- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

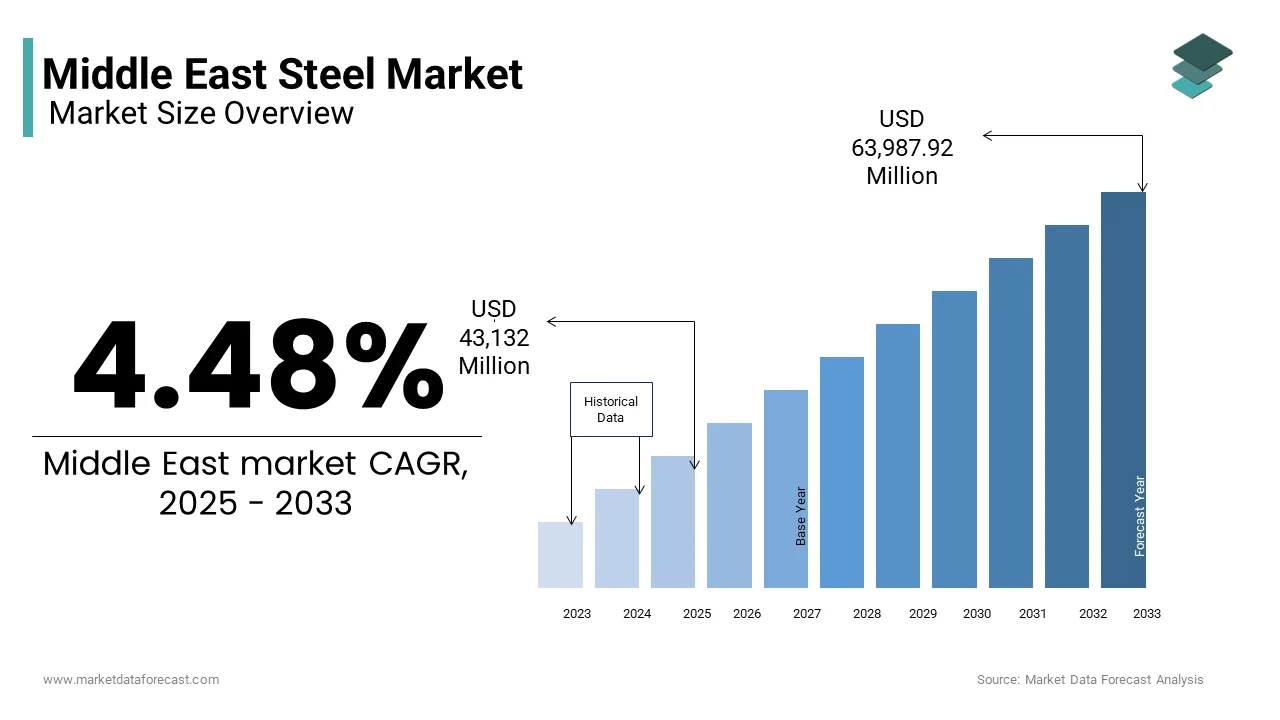

Market Size, 2025

$44438 MnMarket Estimate, 2026

$45785 MnMarket Forecast, 2034

$56425 MnCAGR, 2026–2034

4.48%Middle East Steel Market Size

The Middle East Steel market was valued at USD 44438.9 million in 2025 and is anticipated to reach USD 45785.4 million in 2026 and USD 56425.18 million by 2034, growing at a CAGR of 4.48% during the forecast period from 2026 to 2034.

Steel is a fundamental building material that underpins construction, automotive manufacturing, energy, and heavy industry sectors across key economies such as Saudi Arabia, the UAE, Iran, and Egypt. As per BMI Research (Fitch Solutions), the steel sector in the Middle East is undergoing a phase of modernization and capacity expansion, driven by government-led economic diversification plans that reduce reliance on hydrocarbons. In recent years, countries like the UAE and Oman have invested heavily in upgrading their integrated steel plants and downstream processing facilities to meet domestic demand while also enhancing export capabilities.

MARKET DRIVERS

Infrastructure Development and Urbanization Initiatives

Infrastructure development is one of the most significant drivers of the Middle East steel market in the Gulf Cooperation Council (GCC) countries. Governments across the region are investing heavily in transportation networks, housing projects, and smart city developments to accommodate rapidly growing populations and support economic diversification away from oil revenues. According to Oxford Business Group, GCC nations collectively plan to invest over $500 billion in infrastructure projects by 2030, with Saudi Arabia alone allocating more than $180 billion for Vision 2030-related initiatives. These include megaprojects such as NEOM, Riyadh Metro, and Jeddah Tower, all of which require massive volumes of steel for structural frameworks, bridges, and rail tracks. In 2023, the Dubai Roads and Transport Authority (RTA) reported that over 40 large-scale construction projects were underway, which were contributing significantly to domestic steel demand.

