Middle East & Africa Defibrillators Market Research Report By Product (Implantable Cardioverter Defibrillator and External), End User and Country (KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, rest of MEA) - Industry Analysis on Size, Share, Trends, COVID-19 Impact & Growth Forecast (2026 to 2034)

MEA Defibrillators Market Size

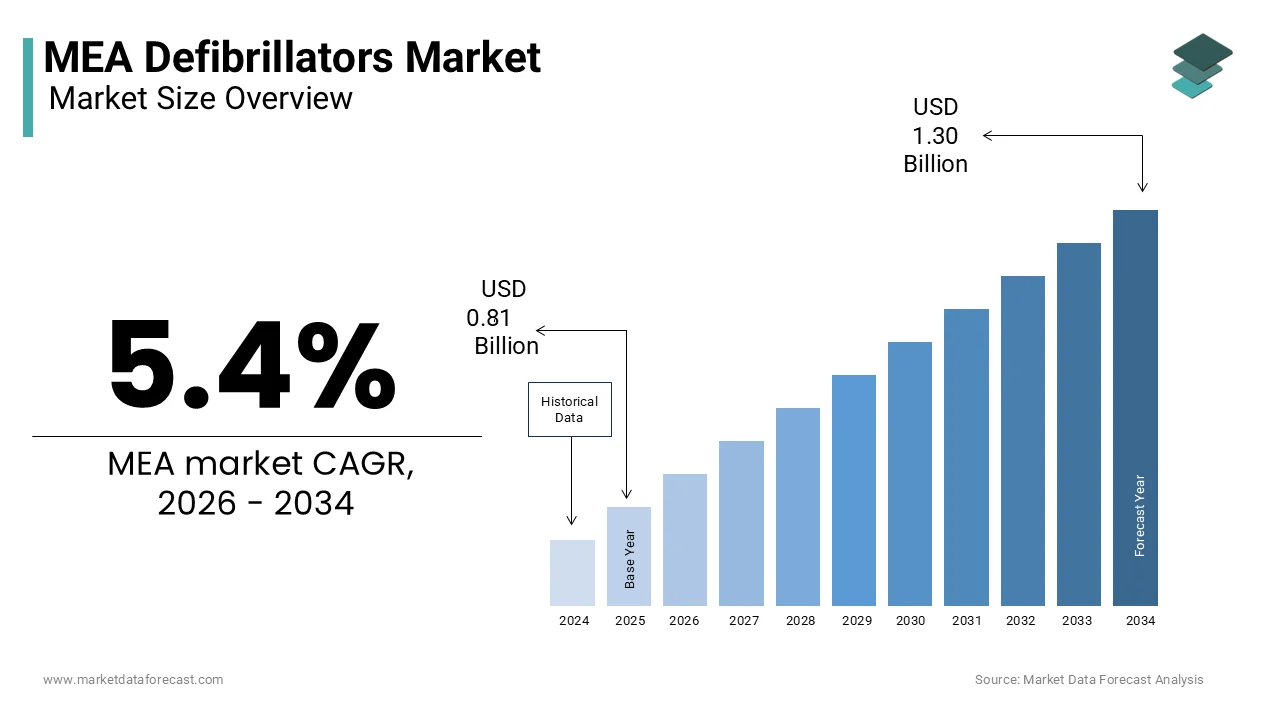

The MEA defibrillators market was valued at USD 0.81 billion in 2025, is estimated to reach USD 0.86 billion in 2026, and is projected to reach USD 1.30 billion by 2034, growing at a CAGR of 5.4% from 2026 to 2034.

