Global Medical Tourism Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Orthopedic Treatment, Cardiovascular Treatment, Dental Treatment, Fertility Treatment, Cosmetic Treatment, Neurological Treatment and Cancer Treatment), Service Provider (Public and Private), and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis from 2026 to 2034

Market Size, 2025

$55.85 BnMarket Estimate, 2026

$66.35 BnMarket Forecast, 2034

$263.45 BnCAGR, 2026–2034

18.8%Global Medical Tourism Market Summary

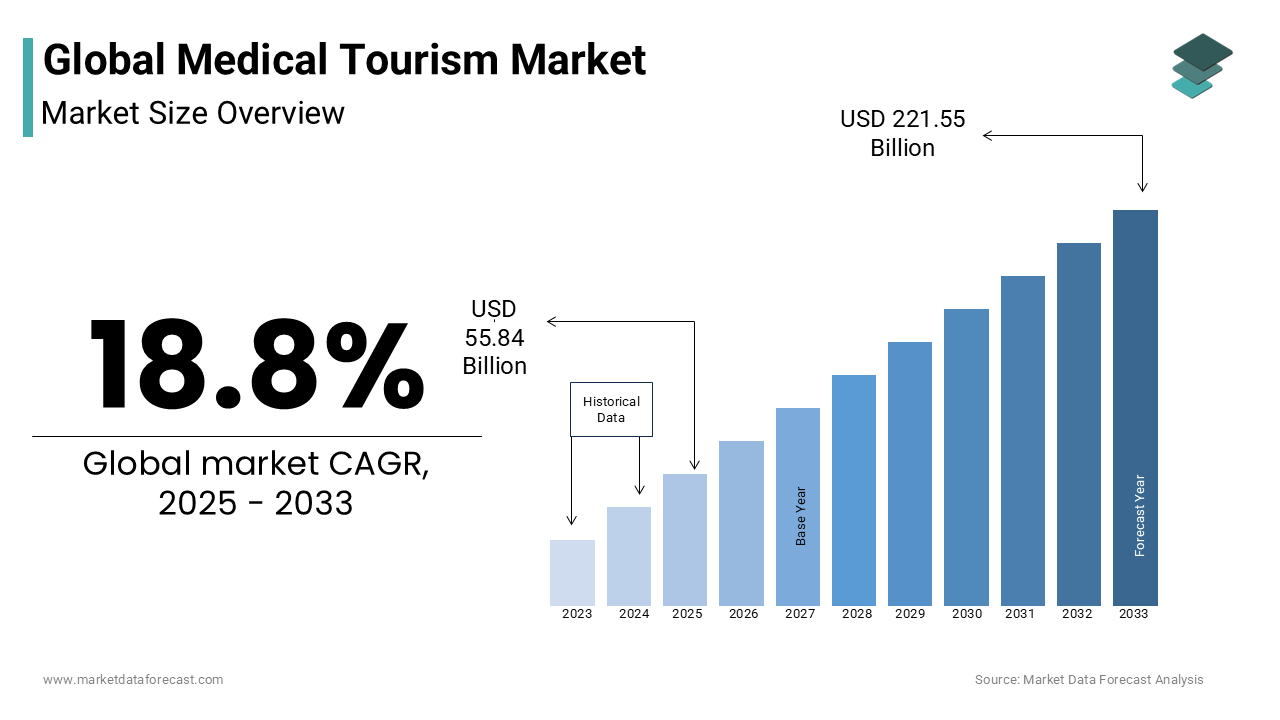

The global medical tourism market size was valued at USD 55.85 billion in 2025 and is expected to reach USD 66.35 billion in 2026 and surge to USD 263.45 billion by 2034, growing at a robust CAGR of 18.8% between 2026 and 2034. Growth is being driven by increasing healthcare costs in developed countries, rising demand for advanced yet affordable treatments abroad, and improvements in healthcare infrastructure and accreditation in emerging destinations.

Medical tourists often seek treatments such as cancer therapy, cosmetic surgery, orthopedics, fertility care, and cardiology in countries offering high-quality care at lower costs. Private hospitals and specialty clinics are the primary service providers driving the market, offering premium services with shorter wait times and internationally certified facilities.

