Middle East and Africa Peanut Butter Market Research Report – Segmented Based on Product (Crunchy, Creamy, and Others (Flavored/Specialty)), Brand Type, Distribution Channel, and Country (KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, rest of MEA) - Analysis on Market Size, Share, Trends, & Growth Forecast (2026 to 2034)

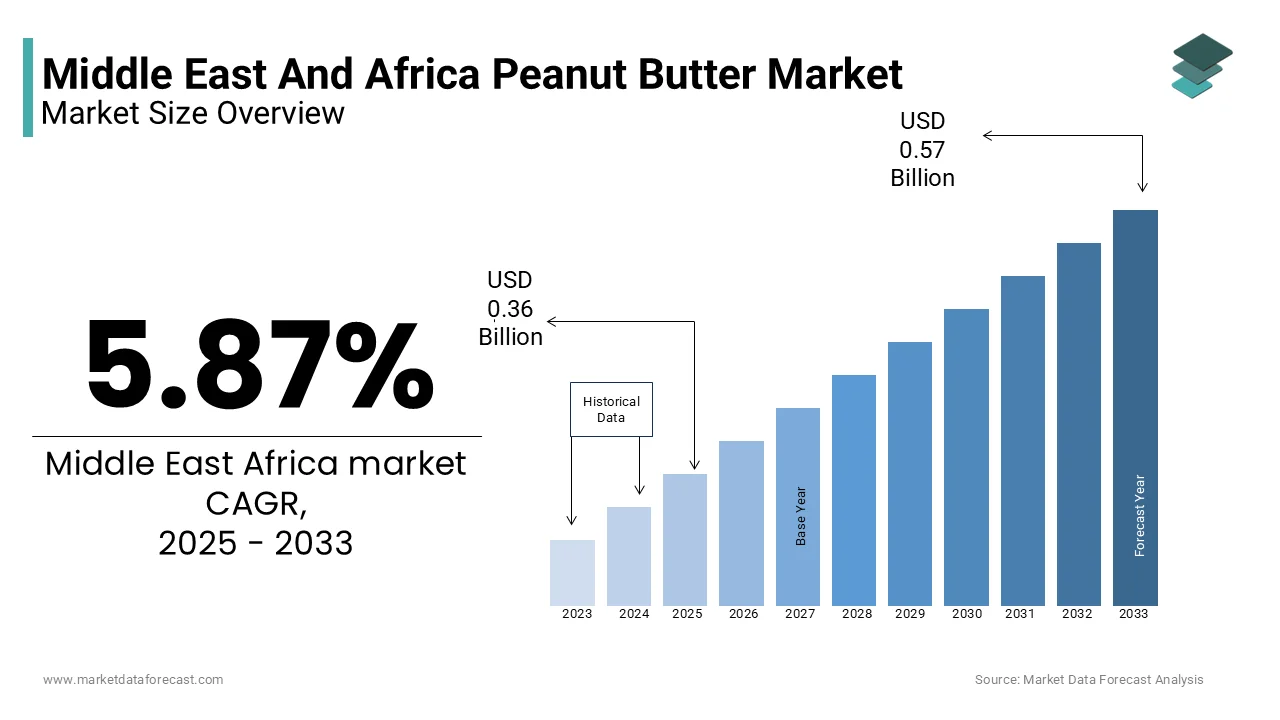

Market Size, 2025

$360.94 MnMarket Estimate, 2026

$382.13 MnMarket Forecast, 2034

$603.11 MnCAGR, 2026–2034

5.87%Middle East and Africa Peanut Butter Market Size

The Middle East and Africa Peanut Butter market was valued at USD 360.94 million in 2025 and is anticipated to reach USD 603.11 million by 2034 from USD 382.13 million in 2026, with a CAGR of 5.87% during the forecast period.

Peanut butter refers to the peanut-based spreads. The region exhibits a fragmented landscape which is known for informal sector dominance, localized production, and growing urban demand. As per the study, peanut cultivation in Sub-Saharan Africa expanded to notable hectares, with countries like Nigeria and Sudan ranking among the top global producers. Concurrently, urbanization rates in Africa surged, as per research, fostering shifts toward processed and convenience foods. These structural changes lay the foundation for increased peanut butter adoption, particularly in urban households seeking affordable protein sources.

