Global Microgrid Controller Market Size, Share, Trends, & Growth Forecast Report, Segmented By Connectivity (Grid Connected, Off-Grid/Remote/Islanded), Offering (Hardware, Software and Services), Vertical (Government, Utilities, Commercial, Industrial, Educational Institutes, Military And Defense, Healthcare and Others) & Region, Industry Forecast From 2025 to 2033

Global Microgrid Controller Market Size

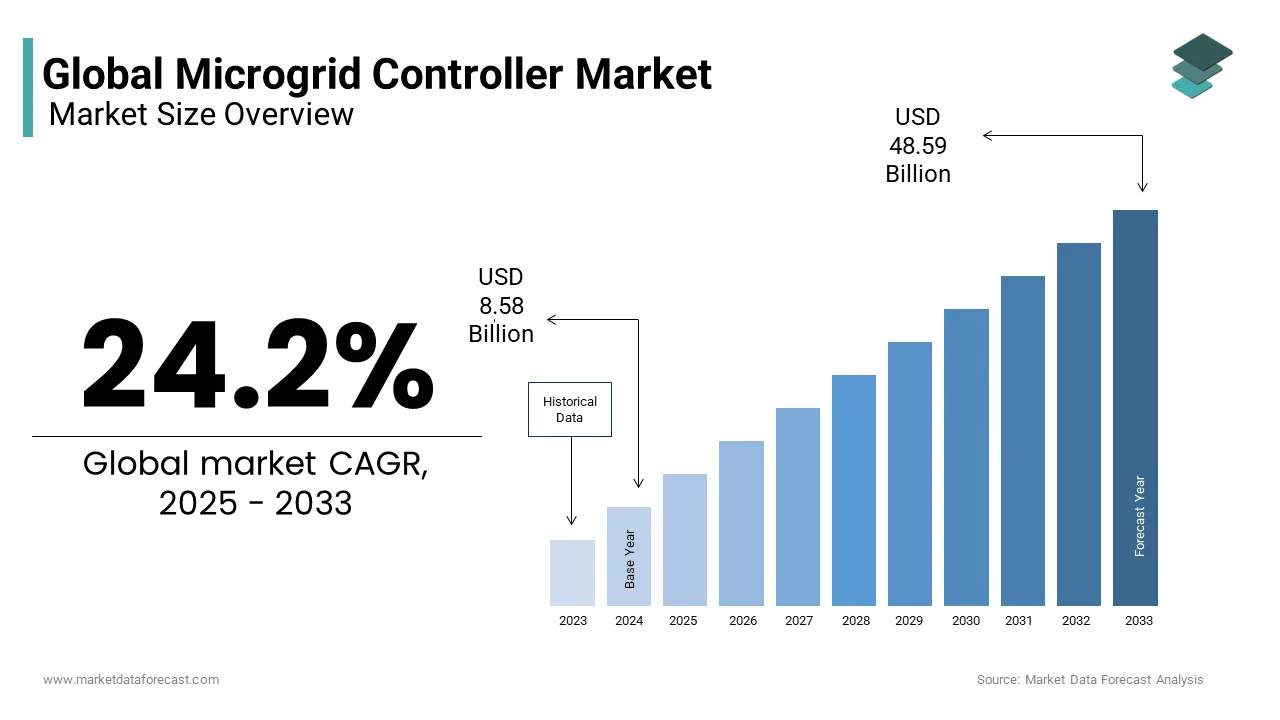

The size of the global microgrid controller market was valued at USD 6.91 billion in 2024 and is anticipated to reach USD 8.58 billion in 2025 to USD 48.59 billion by 2033, expected to growing at a CAGR of 24.2% from 2025 to 2033.

