Middle East And Africa Carbohydrase Market Segmented By Source (Plants, Animals, Microorganisms), Type (Amylases, Cellulases), Application (Animal Feed, Pharmaceuticals, Food & Beverages, Others), And Country (KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan and Rest of MEA) – Size, Share, Trends, Growth, Forecast (2026 to 2034)

Middle East and Africa Carbohydrase Market Size

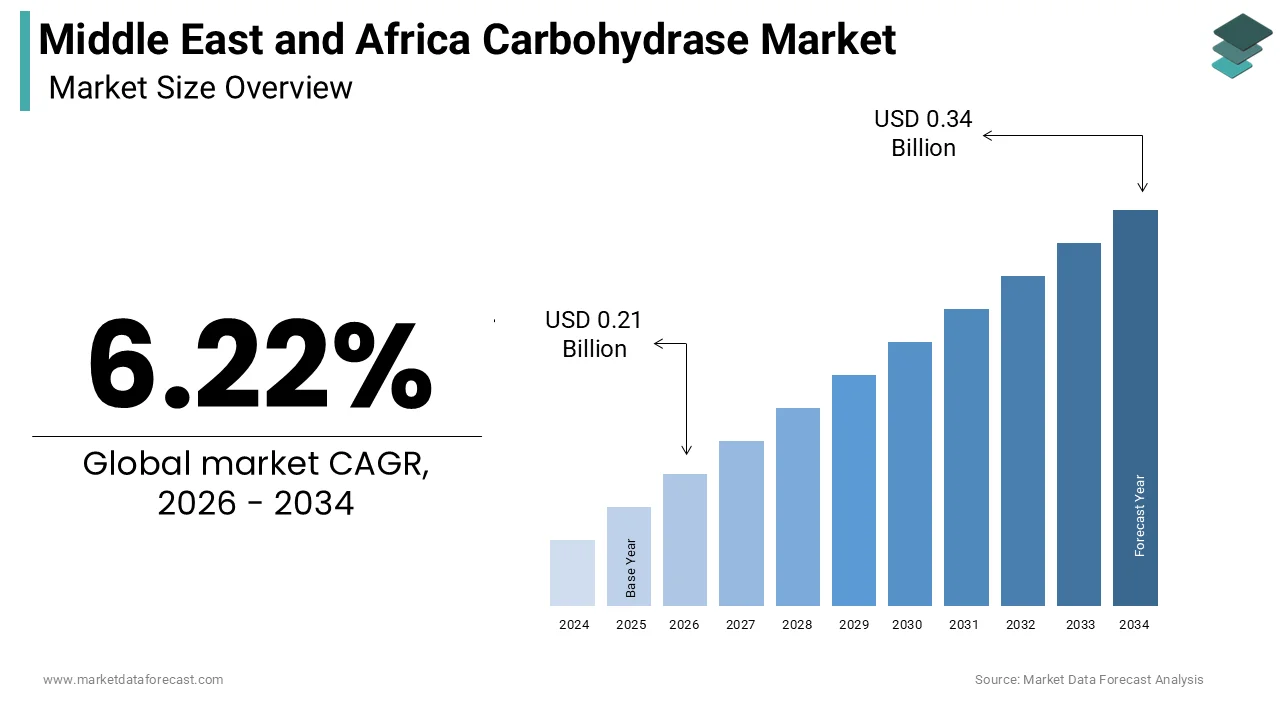

The Middle East and Africa Carbohydrase Market size was calculated to be USD 0.20 billion in 2025 and is anticipated to be worth USD 0.34 billion by 2034, from USD 0.21 billion in 2026, growing at a CAGR of 6.22% during the forecast period.

A carbohydrase is an enzyme that breaks down carbohydrates (like starches and complex sugars) into simple, easily absorbed sugars (like glucose). These biocatalysts are integral to various industries, including food processing, animal feed, biofuel production, and textile manufacturing. The region is witnessing a gradual shift toward sustainable industrial practices, which has elevated the importance of enzymatic solutions over traditional chemical methods. According to data from the Food and Agriculture Organization (FAO), the agricultural sector in Sub-Saharan Africa employs over 60 percent of the region's entire workforce. Furthermore, the World Bank Group and regional bodies confirm that the Middle East and North Africa (MENA) region imports tens of millions of tons of cereal annually to bridge domestic production gaps. Sources note that this high baseline volume of grain moving through the supply chain yields an expanded addressable market for domestic milling and baking optimization systems. UN-Habitat and UN DESA establish that the urbanization rates of Gulf nations like Saudi Arabia and the United Arab Emirates exceed 80 percent. From a commercial standpoint, this rapid shift away from rural settings strongly correlates with a rising consumer reliance on modern retail and shelf-stable packaged foods. This market is characterized by its reliance on importation due to limited local manufacturing capabilities, yet it shows promising growth trajectories driven by regulatory shifts favoring green chemistry and increasing investments in the bioeconomy across key Gulf nations.