MARKET DRIVERS

Protein Gaps and Urban Growth Boost Peanut Butter

The rising demand for affordable plant-based protein sources amid growing food insecurity is primarily boosting the growth of Middle East and Africa peanut butter market. Peanut butter offers a nutrient-dense, low-cost alternative rich in protein, healthy fats, and essential micronutrients because animal protein remains cost-prohibitive for large segments of the population. According to the study, millions of people in Africa faced undernourishment, amplifying the need for accessible protein solutions. Peanuts contain a potion of protein by weight, one of the highest among legumes, as per research. This nutritional profile has prompted integration of peanut-based products into school feeding programs and nutrition interventions across countries like Ethiopia and Malawi. As a result, this normalizes consumption and stimulating commercial demand for processed peanut butter in both rural and urban markets.

Packaged Peanut Products Gain Ground in Expanding Cities

The rapid expansion of urban middle-class populations and their increasing preference for ready-to-eat and packaged foods bolsters the expansion of Middle East and Africa peanut butter. The growth of urban centers and the rise of time-constrained consumers have created a strong demand for convenient shelf-stable food products, providing fertile ground for packaged peanut butter. As per the research, Africa’s middle class expanded to millions of people, with household spending on processed foods rising. In countries like South Africa and Kenya, modern retail penetration has surpassed, which enables wider distribution of branded peanut butter. Apart from these, Western dietary influences and exposure to global food trends through digital media are reshaping consumer perceptions, particularly among younger demographics. This sociocultural shift is fostering acceptance of peanut butter as a breakfast staple or snack, which further accelerates market penetration.

MARKET RESTRAINTS

Food Safety Issues Restrict Peanut Processing Potential

The persistent prevalence of aflatoxin contamination in locally grown peanuts, which impedes food safety and limits commercial scalability, restrains the growth of Middle East and Africa market. Aflatoxins, toxic byproducts of fungal infestation, frequently exceed safe limits in peanut crops due to inadequate post-harvest drying and storage infrastructure. This contamination not only restricts export potential but also deters investment in large-scale processing facilities. Moreover, consumer distrust in locally produced peanut butter persists due to sporadic food safety scares, which compels import reliance in wealthier Gulf states and hindering the growth of regional value chains.

Lack of Processing Infrastructure Slows Peanut Industry

The underdeveloped processing infrastructure across most of the region, which limits the transition from raw peanut farming to value-added product manufacturing, is a barrier hampering the expansion of Middle East and Africa peanut butter market. The majority of peanut production remains in the hands of smallholder farmers who lack access to mechanized shelling, roasting, and grinding technologies. As per the study, less share of peanuts produced in East and West Africa undergo industrial processing, with a portion being sold raw or semi-processed. This deficiency in downstream capabilities results in high production costs, inconsistent product quality, and limited shelf life, factors that deter mainstream retail adoption. Apart from these, inconsistent power supply and poor transportation networks in rural production zones further impede the establishment of centralized processing units, which constrains the market’s ability to scale efficiently.

MARKET OPPORTUNITIES

Fortification Links Peanut Products to Health Solutions

The fortification of peanut butter with micronutrients to address widespread malnutrition, particularly among children and pregnant women, offers potential opportunities for the growth of Middle East and Africa market. Ready-to-Use Therapeutic Foods (RUTFs), such as Plumpy’Nut, already utilize peanut paste as a base, demonstrating the feasibility and efficacy of such interventions. Expanding this model to commercially available, fortified peanut butter could bridge the gap between clinical nutrition and mass-market products. Partnerships between public health agencies and food processors in countries like Uganda and Senegal are already piloting such initiatives. This signals a growing convergence between public health goals and commercial food innovation.