Key Market Trends

- Growing preference for cross-border travel for cost-effective medical care.

- Rising demand for treatments such as cancer therapy, orthopedics, cardiology, fertility care, and cosmetic surgery.

- Increasing investments in internationally certified hospitals and specialty clinics.

- Shorter waiting times and premium services are offered by private healthcare providers.

Segmental Insights

- Based on treatment type, the cancer treatment segment emerged as the leading segment in the global medical tourism market in 2024.

- Based on service providers, private hospitals dominated the market in 2024, supported by international certifications, advanced medical technologies, and premium patient care offerings.

Regional Insights

- North America stood as the dominant regional market in 2024, capturing the largest share due to high outbound patient flows seeking affordable treatment abroad.

- Asia-Pacific is projected to be the fastest-growing regional market during the forecast period, with a surge in medical hubs such as India, Thailand, and Singapore, offering cost-effective, high-quality healthcare.

- Europe accounted for a substantial share in 2024, supported by strong infrastructure and rising inbound flows from neighboring regions.

- Latin America shows promising growth, particularly in Mexico, Costa Rica, and Brazil, which are gaining traction as affordable healthcare destinations.

- Middle East & Africa are demonstrating moderate growth, with countries like the UAE and South Africa investing in healthcare tourism to attract international patients.

Competitive Landscape

Key players in the medical tourism market include Apollo Hospitals, Fortis Healthcare, Bumrungrad International, Raffles Medical, Min-Sheng, KPJ Healthcare, Bangkok Hospital, Samitivej, Prince Court Medical, and Asian Heart Institute. These players are focusing on international accreditations, advanced infrastructure, and strategic collaborations to strengthen their position in the global market

Global Medical Tourism Market Size

As per our recent report, the global medical tourism market size is forecasted to be worth USD 263.25 billion by 2034 from USD 66.35 billion in 2026, growing at a CAGR of 18.8% between 2026 and 2034. The global medical tourism market was valued at USD 55.85 billion in 2025.

To learn about the report, ask for a sample copy of the report

Global Medical Tourism Market Overview

The Medical Tourism is the cross-border movement of individuals seeking medical, surgical, or wellness interventions in destinations outside their home countries, which is often driven by cost efficiency, reduced waiting times, access to advanced technologies, or procedures unavailable domestically. This phenomenon extends beyond traditional healthcare delivery, integrating travel logistics, hospitality, and post-treatment recovery in a seamless patient journey. Unlike conventional healthcare systems constrained by geographic and systemic limitations, medical tourism thrives on global disparities in healthcare affordability and capacity.

MARKET DRIVERS

Escalating Healthcare Costs in Developed Economies

The unsustainable escalation of healthcare expenditures in high-income nations is major factor propelling the growth of the Medical Tourism Market. This staggering disparity incentivizes patients to seek equivalent quality care abroad, where Joint Commission International (JCI)-accredited hospitals deliver outcomes comparable to those in Western facilities. For example, India performs over 500,000 cardiac surgeries annually, with survival rates for CABG procedures aligning with global benchmarks 96.8% at leading hospitals like Apollo and Fortis, according to the Indian Journal of Cardiovascular Disease Research. Similarly, diagnostic imaging costs in Australia and Canada are up to five times higher than in Malaysia or Singapore, prompting cross-Pacific medical travel. The Commonwealth Fund reported in 2022 that nearly 18% of Americans have considered medical treatment abroad due to insurance exclusions or high out-of-pocket expenses.