Industrialization and Expansion of Manufacturing Sectors

Industrialization is another key factor propelling the Middle East steel market, especially as countries seek to build robust manufacturing ecosystems. In line with Saudi Arabia’s Industrial Strategy under Vision 2030, the Kingdom aims to increase the contribution of manufacturing to GDP from 9% to 20% by 2030, as per the Saudi Industrial Development Fund (SIDF). Similarly, the UAE’s Operation 300bn initiative targets the expansion of advanced industries with a strong focus on metals and materials. Moreover, Egypt has been revitalizing its industrial base through the establishment of the Suez Canal Economic Zone (SCZone), which has attracted foreign direct investment in steel-intensive industries.

MARKET RESTRAINTS

High Energy Costs and Resource Constraints

Many Middle Eastern countries face challenges related to energy supply volatility and rising input costs, which limit the growth of the Middle East steel market. Steel production is highly energy-intensive, particularly in integrated mills where blast furnaces require consistent and cost-effective power sources. However, according to the Middle East Economic Survey (MEES), certain countries such as Egypt and Jordan experience periodic electricity shortages due to aging infrastructure and insufficient grid capacity. In 2023, Egypt faced rolling blackouts during peak summer months, forcing some steel mills to operate at reduced capacity. Additionally, while GCC countries enjoy relatively low natural gas prices compared to Europe or Asia, recent shifts in global energy markets have led to increased domestic consumption, reducing surplus availability for export-oriented industries.

Import Competition and Global Oversupply

The Middle East steel market faces intense competition from low-cost imports from China, India, and Turkey, which often undercut local producers on price. According tothe World Steel Association Worldsteell), in 2023, the Middle East imported approximately 18 million metric tons of finished steel products, with Turkish rebar and Chinese wire rods dominating the market. Local producers, especially in the UAE and Saudi Arabia, argue that this influx undermines their ability to expand capacity and invest in technological upgrades. Furthermore, global oversupply continues to put downward pressure on prices, making it difficult for Middle Eastern firms to achieve profitability without government support. The situation was exacerbated by the post-pandemic recovery in China, where production resumed faster than global demand could absorb, leading to aggressive export strategies.

MARKET OPPORTUNITIES

Green Steel and Decarbonization Initiatives

The global shift toward sustainability presents a significant opportunity for the Middle East steel market to position itself as a leader in green steel production. Several governments in the region have committed to net-zero emissions targets by prompting steelmakers to explore cleaner production methods such as hydrogen-based reduction and electric arc furnace (EAF) technologies. Saudi Arabia has announced plans to develop a green hydrogen-powered steel plant in NEOM in collaboration with companies like Hybrit and SSA,y aiming to produce fossil-free steel by 2030. As per the Saudi Green Initiative Secretariat, this project is expected to reduce annual carbon emissions by more than 4.5 million metric tons, aligning with broader climate commitments. Similarly, the UAE’s Ministry of Industry and Advanced Technology has launched the "Green Industries" initiative, offering incentives for companies adopting low-carbon technologies. With access to abundant solar energy and natural gas, the Middle East is well-positioned to become a hub for clean steel production, attracting investment from global players seeking to decarbonize their supply chains.

Regional Integration and Trade Agreements

Enhanced regional integration and the formation of trade agreements offer considerable opportunities for the Middle East steel market to expand beyond national borders and reduce dependency on volatile global markets. The recent normalization of diplomatic relations between several Arab states, coupled with the strengthening of the Gulf Cooperation Council (GCC), has facilitated greater cross-border collaboration in industrial sectors. Additionally, the African Continental Free Trade Area (AfCFTA) agreement provides Middle Eastern steel producers with access to new markets in North and Sub-Saharan Africa, where infrastructure deficits create substantial demand. Egyptian steelmaker Ezz Steel, for example, has increased exports to Libya, Sudan, and Kenya by leveraging preferential trade terms. Moreover, the UAE’s recent free trade agreements with Indonesia and Israel open new avenues for steel exports.

MARKET CHALLENGES

Regulatory Complexity and Policy Uncertainty

The inconsistency in regulatory frameworks across different countries, which complicates investment planning and operational efficiency, is slowly degrading the growth of the Middle East steel market. While some governments offer generous subsidies and tax incentives to attract industrial investment, others impose fluctuating tariffs, restrictive labor laws, and unpredictable customs policies that deter long-term capital deployment. In Saudi Arabia, for instance, the transition from the old Saudization rules to the new Nitaqat system has created uncertainty for steel mills reliant on expatriate technical expertise.