A microgrid controller is an intelligent hardware and software system that orchestrates the real-time operation of distributed energy resources, including solar photovoltaics, battery storage, diesel generators, and demand side loads, within a localized grid architecture. It ensures seamless transition between grid-connected and islanded modes, maintains voltage and frequency stability, optimizes energy dispatch for cost or carbon reduction, and enables participation in ancillary service markets. As per studies, a growing number of community and industrial microgrids are being established across North America, with advanced controllers essential for managing power and ensuring grid resilience. Moreover, the use of microgrids is expanding in remote and underserved global regions to improve energy access and reliability, with controllers providing a crucial management function, according to research. In military applications, the U.S. Army Corps of Engineers and other defense agencies are increasingly focused on requiring highly secure and autonomous microgrid control systems for forward operating bases to ensure reliable operation under challenging conditions. Standards such as IEEE 2030.7 and IEC 61850 govern interoperability, while artificial intelligence and digital twin technologies are increasingly embedded to enable predictive optimization. Far from a passive switchgear component, the microgrid controller is the decision-making core of decentralized, adaptive, and intelligent energy infrastructure.

MARKET DRIVERS

Escalating climate-induced grid disruptions are compelling critical infrastructure operators to deploy autonomous microgrid controllers for operational continuity.

The escalating frequency and severity of extreme weather events have critically compromised grid reliability, which contributes to the growth of the microgrid controller market. This compels essential facilities like hospitals, data centers, military bases, and water utilities to implement microgrids with intelligent, autonomous controls for power management. Weather-related power outages are increasing in frequency and duration, making the resilience of critical facilities a growing concern. In response, federal programs and incentives are increasingly encouraging the adoption of microgrids in healthcare facilities to enhance power resilience. Following significant grid emergencies, there has been a notable increase in the installation of microgrids in industrial areas to mitigate financial losses from downtime. Military adoption is equally urgent. The U.S. military is rapidly adopting autonomous microgrid systems to ensure continuous base operations and enhance energy security against various threats. These systems use real-time load prioritization and generator dispatch algorithms to maintain mission-critical functions without human intervention. The intensification of climate volatility necessitates the reclassification of microgrid controllers from optional enhancements to critical and mandatory resilience infrastructure.

Regulatory mandates for renewable integration and grid services are forcing utilities and developers to adopt advanced controller architectures.

Global decarbonization policies are compelling grid operators to integrate variable renewable sources at scale, which is among the key accelerators of the microgrid controller market. This requires microgrid controllers that can balance intermittency, provide frequency response, and comply with grid code requirements. European transmission system operators are increasingly requiring new power electronic-based interconnections, including microgrids, to provide grid stability services such as synthetic inertia and reactive power support due to the rising penetration of renewable energy sources. Regulatory bodies in regions like California are advancing requirements for distributed energy resources, including commercial-scale microgrids, to integrate with management systems for automated response to grid conditions and market signals. Rural electrification initiatives, such as those in India, are increasingly deploying standardized control systems within solar-hybrid microgrids to ensure reliable voltage stability during the integration of variable renewable inputs and traditional generation sources. Regulators in Australia are focusing on grid resilience, which includes the trend of commercial microgrids adopting advanced controllers with "black start" and islanding capabilities to operate autonomously and support system recovery. These regulatory drivers are not merely technical; they are contractual and financial, as non-compliance results in interconnection denial or penalty fees. Consequently, controller sophistication is no longer a differentiator but a baseline requirement for market entry.

MARKET RESTRAINTS

Lack of standardized communication protocols impedes interoperability and increases integration costs for multi-vendor systems.

Proprietary communication architectures prevent seamless integration of inverters, storage systems, and loads from different manufacturers, despite advances in control algorithms, which poses a major restraint to the microgrid controller market. As per various sources, incompatibilities between diverse controller software and third-party Distributed Energy Resource (DER) hardware present a significant integration challenge, often leading to project delays. The adoption of standardized protocols like IEC 61850 in commercial and industrial microgrids is hindered by the prevalence of legacy equipment and vendor-specific systems, contrasting with its greater traction in utility-scale projects. In addition, rural microgrid reliability, particularly with solar integration, is frequently challenged by communication vulnerabilities between inverters and control systems, especially during transient environmental conditions like variable cloud cover. Cybersecurity adds another layer of complexity. Many existing microgrid control systems continue to utilize non-encrypted legacy communication protocols, which creates significant cybersecurity vulnerabilities to various forms of cyberattacks. Microgrid deployment will be expensive, slow, and unreliable until universal plug-and-play standards are enforced and cybersecurity protocols are harmonized.