E-Commerce Opens New Doors for Peanut Product Growth

The expansion of e-commerce and digital retail platforms, which are enabling broader market access for peanut butter brands, especially in underserved regions, creates new opportunities for the Middle East and Africa peanut butter market. As smartphone penetration in Africa surged, according to the study, digital marketplaces have become important channels for packaged food distribution. These platforms allow small and medium-sized producers to bypass traditional retail gatekeepers and reach urban consumers directly. In Egypt and South Africa, online grocery sales grew, as per the research. This digital shift lowers entry barriers for local brands, facilitates consumer education on peanut butter benefits, and enables real-time feedback loops for product improvement. This positions e-commerce as a transformative force in the region’s evolving peanut butter landscape.

MARKET CHALLENGES

Climate Shifts Threaten Peanut Supply and Price Stability

The volatility in peanut supply due to climate change-induced weather disruptions, which threaten crop yields and price stability, is a constraint impacting the growth rate of Middle East and Africa market. Peanut farming in the region is predominantly rain-fed by making it highly susceptible to shifting precipitation patterns and prolonged droughts. According to the study, West Africa experienced a decline in growing season rainfall between 1970 and 2020, directly impacting peanut productivity. Such fluctuations disrupt supply chains, increase raw material costs, and discourage long-term investment in processing infrastructure. Hence, the regional market is vulnerable to recurring production shocks because of inadequate climate-resilient agricultural practices and insufficient irrigation expansion.

Cultural Favorites Limit Growth of Peanut-Based Spreads

The intense competition from traditional spreads and local alternatives impairs the expansion of Middle East and Africa peanut butter market. In many Middle Eastern and African countries, sesame-based tahini, sunflower butter, and indigenous nut pastes remain culturally entrenched and widely consumed. As per the study, Cultural and Scientific Organization, tahini consumption in Egypt and Lebanon exceeds kilograms per capita annually, deeply embedded in daily diets through dishes like hummus and halva. Similarly, in West Africa, shea butter and locust bean paste hold strong regional preference due to cultural familiarity and lower cost. These alternatives not only dominate taste preferences but also benefit from established supply chains and lower import dependency, which makes it difficult for peanut butter to gain significant market share without substantial consumer education and product localization.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.87% |

| Segments Covered | By Product, Brand Type, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | KSA, UAE, Israel, South Africa, And Ethiopia, Kenya, Egypt, Sudan, Rest of GCC Countries, and Rest of MEA |

| Market Leaders Profiled | Procter & Gamble, Unilever, The J.M. Smucker Company, Hormel Foods Corporation, Boulder Brands Inc., Kraft Canada Inc. and Algood Food Company Inc, and others. |