MARKET DRIVERS

Rising Demand for Processed Food Products Drives Enzyme Adoption

The escalating consumption of processed and convenience foods across the region drives the growth of the MEA carbohydrase market. Rapid urbanization and changing lifestyles have significantly altered dietary habits, leading to a surge in demand for baked goods, beverages, and dairy products, where enzymes are essential for quality improvement. According to macroeconomic datasets published by the World Bank, the non-oil services sector across Gulf Cooperation Council (GCC) economies contributes more than 50 percent to total non-hydrocarbon GDP, mirroring broader economic diversification efforts and urbanized consumption transformations. This transition necessitates efficient industrial processing methods. Carbohydrases such as amylases and cellulases are extensively used to modify starch viscosity, improve bread volume, and enhance juice clarity. The World Health Organization (WHO) shows an escalating prevalence of diet-related noncommunicable diseases across the Middle East, while commercial food processors separately deploy targeted enzyme technologies (such as invertases or lactases) to reformulate consumer products with lower sugar profiles without altering texture. Additionally, the population of the Middle East and Africa is projected to reach 2.5 billion by 2050 as per United Nations estimates, creating an immense consumer base for affordable and shelf-stable food items. Manufacturers are increasingly adopting enzymatic solutions to meet these volume requirements while maintaining consistent product quality, thereby directly fueling the demand for carbohydrases in the regional food and beverage industry.

Expansion of the Animal Feed Industry Boosts Enzyme Utilization

The robust expansion of the livestock and poultry sectors in the region significantly propels the demand for these enzymes in animal feed applications, which further accelerates the expansion of the MEA carbohydrase market. Governments across the region are prioritizing food security and self-sufficiency in meat and dairy production, leading to substantial investments in modern farming infrastructure. As per the Food and Agriculture Organization, poultry meat production in Africa increased by approximately 4 percent annually over the last decade, reflecting a steady rise in protein consumption. Carbohydrases such as xylanases and beta-glucanases are critical in breaking down non-starch polysaccharides in plant-based feed ingredients, thereby improving nutrient digestibility and feed efficiency. This is particularly vital in regions where high-quality grain resources are scarce or expensive. The World Bank highlights that agricultural value added in several Sub-Saharan African countries grows at a rate of 3 to 5 percent per year, driven by intensified livestock operations. By incorporating these enzymes, feed producers can utilize locally available but less digestible raw materials, reducing dependency on imported soy and corn. Furthermore, the push for sustainable agriculture encourages the use of enzymes to reduce phosphorus excretion and environmental pollution from animal waste. This alignment with environmental regulations and economic efficiency makes carbohydrases an indispensable component in the evolving animal nutrition landscape of the MEA region.

MARKET RESTRAINTS

High Dependency on Imported Raw Materials Constrains Market Growth

The heavy reliance on imported raw materials and finished enzyme products is a significant restraint on the MEA carbohydrase market. This exposes the market to global supply chain volatilities and currency fluctuations. Most countries in the Middle East and Africa lack the advanced biotechnology infrastructure required for large-scale enzyme fermentation and purification, forcing them to source these specialized products from Europe, North America, and Asia. The World Trade Organization (WTO) highlights that import duties on specialty industrial chemicals and biological inputs vary considerably across individual jurisdictions, adding to the structural price burdens of localized manufacturing plants. Additionally, fluctuating foreign exchange rates in countries like Egypt and Nigeria significantly impact procurement costs, making budget planning difficult for end users. The United Nations Conference on Trade and Development notes that logistics costs in landlocked African countries can be up to 50 percent higher than in coastal nations, further exacerbating the price burden. This dependency also leads to longer lead times, which can disrupt production schedules for food and feed processors who require just-in-time delivery of perishable or sensitive enzymatic solutions. The lack of local production capabilities means that any global disruption, such as those seen during recent geopolitical tensions or pandemics, immediately affects availability and pricing in the MEA region, thereby hindering consistent market expansion and adoption among small and medium enterprises.

