Middle East and Africa Veterinary Vaccines Market Size, Share, Trends & Growth Forecast Report By Type (Livestock Vaccines, Companion Vaccines), Technology and Country (KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan and Rest of Middle East and Africa), Industry Analysis From 2026 to 2034

Middle East and Africa Veterinary Vaccines Market Report Summary

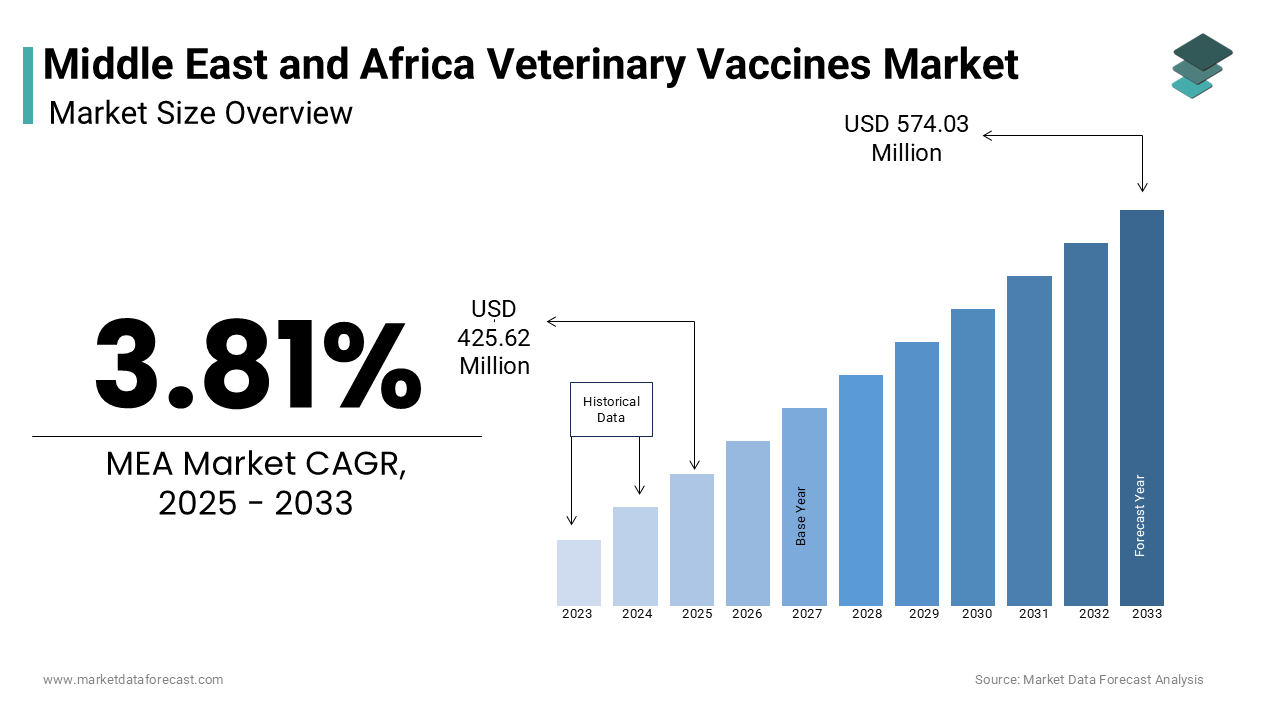

The Middle East and Africa veterinary vaccines market was valued at USD 425.62 million in 2025, is estimated to reach USD 441.84 million in 2026, and is projected to reach USD 595.91 million by 2034, growing at a CAGR of 3.81% during the forecast period from 2026 to 2034. The growth of the Middle East and Africa veterinary vaccines market is driven by the expanding livestock population, rising prevalence of zoonotic diseases, and increasing government initiatives focused on animal health and food security. Growing adoption of preventive animal healthcare practices, increasing investments in veterinary infrastructure, and rising awareness regarding livestock productivity are further accelerating market growth. Moreover, advancements in recombinant vaccine technologies, expansion of regional vaccine manufacturing initiatives, and increasing adoption of digital animal health platforms are supporting the expansion of the Middle East and Africa veterinary vaccines market.

Key Market Trends

- Rising adoption of thermostable veterinary vaccines suitable for tropical climates and infrastructure-constrained rural environments.

- Growing investments in regional veterinary vaccine manufacturing to reduce import dependency and improve supply chain resilience.

- Increasing implementation of One Health initiatives integrating animal health and public health surveillance systems.

- Strong focus on digital livestock monitoring and vaccination tracking platforms to improve disease surveillance and immunization coverage.

- Expansion of commercial poultry and livestock farming operations driving demand for advanced preventive healthcare solutions.

Segmental Insights

- Based on type, the livestock vaccines segment dominated the Middle East and Africa veterinary vaccines market and held the largest share in 2025. The segment’s dominance is attributed to the region’s extensive livestock population, growing economic dependence on animal agriculture, and increasing government-led vaccination programs targeting transboundary animal diseases such as Foot and Mouth Disease and Newcastle disease.