SEGMENTAL ANALYSIS

By Product Insights

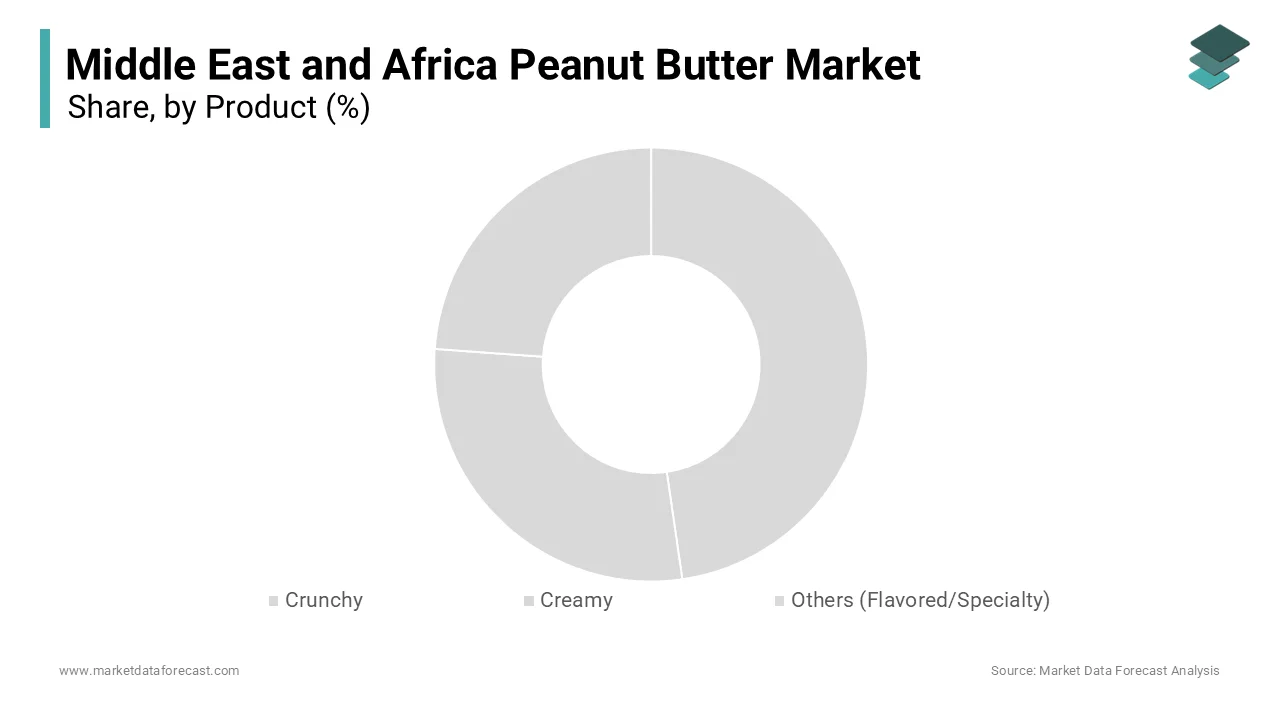

In 2025, the creamy peanut butter segment led the Middle East and Africa peanut butter market by occupying a share of 58.5% in the regional market. Superior spreadability and sensory attributes that align with consumer expectations for smooth texture and ease of use, particularly in household and institutional settings, are largely propelling the growth of creamy peanut butter segment in the regional market. The preference for creamy variants is especially pronounced in urban centers where it is commonly consumed with bread, in sandwiches, or as a base for sauces and desserts. According to a study, a portion of peanut butter buyers cited texture as a decisive factor in their purchase, with creamy formulations scoring highest in palatability and child-friendliness. This sensory advantage has strengthened its position as the default choice in both retail and foodservice applications. Its integration into institutional nutrition programs, where consistency and ease of dosing are important, also supports the dominance of creamy peanut butter segment in the regional market. These interventions have normalized the consumption of smooth peanut spreads,which indirectly influences consumer habits and retail demand. This strengthens market inertia through branding and distribution strength.

The flavored and specialty peanut butter segment is predicted to witness the highest CAGR of 9.4% from 2023 to 2030 due to the rising demand for differentiated, value-added products among younger, health-conscious urban consumers who view peanut butter not only as a staple but as a gourmet or functional food. The introduction of variants infused with honey, cocoa, cinnamon, or protein enrichment has repositioned peanut butter as a premium snack or fitness supplement, particularly in affluent markets like the UAE and South Africa. Rapid expansion is the increasing presence of artisanal and niche producers leveraging social media and direct-to-consumer models to capture market share is another factor accelerating the flavored and specialty segment’s in regional market. In Kenya and Nigeria, startups have introduced organic, sugar-free, and spice-infused peanut butters that cater to evolving dietary preferences. These brands benefit from agile production and localized marketing, enabling them to respond swiftly to consumer feedback. This digital-native approach has accelerated trial and adoption, particularly among millennials and expatriate communities, which fuels the segment’s disproportionate growth trajectory.

By Brand Type Insights

The branded segment dominated the Middle East and Africa peanut butter market and held 62.4% of the regional market share in 2025. The growth of branded segment is majorly attributed to the consumer trust in established quality standards, consistent branding, and wide distribution networks, particularly in formal retail channels. Major multinational and regional brands such as Savola (Saudi Arabia), Bama (Nigeria), and Kraft Heinz (via imports in GCC countries) have strengthened their presence through aggressive marketing and shelf visibility. The trust is especially crucial in markets where food safety concerns persist, making brand reputation a decisive purchase factor. Strategic partnerships with hypermarkets and e-commerce platforms, which ensures superior product placement and promotional support is amplifying the prominence of branded segment in regional market. In the UAE, for instance, branded peanut butter accounts for a portion of supermarket sales, as per study. These brands also benefit from economies of scale in production and packaging, allowing them to maintain competitive pricing while investing in innovation.