Proliferation of Accredited Healthcare Infrastructure in Emerging Destinations

The rapid development and international accreditation of healthcare facilities in emerging economies are additionally boosting the growth of the Medical Tourism Market. As of 2023, India boasts 72 Joint Commission International (JCI)-accredited hospitals, while Thailand maintains 58, and Turkey ranks among the top five globally with 47 accredited institutions, according to the JCI’s official registry. This formal recognition signals adherence to rigorous patient safety, clinical governance, and service delivery standards, effectively mitigating perceived risks associated with cross-border care. For instance, Bumrungrad International Hospital in Bangkok treats over 1.1 million international patients annually, with clinical outcomes for oncology treatments matching those reported in U.S. National Cancer Institute databases. Similarly, South Korea’s Gangnam healthcare district in Seoul has emerged as a hub for precision medicine and regenerative therapies, supported by the country’s investment of USD 3.2 billion in biotechnology and digital health infrastructure between 2020 and 2023, as disclosed by the Korea Health Industry Development Institute. This institutional advancement enables emerging destinations to offer cutting-edge treatments such as proton therapy, robotic surgery, and stem cell interventions at competitive price points. Malaysia’s Penang has positioned itself as a regional leader in orthopedic and spinal surgery, with Gleneagles Hospital achieving a 98.4% patient satisfaction rate among international clients in 2022, as per the Malaysian Healthcare Travel Council. Additionally, digital integration in hospitals across the UAE and Jordan allows real-time teleconsultations, pre-arrival diagnostics, and blockchain-secured medical records by enhancing patient confidence

MARKET RESTRAINTS

Regulatory Fragmentation and Legal Vulnerability in Cross-Border Care

The absence of harmonized international regulations governing patient rights, medical liability, and malpractice redressal is limiting the growth of the Medical Tourism Market. For example, a 2022 study published in the Journal of Patient Safety revealed that 17% of medical tourists who experienced adverse outcomes post-surgery abroad were unable to file legal claims due to conflicting liability laws between their home and host countries. In cases involving surgical errors or post-operative infections, patients from the European Union may find themselves excluded from compensation mechanisms under the EU Cross-Border Healthcare Directive if the procedure was privately arranged without prior authorization. The lack of an international patient rights charter exacerbates vulnerability, particularly for elderly travelers or those undergoing complex interventions such as organ transplants or cosmetic surgeries, where outcomes are less predictable. These legal and regulatory gaps erode consumer confidence and deter institutional insurance coverage for overseas treatments.

Post-Treatment Follow-Up and Continuity of Care Deficiencies

The limitation undermining the efficacy and safety of medical tourism is the discontinuity in post-operative or post-treatment care upon patients’ return to their home countries. Effective recovery from procedures such as bariatric surgery, joint replacement, or cancer therapy requires coordinated follow-up, including wound monitoring, rehabilitation, and medication management. However, a 2023 study by the World Health Organization found that 41% of medical tourists do not receive standardized discharge summaries or treatment records in a format compatible with their domestic healthcare providers, which is leading to fragmented care pathways. This disconnect increases the risk of complications; the same WHO study noted that patients returning from abroad after major surgery face a 1.8 times higher likelihood of hospitalization within 30 days compared to those treated domestically. Additionally, language barriers and time zone differences hinder telemedicine-based follow-ups, particularly for elderly patients.

MARKET OPPORTUNITIES

Expansion of Digital Health Integration and Virtual Care Pathways

The integration of digital health technologies with medical tourism is an emerging opportunity to enhance patient engagement, safety, and care coordination across borders, which is driving the growth of the Medical Tourism Market. Telemedicine platforms now enable pre-travel consultations, remote diagnostics, and post-treatment monitoring, effectively bridging geographical and temporal gaps. As of 2023, over 60% of JCI-accredited hospitals in Asia and the Middle East offer multilingual virtual care services, allowing patients from North America and Europe to consult with specialists in India, Thailand, or Turkey before committing to travel, as reported by the International Medical Travel Journal. For instance, Apollo Hospitals’ “e-Consult” platform facilitated over 220,000 international teleconsultations in 2022, with a 92% conversion rate to in-person treatment, demonstrating the efficacy of digital triage. Furthermore, blockchain-based medical record systems are being piloted in Singapore and Dubai to ensure secure, interoperable health data exchange, reducing documentation delays and improving diagnostic accuracy. According to the WHO’s 2023 Digital Health Global Strategy, countries investing in cross-border digital health infrastructure have seen a 35% increase in medical tourist retention and satisfaction. These advancements not only mitigate risks associated with fragmented care but also position medical tourism as a seamless, technology-enabled continuum rather than a one-off transaction.