- The poultry vaccines segment is projected to witness the fastest CAGR during the forecast period owing to rapid commercialization of poultry production systems, rising awareness regarding biosecurity practices, and increasing demand for export-compliant poultry health management solutions.

- Based on technology, the live attenuated vaccines segment accounted for the leading share of the Middle East and Africa veterinary vaccines market in 2025. The dominance of this segment is driven by its strong immunological efficacy, cost-effectiveness, ease of administration, and long-standing regulatory acceptance across regional veterinary healthcare systems.

- The recombinant vaccines segment is anticipated to register notable growth during the forecast period due to increasing technological advancements, rising demand for safer multivalent vaccines, and growing investments in thermally stable vaccine formulations suitable for remote rural environments.

Regional Insights

South Africa dominated the Middle East and Africa veterinary vaccines market and accounted for the largest share in 2025, supported by advanced veterinary infrastructure, strong regulatory frameworks, and significant livestock production activities. Saudi Arabia remains a major contributor to the market due to extensive investments in livestock health infrastructure under Vision 2030, increasing focus on domestic protein production, and expansion of commercial poultry and dairy operations. Egypt continues to maintain a prominent position owing to its growing domestic vaccine manufacturing capabilities, strong poultry production sector, and increasing regional export ambitions. The United Arab Emirates and Kenya are also witnessing notable growth driven by expanding veterinary healthcare investments, increasing adoption of advanced animal health technologies, and strengthening disease surveillance initiatives.

Competitive Landscape

The Middle East and Africa veterinary vaccines market is highly competitive and characterized by the presence of multinational animal health companies, regional vaccine manufacturers, and biotechnology firms competing through innovation, localized manufacturing, and strategic partnerships. Leading companies are focusing on expanding thermostable vaccine portfolios, strengthening regional distribution networks, investing in digital animal health platforms, and enhancing local manufacturing capabilities. Strategic collaborations with government agencies, veterinary institutions, and international development organizations are further strengthening market positioning across Middle Eastern and African animal healthcare systems. Prominent players in the Middle East and Africa veterinary vaccines market include Bayer HealthCare AG, Bioniche Animal Health Canada, Sanofi Animal Health Inc., Biogenesis Bago SA, Heska Corporation, Indian Immunologicals Ltd., Boehringer Ingelheim GmbH, Zoetis, Novartis Animal Health Inc., Merck & Co., Inc., and Protein Sciences.

Middle East and Africa Veterinary Vaccines Market Size

The veterinary vaccines market size in the Middle East and Africa was valued at USD 425.62 million in 2025. The regional market size is poised to reach USD 595.91 million by 2034 from USD 441.84 million in 2026, growing at a CAGR of 3.81% from 2026 to 2034.

Veterinary vaccines are biological preparations that provide immunity to animals against various infectious diseases, enhancing their health and productivity. The reliance of the Middle East and Africa on livestock for food production and economic sustenance has elevated the demand for veterinary vaccines in this region. According to the Food and Agriculture Organization, livestock contributes over 40% of agricultural GDP in Africa. Government initiatives and international partnerships are fostering regional market growth. For instance, the World Organisation for Animal Health collaborates with regional governments to improve vaccine accessibility and disease surveillance. South Africa and Kenya are prominent markets for veterinary vaccines in this region.

MARKET DRIVERS

Expanding Livestock Populations Drive Preventive Healthcare Adoption

The substantial and growing livestock base across the regional territories fuels the growth of the Middle East and Africa veterinary vaccines market. This creates sustained demand for veterinary vaccines as a primary preventive intervention. Africa maintains approximately 350 million cattle and over 2 billion poultry, according to FAO data, representing a massive reservoir for potential disease spread. This immense animal population requires systematic health management to safeguard productivity minimize mortality and ensure food security for rapidly urbanizing communities. Smallholder farmers, who manage approximately 80% of livestock in Sub-Saharan Africa, are increasingly targeted for vaccination uptake to secure household income and food security. National agricultural policies in countries such as Saudi Arabia and South Africa explicitly prioritize animal health infrastructure under broader food sovereignty frameworks. Saudi Arabia’s Vision 2030 actively allocates resources toward livestock vaccination programs, specifically targeting Avian Influenza and Foot and Mouth Disease (FMD), to boost domestic protein self-sufficiency and biosecurity. The correlation between livestock density and vaccine utilization intensifies as commercial farming operations expand to meet rising regional demand for meat and dairy products. Veterinary service providers respond to this structural demand by scaling distribution networks and introducing thermostable vaccine formulations suitable for remote rural settings. The preventive healthcare paradigm is gaining traction as producers realize that economic losses from unchecked disease outbreaks can exceed vaccination costs by a benefit-cost ratio of 16:1 or higher in high-impact scenarios, according to global vaccine economic models. This rational economic calculus underpins consistent procurement patterns and reinforces the foundational role of vaccines within integrated animal health management systems across the region.