The Middle East and African defibrillators market exhibited a steady performance in 2025 as regional healthcare systems prioritized emergency response upgrades and is likely to maintain a robust growth trajectory during the forecast period. The MEA defibrillators market encompasses a critical segment of medical devices designed to restore normal heart rhythm in patients experiencing life-threatening arrhythmias such as ventricular fibrillation or pulseless ventricular tachycardia. This market includes automated external defibrillators, implantable cardioverter defibrillators, and wearable cardioverter defibrillators utilized across hospitals, ambulatory surgical centers, and public access settings. The region is witnessing a gradual but significant shift towards enhanced cardiac care infrastructure driven by the rising burden of cardiovascular diseases. According to the World Health Organization, cardiovascular diseases are the leading cause of death globally, taking an estimated 17.9 million lives each year, with a substantial proportion occurring in low and middle-income countries within the Middle East and Africa. In the Gulf Cooperation Council countries, the prevalence of risk factors such as diabetes and hypertension is alarmingly high. According to the International Diabetes Federation, the Middle East and North Africa region has the highest comparative prevalence of diabetes in adults at 16.2%, which significantly increases the risk of sudden cardiac arrest. Furthermore, as per the African Union, non-communicable diseases now account for over 30% of all deaths in Africa, a figure projected to rise. These epidemiological trends underscore the urgent need for accessible defibrillation technology. Governments in nations like Saudi Arabia and the United Arab Emirates are increasingly prioritizing emergency cardiac care systems, while South Africa and Nigeria are expanding their critical care capabilities. This evolving healthcare landscape reflects a growing recognition of the importance of timely defibrillation in improving survival rates from sudden cardiac events across the diverse socioeconomic landscapes of the MEA region.

MARKET DRIVERS

Rising Prevalence of Cardiovascular Diseases And Risk Factors

The expansion of cardiac care infrastructure in 2025 was largely dictated by the increasing volume of chronic disease patients and is likely to continue driving the adoption of specialized medical devices throughout the forecast period, which is one of the key factors propelling the growth of the MEA defibrillators market. The escalating prevalence of cardiovascular diseases and associated risk factors serves as a primary catalyst for the expansion of the MEA Defibrillators Market. Conditions such as coronary artery disease, heart failure, and hypertension are becoming increasingly common due to lifestyle changes and demographic shifts. According to the World Heart Federation, cardiovascular disease mortality in the Middle East and North Africa region is expected to increase by 30% by 2030 if current trends continue. In Saudi Arabia, the Ministry of Health reports that heart disease accounts for approximately 28% of all deaths, creating a substantial patient pool requiring advanced cardiac interventions. The high incidence of diabetes is a critical contributing factor, as it significantly elevates the risk of sudden cardiac arrest. According to the International Diabetes Federation, over 73 million adults in the Middle East and North Africa region were living with diabetes in 2021, a number projected to rise to 136 million by 2045. Additionally, obesity rates are climbing rapidly, with the World Obesity Atlas noting that over 35% of adults in several Gulf countries are obese. Excess body weight places additional strain on the cardiovascular system, increasing the likelihood of arrhythmias. The aging population in countries like Egypt and Morocco further exacerbates this trend, as the risk of cardiac events rises with age. These health dynamics drive the demand for both implantable and external defibrillators, as healthcare providers seek to manage the growing burden of sudden cardiac arrest and improve patient survival rates through timely and effective intervention.

Government Initiatives And Healthcare Infrastructure Development

Strategic government initiatives and substantial investments in healthcare infrastructure are also propelling the growth of the Middle East and African defibrillators market. Nations across the Middle East, particularly those in the Gulf Cooperation Council, are implementing comprehensive healthcare transformation programs to enhance emergency cardiac care. As per the Saudi Vision 2030 framework, the Kingdom is investing billions of dollars in upgrading hospital facilities and expanding access to advanced medical technologies, including defibrillators. The Ministry of Health in the United Arab Emirates has mandated the installation of automated external defibrillators in public spaces such as airports, malls, and sports stadiums to improve response times during cardiac emergencies. In Africa, governments are increasingly recognizing the need to strengthen critical care services. The African Society of Cardiology highlights that countries like South Africa and Kenya are expanding their national health insurance schemes to cover cardiac procedures, thereby increasing accessibility to life-saving devices. According to the World Bank, health expenditure per capita in the Middle East has grown by 5% annually over the last decade, reflecting a commitment to improving healthcare outcomes.