Strategic Government Investment in Healthcare Tourism Corridors

National governments in emerging economies are increasingly institutionalizing medical tourism through dedicated economic zones, public-private partnerships, and targeted visa facilitation by creating structured pathways for sustainable growth. The UAE launched the “Health Tourism Strategy 2025,” which aims to attract 1.2 million international patients annually by enhancing infrastructure in Dubai Health Experience (DXH) centers and offering bundled packages that integrate treatment with luxury recovery stays. India’s National Medical and Wellness Tourism Policy, introduced in 2022, includes tax incentives for hospitals achieving international accreditation and fast-track immigration lanes at major airports for medical travelers. As per data from the Federation of Indian Chambers of Commerce and Industry, these initiatives contributed to a 38% year-on-year increase in medical visas issued in 2023. According to the Thailand Board of Investment, the EEC healthcare zone is projected to generate 50,000 jobs and serve 1.5 million international patients by 2027.

MARKET CHALLENGES

Geopolitical and Macroeconomic Volatility Affecting Travel Feasibility

The inherently susceptible to geopolitical tensions, currency fluctuations, and macroeconomic instability, all of which directly influence travel feasibility and patient confidence is impeding the growth of the Medical Tourism Market. For example, the depreciation of the Turkish lira by 85% against the U.S. dollar between 2018 and 2023, as recorded by the Central Bank of the Republic of Turkey, initially made treatments more affordable but simultaneously eroded hospital revenues and compromised service quality due to rising import costs for medical devices and pharmaceuticals. Similarly, political instability in regions such as Eastern Europe and the Middle East deters medical travelers; Ukraine’s medical tourism sector, which attracted over 80,000 patients annually before 2022, collapsed following the Russian invasion, according to the Ukrainian Ministry of Health. Currency volatility also affects patient affordability; a 2023 report by the International Monetary Fund noted that exchange rate fluctuations exceeding 15% year-on-year in countries like Argentina and Egypt disrupted medical travel flows by altering cost projections mid-treatment.

Ethical and Equity Concerns in Domestic Healthcare Resource Allocation

The potential diversion of high-quality healthcare resources from local populations to serve affluent international patients is limiting the growth of the Medical Tourism Market. Similarly, in India, the proliferation of luxury private hospitals catering to international patients has coincided with a physician density of only 0.8 per 1,000 people in rural areas, far below the WHO-recommended 1:1,000 ratio, as per India’s National Health Systems Resource Centre. This dual-tier system risks creating medical enclaves where expatriate patients receive priority access to specialists, advanced diagnostics, and shorter wait times, while indigenous populations face prolonged delays. A 2022 study in The Lancet Global Health revealed that in Jordan, 45% of radiologists and 38% of cardiac surgeons in Amman work primarily in private, medical-tourism-focused hospitals, skewing workforce distribution. Moreover, the prioritization of profitable procedures such as cosmetic surgery and elective orthopedics over essential maternal and infectious disease care distorts public health priorities. These imbalances raise concerns about healthcare commodification and social justice, potentially triggering regulatory backlash or public resistance. Sustainable medical tourism models must therefore integrate equity safeguards, ensuring that global demand does not compromise national health objectives.

SEGMENTAL ANALYSIS

By Treatment Type Insights

The dental treatment segment was the largest and held 32.2% in the global medical tourism market share in 2024 with a confluence of affordability, minimal procedural complexity, and high consumer demand for aesthetic and restorative interventions. This price arbitrage is a primary magnet for patients from North America and Western Europe, where dental care is often excluded from public insurance schemes. For example, nearly 76% of dental procedures in Canada are paid out-of-pocket, prompting over 120,000 Canadians to seek cross-border dental care annually, as reported by the Canadian Dental Association. Countries such as Croatia and Turkey have institutionalized dental tourism, with over 200 private clinics in Zagreb alone catering exclusively to foreign patients, according to the Croatian Chamber of Dentists. These clinics frequently employ English-speaking specialists trained in EU-accredited institutions, ensuring both linguistic and clinical compatibility. The integration of digital smile design (DSD) and CAD/CAM technology in destinations like Costa Rica has further elevated treatment precision, with success rates for dental implants exceeding 95% over five years, matching outcomes in the U.S., as per data from the Journal of Clinical Periodontology.