Rising Zoonotic Disease Burden Accelerates One Health Investment

The persistent prevalence of zoonotic pathogens across the territories in the region stimulates coordinated public and private investment in veterinary vaccines as a critical One Health intervention, which in turn drives the expansion of the Middle East and Africa veterinary vaccines market. Rabies, bovine tuberculosis, leptospirosis, and brucellosis occur broadly across the Middle East and Africa, confirming analysis published in the European Journal of Public Health. These diseases transmit between animals and humans creating dual pressure on veterinary and public health systems to implement preventive vaccination strategies. The World Organisation for Animal Health (WOAH) identifies rabies as a persistent, endemic threat across African territories, causing an estimated 59,000 human deaths globally per year (mostly in Africa and Asia). Government agencies increasingly adopt integrated surveillance frameworks that link animal vaccination coverage with human disease incidence metrics. International partners such as FAO and WOAH support cross sectoral initiatives that strengthen laboratory capacity cold chain logistics and community based vaccination delivery. In East Africa, recent outbreaks of Marburg virus and Ebola have heightened awareness of One Health surveillance and wildlife reservoir monitoring, while vaccination efforts remain focused on distinct preventable livestock diseases like Rift Valley Fever. Veterinary vaccine manufacturers respond by prioritizing multivalent formulations and thermally stable products suitable for tropical climates and limited infrastructure settings. The economic case for One Health is robust; the World Bank and other agencies estimate that investments in animal health systems generate significant returns, with some models showing that every dollar invested in zoonotic disease prevention generates $16 or more in avoided health costs and socioeconomic losses. This evidence based approach encourages policy makers to allocate dedicated budget lines for veterinary immunization within national health security strategies. The convergence of epidemiological necessity economic justification and institutional coordination creates a powerful demand driver for veterinary vaccines throughout the Middle East and Africa region.

MARKET RESTRAINTS

Limited Veterinary Workforce Density Constrains Vaccine Delivery

The scarcity of qualified veterinary professionals across many MEA territories significantly impedes effective vaccine distribution administration and monitoring which hampers the overall growth of the Middle East and Africa veterinary vaccines market. South Africa maintains roughly 60 to 70 veterinarians per million population, severely lagging behind the international benchmark of 200 to 400 professionals per million required for robust national disease surveillance. This deficit is more pronounced in rural and remote areas where livestock populations are concentrated yet veterinary services remain inaccessible. The World Organisation for Animal Health (WOAH) through its workforce observatory initiatives highlights that numerous African nations lack complete or up-to-date veterinary workforce data, complicating strategic planning for targeted animal health interventions. Limited human resources translate into inadequate cold chain management improper vaccine storage and suboptimal immunization coverage particularly among smallholder farmers. Paraprofessional cadres including animal health workers and community based vaccinators help bridge the gap but often lack standardized training and regulatory oversight. To alleviate severe doctor shortages, Eastern and Southern African territories rely heavily on veterinary paraprofessionals and community-based animal health workers, who frequently outnumber registered veterinarians and act as the primary frontline for vaccine delivery. This dependency on paraprofessionals introduces variability in vaccine handling protocols and record keeping practices that can compromise immunization efficacy. Government budgets frequently prioritize urban veterinary clinics over rural outreach programs further exacerbating geographic disparities in service availability. The workforce constraint also limits post vaccination surveillance and adverse event reporting which are essential for maintaining vaccine confidence and optimizing formulation strategies. The region will struggle to achieve meaningful improvements in vaccine coverage despite growing product availability and policy support. This is largely because it lacks targeted investments in veterinary education recruitment and retention.

Inadequate Cold Chain Infrastructure Limits Vaccine Efficacy

The insufficient cold chain infrastructure poses a significant restraint on veterinary vaccine potency and field effectiveness, which inhibits the expansion of the Middle East and Africa veterinary vaccines market. Temperature sensitive biological products require uninterrupted refrigeration from manufacturing to administration yet many rural distribution points lack reliable electricity or specialized storage equipment. Field assessments by international agricultural development agencies indicate that inadequate cold chain infrastructure remains a leading cause of veterinary vaccine spoilage and potency loss across rural Sub-Saharan African distribution networks. This wastage not only represents financial inefficiency but also undermines farmer confidence when immunization campaigns fail to deliver expected disease protection. Solar powered refrigeration units and thermostable vaccine formulations offer partial solutions but remain cost prohibitive for widespread deployment among resource constrained smallholder operations. Transportation logistics present additional challenges as remote pastoral communities often require multi day journeys using unpaved roads that expose vaccines to temperature fluctuations and physical damage. National veterinary authorities in major livestock-producing nations, including Nigeria and Ethiopia, have initiated target infrastructure modernization programs, though progress remains uneven due to restricted public budgets and technical capacity limits. As emphasized by WOAH and FAO guidelines, building a reliable, uninterrupted cold chain framework is an absolute prerequisite for achieving the high herd-immunity coverage targets needed to eradicate transboundary animal diseases. Without systematic investment in temperature monitoring devices backup power systems and trained logistics personnel the region will continue to experience preventable vaccine failures that erode the economic and health benefits of immunization programs. This infrastructure gap represents a fundamental barrier that must be addressed to unlock the full potential of veterinary vaccines across Middle East and Africa markets.