High capital and engineering costs deter adoption in price-sensitive markets despite long-term operational benefits.

High upfront expenses associated with microgrid controller technology make them inaccessible to smaller commercial operators and emerging economies, despite the potential for improved resilience and efficiency, thereby hindering the expansion of the microgrid controller market. According to research, engineering and integration costs for microgrid controllers represent a notable portion of total project capital expenditure, impacting the overall financial viability of mid-size industrial microgrid projects. Securing adequate financing remains a significant challenge for microgrid projects in Sub-Saharan Africa, often leading to delays and the use of less advanced control systems that limit operational efficiency and autonomous capabilities. Permitting and interconnection processes for microgrids, even in developed markets like California, are often complex and time-consuming, contributing substantially to project soft costs and extended development timelines. Vendor proprietary licensing models exacerbate the issue. Siemens and Schneider Electric charge annual subscription fees for advanced optimization modules, adding operational burden. Adoption will remain limited to high-value critical infrastructure and subsidized pilot programs until controller costs are modularized, standardized, and bundled into turnkey financing products.

MARKET OPPORTUNITIES

Expansion of vehicle-to-grid integration creates new revenue streams through bidirectional controller-managed energy exchange.

Aggregated EV batteries are beginning to function as large-scale and distributed energy assets as fleet numbers rise, which creates new opportunities for the growth of the microgrid controller market. Microgrid controllers can orchestrate these assets for grid balancing, peak shaving, and emergency backup, unlocking new monetization pathways. According to multiple studies, the global electric vehicle fleet continues to expand each year significantly, with a growing interest in vehicles capable of vehicle-to-grid (V2G) functionality across major markets. As per research, integrating electric vehicle fleets into microgrids via smart controllers offers substantial potential for generating revenue through services like frequency regulation and demand response programs. Fleet operators are taking notice. Regulatory tailwinds are accelerating adoption. As EV penetration grows and controller intelligence advances, parked vehicles will transform from energy consumers to grid-stabilizing assets.

Growth of mining and remote industrial operations in off-grid regions is driving demand for ruggedized, self-healing controller systems.

Resource extraction industries operating in geographically isolated areas are increasingly deploying microgrids with advanced controllers to reduce diesel dependency, and thereby generate fresh prospects for the expansion of the microgrid controller market. These controllers ensure uninterrupted operations nd comply with emissions regulations. As per sources, New mining projects in remote regions are increasingly requiring autonomous microgrids with ruggedized controllers designed to manage operations in challenging environmental conditions and without access to traditional electrical grids or reliable communication. Major mining companies are integrating hybrid power solutions that combine solar, battery storage, and gas generation to reduce reliance on diesel fuel and lower carbon emissions at their operations. State-owned mining companies in South America are implementing advanced microgrid control systems to ensure operational continuity and manage power reliability in harsh, high-altitude environments prone to extreme weather events. HecHenceicrogrid controllers are becoming mission essential enablers of sustainable, resilient, and cost-efficient remote industrial operations.

MARKET CHALLENGES

Cybersecurity vulnerabilities in legacy controller architectures expose critical infrastructure to escalating digital threats.

Many deployed microgrid controllers rely on outdated communication protocols and lack embedded encryption, making them susceptible to cyberattacks that can disrupt power delivery or manipulate energy markets. This forms a major challenge to the global microgrid controller market. Energy infrastructure operators are experiencing frequent attempted intrusions on control systems, with microgrids increasingly targeted because of their essential role in maintaining critical facility resilience. Attacks on microgrid controllers can cause immediate and significant operational failures, including uncontrolled load shedding and generator desynchronization, shortly after a penetration occurs. Legacy systems using Modbus TCP or unauthenticated DNP3 remain prevalent. Supply chain risks compound the threat. Next-generation controllers feature zero-trust architectures and blockchain command verification, but updating current systems with these technologies is both expensive and challenging. Microgrids will remain a systemic grid risk until cybersecurity is inherently designed into controller hardware and enforced through procurement mandates.