Ther fertility treatment segment is likely to grow with an expected CAGR of 14.8% from 2025 to 2033 with the tightening legal and financial constraints in high-income countries, coupled with superior success rates and broader treatment accessibility abroad. The average cost of an IVF cycle in the UK is USD 8,500, while in Greece, it is USD 4,200 with comparable live birth rates of 38% per cycle, according to Greece’s National Assisted Reproduction Registry. Additionally, countries like Georgia and Cyprus have emerged as fertility hubs due to permissive legal frameworks by allowing treatments for single women, same-sex couples, and surrogacy options unavailable in nations such as Italy and France. The American Society for Reproductive Medicine reported in 2023 that over 15% of U.S. fertility patients traveled internationally due to prohibitive costs and legal limitations, with the average domestic IVF cycle costing USD 12,000, excluding medications. Furthermore, destinations such as Spain perform over 90,000 assisted reproductive technology (ART) cycles annually, supported by a robust regulatory environment and high clinic density, as noted by the Spanish Fertility Society.

By Service Provider Insights

The private service segment was accounted in holding a prominent share of the global medical tourism market in 2024 with their strategic focus on international accreditation, patient-centric infrastructure, and operational agility, which public systems often lack due to bureaucratic inertia and funding constraints. Private facilities invest heavily in luxury amenities, multilingual staff, and integrated travel services, creating a seamless experience that aligns with the expectations of international patients. These hospitals often operate on a for-profit model that incentivizes efficiency and innovation, enabling faster adoption of robotic surgery, digital diagnostics, and AI-driven treatment planning. Additionally, private providers are more likely to engage in international marketing, forming partnerships with medical facilitators and insurance brokers in source countries. The Federation of Indian Chambers of Commerce and Industry noted in 2023 that private hospitals in India accounted for 93% of all medical tourist admissions, driven by their ability to offer bundled pricing, shorter waiting times, and personalized care pathways.

The public service providers segment is likely to witness a CAGR of 9.4% from 2025 to 2033 owing to the government-led initiatives to leverage publicly funded hospitals as instruments of health diplomacy and economic development in countries with high-quality, underutilized healthcare capacity. These institutions perform over 200,000 procedures annually for foreign patients, particularly in oncology and advanced diagnostics, with survival rates for early-stage liver cancer reaching 75% over five years, matching global benchmarks, according to the Korean Central Cancer Registry. Public hospitals in Spain and Germany are also expanding their international outreach, leveraging universal healthcare-trained specialists and cutting-edge research infrastructure to attract patients seeking evidence-based treatments.

REGIONAL ANALYSIS

Asia Pacific Medical Tourism Market Insights

Asia-Pacific was the top performer in the global medical tourism market by capturing 38.3% of the share in 2024. The region’s ascendancy is rooted in its unparalleled combination of cost efficiency, clinical excellence, and state-backed healthcare internationalization. Thailand, India, and Singapore serve as the primary engines of growth, collectively attracting over 6 million international patients annually. Thailand alone welcomed 1.5 million medical tourists in 2022, generating USD 5.6 billion in revenue, with Bumrungrad and Bangkok Hospital achieving JCI accreditation and survival rates for coronary interventions exceeding 97%, as reported by the Thai Ministry of Public Health. India’s medical tourism sector grew by 22% year-on-year in 2023, driven by high-volume procedures in cardiology and orthopedics, with costs up to 65% lower than in the U.S., according to the Confederation of Indian Industry. Singapore, though catering to a premium segment, excels in precision oncology and neurology, with the National University Hospital achieving a 92% five-year survival rate for glioblastoma patients, as per Singapore’s Ministry of Health.

