Middle East Marketing and Advertising Market Size, Share, Trends & Growth Forecast Report By Service Type (Full-Service Agencies, Digital-Only Agencies, Others), By Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), By Coverage Model (Full-Service Mandates, Specialized Engagements), By End-User Sector (Public and Institutional, Private Enterprises), and By Country (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, Oman, Yemen, Iraq, Iran, Jordan, Lebanon, Syria, Israel, Palestine, Egypt, Turkey) – Industry Analysis and Forecast in Terms of Value (USD), 2026 to 2034

Middle East Advertising Market Size

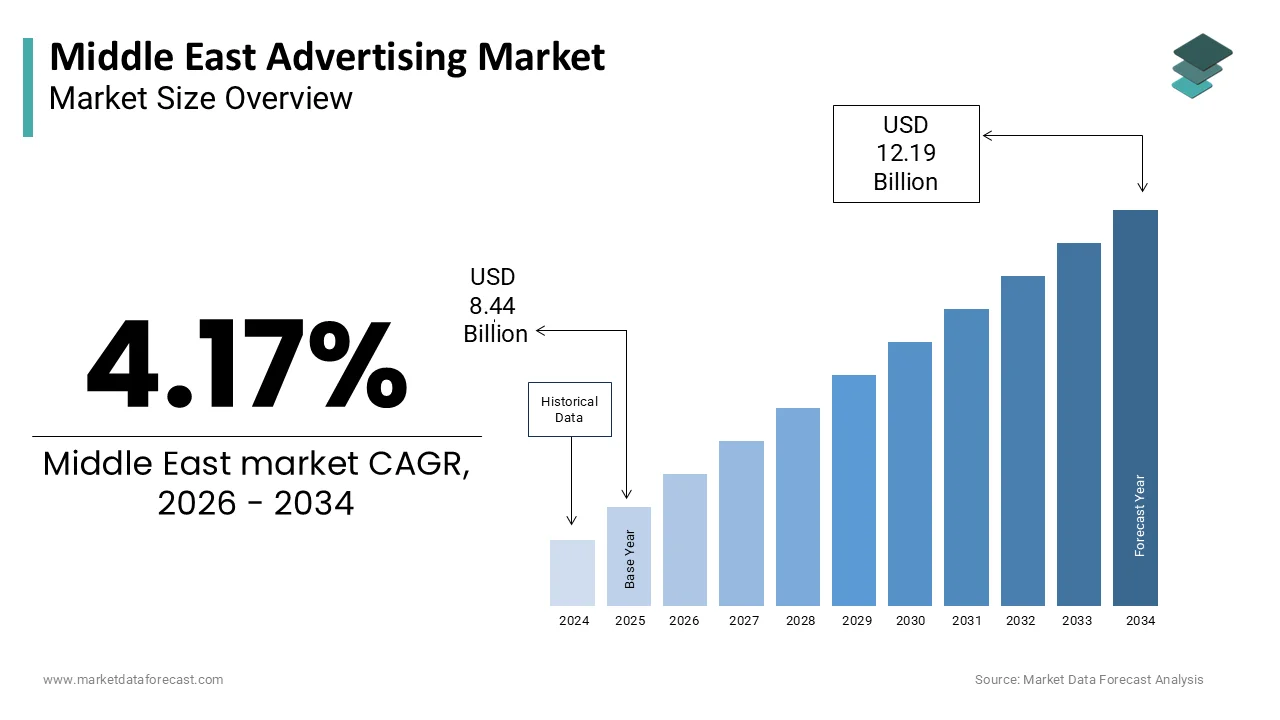

The Middle East advertising market was worth USD 8.44 billion in 2025 and is estimated to rise from USD 8.79 billion in 2026 to USD 12.19 billion by 2034, at a CAGR of 4.17%. From 2026 to 2034.