Furthermore, partnerships between public health authorities and international organizations are facilitating the training of healthcare professionals in advanced cardiac life support. These efforts are creating a favorable environment for the adoption of defibrillation technologies. By prioritizing emergency preparedness and infrastructure development, governments are directly stimulating the demand for defibrillators, ensuring that these critical devices are available in both clinical and community settings across the region.

MARKET RESTRAINTS

High Cost of Advanced Defibrillation Technologies and Limited Reimbursement

The prohibitive cost of advanced defibrillation technologies, coupled with limited reimbursement policies, are majorrestraints to the growth of the MEA defibrillators market. High-end implantable cardioverter defibrillators and sophisticated automated external defibrillators carry substantial price tags that are often inaccessible to the majority of the population, particularly in low-income African nations. According to the World Bank, out-of-pocket health expenditure in many sub-Saharan African countries exceeds 40% of total health spending, placing a heavy financial burden on patients. In nations like Yemen and Sudan, public health budgets are severely constrained, limiting the procurement of expensive imported medical devices. According to the African Development Bank, fiscal deficits in several countries have led to reduced healthcare funding, which is forcing public hospitals to rely on basic equipment rather than advanced defibrillation systems. Reimbursement frameworks are often inadequate or nonexistent for private sector devices. In Egypt, while public hospitals provide basic care, coverage for premium implantable devices is limited, requiring patients to pay significant amounts upfront. According to a study by the Eastern Mediterranean Public Health Network, nearly 50% of patients requiring cardiac devices delay or forego treatment due to financial constraints. This economic barrier restricts market penetration for high-value products and forces manufacturers to compete primarily on price. Consequently, the adoption of cutting-edge defibrillation technologies remains sluggish, hindering the overall market potential despite the growing clinical need for effective cardiac care solutions in the region.

Shortage of Trained Healthcare Professionals And Technical Expertise

A critical shortage of trained healthcare professionals and technical expertise is also inhibiting the expansion of the MEA defibrillators market. Effective use of defibrillators, particularly implantable devices, requires specialized knowledge for implantation, programming, and long-term management. According to the World Health Organization, the density of physicians in the African region is approximately 2.5 per 10,000 population, far below the global average, with cardiologists being even scarcer. In countries like Ethiopia and Nigeria, the ratio of cardiologists to population is less than 1 per 1 million inhabitants, severely limiting the capacity to manage complex cardiac cases. This scarcity of skilled professionals restricts the number of procedures that can be performed and hinders the proper maintenance of installed devices. According to the Middle East Council of Cardiologists, while Gulf countries have better ratios, there is still a reliance on expatriate specialists, which can lead to continuity issues.

Furthermore, training programs for emergency medical technicians and nurses in the use of automated external defibrillators are not uniformly implemented across the region. According to the International Liaison Committee on Resuscitation, bystander CPR and defibrillation rates in many MEA countries remain below 10%, largely due to a lack of public awareness and training. Without a robust workforce of trained professionals, the utilization of defibrillators remains suboptimal. This skills gap undermines the effectiveness of healthcare investments and limits the market's ability to expand, as hospitals struggle to operate and maintain advanced cardiac care units efficiently.

MARKET OPPORTUNITIES

Expansion of Public Access Defibrillation Programs

The expansion of public access defibrillation programs is a substantial opportunity for market growth in the MEA region. Increasing awareness of the importance of early defibrillation in improving survival rates from sudden cardiac arrest is driving initiatives to place automated external defibrillators in public spaces. According to the European Resuscitation Council, immediate defibrillation can increase survival chances by up to 70%. In the United Arab Emirates, the Dubai Corporation for Ambulance Services has launched initiatives to install automated external defibrillators in malls, hotels, and transportation hubs, setting a precedent for other nations. Saudi Arabia is also integrating these devices into its smart city projects, such as NEOM, where safety and health technology are prioritized. The World Health Organization encourages member states to develop national strategies for out-of-hospital cardiac arrest, which include public access defibrillation. In South Africa, private sector collaborations are leading to the placement of defibrillators in corporate offices and shopping centers. The International Federation of Red Cross and Red Crescent Societies is actively training volunteers in cardiopulmonary resuscitation and defibrillator use across various African countries. These efforts create a growing demand for user-friendly, durable automated external defibrillators. Manufacturers can capitalize on this trend by offering bundled solutions that include training and maintenance services. As more governments and private entities recognize the value of public access defibrillation, the market for these devices is expected to expand significantly, offering new revenue streams beyond traditional hospital settings.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | KSA, UAE, Israel, Rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, Rest of MEA |