Limited Technical Expertise and Awareness Hinders Adoption

The limited technical expertise and low awareness regarding the benefits of enzymatic solutions among small and medium-sized enterprises are a major barrier to penetration in the MEA carbohydrase market. Many local manufacturers in the food and feed sectors continue to rely on traditional chemical processes due to a lack of understanding about the efficiency and sustainability advantages of carbohydrases. As per the United Nations Industrial Development Organization, the manufacturing sector in many African countries is dominated by micro and small enterprises that often lack access to technical training and innovation resources. This knowledge gap prevents them from optimizing enzyme usage, leading to skepticism about return on investment. Furthermore, there is a shortage of skilled biotechnologists and process engineers who can provide adequate technical support and customization for local applications. The World Bank indicates that only 20 percent of firms in Sub-Saharan Africa offer formal training programs for their employees, which limits the diffusion of advanced industrial technologies. Without proper guidance, potential users may experience suboptimal results from enzyme application, reinforcing negative perceptions. Educational institutions and industry bodies have been slow to integrate modern bioprocessing curricula, resulting in a talent pool that is not fully equipped to drive enzymatic innovation. This human capital deficit slows down the transition from conventional methods to enzyme-based technologies, restricting market growth despite the clear economic and environmental benefits.

MARKET OPPORTUNITIES

Growth in Biofuel Production Presents Significant Opportunities

The emerging biofuel sector in the region offers substantial opportunities for the MEA carbohydrase market. This trend is particularly visible in the production of second-generation bioethanol from lignocellulosic biomass. Several countries in the region are diversifying their energy mix to reduce dependence on fossil fuels and meet international climate commitments. The IEA indicates that Africa possesses massive bioenergy potential, but notes that over 80% of current bioenergy use in Sub-Saharan Africa remains traditional biomass (wood and charcoal) used for inefficient cooking, rather than modernized industrial liquid biofuels. Carbohydrases such as cellulases and hemicellulases are essential for hydrolyzing complex plant fibers into fermentable sugars, a critical step in bioethanol production. The African Union’s Agenda 2063 framework targets sustainable industrialization, which AFREC (African Energy Commission) implements by pushing for formalized policy guidelines to modernize bioenergy sectors and transition away from forest degradation. This creates a new demand stream for industrial enzymes beyond traditional food and feed applications. Furthermore, governments are introducing incentives for renewable energy projects, which can offset the high initial costs of enzymatic hydrolysis processes. The FAO highlights that optimizing agro-industrial investment and circular value chains in Africa is vital, warning that modern bioenergy systems must be carefully designed to prevent land tenure disputes or food security concerns. As technology matures and economies of scale are achieved, the cost-effectiveness of enzymatic biofuel production will improve, making it a viable alternative to first-generation biofuels that compete with food crops. This shift positions carbohydrases as key enablers of the regional green energy transition.

Regulatory Shifts Toward Green Chemistry Favor Enzyme Adoption

Increasing regulatory pressure to adopt environmentally friendly manufacturing processes opens the door for the MEA carbohydrase market. Governments and regional bodies are progressively implementing stricter environmental standards to reduce industrial pollution and promote sustainable development. The United Nations Environment Programme (UNEP) coordinates regional compliance with the Bamako Convention and Stockholm Convention to ban or limit hazardous chemical waste imports and usage across Africa. Carbohydrases offer a green alternative to harsh acids and alkalis traditionally used in textile desizing, paper pulping, and starch processing. The European Union's Green Deal influences the MEA region primarily through the impending implementation of the Carbon Border Adjustment Mechanism (CBAM) and strict pesticide/chemical maximum residue limits (MRLs) on agricultural imports. Local regulations in countries like Morocco and Tunisia are increasingly aligning with these global standards, mandating lower wastewater toxicity and reduced energy consumption. Enzymatic processes operate under milder conditions, significantly lowering water and energy usage compared to conventional methods. The World Bank warns that the Middle East and North Africa (MENA) is the most water-scarce region globally, with over 60% of the population facing high water stress. This drives a strategic push toward solar-powered desalination and advanced wastewater recycling. By switching to enzyme-based solutions, manufacturers can comply with environmental regulations while reducing operational costs related to waste treatment and energy bills. This regulatory tailwind not only drives adoption in regulated industries but also enhances the brand image of companies committed to sustainability, opening doors to premium markets and eco-conscious consumers.