The advertising is a dynamic and rapidly digitizing ecosystem shaped by shifting consumer behaviors, technological advancement, and government-led economic diversification. It encompasses a broad spectrum of promotional activities across digital platforms, broadcast media, out-of-home (OOH) installations, and experiential marketing, serving industries ranging from retail and real estate to fintech and entertainment. Additionally, the expansion of e-commerce is driven by platforms like Noon and Amazon, ae.ae has intensified demand for performance-based advertising models.

MARKET DRIVERS

Surge in Digital and Mobile-First Consumer Engagement

The rapid adoption of mobile internet and social media platforms is driving the growth of the Middle East advertising market. According to the Arab Social Media Report published by the Mohammed Bin Rashid School of Government, the region recorded 190 million active social media users in 2023, with average daily usage reaching 3.5 hours, which is the highest globally. This deep digital immersion has prompted advertisers to shift budgets from traditional TV and print to targeted digital campaigns. In the UAE and Saudi Arabia, digital advertising accounted for 68% of total ad spend in 2023, as reported by Statista, with Instagram, Snapchat, and YouTube dominating engagement. The proliferation of Arabic-language content and localized influencer partnerships has further enhanced campaign effectiveness.

Expansion of E-Commerce and Performance-Based Advertising Models

The exponential growth of online shopping, where brands prioritize measurable outcomes such as clicks, conversions, and customer acquisition, is amplifying the growth of the Middle East advertising market. According to the Dubai Department of Economy and Tourism, e-commerce sales in the UAE reached $108 billion in 2023, while Saudi Arabia’s online retail market grew to $18.5 billion, as disclosed by the Saudi Data and Artificial Intelligence Authority. This surge has led to increased investment in pay-per-click (PPC), retargeting, and affiliate marketing strategies. Platforms like Google Ads and Meta Business Suite report year-on-year ad spend growth of over 25% in the GCC region. Additionally, the integration of AI-powered analytics enables real-time optimization of ad placements and audience segmentation.

MARKET RESTRAINTS

Fragmented Regulatory Environment and Inconsistent Data Privacy Frameworks

The absence of harmonized digital advertising regulations and data protection laws across countries is limiting the growth of the Middle East advertising market. According to the Gulf Cooperation Council (GCC) Secretariat General, only four of the six member states have enacted formal data localization or consent-based tracking policies. This regulatory asymmetry complicates cross-border campaign management, particularly for programmatic advertising that relies on user behavior tracking.

Persistent Reliance on Traditional Media in Conservative Markets

The expenditure in certain Middle Eastern markets remains allocated to traditional media such as television, radio, and print, which is slowing down the growth of the Middle East advertising market. In Egypt and Iraq, over 50% of advertising budgets were still directed toward TV and newspapers in 2023, as reported by the Arab States Broadcasting Union, due to broader reach among older demographics and limited digital literacy in rural areas. This reliance is reinforced by the continued dominance of free-to-air satellite channels like MBC and Rotana, which maintain high viewership during Ramadan and national events. However, traditional formats lack the targeting precision and performance analytics of digital platforms, reducing campaign efficiency. Moreover, the absence of standardized audience measurement systems such as Nielsen ratings across many countries hampers ROI evaluation. These structural inertia and measurement gaps discourage full-scale digital migration, particularly among local and regional brands with limited marketing expertise.

MARKET OPPORTUNITIES

Growth of Influencer and Creator-Led Brand Campaigns

The rise of a vibrant digital creator is enabling brands to engage audiences through authentic, culturally resonant storytelling, which is posing new opportunities for the growth of the Middle East advertising market. As of 2023, the region boasted over 15,000 professional influencers with followings exceeding 100,000, according to Influencer Marketing Hub MENA, many of whom specialize in fashion, beauty, parenting, and lifestyle content. Platforms like TikTok and Instagram have become primary discovery channels, with 68% of consumers in Saudi Arabia stating they have purchased a product after seeing it promoted by an influencer, as per a 2023 PwC Middle East Consumer Insights Survey. Brands are increasingly adopting micro-influencer strategies to achieve higher engagement at lower costs.