| Market Leaders Profiled | Medtronic PLC (Ireland), St. Jude Medical, Inc. (U.S.), Boston Scientific Corporation (U.S.), BIOTRONIK SE & Co. KG (Germany), LivaNova PLC (U.K.), Koninklijke Philips N.V. (Netherlands), ZOLL Medical Corporation (U.S.), Cardiac Science Corporation (U.S.), Physio-Control, Inc. (U.S.), and Nihon Kohden Corporation (Japan)

|

COUNTRY LEVEL ANALYSIS

Saudi Arabia Defibrillation Market Analysis

Saudi Arabia led the regional market in 2025 with 27.1% of the regional market share through massive healthcare infrastructure investments and is likely to remain the dominant contributor during the forecast period. The market in Saudi Arabia is characterized by aggressive healthcare transformation under Vision 2030, which prioritizes advanced cardiac care infrastructure. The primary driver of market growth is the high prevalence of cardiovascular risk factors such as diabetes and obesity, coupled with significant government investment in hospital modernization. According to the Ministry of Health, the Kingdom is establishing new specialized cardiac centers and upgrading existing facilities with state-of-the-art defibrillation technologies. The Saudi Heart Association reports that cardiovascular diseases account for nearly 30% of all deaths, creating urgent demand for both implantable and external defibrillators. The government’s mandate for public access defibrillators in major venues and transportation hubs is further stimulating market growth. According to the General Authority for Statistics, health expenditure has increased by 8% annually, supporting the procurement of advanced medical devices. Additionally, the privatization of healthcare services is attracting foreign investment and introducing competitive dynamics that enhance product availability. The Kingdom’s focus on preventive care and emergency response readiness ensures sustained demand for defibrillators. With ongoing mega projects like NEOM incorporating smart health solutions, Saudi Arabia remains the dominant force in the MEA defibrillators market, driving innovation and volume growth through strategic policy and demographic needs.

United Arab Emirates Defibrillation Market Analysis

The United Arab Emirates secured a strong second position in 2025 by achieving high AED density in urban areas and is likely to lead in technological adoption during the forecast period. The UAE market is defined by a world-class healthcare system and a strong emphasis on public safety and emergency preparedness. The robust regulatory framework mandating the installation of automated external defibrillators in public spaces is driving the expansion of the UAE market. According to the Dubai Health Authority, all new buildings and public facilities must be equipped with AEDs, leading to consistent procurement volumes. The UAE has one of the highest densities of AEDs in the region, supported by initiatives like the Dubai Pulse platform, which maps device locations for emergency responders. According to the Ministry of Health and Prevention, cardiovascular disease is a leading cause of mortality, driving demand for implantable devices in private hospitals. The country’s status as a medical tourism hub attracts patients seeking advanced cardiac care, further boosting the market for high-end defibrillation technologies. According to the Department of Economic Development, the healthcare sector is growing at 6% annually, fueled by population growth and expatriate influx. The UAE’s proactive approach to integrating technology in healthcare, including remote monitoring for implantable devices, positions it as a leader in adopting innovative defibrillation solutions. This combination of regulatory support, high healthcare spending, and technological adoption sustains the UAE’s significant market share.