MARKET CHALLENGES

Volatility in Agricultural Raw Material Prices Impacts Cost Structure

Price volatility in agricultural raw materials remains a primary challenge for the MEA carbohydrase market. Because these materials function as both substrates for enzyme production and final end-use applications, these price fluctuations heavily impact overall market stability. Since many carbohydrases are produced through fermentation using starch or sugar-based media, fluctuations in the cost of corn, wheat, and sugarcane directly affect manufacturing expenses. The FAO Food Price Index (FFPI) tracks massive global swings, notably peaking at an all-time record high of 159.7 points following geopolitical shocks, affecting global agribusiness supply chains. In the MEA region, where agriculture is heavily dependent on rainfall and subject to extreme weather events, local crop yields can be unpredictable, forcing reliance on volatile international markets. The World Bank stresses that Sub-Saharan Africa is disproportionately vulnerable to climate shocks, where severe droughts or unpredictable rainfall cycles trigger localized crop yield shocks ranging from 15% to over 25% for staple grains. This unpredictability makes it difficult for enzyme manufacturers to maintain stable pricing structures, potentially passing on costs to end users who may already be operating on thin margins. Additionally, high raw material costs can discourage small-scale farmers and processors from adopting enzyme technologies, as they perceive them as premium inputs. The lack of long-term hedging mechanisms and futures markets for agricultural commodities in many African countries further amplifies this risk. Consequently, manufacturers must constantly navigate a complex pricing environment, balancing cost efficiency with product affordability, which can hinder widespread market penetration and consistent revenue growth.

Inadequate Infrastructure Limits Distribution and Storage Efficiency

The inadequate infrastructure for cold chain logistics and storage is a significant limitation to the effective distribution and preservation of carbohydrase products in the region, which holds back the expansion of the Middle East and Africa market. Enzymes are biological molecules that are sensitive to temperature and humidity, requiring controlled storage conditions to maintain their activity and shelf life. However, many regions in Africa and parts of the Middle East suffer from unreliable electricity supply and insufficient refrigerated transport networks. The IEA consistently verifies that roughly 600 million people in Sub-Saharan Africa completely lack electricity access, making basic cold-chain infrastructure for everyday food security and life-saving medicines incredibly difficult to sustain. The World Bank and partner groups track that post-harvest losses in Sub-Saharan Africa average 20% to 40% for highly perishable fruits and vegetables due to systemic logistics bottlenecks, which severely impact agricultural market value. This infrastructural deficit leads to product degradation during transit, resulting in financial losses for distributors and reduced efficacy for end users. Furthermore, the high cost of establishing and maintaining cold chain infrastructure discourages smaller distributors from entering the market, limiting reach to remote agricultural and industrial zones. Without reliable logistics, manufacturers face difficulties in ensuring product quality consistency, which can damage brand reputation and customer trust. Addressing these infrastructural gaps requires substantial investment in power grids and transportation networks, which remains a long-term challenge for many governments in the region, thereby constraining the efficient dissemination of carbohydrase technologies.

The Carbohydrase market is showcasing significant potential over the mentioned forecast period. The market continues to build up momentum with the pharma sector registering rapid growth over recent years, leading to increased interest shown by companies in the market.

Carbohydrase is a kind of enzyme, with a large family of cellulase, amylase, etc. Carbohydrase is an important raw material in various applications in different industries like food, beverages, animal feed, pharmaceuticals, leather, textile, and others. One of the major purposes of carbohydrase in these industries is to reduce greenhouse gas emissions and avoid wastage of other raw materials.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.22% |

| Segments Covered | By Type, Application, Source, And Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | KSA, UAE, Israel, the rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, and the rest of MEA. |

| Market Leader Profiled | Dyadic International, Inc, Amano Enzyme Inc, AB Enzymes GmbH, Novozymes, Royal DSM, CHR. Hansen Holding A/S, Advanced Enzymes, Verenium, E.I. Dupont De Nemours & Co, And Specialty Enzymes |