Adoption of AI and Programmatic Advertising Technologies

The integration of artificial intelligence and programmatic buying platforms is additionally to leverage the growth of the Middle East advertising market. AI-powered tools now enable real-time bidding, audience segmentation, and predictive analytics by allowing advertisers to optimize campaigns dynamically. In the UAE, over 70% of digital display ads are now served through automated platforms, as reported by the Dubai Advertising Regulatory Council. Additionally, generative AI is being used to create localized ad copy and visuals in Arabic dialects, reducing production time and costs. For instance, Emirates NBD leveraged AI-driven personalization in its 2023 digital campaign, which is achieving a 45% higher click-through rate.

MARKET CHALLENGES

High Levels of Digital Ad Fraud and Piracy-Related Revenue Loss

The Middle East advertising market faces escalating threats from digital ad fraud, including fake impressions, bot traffic, and domain spoofing, which undermine campaign integrity and erode advertiser confidence. According to White Ops (now HUMAN Security), the region experienced a 29% higher rate of automated bot traffic than the global average in 2023, with up to 22% of digital ad impressions deemed non-human. In markets like Egypt and Lebanon, unregulated websites and pirated streaming platforms generate fraudulent ad revenue by embedding counterfeit inventory into programmatic exchanges. The International Advertising Bureau estimates that ad fraud costs the Middle East over $600 million annually. This environment discourages premium brands from investing in open exchanges and forces agencies to adopt costly verification tools. Additionally, the lack of centralized fraud detection standards across regional ad tech providers exacerbates the problem by requiring greater collaboration between regulators, platforms, and industry bodies to restore transparency.

Cultural and Linguistic Fragmentation Limiting Pan-Regional Campaigns

The diverse linguistic and cultural landscape is a challenge for advertisers seeking to execute unified regional campaigns, which is also limiting the growth of the Middle East advertising market. According to a 2023 study by Kantar MENA, advertisements using localized dialects achieved 3.7 times higher engagement than those in formal Arabic. Additionally, cultural sensitivities around gender roles, religion, and social norms differ across countries, requiring careful adaptation. For example, a 2022 campaign by a global beauty brand was withdrawn in Kuwait after backlash over perceived immodesty, despite its success in the UAE.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Organization, Coverage, End-User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, Oman, Yemen, Iraq, Iran, Jordan, Lebanon, Syria, Israel, Palestine, Egypt, Turkey. |

| Market Leaders Profiled | Omnicom Group (TBWA\RAAD), Publicis Groupe, Impact BBDO, Memac Ogilvy, Leo Burnett MENA, Saatchi & Saatchi Middle East, Dentsu, Multiply Group PJSC (BackLite Media LLC), Tonic International, Dooha Media, Mars Media Group, BPG Group, 3Points Advertising, Maat Marcom Agency, MBC Group, Al Arabia (ACSC), Google, Meta (Facebook/Instagram), Amazon, Apple, Microsoft, Twitter (X), Alibaba, Baidu, Tencent, Applovin, Boopin, Amplify Dubai, Digital Gravity, ELAN Group, HyperMedia FZ, and McCollins Media. |

SEGMENTAL ANALYSIS

By Organization Insights

The large enterprises segment was the largest and held a prominent share of the Middle East advertising market in 2025, with the substantial marketing budgets of multinational corporations and state-backed conglomerates operating in high-revenue sectors such as telecommunications, banking, real estate, and retail. For instance, telecom giants like Etisalat and STC allocate over $200 million annually to integrated advertising campaigns, according to internal financial disclosures reviewed by Gulf Business. The increasing reliance on data-driven, omnichannel advertising strategies that require significant investment in technology and expertise is additionally to propel the growth of the Middle East advertising market.