Complexity in real-time multi-objective optimization limits controller effectiveness in dynamic pricing and carbon-constrained environments.

Modern microgrid controllers must simultaneously balance cost minimization, carbon reduction, equipment degradation, and grid service participation, objectives that often conflict and require sophisticated multi-variable algorithms that most systems lack, thereby constraining the expansion of the microgrid controller market. Most commercial microgrid controllers rely on basic optimization methods, which result in inefficient operational decisions when responding to dynamic pricing or carbon intensity signals. The performance of certain microgrids in demand response programs is hindered because their controllers cannot dynamically adjust economic versus emissions priorities based on immediate grid conditions. Machine learning integration remains nascent. The consequence is operational inefficiency. The full economic and environmental benefits of microgrids cannot be realized until their control software can manage real-time, probabilistic, multi-criteria decision making.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 24.2% |

| Segments Covered | By Connectivity, Offering, Vertical, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | ABB Ltd, Eaton Corporation, Emerson Electric Co., General Electric Power, HOMER Energy LLC, Honeywell International Inc., Lockheed Martin Corporation, Pareto Energy Ltd, Power Analytics Corporation, Princeton Power Systems, S&C Electric Company, Schneider Electric SE, Schweitzer Engineering Laboratories, Inc., Siemens AG, Spirae LLC, and Others. |

SEGMENTAL ANALYSIS

By Connectivity Insights

The grid-connected microgrids segment led the microgrid controller market by accounting for a 63.3% share in 2024. The dominance of the grid-connected microgrids segment is driven by their ability to generate revenue through grid services while maintaining backup resilience. Unlike off-grid systems, grid-tied microgrids can participate in demand response, frequency regulation, and capacity markets, functions enabled by advanced controllers that synchronize with utility signals and autonomously adjust dispatch. According to research, grid-connected microgrids are increasingly enrolling in ancillary service programs, where they earn performance payments for their contributions. Microgrids with advanced, certified controllers effectively reduce peak grid stress by managing energy storage and critical loads. New, larger capacity microgrids are required to provide synthetic inertia, a function dependent on advanced, rapid-response algorithms in their control systems. Compensation programs for microgrid operators are in place to incentivize the provision of essential grid support services, such as voltage stability. Commercial and industrial users are primary adopters. This financial incentive, combined with regulatory compliance, ensures grid-connected systems remain the dominant architecture.

The off-grid and islanded microgrids segment is likely to experience the fastest CAGR of 19.3% from 2025 to 2033. The swift acceleration of this segment is propelled by resource extraction industries and rural electrification programs operating beyond utility infrastructure, where controller-managed autonomy is non-negotiable. A majority of new resource extraction projects are initiated in remote areas where reliable electrical grids are unavailable, as per studies. Advanced control systems are integrating multiple sources of generation, such as solar, battery storage, and traditional fuel, to optimize energy use and decrease reliance on a single fuel type. According to sources, significant investment is being directed toward off-grid industrial power systems, which require robust control technology that can withstand extreme environmental conditions. Funding is being provided for numerous localized power systems equipped with intelligent controllers capable of managing essential electrical loads when fuel supplies are low. Many hybrid solar and fuel-based microgrids are being standardized with automated sequencing controllers to ensure stable power output during sudden environmental changes. Off-grid controllers are emerging as mission-critical enablers of sustainable and resilient operations as the pressure from mineral demand and energy access requirements intensifies.

By Offering Insights

The hardware components segment was the largest in the microgrid controller market and captured a 54.3% share in 2024. The growth of the hardware components segment is attributable to the physical necessity of ruggedized, safety-certified equipment to interface with generators, inverters, and switchgear in real time. Regulatory frameworks mandate certified hardware. Federal facilities utilize microgrid controllers that comply with specific standards governing anti-islanding and ride-through functions. In one region, directives for low-voltage equipment necessitate hardware validation for electromagnetic compatibility and fault current interruption, features commonly integrated into major manufacturers' controller chassis. Industrial users prioritize durability. Military specifications are even stricter. Even as software capabilities advance, the physical layer remains irreplaceable; controllers must survive dust, moisture, voltage spikes, and cyber-physical attacks to ensure operational continuity. Hardware will continue to be the essential foundation for microgrid control until virtualization and edge computing are fully developed.

