a significant growth frontier for high performance insulation as extreme temperatures and massive urban development projects prioritize thermal efficiency. Countries in the Gulf Cooperation Council are investing heavily in mega projects and urban development as part of economic diversification strategies. According to the World Bank, nations in the Middle East and North Africa are increasingly looking toward green infrastructure and sustainable urban planning to combat climate risks. Saudi Arabia and the United Arab Emirates are the largest markets in the region with projects such as NEOM and Expo City driving material consumption. The construction sector is the primary end user of polyurethane products in this region. As per the Saudi General Authority for Statistics, the non oil sector in Saudi Arabia grew by 4.4% in 2023. South Africa is the largest market in the African region with growing construction and industrial sectors. The region faces challenges related to raw material availability but offers potential for growth. Urbanization and population growth are driving demand for residential and commercial buildings. The adoption of international building standards is influencing the quality of materials used. The hot climate in the region increases the need for effective thermal insulation to reduce cooling costs. These factors support the gradual expansion of the polyurethane market in the Middle East and Africa.

COMPETITIVE LANDSCAPE

The MDI TDI and polyurethane market features intense competition among established chemical giants and emerging regional producers. Competitive dynamics are driven by the need to balance cost efficiency with performance and environmental compliance. Major players differentiate themselves through innovation in sustainable technologies such as bio based polyols and chemical recycling methods. The market is consolidated with a few large corporations controlling significant production capacities globally. Smaller firms focus on niche applications and specialized products to retain customer loyalty. Regulatory pressures regarding hazardous substances and carbon emissions force continuous adaptation and investment in cleaner technologies. Price volatility of raw materials like benzene and natural gas adds complexity to competitive strategies. Companies must navigate these challenges by optimizing supply chains and enhancing product value propositions. The shift towards green chemistry creates opportunities for those who can successfully innovate while maintaining profitability. Strategic alliances and capacity expansions are common tactics to expand market reach. This competitive landscape demands agility and forward thinking to sustain growth and relevance in the global chemical industry.

Key Market Players

The major key players of the global MDI, TDI, and polyurethane market are

-

BASF SE

-

Dow

-

Covestro AG

-

Huntsman International LLC

-

Era Polymers Pty Ltd

-

Shandong INOV Polyurethane Co., Ltd

-

Kuwait Polyurethane Industries W.L.L

-

Wanhua Chemical Group Co. Ltd

-

Tosoh Corporation

-

Yantai Shunda Polyurethane Co. Ltd

Top Players in the Market

-

BASF SE is a leading global chemical producer with a significant portfolio in isocyanates and polyurethane systems. The company provides innovative solutions for construction automotive and furniture industries through its advanced material technologies. BASF focuses on sustainability by developing bio based polyols and recycling technologies for polyurethane waste. Recent actions include the expansion of its production capabilities in Asia to meet growing regional demand. The company also invests in digital platforms to enhance customer engagement and supply chain efficiency. By prioritizing circular economy principles BASF strengthens its market position through products that support environmental goals. Their continuous research and development efforts ensure they remain at the forefront of technological advancements in the polyurethane sector.

-

Covestro AG is a premier supplier of high quality polymer materials including MDI TDI and polyurethane precursors. The company serves diverse sectors such as automotive construction and electronics with specialized coating and adhesive solutions. Covestro emphasizes innovation and sustainability by launching carbon neutral production processes and bio based alternatives. Recent initiatives include the construction of new facilities in China to expand capacity and improve local supply chains. The company actively collaborates with partners to develop recyclable polyurethane materials for various applications. These strategic moves enhance its competitive edge by addressing regulatory requirements and consumer preferences for eco friendly products. Covestro remains a key driver of innovation in the global isocyanate and polyurethane industry.

-

Wanhua Chemical Group Co Ltd is a major global player in the MDI and polyurethane market with extensive production capacities. The company offers a wide range of isocyanates and polyol products for industrial and consumer applications. Wanhua focuses on vertical integration to secure raw material supplies and optimize cost efficiency. Recent actions include the acquisition of technology firms to enhance its research and development capabilities. The company has expanded its global footprint by establishing production sites in Europe and North America. Wanhua also invests in sustainable chemistry initiatives to reduce environmental impact. These efforts strengthen its position as a reliable supplier of high performance polyurethane materials worldwide. Their strategic growth initiatives ensure long term competitiveness in the dynamic chemical market.

Top Strategies Used by Key Market Participants

Key players in the MDI TDI and polyurethane market primarily focus on sustainability and innovation to maintain competitive advantage. Companies invest heavily in research and development to create bio based and recyclable polyurethane solutions that meet stringent environmental regulations. Strategic expansions of production facilities in emerging markets allow manufacturers to cater to growing demand in Asia Pacific and Latin America. Partnerships with raw material suppliers ensure stable access to feedstocks and reduce supply chain risks. Additionally firms engage in collaborations with downstream customers to develop customized formulations for specific applications. Digitalization of operations enhances efficiency and customer service. These strategies collectively strengthen market positions by addressing regulatory pressures and evolving consumer preferences for eco-friendly products while optimizing operational costs.

MARKET SEGMENTATION

This research report on the global MDI, TDI, and polyurethane market has been segmented and sub-segmented based on product, type, end-user, and region.

By Application

-

Flexible Foams

-

Rigid Foams

-

Paints & Coatings

-

Elastomers

-

Adhesives & Sealants

-

Others (PUD, RIM, Binders)

By End-use Industry

-

Construction

-

Furniture & Interiors

-

Electronics & Appliances

-

Automotive

-

Footwear

-

Others (Apparel, Marine, Medical, Packaging)

By Region

-

North America

-

Europe

-

Asia Pacific

-

Latin America

-

Middle East & Africa

Frequently Asked Questions

1.What is the MDI, TDI, and polyurethane market?

The MDI, TDI, and polyurethane market covers the production and use of methylene diphenyl diisocyanate MDI, toluene diisocyanate TDI, and polyurethane materials used in foam and non foam applications.

2.What factors are driving growth in the MDI, TDI, and polyurethane market?

Market growth is driven by rising demand from construction, automotive, furniture, and appliances industries.

3.What is the difference between MDI and TDI?

MDI is mainly used in rigid foams and structural applications, while TDI is commonly used in flexible foams for bedding and seating.

4.How are polyurethanes used in the construction industry?

Polyurethanes are used in insulation panels, spray foams, sealants, and coatings to improve energy efficiency and durability.

5.What role does the automotive industry play in market demand?

The automotive industry drives demand for polyurethane foams in seating, interiors, insulation, and lightweight components.

6.What are the main types of polyurethane products?

Major types include rigid foams, flexible foams, elastomers, coatings, adhesives, and sealants.

7.What industries are the largest consumers of MDI and TDI?

Key consuming industries include construction, furniture and bedding, automotive, electronics, and footwear.

8.Which regions dominate the global MDI, TDI, and polyurethane market?

Asia Pacific, North America, and Europe dominate the market due to strong manufacturing and construction activities.

9.Who are the key players in the MDI, TDI, and polyurethane market?

Key players include BASF, Covestro, Huntsman Corporation, Dow, and Wanhua Chemical.

10.What challenges does the market face?

Challenges include volatile raw material prices, health and safety regulations, and environmental concerns.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com