The small and medium-sized enterprises (SMEs) segment is likely to grow with an expected CAGR of 14.2% during the forecast perio,d with the democratization of digital advertising tools, which enable SMEs to compete with larger brands at a fraction of the cost. Platforms like Google Ads, Meta Business Suite, and TikTok Ads offer pay-per-click models and granular targeting by allowing small retailers, startups, and local service providers to launch hyper-local campaigns with measurable outcomes.

By Coverage Insights

The full-service segment accounted in holding 58.3% of the Middle East advertising market share in 2025, with the preference of major brands for integrated agencies that can manage end-to-end campaigns across strategy, creative development, media buying, and performance analytics. Full-service agencies such as FP7 McCann, Impact BBDO, and Leo Burnett Middle East offer comprehensive solutions tailored to complex regional dynamics, including cultural sensitivities, multilingual audiences, and diverse regulatory environments.

The specialized capabilities segment is likely to grow with an anticipated CAGR of 16.5% during the forecast period, with the increasing demand for niche expertise in digital performance marketing, influencer management, and AI-driven analytics. Brands are shifting from generalized campaigns to precision-targeted strategies that require specialized agencies focusing exclusively on programmatic advertising, search engine optimization (SEO), or social media monetization. Specialized agencies offer deep sector knowledge and technical proficiency, such as compliance with financial advertising regulations or integration with e-commerce platforms like Noon and Amazon.ae.

By End-User Insights

The private enterprises segment was the largest and held a significant share of the Middle East advertising market in 2025, with the expanding consumer economy, where private companies in retail, automotive, telecommunications, and FMCG sectors invest heavily to capture market share and build brand equity. The proliferation of shopping malls, e-commerce platforms, and luxury retail destinations has intensified competition, necessitating sustained advertising efforts. The aggressive expansion strategies of regional and multinational corporations seeking to capitalize on rising disposable incomes and urbanization are also limiting the growth of the Middle East advertising market. Additionally, the entry of global brands into the Middle East, such as Apple, Tesla, and IKEA, has elevated advertising standards, prompting local competitors to respond with high-production campaigns.

The public and institutional sector is likely to register a CAGR of 10.8% during the forecast periodd with the government-led national transformation programs that rely on mass communication to promote social, economic, and behavioral change. In Saudi Arabia, the Vision 2030 initiative has necessitated large-scale public awareness campaigns on topics such as women’s workforce participation, health awareness, and tourism promotion. The institutionalization of branding for government entities and semi-public organizations is additionally leveraging the growth of the Middle East advertising market. Entities such as NEOM, Riyadh Air, and the General Entertainment Authority have adopted corporate-style marketing with high-budget campaigns featuring global celebrities and cinematic production. In 2023, NEOM’s “This is It” campaign reached over 1.2 billion impressions worldwide, as reported by Campaign Middle East. Similarly, the UAE’s “We the UAE 2031” national agenda includes a dedicated communications strategy to foster civic engagement. Public health campaigns during the pandemic and initiatives promoting digital government services have further normalized institutional advertising.

COUNTRY LEVEL ANALYSIS

Saudi Arabia Advertising Market Insights

Saudi Arabia was the top performer in the Middle East advertising market by capturing 34.3% of share in 2025. Government entities and state-backed giga-projects such as NEOM, Red Sea Global, and Qiddiya are investing heavily in global branding campaigns, with NEOM alone allocating over $500 million to marketing since 2021, as reported by Bloomberg. Simultaneously, the private sector is expanding its advertising footprint to meet rising consumer demand in retail, fintech, and entertainment. The General Commission for Audiovisual Media reported a 40% increase in licensed advertising agencies between 2021 and 2023.

United Arab Emirates Advertising Market Insights

The United Arab Emirates advertising market held 28.3% of the share in 2025. Dubai and Abu Dhabi host the headquarters of major global agencies, including WPP, Omnicom, and Publicis, which manage regional campaigns for multinational clients. The UAE’s advanced digital infrastructure enables sophisticated programmatic advertising, with 70% of digital display ads served through automated platforms in 2023. The country also leads in experiential marketing, hosting high-profile events such as Expo 2020 and Dubai Shopping Festival, which generate massive ad spend.