The software and services segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 22.1% over the forecast period, owing to the shift from rule-based control to predictive, multi-objective optimization powered by machine learning and cloud analytics. As per sources, microgrids using AI-driven controllers reduced energy costs and carbon emissions compared to conventional systems. Utilities are leading adoption. Software has been deployed across microgrids to autonomously rebalance loads during storm outages, reducing restoration time. Managed services are equally influential. Controller software is being provided as a service for military bases, eliminating upfront licensing costs. Startups offer subscription-based optimization platforms that integrate weather forecasts, real-time pricing, and equipment degradation models. Controller intelligence is now the key differentiator. Coupled with the shift to opex models, software and services have become core value drivers.

By Vertical Insights

The commercial segment held the leading share of 31.8% of the global microgrid controller market, with retail chains, data centers, and mixed-use developments serving as primary adopters. These entities prioritize uninterrupted operations due to revenue sensitivity, regulatory compliance, and brand reputation, all enabled by intelligent controllers that manage seamless islanding and load prioritization. According to research, most advanced data centers are being equipped with microgrid controllers that enable seamless, autonomous transition during grid failures, ensuring continuous cloud service availability. Major retail chains are implementing microgrid controllers as standard equipment for all new supercenters. These systems successfully reduce peak demand charges across numerous locations. In Europe, the EU’s Energy Efficiency Directive requires large commercial buildings to implement active energy management systems, accelerating controller adoption in shopping malls and office complexes. Asia Pacific is emerging rapidly. The increasing energy needs of e-commerce and digital services have prompted commercial entities to see controllers not as a simple cost, but as critical infrastructure for safeguarding revenue.

The industrial vertical segment is expected to exhibit a noteworthy CAGR of 20.8% from 2025 to 2033 due to manufacturers’ need to maintain production continuity during grid instability while complying with tightening carbon regulations, objectives only achievable through advanced microgrid controllers. As per various sources, new industrial facilities frequently require autonomous controllers to manage integrated energy assets like solar, cogeneration, and battery storage due to power grid limitations. Advanced controllers manage industrial facility energy consumption, significantly reducing reliance on the main power grid during peak pricing windows. In addition, Industrial microgrids benefit from AI-optimized controllers that improve overall energy efficiency. Mining and chemicals are equally dependent. Industrial controllers are shifting from purely operational functions to strategic roles in compliance and competitiveness, a change spurred by stricter carbon border adjustments and ESG reporting standards.

REGIONAL ANALYSIS

North America Market Analysis

North America dominated the global microgrid controller market and accounted for a 38.7% share in 2024. The supremacy of North America's leadership is sustained by the United States’ aggressive regulatory frameworks, federal funding programs, and concentration of mission-critical infrastructure. Funding for microgrid projects increasingly requires compliance with specific distributed energy resource management system (DERMS) compliant controllers. Regulatory bodies are mandating the participation of commercial microgrids in their distributed energy resource management systems. Autonomous controllers are being deployed to ensure continuous critical operations during grid disruptions. Canada complements this ecosystem. So, North America remains the most technically advanced and commercially dense microgrid controller market globally.

Europe Market Analysis

Europe was the next-biggest player in the global microgrid controller market and held a 27.1% share in 2024, with Germany, the United Kingdom, and the Nordics serving as innovation anchors. The region’s influence stems from its early adoption of grid code requirements and carbon pricing mechanisms that compel controller integration. Regulatory requirements are being established for new microgrids above a certain capacity to provide synthetic inertia and reactive power support. Industrial centers are implementing controller-managed microgrids to meet grid stability guidelines set by energy legislation. Microgrid operators are receiving compensation through specific programs for providing voltage support services to the national grid. Industrial decarbonization is equally influential. Europe’s market is not the largest by volume, but it sets global standards for regulatory and environmental sophistication in microgrid control.