SEGMENTAL ANALYSIS

By Type Insights

The amylase segment was the largest in the MEA carbohydrase market and occupied a 55.6% share in 2025. This supremacy of the segment was supported by its extensive utility in starch processing and baking industries, which are foundational to regional food security. The main driver is the massive consumption of wheat-based products across the Middle East and North Africa region. The Food and Agriculture Organization (FAO) highlights that several Middle Eastern and North African economies rely on imports for more than 50 percent of their cereal supply, while downstream commercial mills independently utilize specialized baking enzymes like amylases to standardize flour quality and extend shelf life. These enzymes improve dough handling and extend shelf life, which is critical in hot climates. A further key driving factor is the growth of the brewing and beverage sector in countries like Egypt and South Africa. As per sources, the manufacturing sector in these nations continues to expand, with beverage production seeing steady annual growth. Amylases facilitate the conversion of starch into fermentable sugars essential for alcohol and soft drink production. The ease of integration into existing industrial processes and the proven cost-effectiveness of amylases compared to alternative methods further solidify their market dominance, making them the preferred choice for large-scale industrial applications throughout the region.

However, the cellulase segment is projected to register the fastest CAGR of 7.5% during the forecast period. This accelerated growth of the segment is mainly propelled by the rising demand for sustainable textile processing and biofuel production. The textile industry in countries such as Egypt and Turkey, which serves as a major export hub for the region, is increasingly adopting enzymatic desizing and biopolishing techniques to meet international environmental standards. According to the United Nations Industrial Development Organization, the textile sector contributes significantly to industrial output in North Africa, prompting a shift away from harsh chemical treatments. Cellulases offer a greener alternative that reduces water usage and effluent toxicity. Additionally, the emerging bioenergy sector in South Africa and Kenya is leveraging cellulases to convert agricultural residues into second-generation bioethanol. The International Energy Agency shows that Africa has vast untapped potential for biomass energy, with millions of tons of crop waste available annually. As governments implement policies to reduce carbon footprints and diversify energy sources, the adoption of cellulases in lignocellulosic biomass hydrolysis is gaining momentum, thereby driving the rapid expansion of this segment.

By Application Analysis

In 2025, the animal feed segment held the 40.2% majority share of the MEA carbohydrase market because of the urgent need to enhance livestock productivity and ensure food security in a region characterized by limited arable land and water resources. Governments across the Gulf Cooperation Council and North Africa are heavily investing in modernizing their poultry and dairy sectors to reduce reliance on meat imports. As per the Food and Agriculture Organization, poultry meat consumption in the Middle East has grown by over 3 percent annually in recent years, necessitating efficient feed solutions. Carbohydrases such as xylanases and beta-glucanases improve the digestibility of plant-based feed ingredients, allowing manufacturers to utilize locally sourced but less nutritious crops. This reduces dependency on expensive imported soy and corn. A different key driver is the increasing focus on reducing environmental impact from livestock farming. The World Bank notes that agricultural intensification in Sub-Saharan Africa is leading to higher waste outputs, prompting the use of enzymes to minimize phosphorus excretion. By improving nutrient absorption, carbohydrases help lower the ecological footprint of intensive farming operations. This makes them a critical component in the strategic development of the regional livestock industry.

But the pharmacy segment is anticipated to witness the highest CAGR of 8.2% from 2026 to 2034 due to the rising prevalence of lifestyle-related diseases and the growing healthcare infrastructure in the region. The World Health Organization reports that noncommunicable diseases such as diabetes and obesity are increasing at an alarming rate in the Middle East, with some Gulf countries having among the highest prevalence rates globally. This has spurred demand for digestive health supplements and therapeutic enzymes, including carbohydrases like lactase and alpha galactosidase, which aid in managing dietary intolerances and metabolic disorders. Furthermore, the pharmaceutical industry in countries like Saudi Arabia and the United Arab Emirates is undergoing a significant transformation under national vision programs aimed at localizing drug manufacturing. According to the World Bank, healthcare expenditure in the Gulf region is expected to rise substantially as populations age and chronic disease burdens increase. The push for preventive healthcare and wellness products is also driving consumer interest in enzyme-based dietary supplements. Regulatory frameworks are becoming more supportive of biopharmaceutical innovations. As a result, the pharmacy application segment is poised for robust growth driven by both clinical demand and consumer health awareness.