Europe Medical Tourism Market Insights

Europe medical tourism market held 26.3% of the share in 2024. The continent’s appeal lies in its stringent regulatory frameworks, high clinical standards, and growing specialization in niche treatments such as fertility, orthopedics, and cosmetic surgery. Countries like Germany, Hungary, and Spain have developed targeted medical tourism corridors, combining advanced care with cost advantages relative to North America. Germany treats over 400,000 international patients annually, particularly in oncology and cardiac surgery, with mortality rates for coronary bypass surgery at 1.8%, below the OECD average of 2.4%, as reported by the German Federal Statistical Office. Hungary dominates dental tourism in Europe, with over 700,000 foreign patients visiting Budapest annually for procedures averaging 60% less than in the UK, according to the Hungarian Dental Chamber. Spain has emerged as a leader in reproductive medicine, performing over 90,000 IVF cycles in 2022 with a live birth rate of 38%, as per the Spanish Fertility Society. The EU Cross-Border Healthcare Directive has further facilitated patient mobility, enabling reimbursement for treatments in other member states under specific conditions.

North America Medical Tourism Market Insights

North America medical tourism market growth is substantially to grow with a prominent CAGR in the next coming years. MD Anderson Cancer Center in Texas treated over 12,000 international patients in 2022, with a five-year survival rate of 78% for early-stage lung cancer, surpassing the global average, as reported by the American Cancer Society. Similarly, the Mayo Clinic welcomed over 9,000 patients from 140 countries, offering advanced diagnostics and personalized medicine protocols. Canada, though limited by public healthcare wait times, draws patients from the Caribbean and Africa for MRI and CT scans, where average wait times in the public system exceed 12 weeks, compared to under 72 hours in private imaging centers, according to the Canadian Institute for Health Information. The U.S. also benefits from FDA-approved therapies unavailable elsewhere, such as CAR-T cell treatments, which command premium pricing but attract patients requiring last-line interventions. However, the high cost of care remains a deterrent for volume-based medical tourism.

Latin America Medical Tourism Market Insights

Latin America medical tourism market growth is emerging swiftly with prominent opportunities in the next coming years. Mexico alone receives over 800,000 U.S. citizens each year for dental, cosmetic, and bariatric procedures, with savings averaging 50–70% compared to domestic costs, according to the Mexican Ministry of Tourism. The city of Tijuana has developed a medical corridor along the U.S.-Mexico border, where accredited hospitals perform over 150,000 procedures annually, including robotic surgeries and stem cell therapies. Costa Rica, renowned for its eco-tourism, has seamlessly integrated wellness and medical care, with over 60% of its private hospitals JCI-accredited and a 95% success rate in dental implant procedures, as reported by the Costa Rican College of Dentists. Colombia has gained recognition for high-quality plastic surgery, with Bogotá and Medellín hosting over 100,000 cosmetic surgery patients in 2022, supported by a pool of surgeons trained in the U.S. and Europe, according to the Colombian Society of Plastic Surgery. The region’s geographic proximity allows for short travel times and easier post-operative follow-ups, while Spanish-speaking medical staff facilitate communication for Latin American patients.

Middle East and Africa Medical Tourism Market Insights

The Middle East and Africa medical tourism market with the Gulf Cooperation Council (GCC) countries is driving regional growth through strategic healthcare investments and medical city developments, as outlined in the Gulf Health Council’s 2023 report. The UAE, Saudi Arabia, and Jordan are at the forefront, transforming into regional healthcare hubs. The UAE generated USD 1.1 billion in medical tourism revenue in 2022, with Dubai Health Experience (DXH) attracting over 600,000 patients from Africa, South Asia, and the Levant, according to Dubai Health Authority. Saudi Arabia’s Vision 2030 includes a USD 40 billion investment in healthcare infrastructure, aiming to reduce medical travel outflows and attract 1.5 million inbound patients annually by 2030.

KEY MARKET PARTICIPANTS AND COMPETITIVE LANDSCAPE

Companies playing a leading role in the worldwide medical tourism market profiled in this report are Min-Sheng General Hospital, Apollo Hospitals Enterprise Limited, Samitivej Sukhumvit, Fortis Healthcare Ltd, Asian Heart Institute, Prince Court Medical Center, Bangkok Hospital Medical Center, KPJ Healthcare Berhad, Raffles Medical Group and Bumrungrad International Hospital.