Asia Pacific Market Analysis

Asia Pacific is the fastest-growing region in the global microgrid controller market, with growth concentrated in India, China, Australia, and Southeast Asia. India remains the regional leader in deployment volume. Solar diesel microgrids are being commissioned, and they incorporate standardized auto sequencing controllers to manage voltage during power fluctuations. Controller-managed microgrids are being deployed in industrial parks to ensure consistent manufacturing operations when the main grid experiences rationing. Australia’s mining sector is a major adopter. Southeast Asia is emerging rapidly. Local manufacturers have expanded controller production capacity. Asia Pacific’s combination of energy access deficits, manufacturing scale, and climate vulnerability ensures its trajectory as the fastest-growing regional market in absolute deployment terms.

Latin America Market Analysis

Latin America expanded steadily in the global microgrid controller market, with Brazil, Chile, and Mexico leading regional demand. Chile’s mining sector is the primary driver. Controller-managed microgrids are being commissioned at mines to autonomously rebalance loads during generator failures. Industrial parks are installing microgrids with controllers to reduce reliance on diesel and comply with emissions rules. Mexico’s proximity to the U.S. has made it a key manufacturing hub. While regulatory frameworks remain fragmented, initiatives like Mercosur’s mutual recognition of grid code standards are reducing barriers. Latin America’s market is expanding not through per capita sophistication but through industrial necessity and geographic isolation, creating structural demand for autonomous control systems.

Middle East and Africa Market Analysis

The Middle East and Africa region is likely to grow in the global microgrid controller market during the forecast period. South Africa, Saudi Arabia, Nigeria, and Kenya are propelling the region’s growth. South Africa’s mining sector is the primary adopter. New mining projects are incorporating compliant controllers to manage hybrid power systems under load shedding conditions. Industrial programs are mandating microgrid controllers for new manufacturing zones to ensure resilience during outages. Community microgrids are being equipped with controllers that manage load shedding sequences during fuel shortages. Rural electrification efforts are deploying controller-managed solar microgrids across off-grid villages, prioritizing essential services during low insolation periods. Commercial estates are installing microgrids with controllers to maintain operations during grid collapse. A surge in donor funding, mineral demand, and grid vulnerability is propelling adoption forward, notwithstanding the low level of per capita investment. The region’s market is nascent but growing faster than the global average, with potential unlocked through modular controller designs and pay-as-you-go financing.

COMPETITIVE LANDSCAPE

The microgrid controller market features intense competition among industrial automation giants, energy software specialists, and defense contractors striving for technical differentiation and sector-specific penetration. Leading players such as Schneider Electric, Siemens, and Honeywell dominate through vertically integrated hardware, software, and advanced cybersecurity protocols and global service networks. They compete not on price, but on resilience, hence interoperability, and revenue generation capabMid-tierid tier suppliers focus on niche applications like rural electrification or island grids, where cost-optimized controllers offer an advantage. Regional players in Asia and Latin America leverage proximity and regulatory familiarity to capture local industrial and community projects. Innovation cycles are accelerating as grid services and carbon markets demand real-time multi-criteria decision making. Regulatory ambiguity forces continuous recertification and documentation. Strategic acquisitions and partnerships are common as companies seek to fill technology gaps and expand regional footprints. Customer loyalty is built through managed service models and predictive maintenance tools. The absence of universal communication standards creates an opportunity for premium players but also fragmentation. Competition is less about unit sales and more about embedding into revenue-generating, resilient energy ecosystems through science-led collaboration and regulatory foresight.

KEY MARKET PLAYERS

Companies playing a notable role in the global microgrid controller market include

- ABB Ltd

- Eaton Corporation

- Emerson Electric Co

- General Electric Power

- HOMER Energy LLC

- Honeywell International Inc.

- Lockheed Martin Corporation

- Pareto Energy Ltd.