By Source Analysis

The microorganisms segment dominated the MEA carbohydrase market and accounted for a substantial share in 2025. This overwhelming dominance of the segment was driven by the superior efficiency, scalability, and cost-effectiveness of microbial fermentation compared to animal or plant extraction methods. Microbial enzymes can be produced in large quantities with consistent quality and high purity, which is essential for industrial applications. Industrial biochemistry patents show a continuous focus on microbial strain optimization and directed evolution techniques to engineer industrial enzymes capable of maintaining structural stability under extreme processing temperatures and pH levels. Bacteria and fungi such as Aspergillus and Bacillus species are widely used because they produce robust enzymes that withstand high temperatures and varying pH levels common in food and feed processing. Additionally, the main driver keeping this segment in the lead is the ethical and religious considerations prevalent in the Middle East and Africa. The widespread adherence to Halal dietary laws makes microbial sources more acceptable than animal-derived enzymes, which may raise concerns about source certification. The global trend toward sustainable and vegan-friendly products also favors microbial enzymes. Research shows that fermentation-derived microbial enzymes remain the foundational supply chain anchor for industrial processing, due to the high scalability and rapid production cycles of microbial bioreactors compared to plant extraction.

On the other hand, the plants segment is likely to experience the fastest CAGR of 6.8% over the forecast period. This swift growth of the segment is fuelled by the increasing consumer preference for natural and clean-label ingredients in food and pharmaceutical applications. As health consciousness rises across the Middle East and Africa, consumers are actively seeking products free from synthetic additives and genetically modified organisms. The World Health Organization (WHO) supports frameworks for evaluating the safety of traditional herbal medicine systems in Africa, whereas plant-derived industrial enzymes separately expand their footprints within commercial food and beverage processing sectors. Papain from papaya and bromelain from pineapple are gaining traction in digestive health supplements and meat tenderizing applications. The agricultural diversity in countries like Kenya and Ethiopia provides a rich base for extracting these enzymes from locally grown fruits and vegetables. Furthermore, the rise of the organic food sector in urban centers such as Dubai and Cairo is creating niche markets for plant-based processing aids. The United Nations Conference on Trade and Development highlights that organic agriculture is expanding in Africa with increased exports of certified organic products. This trend encourages local manufacturers to invest in plant extraction technologies, thereby driving the rapid growth of the plant source segment in the regional carbohydrase market.

REGIONAL ANALYSIS

Saudi Arabia Carbohydrase Market Analysis

Saudi Arabia led the MEA carbohydrase market and captured a 25.3% share in 2025. This supremacy of the country’s market was supported by its aggressive economic diversification strategy under Vision 2030, which prioritizes food security and industrial localization. The government is heavily investing in the agricultural and food processing sectors to reduce dependency on imports. According to the General Authority for Statistics, the food and beverage industry in Saudi Arabia has seen consistent growth driven by a young and affluent population. The demand for high-quality baked goods and processed foods is surging, which directly boosts the consumption of amylases and other carbohydrases. Additionally, the kingdom is promoting the use of advanced biotechnologies in its livestock sector to enhance productivity. The Ministry of Environment, Water, and Agriculture has launched initiatives to improve feed efficiency using enzymatic solutions. The presence of major international enzyme manufacturers establishing regional headquarters in Riyadh further strengthens the supply chain. The combination of strong government support, rising disposable income,s and a booming food service sector ensures that Saudi Arabia remains the largest and most dynamic market for carbohydrases in the Middle East.

UAE Carbohydrase Market Analysis

The United Arab Emirates was positioned second in the MEA carbohydrase market and held an 18.6% share in 2025. Also, the country serves as a major re-export hub for the entire region due to its world-class logistics infrastructure and free trade zones. The market status is characterized by a highly developed food and beverage industry catering to a diverse multinational population. The UAE Ministry of Economy outlines a targeted strategy to scale the national UAE Food Cluster's GDP contribution, accelerating manufacturing innovation and advanced food processing to build a self-sustaining regional ecosystem. The UAE is also a leader in adopting sustainable industrial practices with strict environmental regulations encouraging the use of green chemistry solutions like carbohydrases inthe textile and paper industries. The government’s focus on innovation and technology transfer through initiatives like the National Innovation Strategy attracts global biotech firms to set up research and distribution centers in the country. This ecosystem facilitates the rapid adoption of new enzyme technologies. The high purchasing power of consumers and the presence of sophisticated manufacturing facilities make the UAE a key driver of market growth and a gateway for introducing advanced carbohydrase products to neighboring markets.