KEY MARKET PLAYERS

The key players in the Middle East advertising market include Omnicom Group (TBWA\RAAD), Publicis Groupe, Impact BBDO, Memac Ogilvy, Leo Burnett MENA, Saatchi & Saatchi Middle East, Dentsu, Multiply Group PJSC (BackLite Media LLC), Tonic International, Dooha Media, Mars Media Group, BPG Group, 3Points Advertising, Maat Marcom Agency, MBC Group, Al Arabia (ACSC), Google, Meta (Facebook/Instagram), Amazon, Apple, Microsoft, Twitter (X), Alibaba, Baidu, Tencent, Applovin, Boopin, Amplify Dubai, Digital Gravity, ELAN Group, HyperMedia FZ, and McCollins Media.

TOP LEADING PLAYERS IN THE MARKET

Impact BBDO

Impact BBDO Middle East is a leading creative force in the region’s advertising landscape, known for its culturally insightful campaigns and strategic brand transformation initiatives. Operating across Dubai, Riyadh, and Cairo, the agency has pioneered award-winning work for clients such as STC, Nissan, and Nestlé, which is blending global creative standards with deep local understanding. In recent years, Impact BBDO has strengthened its digital capabilities by launching a dedicated performance marketing division focused on AI-driven audience segmentation and real-time campaign optimization. The agency also introduced a regional behavioral insights unit to decode Arab consumer psychology, enhancing message resonance. In 2023, it led the rebranding of Saudi Arabia’s Ministry of Investment by aligning its visual identity with Vision 2030’s economic ambitions.

FP7 McCann

FP7 McCann has established itself as a dominant player in integrated brand communication across the Middle East, delivering high-impact campaigns that merge storytelling with digital innovation. With offices in Dubai, Abu Dhabi, and Jeddah, the agency serves major regional and multinational clients, including Emirates, Etisalat, and Pfizer. FP7 McCann has recently invested in an in-house content studio specializing in short-form video for TikTok and Instagram Reels, catering to the region’s youth-driven digital consumption. In 2023, it launched “Creative X,” a cross-functional team combining data scientists, cultural anthropologists, and AR designers to develop immersive brand experiences. The agency also partnered with MBC Group to co-develop branded entertainment formats for Ramadan programming.

Leo Burnett

Leo Burnett Middle East has redefined brand engagement in the region by prioritizing emotional storytelling and purpose-driven advertising. With a presence in Dubai, Riyadh, and Cairo, the agency has crafted iconic campaigns for brands such as Almarai, Pepsi, and Dubai Tourism, consistently winning accolades at Cannes Lions and Dubai Lynx. In 2023, Leo Burnett launched “HumanKind MENA,” a strategic framework applying behavioral science to create culturally relevant messaging that drives action. The agency has also expanded its influencer marketing arm, forging long-term partnerships with top Arab digital creators to amplify brand authenticity. It introduced AI-powered sentiment analysis tools to monitor campaign performance across Arabic dialects in real time.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Middle East advertising market are leveraging data-driven personalization, AI-powered analytics, and culturally attuned storytelling to strengthen brand engagement. Agencies are investing in in-house creative studios and behavioral research units to decode regional consumer psychology. Integration of programmatic advertising and performance marketing enables real-time campaign optimization. Strategic partnerships with media platforms and influencers enhance reach and authenticity. Expansion into experiential and branded content allows agencies to transcend traditional formats. Additionally, agencies are adopting agile workflows and cross-functional teams combining creatives, technologists, and data scientists to deliver integrated solutions that align with national transformation agendas and digital-first consumer behaviors.