- Power Analytics Corporation

- Princeton Power Systems

- S&C Electric Company

- Schneider Electric SE

- Schweitzer Engineering Laboratories, Inc.

- Siemens AG and Spirae LLC.

Top Players In The Market

- Schneider Electric SE strengthens its leadership in microgrid control through its EcoStruxure Microgrid Advisor platform, which integrates AI-driven optimization with real-time grid service participation. The company also partnered with Walmart to retrofit two hundred supercenter microgrids with predictive dispatch algorithms that reduced peak demand charges by twenty-eight percent. Schneider launched a controller as a service subscription model in Europe, eliminating upfront licensing costs for commercial users. Its controllers now comply with IEEE 2030.7 and IEC 61850 standards across all regions. These initiatives reflect a strategy anchored in interoperability, financialization, and mission-critical reliability, positioning Schneider as an orchestrator of intelligent, revenue-generating energy systems.

- Siemens AG drives innovation in microgrid control through its Spectrum Power Microgrid Management System, engineered for industrial decarbonization and grid code compliance. Siemens partnered with Duke Energy to deploy GridOS software across seventeen U.S. microgrids, autonomously rebalancing loads during storm outages. The company integrated blockchain-based command verification into its controllers to prevent spoofing attacks, meeting NIST SP 800 82 Rev 3 cybersecurity guidelines. A digital twin module was launched for predictive maintenance and failure simulation. These actions demonstrate Siemens’ commitment to industrial resilience, regulatory alignment, and cyber-physical security, ensuring relevance across evolving grid and sustainability mandates.

- Honeywell International Inc. reinforces its microgrid controller leadership through ruggedized, MIL STD 81G-compliant systems tailored for mining, defense, and remote operations. Honeywell partnered with the U.S. Army Corps of Engineers to standardize its controllers across forward operating bases for contested environment resilience. The company launched a self-healing algorithm that reconfigures power flows during communication dropouts, validated in Arctic and desert deployments. Its controllers now include an embedded zero-trust architecture to block unauthorized command injections. These initiatives reflect a strategy focused on extreme environment reliability, autonomous recovery, and defense-grade cybersecurity, positioning Honeywell as the enabler of mission-critical energy autonomy in the most demanding global locations.

Top Strategies Used By Key Market Participants

Product innovation through AI-driven multi-objective optimization remains central to competitive differentiation. Companies invest heavily in R and D to engineer controllers that balance cost, carbon,n and reliability in real time. Strategic geographic expansion targets high-growth regions like the Asia Pacific through localized certification and cold-weather ruggedization. Partnerships with utilities and industrial operators enable co-development of grid service participation models and long-term managed service agreements. Cybersecurity hardening focuses on zero-trust architectures and blockchain-based command verification to meet NIST and MIL STD standards. Cloud-based controller as a service models democratize access by eliminating upfront licensing costs. Acquisitions of energy analytics startups broaden predictive capabilities and fill algorithmic gaps. Participation in global interoperability initiatives like IEEE 2030.7 ensures compliance and market access. Training programs for facility engineers build technical loyalty. Investment in digital twin simulations reduces commissioning risk. Regulatory advisory services help customers navigate complex interconnection and ancillary service requirements.

MARKET SEGMENTATION

This research report on the global microgrid controller market has been segmented and sub-segmented based on connectivity, offering, vertical, and region.

B,y Cnnectivity

- Grid Connected

- Off Grid/Remote/Islanded

By Offering

- Hardware

- Software

- Services

By Vertical

- Government

- Utilities

- Commercial

- Industrial

- Educational Institutes

- Military & Defense

- Healthcare

- Others (Small Residential Communities, Townships, and Villages),

By Region

- North America

- The United States

- Canada

- Rest of North America

- Europe

- The United Kingdom

- Spain

- Germany

- Italy

- France

- Rest of Europe

- The Asia Pacific

- India

- Japan

- China

- Australia

- Singapore

- Malaysia

- South Korea

- New Zealand

- Southeast Asia

- Latin America

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- The Middle East and Africa

- Saudi Arabia

- UAE

- Lebanon

- Jordan

- Cyprus

Frequently Asked Questions

Why is the microgrid controller market growing faster than overall microgrid deployments?