MARKET OPPORTUNITIES

Digital Health Platforms Enable Precision Vaccination Strategies

The emergence of digital health technologies creates a pathway for optimizing veterinary vaccine deployment and monitoring across regional territories, which is expected to boost the growth of the Middle East and Africa veterinary vaccines market. Mobile based livestock registration systems and geospatial mapping tools enable authorities to identify high risk zones prioritize vaccination campaigns and track coverage in real time. The World Organisation for Animal Health (WOAH) actively promotes digital transformation through its WAHIS platform, encouraging members to digitize animal disease reporting to support evidence-based decision-making. Startups and development partners are piloting blockchain enabled vaccine traceability solutions that enhance supply chain transparency and reduce counterfeit product infiltration. In Kenya and Tanzania, mobile-based platforms have improved community disease reporting (e.g., surveillance of Rift Valley Fever), though "48-hour" targeted vaccination deployment remains an aspirational pilot metric rather than a standard national capability due to logistical constraints. These technologies also empower smallholder farmers through SMS based reminders for booster doses and access to verified veterinary service providers. The scalability of digital solutions is particularly valuable in pastoral systems where livestock mobility complicates traditional vaccination approaches. International funding agencies, including the Gates Foundation and FAO, increasingly prioritize digital innovation in animal health grants to improve data quality and surveillance cost-effectiveness. As smartphone penetration and mobile network coverage expand across rural Africa the addressable market for digital veterinary services grows commensurately. This convergence of technological capability epidemiological need and institutional support positions digital health platforms as a high impact opportunity for enhancing vaccine coverage and animal health outcomes throughout the region.

Regional Manufacturing Initiatives Enhance Vaccine Access and Affordability

The strategic development of regional vaccine manufacturing capabilities provides a significant opportunity to improve product accessibility reduce import dependency and lower costs across Middle East and Africa markets. South Africa's recent launch of a domestically produced Foot and Mouth Disease vaccine marks a milestone in regional biopharmaceutical sovereignty according to Agricultural Research Council announcements. Local production shortens supply chains minimizes currency exposure and enables formulation customization for regionally prevalent disease strains. The African Union's Partnership for African Vaccine Manufacturing (PAVM) has set a continental target to manufacture 60% of Africa’s vaccines locally by 2040, creating an expanded industrial base and policy framework that indirectly supports investment in veterinary biologics. Technology transfer agreements between international manufacturers and African research institutions accelerate knowledge diffusion and quality assurance capability building. Regional regulatory harmonization for veterinary products is progressing chiefly through Regional Economic Communities (RECs) and the VMP (Veterinary Medicinal Products) workstream of the African Medicines Regulatory Harmonisation (AMRH) initiative, making the approval pathway for locally produced animal vaccines more predictable. These initiatives align with broader industrialization agendas that seek to capture value within regional economies rather than relying on imported finished products. The economic multiplier effect of local manufacturing extends beyond vaccine availability to include job creation skills development and ancillary service sector growth. Governments in Saudi Arabia (under Vision 2030) and the UAE are developing broad biotechnology and life sciences hubs that offer tax incentives and infrastructure suitable for pharmaceutical manufacturing, including potential capacity for animal health products. This manufacturing opportunity represents a structural shift that can enhance supply security price stability and product relevance for Middle East and Africa animal health stakeholders.

MARKET CHALLENGES

Climate Variability Disrupts Disease Patterns and Vaccination Schedules

Increasing climate variability across the region introduces unpredictability into animal disease epidemiology and complicates veterinary vaccination planning. This challenges the growth of the Middle East and Africa veterinary vaccines market. Shifting rainfall patterns, temperature extremes, and prolonged droughts alter vector habitats, host susceptibility, and pathogen transmission dynamics, according to peer-reviewed veterinary and climate research. The Food and Agriculture Organization (FAO) notes that climate-driven changes in traditional pastoralist livestock migration routes alter animal density and movement patterns, increasing exposure to transboundary animal diseases and complicating the geographic targeting of regional vaccination campaigns. Traditional immunization calendars based on historical seasonal patterns become less reliable as disease outbreaks occur outside expected windows. Extreme weather events can damage cold chain infrastructure disrupt transportation networks and displace livestock populations undermining vaccination coverage achievements. Pastoral communities who rely on seasonal mobility for livestock management face additional complexity when climate anomalies force unplanned movements that intersect with disease endemic zones. Veterinary authorities must invest in climate resilient surveillance systems that incorporate meteorological data to anticipate outbreak risks and adjust vaccination strategies dynamically. The economic burden of climate related vaccine program adjustments falls disproportionately on smallholder farmers who lack financial buffers to absorb repeated immunization costs. Public and private research institutions are actively developing thermostable veterinary vaccine strains and flexible, community-based delivery protocols to withstand extreme temperatures, though scaling these logistics requires sustained public-private funding and cross-sectoral coordination. The region has made substantial vaccine investments. However, without proactively integrating climate science into animal health planning, it still risks inefficient resource allocation and suboptimal disease control outcomes.