Israel Defibrillation Market Analysis

Israel demonstrated exceptional clinical outcomes in 2025 due to its advanced responder networks and is likely to continue as a high-value market during the forecast period. The Israeli market is distinguished by a highly developed healthcare system and a strong culture of public safety and emergency response. The high standard of cardiac care and widespread public access to defibrillation technology are primarily driving the market growth in Israel. According to the Israeli Ministry of Health, the country has one of the highest survival rates from out-of-hospital cardiac arrest in the world, partly due to the dense network of AEDs and trained responders. Magen David Adom, the national emergency service, maintains a comprehensive fleet of ambulances equipped with advanced defibrillators. The Israeli Heart Society reports that implantation rates for cardioverter defibrillators are among the highest globally, supported by comprehensive national health insurance coverage. According to the Central Bureau of Statistics, health expenditure per capita is high, enabling access to cutting-edge technologies. Israel is also a hub for medical technology innovation, with local companies developing next-generation defibrillation solutions. The integration of digital health tools for remote monitoring of implantable devices is widespread, enhancing patient management. This combination of clinical excellence, public preparedness, and technological innovation sustains Israel’s strong position in the MEA defibrillators market, driving value through high adoption of premium products.

South Africa Defibrillation Market Analysis

South Africa navigated a complex economic environment in 2025 to maintain its status as a critical gateway for African cardiac care and is likely to see steady private sector growth during the forecast period. The South African market is characterized by a dual healthcare system with a sophisticated private sector and a developing public infrastructure. The high burden of cardiovascular disease and the expanding private healthcare industry are propelling the market growth in this country. According to the Heart and Stroke Foundation South Africa, cardiovascular diseases cause one in five deaths in the country, creating a substantial need for defibrillation devices. The private healthcare sector, which serves about 16% of the population, drives demand for advanced implantable cardioverter defibrillators and cardiac resynchronization therapy devices. According to Stats SA, medical scheme membership is stable, supporting affordability for premium devices. In the public sector, government initiatives to improve emergency medical services are gradually increasing the availability of external defibrillators in ambulances and clinics. The Council for Medical Schemes reports that prescribed minimum benefits cover cardiac interventions, ensuring access for beneficiaries. Additionally, South Africa serves as a regional hub for medical device distribution, influencing markets in neighboring countries. Corporate wellness programs in major cities are also contributing to the placement of AEDs in workplaces. Despite economic challenges, the resilience of the private healthcare sector and ongoing public health improvements sustain South Africa’s position as a key market player in the MEA region.

COMPETITIVE LANDSCAPE

The competitive landscape of the MEA Defibrillators Market is characterized by the presence of established multinational corporations and emerging local distributors. Global giants dominate the sector due to their extensive product portfolio, ios advanced technological capabilities, and strong brand recognition. These companies leverage their financial resources to invest heavily in research and development,pment resulting in continuous innovation of defibrillation devices. H, however, local players are gaining traction by leveraging cost-effective distribution services and navigating complex regulatory environments more efficiently. The market exhibits moderate consolidation as larger entities acquire smaller firms or form joint ventures to expand their geographic reach and product offerings. Competition is further intensified by varying regulatory requirements across different countries, which create barriers to entry for new participants. Companies differentiate themselves through superior customer service,e comprehensive surgeon training programs, ms and strategic partnerships with local healthcare providers. The race to introduce connected and minimally invasive technologies adds another layer of complexity to the competitive dynamics. As healthcare infrastructure improves and demand for advanced cardiac care rises,ses the intensity of competition is expected to increase, driving further innovation and strategic maneuvering among key market participants in the region.

KEY MARKET PLAYERS

Some of the notable companies operating in the MEA defibrillators market.are

- Medtronic plc

- St. Jude Medical Inc.

- Boston Scientific Corporation

- BIOTRONIK SE & Co. KG

- LivaNova plc

- Koninklijke Philips N.V.

- ZOLL Medical Corporation

- Cardiac Science Corporation

- Physio-Control Inc.