South Africa Carbohydrase Market Analysis

South Africa plays a key role in the MEA carbohydrase market. The country possesses the most advanced industrial base in the region, with a well-established food processing, mining, and textile sector. The market status shows a mature regulatory framework and a strong emphasis on agricultural efficiency. According to Statistics South Africa, the manufacturing sector contributes significantly to the national gross domestic product,t with food and beverages being a major component. The poultry and livestock industries are highly commercialized and rely heavily on enzyme-supplemented feeds to optimize costs and improve animal health. The country is also a pioneer in biofuel research with several pilot projects exploring the use of cellulases for ethanol production from sugarcane bagasse. The Department of Science and Innovation supports biotechnology initiatives that promote the local production and application of industrial enzymes. Furthermore, South Africa’s integration into global trade networks allows for the easy import of specialized carbohydrases while also exporting value-added agricultural products. This dual role as a consumer and producer positions South Africa as a critical growth engine for the carbohydrase market in Africa.

Egypt Carbohydrase Market Analysis

Egypt maintains a noteworthy position in the regional market due to its large population and substantial agricultural sector, which forms the backbone of its economy. It is one of the largest importers of wheat in the world, creating a massive demand for milling and baking enzymes. As per the Central Agency for Public Mobilization and Statistics, the food industry is one of the largest industrial sectors in Egypt, employing a significant portion of the workforce. The government is actively supporting modernization efforts in the flour milling and bakery sectors to improve product quality and reduce waste. Additionally, Egypt has a thriving textile industry which is increasingly adopting enzymatic processes for desizing and anbiopolishing to meet European export standards. The Ministry of Trade and Industry promotes sustainable manufacturing practices that favor the use of carbohydrases over traditional chemicals. The availability of low-cost labor and raw materials, combined with strategic geographic location, makes Egypt an attractive market for enzyme suppliers. The ongoing economic reforms and infrastructure developments further enhance the business environment for industrial biotechnology products.

Kenya Carbohydrase Market Analysis

Kenya is also a significant player in the regional market, owing to a vibrant agricultural sector and a growing middle class that is driving demand for processed foods and animal products. The Kenya National Bureau of Statistics (KNBS) confirms that the agricultural sector serves as the backbone of the economy, contributing approximately 33 percent of Kenya's Gross Domestic Product (GDP) and employing over 40 percent of the total population. The poultry and dairy industries are expanding rapidly, leading to increased adoption of feed enzymes to improve productivity. Kenya is also a leader in renewable energy initiatives, with growing interest in biofuel production from agricultural residue,s which creates opportunities for cellulase applications. The government’s Big Four Agenda prioritizes food security and manufacturing, which includes support for value addition in agriculture through technological interventions. The presence of regional headquarters for many multinational companies in Nairobi facilitates the distribution of carbohydrate products across East Africa. The country’s stable political environment and progressive regulatory framework make it an ideal entry point for companies looking to expand their footprint in the broader African market.

COMPETITION OVERVIEW

The competition in the MEA carbohydrase market is characterized by the presence of a few dominant global players alongside a growing number of regional distributors and local manufacturers. Multinational corporations leverage their advanced research and development capabilities and extensive product portfolios to maintain a competitive edge. However, they face increasing pressure from local entities that offer cost-effective solutions and a better understanding of regional market dynamics. The market is moderately consolidated, with key players focusing on differentiation through product quality, technical support, and sustainability credentials. Price competition remains intense, particularly in the animal feed segment, where margins are thin. Companies are increasingly competing on value-added services such as process optimization and regulatory compliance assistance. The lack of local production facilities means that most competitors rely on imports, making supply chain efficiency a critical competitive factor. As demand grows, new entrants are likely to emerge, particularly in countries with supportive biotechnology policies, leading to a more dynamic and fragmented competitive landscape in the coming years.

KEY MARKET PLAYERS

A few major players of the MEA Carbohydrase Market include

- Dyadic International, Inc

- Amano Enzyme Inc

- AB Enzymes GmbH

- Novozymes

- Royal DSM

- CHR. Hansen Holding A/S

- Advanced Enzymes

- Verenium

- E.I. Dupont De Nemours & Co

- Specialty Enzymes

Top Strategies Used by Key Market Participants

Key players in the MEA carbohydrase market primarily employ strategic partnerships and localized distribution networks to enhance their market reach and customer engagement. Companies are increasingly investing in technical support centers to provide customized solutions and training to local manufacturers, ensuring optimal enzyme usage. Product innovation focused on heat stability and cost efficiency is another major strategy catering to the specific climatic and economic conditions of the region. Additionally, firms are engaging in sustainability initiatives and educational campaigns to promote the adoption of green enzymatic processes over traditional chemical methods. Mergers and acquisitions are also utilized to consolidate market presence and acquire local expertise. These strategies collectively aim to build long-term relationships with customers and navigate the complex regulatory and logistical landscape of the Middle East and Africa.