Regulatory Fragmentation Hinders Cross Border Vaccine Trade and Adoption

The absence of harmonized regulatory frameworks creates significant barriers to efficient distribution of these vaccines and the Middle East and Africa veterinary vaccines market expansion. National approval processes vary considerably in documentation requirements testing protocols and timelines delaying product registration and market entry. The World Organisation for Animal Health (WOAH) advocates for the international harmonization of regulatory standards to streamline the cross-border trade of veterinary biologics while rigorously ensuring global safety, efficacy, and quality control metrics. However implementation remains inconsistent with some countries requiring redundant clinical trials or imposing import restrictions that limit product availability. This fragmentation increases compliance costs for manufacturers who must navigate multiple approval pathways for regionally relevant vaccines. Small and medium enterprises face disproportionate burdens as they lack resources to manage complex multi jurisdictional registration processes. The resulting market inefficiencies reduce competition limit farmer choice and keep prices elevated relative to production costs. Regional economic communities such as the East African Community and Economic Community of West African States have initiated harmonization efforts but progress is gradual due to sovereignty concerns and capacity constraints. The lack of mutual recognition agreements for vaccine quality certifications further complicates cross border procurement and emergency response coordination during disease outbreaks. The region will continue to experience suboptimal vaccine access until regulatory systems achieve greater alignment. This lack of alignment leads to delayed innovation adoption and fragmented market development that constrains the full potential of veterinary immunization programs.

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.81% |

| Segments Covered | By Type, Technology and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | KSA, UAE, Israel, Rest of GCC Countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, and Rest of MEA. |

| Market Leaders Profiled | Bayer HealthCare AG, Bioniche Animal Health Canada, Sanofi Animal Health Inc., Biogenesis Bago SA, Heska Corporation, Indian Immunologicals Ltd., Boehringer Ingelheim GmbH, Zoetis, Novartis Animal Health Inc., Merck & Co., Inc., and Protein Sciences. |

SEGMENTAL ANALYSIS

By Type Insights

The livestock vaccines segment held the majority share of 63.5% of the Middle East and Africa Veterinary Vaccines Market in 2025. Factors such as the region's extensive livestock base and economic dependence on animal agriculture are contributing to the supremacy of this segment. The immense animal inventory generates consistent demand for immunization products targeting Foot and Mouth Disease Newcastle disease and other endemic pathogens. Smallholder farmers, who manage approximately 80% of livestock in Sub-Saharan Africa, are increasingly integrated into targeted vaccination programs to protect vital household assets and rural income streams. Government programs in Saudi Arabia and South Africa prioritize livestock health under national food security frameworks allocating budget resources for mass immunization campaigns. Commercial dairy and beef operations expanding to meet urban protein demand require systematic vaccination protocols to maintain herd productivity and minimize mortality losses. The economic rationale strongly favors preventive vaccination; severe transboundary animal disease outbreaks routinely cause catastrophic asset destruction, slashing livestock market value and crippling smallholder farm equity. Veterinary service providers respond by developing thermostable formulations suitable for rural distribution and training paraprofessionals in vaccine administration. This structural demand foundation ensures livestock vaccines remain the dominant revenue generator within the regional veterinary biologics sector.

Furthermore, rising population growth and urbanization across Middle East and Africa territories intensify pressure on governments to secure domestic protein supplies through enhanced livestock productivity. WOAH guidelines emphasize that robust national vaccination coverage is a core pillar for reducing animal mortality, which directly safeguards regional food security and improves overall livestock production metrics. National agricultural policies in Egypt Kenya and Ethiopia explicitly link livestock immunization programs to broader food sovereignty objectives. International development agencies including FAO and GALVmed support vaccine procurement and distribution initiatives targeting smallholder farmers in high disease burden zones. The economic multiplier effect of livestock vaccination extends beyond animal health to include rural employment stabilization and export market access for disease free certified products. Regional trade agreements increasingly require proof of vaccination status for cross border livestock movement creating regulatory incentives for compliance. Public private partnerships facilitate technology transfer for locally adapted vaccine formulations that address regionally prevalent disease strains. This institutional procurement ecosystem sustains consistent demand for livestock vaccines while encouraging product innovation and supply chain resilience across the Middle East and Africa region.

On the contrary, the poultry vaccines segment is anticipated to witness the fastest CAGR of 7.3% between 2026 and 2034 owing to intensification of poultry production systems and heightened biosecurity awareness across the region.

Poultry production across Middle East and Africa territories is rapidly shifting from backyard systems to commercial operations requiring systematic disease prevention protocols. Commercial integrators operating large scale broiler and layer facilities implement comprehensive vaccination schedules to protect capital intensive investments and ensure consistent product quality. Avian influenza outbreaks in Egypt and Nigeria during recent years have heightened industry awareness of preventive immunization value. Technology adoption includes automated vaccination equipment and digital record keeping systems that improve coverage accuracy and regulatory compliance. Feed manufacturers and veterinary service providers bundle vaccine products with technical support creating integrated health management solutions for poultry producers. The economic efficiency of poultry vaccination is highly compelling; the cost of routine vaccine administration represents a negligible fraction of the devastating total financial losses triggered by unchecked outbreaks of highly pathogenic avian influenza or Newcastle disease. This commercial intensification trend positions poultry vaccines as the fastest growing segment within the regional veterinary biologics market.