- Nihon Kohden Corporation

TOP LEADING PLAYERS IN THE MARKET

- Medtronic plc stands as a global leader in medical technology with a significant footprint in the MEA defibrillators sector. The company offers a comprehensive portfolio of implantable and external defibrillation solutions that cater to diverse clinical needs. In the Middle East and Africa, Medtronic strengthens its position through strategic partnerships with local healthcare providers and government bodies to enhance cardiac care infrastructure. Recently,y the company has focused on expanding its training programs for electrophysiologists and emergency responders in key markets like Saudi Arabia and South Africa. Medtronic also invests in digital health innovations such as remote monitoring platforms that improve patient outcomes and reduce hospital visits. By leveraging its global expertise and local engagement,nt Medtronic continues to drive adoption of advanced defibrillation technologies. Its commitment to improving access to life-saving therapies ensures a strong presence in both public and private healthcare sectors across the region.

- Abbott Laboratories is a major contributor to the global defibrillators market with a robust presence in the MEA region. The company is renowned for its innovative implantable cardioverter defibrillators and cardiac resynchronization therapy devices. In recent years, Abbott has intensified its efforts to streamline supply chain operations in countries like the United Arab Emirates and Egypt to ensure consistent product availability. The organization actively collaborates with regional medical societies to promote best practices in sudden cardiac arrest management. Abbott also focuses on educating healthcare professionals through workshops and symposiums that highlight the benefits of its latest technologies. The company’s introduction of smaller and more durable devices appeals to patients seeking minimally invasive options. By combining product innovation with strong clinical support,t Abbott effectively addresses the growing demand for high-quality cardiac care solutions. Its strategic initiatives help solidify its reputation as a trusted partner in the MEA healthcare landscape.

- Boston Scientific Corporation is a key player in the MEA defibrillators market, known for its advanced cardiac rhythm management solutions. The company contributes significantly to the global market by developing cutting-edge technologies such as subcutaneous implantable defibrillators. In the MEA region, Boston Scientific has recently expanded its distribution network to reach underserved areas in Africa and the Middle East. The corporation engages in collaborative projects with local hospitals to facilitate the adoption of novel defibrillation therapies. It also prioritizes physician education by offering specialized training on complex implant procedures. Boston Scientific’s focus on clinical evidence and patient safety resonates well with healthcare providers in the region. The company regularly participates in regional cardiology conferences to showcase its latest advancements. By maintaining a strong local presence and fostering relationships with key opinion leaders,s Boston Scientific continues to grow its influence and drive improvements in cardiac care standards throughout the MEA region.

Top Strategies Used by the Key Market Participants

Key players in the MEA Defibrillators Market primarily employ strategic partnerships and localized training initiatives to strengthen their competitive stance. Companies frequently collaborate with government health ministries and local distributors to navigate regulatory complexities and improve supply chain efficiency. This approach ensures the timely delivery of critical devices to hospitals across diverse geographical areas. Another major strategy involves investing in physician education and public awareness campaigns. By enhancing the skills of local medical professionals and informing the public about sudden cardiac arrest, manufacturers foster loyalty and increase the adoption of their proprietary technologies. Product innovation remains central to corporate strategy,s with firms introducing connected and minimally invasive solutions to meet rising demand for advanced care. Additionally, key participants focus on expanding their presence in private healthcare sectors where reimbursement rates are higher. They also engage in tender bids for public sector projects to secure large volume contracts. These multifaceted strategies enable companies to address unique regional challenges while capitalizing on growth opportunities in emerging economies throughout the Middle East and Africa.

MARKET SEGMENTATION

This research report on the Middle East and Africa defibrillators market has been segmented and sub-segmented into the following categories:

By Product

- Implantable Defibrillators

- Transvenous Implantable Cardioverter Defibrillator (T-ICDs)

- Subcutaneous Implantable Cardioverter Defibrillator (S-ICDs)

- Cardiac Resynchronization Therapy- Defibrillator (CRT-D)

- External defibrillators

- Manual External Defibrillator

- Automated External Defibrillator (AEDs)

- Wearable Cardioverter Defibrillator (WCDs)

By End User

- Hospitals

- Prehospital

- Public Access market

- Alternate Care Market

- Home

By Country

- KSA

- UAE

- Israel

- rest of the GCC countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- rest of MEA

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com