While microgrid hardware (solar, storage, gensets) scales linearly, controllers—especially AI-enabled, cloud-connected platforms—are becoming the intelligence layer that unlocks value: optimizing dispatch, enabling grid services (frequency regulation, peak shaving), and ensuring resilience. As project complexity rises, controller spend per MW is increasing—making it the highest-margin, fastest-evolving segment.

What segment is driving the most innovation in controller architecture?

Hybrid AC/DC microgrids with multi-energy integration (solar + wind + battery + hydrogen + thermal) are pushing demand for hierarchical, multi-layer controllers—with fast-acting (millisecond) local controllers for stability and slower supervisory layers for economic optimization—especially in islanded and remote industrial applications (mining, telecom, military).

Which region leads in advanced controller adoption—and why?

North America dominates in revenue and sophistication—driven by U.S. military microgrids (e.g., DOE’s REopt projects), California’s Self-Generation Incentive Program (SGIP), and ISO/Grid services participation. The U.S. accounts for >40% of global controller revenue, with vendors like Schneider Electric, Siemens, and Power Electronics integrating IEEE 2030.7/2030.8 compliance and UL 1741 SA/UL 9540A certification as baseline.

How are grid-interactive microgrids reshaping controller requirements?

Modern controllers must now support dynamic islanding, seamless grid synchronization, and real-time market bidding (e.g., via APIs to PJM, ERCOT)—turning microgrids into transactive energy assets. This demands cybersecurity (NISTIR 7628, IEC 62443), advanced forecasting (solar + load), and adaptive protection schemes to avoid unintentional islanding.

Who are the key players and how is the competitive landscape evolving?

Tier-1: Schneider Electric (EcoStruxure), Siemens (Spectrum Power), ABB (Ability Microgrid Solutions)—offer integrated hardware-software stacks. Pure-play innovators: Power Analytics (GridBlox), Ageto (now part of Generac), Blue Pillar (acquired by Honeywell)—focus on open-architecture, vendor-agnostic control. Cloud-native startups (Span.IO, Wärtsilä’s Greensmith) are gaining traction with SaaS-based optimization.

What’s the biggest technical hurdle in controller deployment today?

Interoperability—legacy DG units (diesel gensets, older inverters) often lack standardized communication (Modbus, CAN, DNP3), forcing costly retrofitting or gateways. The rise of IEEE 1547-2018 and SunSpec Modbus is helping, but field integration remains 30–50% of project CAPEX in complex retrofits.

How are AI and digital twins transforming controller capabilities?

AI-driven controllers now predict faults (e.g., battery degradation, inverter overheating), simulate “what-if” scenarios via digital twins, and auto-tune parameters in real-time—improving uptime by 15–25% and reducing O&M costs. For example, Hitachi Energy’s Grid-eXpand uses ML to optimize battery cycling for 20% longer lifespan.

Are developing markets adopting simpler or smarter controllers?

Contrary to assumptions, off-grid Africa and Southeast Asia are leapfrogging to cloud-managed, IoT-enabled controllers (e.g., Xendee, LO3 Energy)—enabling remote monitoring, pay-as-you-go billing, and fleet-level optimization across hundreds of village microgrids, often via low-bandwidth cellular (NB-IoT, LoRaWAN).

What regulatory shift is most impactful for controller vendors?

FERC Order 2222 (U.S.) and EU’s Clean Energy Package now allow aggregated microgrids to participate in wholesale markets—requiring controllers to provide telemetry, dispatch signals, and performance guarantees to ISOs—effectively turning them into grid-edge virtual power plants (VPPs).

What’s the market outlook for 2025–2030?

The global microgrid controller market is projected to grow at >18% CAGR—fueled by decarbonization mandates, grid resilience investments, and AI-driven autonomy. The future lies in adaptive, self-healing controllers that treat microgrids as dynamic, market-responsive organisms—not just backup systems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com