Moreover, regional poultry producers targeting export markets in Europe and the Gulf Cooperation Council face stringent animal health certification requirements that mandate documented vaccination protocols. WOAH international trade standards dictate rigorous disease status certifications for livestock products, meaning specific regional vaccination policies can heavily dictate or restrict access to premium global export markets. Countries such as South Africa and Saudi Arabia have invested in laboratory capacity and surveillance systems to support export certification processes. Private sector poultry integrators partner with global vaccine manufacturers to access advanced formulations that meet international regulatory expectations. The economic incentive for export oriented production drives premium vaccine adoption even among mid scale producers seeking market differentiation. Regional harmonization efforts through African Union frameworks facilitate mutual recognition of vaccination records reducing trade barriers. This export driven quality imperative creates sustained demand for high efficacy poultry vaccines while encouraging local manufacturing partnerships and technology transfer initiatives across Middle East and Africa territories.

By Technology Insights

The live attenuated vaccines segment was the largest by occupying a 37.1% share of the Middle East and Africa Animal Vaccines Market in 2025. This segment spearhead due to proven efficacy cost effectiveness and established regulatory acceptance.

Live attenuated vaccines deliver robust, long-lasting immune responses by replicating harmlessly within the host organism, making them highly effective tools for controlling transboundary animal diseases in low-resource environments. This characteristic enables single dose protection for many poultry and livestock pathogens reducing administration costs and logistical complexity. Regional vaccine manufacturers in South Africa and Egypt prioritize this technology due to established production expertise and lower capital requirements compared to recombinant platforms. Field performance data from vaccination campaigns in Kenya and Sudan demonstrate high seroconversion rates supporting continued preference among veterinary practitioners. The cost advantage of live attenuated vaccines typically lower than recombinant alternatives. This combination of immunological efficacy operational simplicity and economic accessibility sustains the dominant market position of live attenuated vaccines across Middle East and Africa territories.

In addition, national veterinary authorities across Middle East and Africa maintain well defined approval processes for live attenuated vaccines based on decades of regulatory experience. This regulatory predictability reduces time to market for new products and encourages manufacturer investment in regionally relevant formulations. Technology transfer agreements between international developers and local producers frequently focus on live attenuated platforms due to lower technical barriers and established quality control protocols. Veterinary practitioners express confidence in live attenuated products based on long term field experience creating demand pull that reinforces manufacturer supply decisions. The convergence of regulatory clarity practitioner preference and manufacturing capability creates a self reinforcing cycle that sustains live attenuated vaccines as the leading technology segment within the regional veterinary biologics market.

But the recombinant vaccines segment is projected to register the highest growth rate within the veterinary vaccines market. This swift growth is fuelled by technological advancement and evolving disease control requirements.

Recombinant vaccine technology enables targeted expression of specific pathogen antigens without introducing live organisms according to veterinary biotechnology principles. This approach minimizes adverse reactions and eliminates reversion risk particularly valuable for immunocompromised animals or high value breeding stock. Advanced platforms including viral vectors and subunit expression systems allow multivalent formulations that protect against multiple pathogens with single administration. Research institutions in South Africa and Egypt collaborate with international partners to develop recombinant vaccines targeting regionally prevalent strains of lumpy skin disease and avian influenza. Advancing the recombinant vaccine pipeline, the University of Cape Town engineered a proprietary recombinant Lumpy Skin Disease Virus (LSDV) vector platform, introducing highly adaptive, modular antigen design to African veterinary medicine. Field evaluations of advanced recombinant poultry vaccines in East Africa demonstrate strong seroconversion rates paired with superior thermal stability, allowing these formulations to maintain efficacy even when rural cold chains fail. This technological precision positions recombinant vaccines as the preferred solution for complex disease challenges driving accelerated adoption across commercial livestock and poultry operations.

Furthermore, recombinant vaccine development increasingly prioritizes thermal stability to address cold chain limitations prevalent across rural Middle East and Africa territories. Novel formulation techniques including lyophilization and adjuvant optimization extend product shelf life at ambient temperatures according to biopharmaceutical research. This innovation reduces vaccine spoilage losses in Sub Saharan distribution networks. Mobile vaccination teams serving pastoral communities benefit from thermostable recombinant products that maintain potency during multi day field operations. Government procurement specifications increasingly include thermal stability criteria creating market incentives for manufacturers to invest in advanced formulation capabilities. International development funding supports technology transfer initiatives enabling regional producers to access recombinant platforms with enhanced stability profiles. This convergence of scientific innovation logistical practicality and policy support positions recombinant vaccines as the fastest growing technology segment within the regional veterinary biologics market.