Leading Players in the Market

- Novozymes A S is a global leader in biosolutions with a strong presence in the MEA region through strategic partnerships and distribution networks. The company focuses on providing innovative enzyme solutions for food, feed, and technical industries. Novozymes actively collaborates with local manufacturers to customize carbohydrase products that meet specific regional requirements, such as heat stability for baking in hot climates. Their recent initiatives include launching digital platforms to provide technical support and optimization services to customers in the Middle East and Africa. By investing in local training programs and sustainability projects,s Novozymes strengthens its brand loyalty and market penetration. The company’s commitment to reducing environmental impact aligns with regional regulatory trends, making it a preferred partner for industries seeking green solutions.

- DuPont de Nemours Inc operates extensively in the MEA carbohydrase market, offering a wide portfolio of enzymes for various industrial applications. The company leverages its global research and development capabilities to introduce high-performance carbohydrases that enhance process efficiency and product quality. DuPont has been strengthening its position by expanding its distribution channels and forming alliances with local distributors in key markets like Saudi Arabia and South Africa. Recent actions include the introduction of next-generation amylases that offer improved stability and activity under diverse processing conditions. The company also engages in educational campaigns to raise awareness about the benefits of enzymatic solutions among small and medium enterprises in the region.

- AB Enzymes GmbH is a specialized enzyme manufacturer that has gained significant traction in the MEA market by focusing on niche applications and customer-centric solutions. The company provides high-quality carbohydrases for the food feed, and detergent industries. AB Enzymes has been enhancing its market position by establishing technical service centers in the region to provide immediate support and customization services. Recent strategies include partnering with local ingredient suppliers to create integrated solutions for bakeries and feed mills. The company emphasizes sustainability and efficiency, helping customers reduce production costs and environmental footprints. Its agile approach and focus on innovation allow it to compete effectively against larger multinational corporations in the MEA region.

MARKET SEGMENTATION

This research report on the mea carbohydrase market has been segmented and sub-segmented into the following categories.

By Type

- Cellulase

- Amylase

By Application

- Animal feed

- Pharmacy

- Food & beverages

- Other applications

By Source

- Animals

- Microorganisms

- Plants

- Others

By Region

- KSA

- UAE

- Israel

- The rest of the GCC countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- Rest of MEA

Frequently Asked Questions

1. What is driving the growth of the Middle East and Africa carbohydrase market?

Growth is driven by increasing demand for enzyme-based food processing, expanding livestock production, and rising adoption of industrial biotechnology.

2. Which application segment dominates the market?

The animal feed segment holds a significant market share due to the use of carbohydrase enzymes to improve feed digestibility and animal performance.

3. What are the major types of carbohydrase enzymes?

Amylase, cellulase, xylanase, pectinase, and lactase are among the most widely used carbohydrase enzymes.

4. How are carbohydrase enzymes used in the food industry?

They improve texture, enhance processing efficiency, increase product yield, and support the production of bakery products, dairy products, juices, and beverages.

5. What factors are boosting the use of carbohydrase in animal feed?

Increasing demand for high-quality meat and dairy products and the need to improve feed efficiency are driving enzyme adoption.

6. What challenges does the market face?

High production costs, limited awareness in some regions, and stringent regulatory requirements are key challenges.

7. How is biotechnology influencing the market?

Advancements in enzyme engineering and fermentation technologies are improving enzyme efficiency, stability, and cost-effectiveness.

8. Which end-use industry is expected to grow the fastest?

The food and beverage industry is expected to witness strong growth due to increasing demand for processed and convenience foods.

9. What trends are shaping the Middle East and Africa carbohydrase market?

Growing demand for clean-label products, sustainable enzyme solutions, and the expansion of industrial biotechnology are key market trends.

10. What is the future outlook for the Middle East and Africa carbohydrase market?

The market is expected to grow steadily, supported by rising industrialization, increasing food production, advancements in biotechnology, and expanding applications across multiple industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com