COMPETITION OVERVIEW

Competition in the Middle East advertising market is intensifying as global networks, regional independents, and digital-native agencies vie for dominance in a rapidly evolving ecosystem. Legacy agencies are modernizing through AI integration and performance marketing, while boutique firms specialize in influencer campaigns and ad tech solutions. The rise of in-house agency models among large corporations adds pressure on traditional players. Government-led branding initiatives in Saudi Arabia and the UAE have created high-value public sector contracts, attracting top talent and investment. Simultaneously, digital platforms like Meta, Google, and TikTok are encroaching on creative services, offering end-to-end campaign management. Success now depends on cultural fluency, technological agility, and the ability to deliver measurable ROI in a market where consumer expectations are increasingly shaped by global standards and local identity.

RECENT MARKET DEVELOPMENTS

- In January 2023, Impact BBDO launched a behavioral insights unit focused on Arab consumer psychology, enhancing campaign relevance and engagement for clients across Saudi Arabia and the UAE.

- In April 2023, FP7 McCann introduced a dedicated short-form video studio for TikTok and Instagram Reels, positioning itself at the forefront of mobile-first advertising in the region.

- In August 2023, Leo Burnett Middle East partnered with MBC Group to co-develop branded entertainment formats for Ramadan, increasing client visibility through culturally immersive content.

- In May 2025, FP7 McCann integrated AI-powered sentiment analysis across its campaign monitoring systems, enabling real-time adjustments to messaging in multiple Arabic dialects.

MARKET SEGMENTATION

This research report on the middle mast advertising market is segmented and sub-segmented into the following categories.

By Organization Size

- Small and Medium-sized Enterprises (≤ 250 employees)

- Large Enterprises (> 250 employees)

By Coverage Model

- Full-Service Mandates

- Specialized/Best-of-Breed Engagements

By End-user Sector

- Public and Institutional

- Private Enterprises

By Country

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Bahrain

- Oman

- Yemen

- Iraq

- Iran

- Jordan

- Lebanon

- Syria

- Israel

- Palestine

- Egypt

- Turkey

Frequently Asked Questions

1. What drives growth in the Middle East Advertising Market?

Growth in the Middle East Advertising Market is driven by

digital transformation, e-commerce, and increased investment in mobile and online advertising channels.

2. What are key digital trends in the Middle East Advertising Market?

In the Middle East Advertising Market, digital out-of-home advertising,

AI-driven campaigns, influencer partnerships, and data-based targeting are shaping marketing strategies.

3. What industries are top advertisers in the Middle East Advertising Market?

The Middle East Advertising Market has strong demand from the technology, telecom, financial services, retail, and consumer goods industries.

With these sectors driving ad spend.

4. How is influencer marketing used in the Middle East Advertising Market?

Influencer marketing in the Middle East Advertising Market uses local digital creators to reach young, tech-savvy audiences,

boosting engagement across platforms like Instagram and TikTok

5. What is programmatic advertising in the Middle East Advertising Market?

Programmatic advertising in the Middle East Advertising Market automates the buying of digital ad space,

improving targeting, reach, and ROI for campaigns.

6. How is social media shaping the Middle East Advertising Market?

Social media plays a key role in the Middle East Advertising Market,

Platforms such as Instagram, TikTok, and Snapchat are widely used for regional marketing and brand engagement.

7. What regulations impact the Middle East Advertising Market?

The Middle East Advertising Market is influenced by diverse regulations on advertising content,

especially in countries like Saudi Arabia and the UAE, requiring compliance for successful campaigns.

8. What is the role of Arabic language in the Middle East Advertising Market?

Arabic language is essential in the Middle East Advertising Market,

helping brands personalize messages, connect culturally, and increase campaign effectiveness with local consumers

9 What are leading formats in the Middle East Advertising Market?

Video ads, digital out-of-home displays, and mobile-first campaigns lead in the Middle East Advertising Market.

reflecting shifting consumer habits and high smartphone usage

10. How is performance measured in the Middle East Advertising Market?

Performance in the Middle East Advertising Market is tracked using metrics such as reach, engagement, conversions,

and ROI, especially for digital and social campaigns.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com