REGIONAL ANALYSIS

South Africa Veterinary Vaccines Market Analysis

South Africa dominated the Middle East and Africa Veterinary Vaccines Market and accounted for a 28.5% share in 2025. The demand for these vaccines was driven by advanced veterinary infrastructure robust regulatory frameworks and significant livestock production. South Africa's animal vaccines landscape generated revenue of 196.1 million United States dollars in 2025. The nation hosts regional headquarters for multiple global animal health companies facilitating technology transfer and local manufacturing partnerships. Government initiatives under the South African Veterinary Strategy prioritize disease surveillance and vaccination coverage for Foot and Mouth Disease and lumpy skin disease. Private sector investment in biopharmaceutical capacity enables domestic production of key vaccines reducing import dependency. Research institutions including the Agricultural Research Council collaborate with international partners on novel vaccine development for regionally relevant pathogens. The convergence of regulatory sophistication manufacturing capability and disease control commitment sustains South Africa's market leadership position across the Middle East and Africa veterinary biologics sector.

Saudi Arabia Veterinary Vaccines Market Analysis

Saudi Arabia followed closely behind in the Middle East and Africa Veterinary Vaccines Market and captured a 18.6% share in 2025. National food security priorities under Vision 2030 drive substantial public investment in livestock health infrastructure and vaccination programs. Government agencies prioritize immunization against avian influenza and Foot and Mouth Disease to protect domestic protein production capacity. The establishment of specialized economic zones for animal health manufacturing offers tax incentives and streamlined regulatory pathways for vaccine producers. Regional trade ambitions encourage alignment with international animal health standards creating demand for high efficacy vaccine products. Private sector poultry and dairy integrators implement comprehensive vaccination protocols to support export oriented production strategies. This combination of policy support infrastructure investment and commercial demand positions Saudi Arabia as a high growth market within the regional veterinary biologics sector.

Egypt Veterinary Vaccines Market Analysis

Egypt is another key player in the Middle East and Africa Veterinary Vaccines Market. The country serves as both a major consumption center and emerging production hub for veterinary biologics. The nation hosts MEVAC a prominent veterinary vaccine manufacturer serving Middle East and Africa territories according to Arab Authority for Agricultural Investment and Development. Government strategy emphasizes localization of vaccine manufacturing to reduce import dependency and enhance supply security. Poultry production intensification drives consistent demand for Newcastle disease and avian influenza vaccines. Regional export ambitions encourage adoption of internationally recognized vaccination protocols supporting market access for Egyptian livestock products. Public private partnerships facilitate technology transfer for advanced vaccine platforms targeting endemic pathogens. This dual role as consumer and producer positions Egypt as a strategically important market within the regional veterinary biologics ecosystem.

United Arab Emirates Veterinary Vaccines Market Analysis

The United Arab Emirates held a promising share of the Middle East and Africa Veterinary Vaccines Market in 2025 due to the fact that it serves as a regional hub for animal health innovation trade and regulatory harmonization. Government initiatives prioritize food security and biosecurity driving investment in advanced veterinary vaccine procurement and distribution systems. The UAE hosts regional offices for multiple global animal health companies facilitating market access across Gulf Cooperation Council territories. Regulatory authorities maintain alignment with international standards creating predictable pathways for product registration and market entry. Private sector demand from commercial poultry and camel operations supports adoption of premium vaccine formulations. The nation's logistics infrastructure enables efficient distribution of temperature sensitive biologics across regional markets. Research collaborations with international institutions support development of vaccines targeting regionally relevant pathogens. This combination of regulatory sophistication logistical capability and commercial demand positions the UAE as a high value market within the regional veterinary biologics sector.

Kenya Veterinary Vaccines Market Analysis

Kenya is expected to grow notably in the Middle East and Africa Veterinary Vaccines Market during the forecast period. The nation serves as a growth center for veterinary biologics adoption across East African territories. Government programs supported by international agencies prioritize vaccination against Newcastle disease and contagious bovine pleuropneumonia to protect smallholder livelihoods. Private sector poultry integrators implement systematic vaccination protocols to support commercial production expansion. Regional trade initiatives encourage harmonization of animal health standards creating incentives for vaccine adoption among livestock exporters. Research institutions collaborate with global partners on development of thermostable vaccine formulations suitable for rural distribution. Mobile vaccination campaigns leveraging digital platforms improve coverage accuracy among pastoral communities. Public private partnerships facilitate technology transfer for locally adapted vaccine products. This convergence of policy support commercial demand and innovation capacity positions Kenya as an emerging high growth market within the regional veterinary biologics sector.

COMPETITIVE LANDSCAPE

Competition within the Middle East and Africa Veterinary Vaccines Market features a dynamic interplay between global multinational corporations and emerging regional manufacturers. Global players leverage advanced research capabilities extensive product portfolios and established regulatory expertise to maintain market leadership positions. Regional manufacturers compete through cost effective production localized formulations and deep understanding of epidemiological and logistical realities. Market dynamics encourage strategic partnerships rather than pure competition as global companies seek local manufacturing partners while regional producers access advanced technologies through licensing agreements. Regulatory harmonization efforts across African Union frameworks create opportunities for scaled distribution while maintaining quality standards. Innovation focus centers on thermostable formulations multivalent products and digital integration to address regional challenges. Price sensitivity among smallholder farmers creates demand for affordable yet efficacious products encouraging tiered pricing strategies. The competitive landscape rewards companies that balance scientific innovation with operational practicality and cultural relevance across diverse Middle East and Africa territories.