The private-label segment is on the rise and is expected to be the fastest growing segment in the regional market by witnessing a CAGR of 8.7% from 2026 to 2034. Factors such as the increasing retail consolidation and the expansion of modern grocery chains that leverage their own-label products to enhance margins and customer loyalty are primarily boosts the growth of private-label segment in the regional market. Retailers such as Shoprite, Pick n Pay in South Africa, and Lulu Hypermarket across the GCC have aggressively expanded their private-label peanut butter offerings, often priced lower than national brands. Economic volatility, including currency devaluations in Nigeria and Egypt, has further incentivized cost-conscious shoppers to switch to store brands without compromising on basic quality. The improvement in manufacturing standards and packaging quality, which has diminished the historical perception gap between store brands and premium labels is also a reason behind the expansion of private-label segment in the regional market. Many retailers now source from the same contract manufacturers used by branded companies, ensuring comparable product consistency. Apart from these, retailers are investing in sustainability messaging, such as recyclable packaging and local sourcing. This aligns with evolving ethical consumption trends and further accelerating adoption.

By Distribution Channel Insights

The supermarkets and hypermarkets segment led the Middle East and Africa peanut butter market by capturing a 54.4% of the regional market share in 2025. The dominance of the supermarkets and hypermarkets segment is driven by the sector’s ability to offer a wide product assortment, consistent availability, and trusted quality assurance, factors that are particularly important for perishable and processed food items. According to the research, the floor space of organized retail in Africa grew, driven by rising consumer demand for hygiene, convenience, and brand transparency. These stores also serve as important platforms for product sampling, promotional discounts, and brand visibility, further strengthening their centrality in the peanut butter supply chain. Their integration with supply chain infrastructure and cold storage capabilities, ensuring product freshness and minimizing spoilage, is an additional growth factor for the supermarkets and hypermarkets segment in the regional market. Moreover, supermarkets are the primary channel for branded and private-label peanut butter alike, enabling coexistence of premium and economy options under one roof. This dual availability caters to diverse income groups, making supermarkets a universal access point and consolidating their role as the backbone of peanut butter distribution.

The online stores segment is anticipated to witness the fastest CAGR of 12.3% over the forecast period owing to the rapid digitization of consumer behavior, particularly in urban centers where smartphone penetration and internet access have surged. Platforms have integrated peanut butter into bundled grocery kits and subscription models, enhancing convenience and repeat purchases. The growth of online stores is further propelled by targeted digital marketing and personalized promotions that drive trial and loyalty. Algorithms on platforms like Amazon.ae and Kimi.com in Egypt recommend peanut butter based on dietary preferences such as high-protein or gluten-free diets, increasing relevance and conversion. Apart from these, e-commerce enables access to specialty and imported variants, such as organic or American-style brands, that are unavailable in physical stores outside major cities. As per the study, cross-border e-commerce in Africa expanded, allowing consumers in remote areas to purchase premium peanut butter directly. This democratization of access, cash-on-delivery options and same-day fulfillment in cities have cemented online retail as the most dynamic channel in the region’s peanut butter ecosystem.

REGIONAL ANALYSIS

The African region dominated the Middle East and Africa's peanut butter market revenue due to the wide adoption of healthy food products. Increasing awareness among people regarding the health benefits of peanut butter is increasing the country's market revenue. As peanut butter can be the go-to option for breakfast and snacks, people are encouraged to adopt it due to their busy, sedentary lifestyle. The growing population across the GCC countries, with an awareness of peanut butter, contributes to the region's market growth. Most people in GCC countries prioritize healthier dietary choices, escalating the demand for peanut butter with a protein-rich and natural ingredient profile. The increasing marketing strategies and efforts by the manufacturers to promote peanut butter health benefits and flavors are raising the market revenue across countries like the UAE and Israel. Saudi Arabia is the most significant contributor to the GCC peanut butter market as it consists of a substantial market share of peanut butter.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

- Procter & Gamble

- Unilever

- The J.M. Smucker Company

- Hormel Foods Corporation

- Boulder Brands Inc.

- Kraft Canada Inc.