The competitive landscape of the medical tourism market is defined by a dynamic interplay of clinical excellence, service innovation, and strategic positioning. Unlike traditional healthcare markets, competition here extends beyond medical outcomes to encompass the entire patient journey—from initial inquiry to post-treatment recovery. Hospitals and healthcare groups vie not only on cost and quality but also on accessibility, cultural adaptability, and technological integration. The absence of a dominant global player has led to regional specialization, with certain countries establishing reputations for specific treatments, such as dental care in Hungary, fertility in Spain, or cardiac surgery in India. Providers differentiate themselves through branding, international accreditations, and patient experience design, often emulating luxury service models from the hospitality industry. The rise of digital health platforms has intensified competition, enabling patients to compare providers, read reviews, and consult specialists remotely before making decisions. Additionally, government-backed initiatives in countries like Thailand, Turkey, and the UAE have institutionalized medical tourism, creating national brands that compete on a global scale.

Top Players in the Medical Tourism Market

Bumrungrad International Hospital (Thailand)

Bumrungrad International Hospital has emerged as a global benchmark in medical tourism, renowned for its patient-centric care model and seamless integration of healthcare and hospitality. Located in Bangkok, the hospital caters to a diverse international clientele, offering a transparent pricing system, multilingual support, and end-to-end travel coordination. Its commitment to international accreditation and clinical excellence has positioned it as a preferred destination for complex procedures ranging from cardiac interventions to advanced diagnostics.

Apollo Hospitals (India)

Apollo Hospitals pioneered the concept of organized private healthcare in India and has since become a cornerstone of the country’s medical tourism industry. The institution combines cutting-edge medical technology with a vast network of specialty centers, delivering high-quality treatments in oncology, cardiology, and organ transplantation. Apollo’s emphasis on ethical practice, clinical innovation, and digital health integration has earned it global recognition. The hospital group actively collaborates with international insurers and facilitators by ensuring smooth patient journeys. Its reputation for clinical rigor and compassionate care continues to attract patients from across Africa, the Middle East, and Southeast Asia.

Mayo Clinic (United States)

The Mayo Clinic stands as a symbol of medical authority and research-driven care, drawing patients globally for rare, complex, and second-opinion consultations. While not traditionally classified as a medical tourism provider, its reputation for diagnostic precision and multidisciplinary treatment planning makes it a top destination for high-acuity cases. The clinic offers dedicated international services, including visa assistance, translation, and concierge coordination by enabling seamless access for global patients. Its influence extends beyond treatment, shaping global standards in patient safety, clinical protocols, and personalized medicine, thereby setting a gold standard in the international healthcare landscape.

Top Strategies Used by Key Market Participants

One of the most impactful strategies employed by leading players is the integration of healthcare with hospitality to create a holistic patient experience. Hospitals are increasingly designing facilities with luxury accommodations, private suites, and recovery-centric environments that mirror high-end wellness resorts. This approach not only alleviates the stress associated with medical travel but also appeals to patients seeking dignity, comfort, and privacy during treatment.

Another strategy is the establishment of international partnerships with insurance providers, medical facilitators, and travel agencies. These alliances enable seamless coordination of pre-travel consultations, visa processing, and post-treatment follow-ups, reducing logistical friction for patients.

Another strategy involves the pursuit of global accreditations such as Joint Commission International (JCI) and TEMOS certification. These credentials serve as trust signals, assuring patients of adherence to international standards in safety, hygiene, and clinical outcomes. Accredited institutions gain a competitive edge in marketing, as patients and referring physicians rely on these validations when making cross-border care decisions. This institutional validation strengthens brand equity and fosters long-term confidence in the provider’s capabilities.

Global Medical Tourism Market News

- In June 2023, Apollo Hospitals partnered with a leading European medical facilitator to offer bundled treatment and travel packages, which is streamlining access for patients from the Middle East and North Africa.

- In September 2024, Mayo Clinic expanded its international patient services by opening a dedicated coordination center in Dubai that aimed at improving outreach and follow-up for patients from Asia and Africa.

- In January 2023, Fortis Healthcare entered a strategic collaboration with a global health insurance network to enable direct billing and coverage for cross-border treatments by reducing financial barriers for international patients.