KEY MARKET PLAYERS

Companies playing a prominent role in the Middle East and Africa Veterinary Vaccines Market include

- Bayer HealthCare AG

- Bioniche Animal Health Canada

- Sanofi Animal Health Inc.

- Biogenesis Bago SA

- Heska Corporation

- Indian Immunologicals Ltd.

- Boehringer Ingelheim GmbH

- Zoetis

- Novartis Animal Health Inc.

- Merck & Co., Inc.

- Protein Sciences

Top Market Players

Zoetis Inc Global Innovation Leader

Zoetis Inc contributes significantly to the global veterinary vaccines market through advanced research and development capabilities and extensive product portfolios. The company maintains active engagement in the Middle East and Africa region by introducing innovative vaccine formulations targeting regionally prevalent diseases. Recent strategic actions include partnerships with local distributors to enhance product accessibility and technical support services. Zoetis invests in digital health platforms that enable precision vaccination strategies and real time disease monitoring for livestock producers. The company collaborates with regional research institutions to develop thermostable vaccine formats suitable for rural distribution environments. These initiatives strengthen market position by addressing specific epidemiological and logistical challenges across Middle East and Africa territories while leveraging global scientific expertise.

Boehringer Ingelheim Animal Health Integrated Solutions Provider

Boehringer Ingelheim Animal Health delivers comprehensive veterinary vaccine solutions supported by robust manufacturing capabilities and scientific expertise. The company strengthens its Middle East and Africa presence through strategic acquisitions of regional distributors and technology transfer agreements with local producers. Recent initiatives include launch of combination vaccines targeting multiple poultry pathogens and investment in cold chain infrastructure to ensure product integrity. Boehringer Ingelheim collaborates with government agencies on disease surveillance programs that inform vaccine development priorities. The company emphasizes training programs for veterinary practitioners to optimize vaccine administration and coverage outcomes. These integrated approaches enhance market position by aligning product innovation with regional disease control objectives and operational realities.

Merck Animal Health Strategic Partnership Catalyst

Merck Animal Health advances veterinary vaccine accessibility across Middle East and Africa through strategic partnerships and localized manufacturing initiatives. The company recently expanded distribution networks in East Africa and introduced digital tools for vaccine inventory management and coverage tracking. Merck collaborates with international development agencies on vaccination campaigns targeting smallholder farmers and pastoral communities. The company invests in research focused on regionally relevant pathogens including lumpy skin disease and avian influenza. Recent product launches include thermostable poultry vaccines designed for tropical climates and limited infrastructure settings. These efforts strengthen market position by combining global scientific capabilities with region specific solutions that address epidemiological and logistical challenges across Middle East and Africa territories.

Top Strategies Used By Key Market Participants

Key players in the Middle East and Africa Veterinary Vaccines Market employ strategic approaches including technology transfer agreements with regional manufacturers to enhance local production capacity and reduce import dependency. Companies pursue distribution partnerships with established veterinary supply chains to improve product accessibility across rural and remote territories. Investment in thermostable vaccine formulations addresses cold chain limitations prevalent in tropical climates and infrastructure constrained settings. Digital health platforms enable precision vaccination strategies real time disease monitoring and improved coverage documentation for regulatory compliance. Collaborative research initiatives with regional institutions focus on developing vaccines targeting endemic pathogens and emerging disease threats. Training programs for veterinary practitioners and paraprofessionals optimize vaccine administration techniques and enhance field effectiveness. Strategic acquisitions of local distributors strengthen market penetration and customer relationship management across diverse geographic segments.

MARKET SEGMENTATION

This research report on the Middle East and Africa veterinary vaccines market is segmented and sub-segmented into the following categories.

By Type

- Livestock Vaccines

- Bovine

- Porcine

- Ovine

- Poultry

- Equine

- Companion Vaccines

- Feline Vaccines

- Canine Vaccines

By Technology

- Live Attenuated Vaccines

- Inactivated Vaccines

- Recombinant Vaccines

- Toxoid Vaccines

- Subunit Vaccines

- DNA Vaccines

- Conjugate Vaccines

By Country

- KSA

- UAE

- Israel

- rest of GCC countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- rest of MEA

Frequently Asked Questions

What are the key trends influencing the veterinary vaccines market in Africa?

Increasing adoption of companion animals, rising awareness about animal health, and the prevalence of infectious diseases are driving the growth of the veterinary vaccines market in Africa.

Which countries contribute significantly to the veterinary vaccines market in the Middle East?

Saudi Arabia, UAE, and Egypt are among the leading contributors.

Who are the key players in the veterinary vaccines market in the Middle East?

Bayer HealthCare AG, Bioniche Animal Health Canada, Sanofi Animal Health Inc., Biogenesis Bago SA, Heska Corporation, Indian Immunologicals Ltd., Boehringer Ingelheim GmbH, Zoetis, Novartis Animal Health Inc., Merck & Co Inc., and Protein Sciences are some of the major players in the MEA veterinary vaccines market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com