- Algood Food Company Inc.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the Middle East and Africa peanut butter market are deploying a range of strategic initiatives to consolidate their presence and capture emerging opportunities. Major companies are investing in localized production to reduce costs and ensure supply chain resilience, particularly in peanut-rich countries like Nigeria and Sudan. Product innovation is a central focus, with firms launching flavored, fortified, and health-oriented variants to appeal to evolving consumer preferences. Strategic partnerships with retailers and e-commerce platforms are enhancing distribution reach, especially in urban centers. Apart from these, brands are emphasizing halal certification and clean labeling to build consumer trust. Marketing campaigns leveraging digital platforms are being used to educate consumers on peanut butter’s nutritional benefits. Some firms are also integrating sustainability into operations, from sourcing to packaging, to align with global and regional environmental standards.

COMPETITIVE OVERVIEW

The competitive landscape of the Middle East and Africa peanut butter market is characterized by a mix of multinational corporations, regional powerhouses, and agile local producers vying for consumer attention across diverse economic and cultural terrains. While established brands dominate formal retail channels through strong distribution and branding, a growing number of artisanal and digital-native startups are capturing niche segments with innovative, health-focused products. Competition is intensifying as companies differentiate through product formulation, packaging, and targeted marketing. The informal sector remains influential in rural areas, posing a challenge to standardized branding. At the same time, rising consumer awareness, urbanization, and dietary shifts are creating space for both premium and affordable offerings. Strategic investments in local processing, food safety compliance, and e-commerce integration are becoming important success factors in this fragmented yet rapidly evolving market.

TOP PLAYERS IN THE MARKET

Savola Group (Saudi Arabia)

Savola Foods, a leading consumer goods company based in Saudi Arabia, plays a pivotal role in shaping the peanut butter landscape across the Gulf and North Africa. The company markets its peanut butter under the popular Almarai brand, leveraging its robust dairy and food distribution network to ensure wide retail availability.

Bama Foods (Nigeria)

Bama Foods is a dominant force in West Africa’s peanut butter sector, renowned for its localized production and deep market penetration in Nigeria and neighboring ECOWAS countries. Bama has extended its reach to younger, urban consumers by leveraging digital marketing and partnering with e-commerce platforms. Its grassroots distribution model, which includes direct engagement with small retailers, which ensures availability even in semi-urban and rural markets. This strengthens its position as a homegrown market leader.

Ruprecht (South Africa)

Ruprecht, a well-established South African food manufacturer, has been instrumental in shaping consumer preferences for premium peanut butter in Southern Africa. Known for its creamy and crunchy variants made from high-grade roasted peanuts, the brand emphasizes natural ingredients and minimal additives, appealing to health-oriented demographics. The company also enhanced its sustainability profile by adopting recyclable packaging and reducing carbon emissions across its Cape Town production site. Ruprecht actively participates in food expos and wellness campaigns, supporting brand visibility. Its focus on quality, innovation, and clean labeling has positioned it as a preferred domestic alternative to imported brands, particularly among urban middle- and upper-income households.

MARKET SEGMENTATION

This research report on the Middle East and Africa peanut butter market has been segmented and sub-segmented based on the following categories.

By Product

- Crunchy

- Creamy

- Others (Flavored/Specialty)

By Brand Type

- Branded

- Private-Label

- Others (Artisanal and Specialty manufacturers)

By Distribution Channels

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Stores

By Country

- KSA

- UAE

- Israel

- rest of GCC countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- rest of MEA

Frequently Asked Questions

1. What is the Middle East & Africa peanut butter market?

It’s the regional industry producing and selling peanut butter for retail, foodservice, and bakery sectors.

2. What drives growth in this market?

Rising health awareness, urban snacking trends, and demand for protein-rich spreads fuel market growth

3. Which countries lead this market?

Saudi Arabia, the UAE, and South Africa hold the largest market shares.

4. Which segment is growing fastest?

Organic and natural peanut butter are rising fastest as clean-label demand increases.

5. What challenges affect this market?

Price volatility of peanuts, limited cold storage, and competition from other spreads impact growth.

6. How are distribution channels evolving?

E-commerce, supermarkets, and hypermarkets are expanding availability across the region.

7. What future trends will shape this market?

Trends include fortified peanut butter, innovative flavors, and sustainable packaging.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com