- In May 2024, Mediclinic Middle East launched a digital health passport initiative in partnership with a blockchain technology firm by ensuring secure and interoperable medical records for inbound medical travelers.

Global Medical Tourism Market Report Scope

| Metric | Value |

|---|---|

| Base Year | 2025 |

| Market Size Available | 2025 to 2034 |

| Forecast Period | 2026 to 2034 |

| Market Size in 2024 | USD 55.85 Billion |

| Projected Market Size in 2025 | USD 66.35 Billion |

| Projected Market Size by 2033 | USD 263.25 Billion |

| Projected CAGR | 18.8% |

| Quantitative Units | Market Size in USD Billion and CAGR from 2026 to 2034 |

| Various Analyses Included | Regional & Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE; Porter's Five Forces; Competitive Landscape; Investment Opportunities |

| Segments Covered | Treatment Type, Service Provider and Region |

| Key Market Players Covered | Min-Sheng General Hospital, Apollo Hospitals Enterprise Limited, Samitivej Sukhumvit, Fortis Healthcare Ltd, Asian Heart Institute, Prince Court Medical Center, Bangkok Hospital Medical Center, KPJ Healthcare Berhad, Raffles Medical Group and Bumrungrad International Hospital |

| Regions Analyzed | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | U.S, Canada, Mexico, UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Brazil, Argentina, Chile, KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan and Other Countries |

| Report Format | PDF, Excel, PPT, BI |

| Customization | Report customization as per your requirements concerning countries, region and segmentation. |

MARKET SEGMENTATION

This research report on the global medical tourism market has been segmented and sub-segmented based on the treatment type and region.

By Treatment Type

- Orthopedic Treatment

- Cardiovascular Treatment

- Dental Treatment

- Fertility Treatment

- Cosmetic Treatment

- Neurological Treatment

- Cancer Treatment

By Service Provider

- Public

- Private

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the current size of the global medical tourism market?

The global medical tourism market size is forecasted to be worth USD 221.55 billion by 2033 from USD 55.84 billion in 2025, growing at a CAGR of 18.8% between 2025 and 2033.

What factors are driving growth in the medical tourism market?

Key growth drivers include cost savings on treatments, long waiting times in domestic healthcare systems, expanding medical infrastructure in emerging markets, and increased cross-border health insurance coverage.

Which regions are leading the medical tourism market globally?

Asia-Pacific dominates the market due to advanced medical facilities and affordability in countries like India, Thailand, and Malaysia. Latin America and the Middle East are also rapidly emerging as preferred destinations.

What are the major treatment segments in the medical tourism market?

The market is segmented by procedures such as cosmetic surgery, orthopedic surgery, cardiac treatments, fertility/IVF, dental care, and wellness therapies, each with varying growth rates and margins.

Who are the key players operating in the medical tourism market?

Prominent players include Apollo Hospitals (India), Bumrungrad International (Thailand), Gleneagles Global (Malaysia), KPJ Healthcare, and facilitators like Healthbase and MedRetreat, who connect international patients with accredited providers.

What is the expected CAGR of the medical tourism market from 2025 to 2033?

The market is projected to grow at a CAGR of 18.8% during the forecast period, supported by digital health adoption, increased government promotion, and rising demand for elective surgeries.

What role do digital platforms play in the medical tourism market?

Digital health platforms facilitate remote consultations, price transparency, treatment package comparison, and post-operative care coordination, making medical tourism more accessible and scalable.

How are governments influencing the medical tourism market?

Governments in countries like Thailand, India, and Mexico actively promote medical tourism through policy support, infrastructure investment, and international accreditation programs to attract global patients.

What are the key challenges facing the medical tourism market?

Major challenges include regulatory inconsistencies, medical malpractice risk in cross-border care, limited insurance portability, and post-treatment care difficulties in the patient’s home country.

What are the future trends shaping the medical tourism market?

Key trends include AI-driven patient matchmaking, growth of medical wellness tourism, blockchain-based health records, customized treatment packages, and increased investments in smart hospitals and concierge healthcare for international patients.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com