Skilled Labor Shortages and Technological Gaps

The Middle East steel market continues to grapple with a shortage of skilled labor and gaps in technical expertise in maintenance, metallurgy, and process engineering. Many steel plants in the region rely heavily on expatriate workers, but tightening visa regulations and higher labor costs are making this model unsustainable. According to the Arab Center for Research and Policy Studies, Gulf Cooperation Council (GCC) countries face a deficit of over 400,000 skilled industrial workers, with the steel sector hardest hhitt For example, Saudi Basic Industries Corporation (SABIC) has collaborated with King Abdullah University of Science and Technology (KAUST) to develop specialized metallurgical engineering courses. However, progress remains slow, and many steel producers continue to experience equipment downtime due to inadequate maintenance knowledge. Additionally, while some large mills have adopted Industry 4.0 technologies such as predictive analytics and AI-driven quality control, smaller and mid-sized producers lag due to limited budgets and a lack of digital readiness. Bridging these skill and technology gaps will be essential for the Middle East steel market to improve productivity and global competitiveness.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.48% |

| Segments Covered | By Type, Application, Product, and By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | KSA, UAE, Israel, the Rest of GCC countries Rest of the Middle East. |

| Market Leaders Profiled | Emirates Steel, SABIC Hadeed, ArcelorMittal, Tata Steel, Ezz Steel, Qatar Steel, Jindal Steel & Power, Al-Ittefaq Steel, Bahrain Steel, Liberty Steel Group, Hyundai Steel, United Iron & Steel Company, Nippon Steel, Essar Steel, Suez Steel Company. |

SEGMENTAL ANALYSIS

By Type Insights

The flat steel segment accounted in holding 54.3% of the Middle East steel market share in 2025. In Saudi Arabia, for instance, the government’s push toward localizing vehicle production under Vision 2030 has led to increased demand for flat steel in automotive assembly plants. According to the Saudi Automotive Industry Council, domestic auto manufacturing grew by 18% in 2023, which is directly boosting flat steel consumption. Additionally, the UAE’s growing emphasis on advanced manufacturing and export-oriented industries has further strengthened the demand for coated and alloyed flat steel products. The region’s expanding oil and gas sector also contributes significantly, as pipelines, storage tanks, and offshore platforms require corrosion-resistant steel plates.

The long steel segment is emerging with an expected CAGR of 6.9% during the forecast period. Long steel products, including rebar, wire rods, and structural sections, are crucial for construction and infrastructure development. The growth is largely attributed to the surge in public and private investment in residential, commercial, and transportation projects across key markets. In Egypt, for example, the government announced plans to build over 500,000 new housing units in 2023 alone, as reported by the Ministry of Housing, Utilities, and Urban Communities, all of which require substantial volumes of reinforcing steel bars. Similarly, the UAE’s infrastructure spending reached $48 billion in 2023, with major developments such as Dubai’s Expo City expansion and Abu Dhabi’s Musaffah Bridge project driving demand for long steel products. Moreover, the revival of large-scale railway initiatives, including the Riyadh-Dammam rail corridor and Oman’s Duqm port connectivity plan, is further boosting the need for durable steel rails and support structures.

By Application Insights

The building and construction segment held 47.3% of the Middle East steel market share in 2025, with the aggressive urbanization agenda in GCC countries, where governments are investing heavily in real estate, infrastructure, and smart city development. In Saudi Arabia, Vision 2030 has catalyzed a wave of mega-projects such as NEOM, Qiddiya, and Riyadh Metro, all requiring vast quantities of steel for structural frameworks, bridges, and foundations. According to the Saudi Ministry of Municipal and Rural Affairs, over 12,000 new buildings were approved for construction in 202, reflecting strong momentum in the sector.

The mechanical equipment segment is likely to grow with a CAGR of 7.4% from 2025 to 2033, with the usage in industrial machinery, automation systems, and heavy-duty mechanical components essential for manufacturing, energy, and mining operations. The rise in demand is closely tied to the region’s industrial transformation strategies aimed at reducing reliance on hydrocarbons and fostering advanced manufacturing capabilities. In Saudi Arabia, Operation Gulf 2030 has incentivized the localization of mechanical engineering and precision manufacturing, resulting in increased procurement of high-strength steel alloys for machine parts, turbines, and hydraulic systems. According to the Saudi Industrial Development Fund (SIDF), the mechanical equipment sector expanded by 14% in 2023, supported by foreign partnerships and technology transfer agreements. Similarly, in the UAE, the "Operation 300bn" initiative has led to a surge in demand for automated production lines and robotics, many of which depend on specialized steel grades. Egyptian manufacturers have also ramped up their use of steel-based machinery to modernize the textile, food processing, and pharmaceutical industries.

COUNTRY ANALYSIS

Kingdom of Saudi Arabia (KSA) Steel Market Analysis

Saudi Arabia was the top performer in the Middle East steel market with 32.1% of the share in 2025. SABIC and Saudi Steel Company (formerly Arabian Shield) play pivotal roles in supplying both domestic and international markets. According to the Saudi Ministry of Industry and Mineral Resources, the steel sector contributed over SAR 35 billion ($9.3 billion) to the national GDP in 2023. The government's focus on megaprojects such as NEOM, Riyadh Metro, and Jeddah Tower continues to drive demand for construction-grade and specialty steel. Additionally, the Kingdom has been actively investing in green steel technologies, with plans to develop a hydrogen-based steel plant in collaboration with European partners.

United Arab Emirates (UAE) Steel Market Analysis

The UAE ranked second in the Middle East steel market by capturing 23.7% of the market share in 2025. Steel demand in the UAE is primarily driven by construction, infrastructure, and industrial sectors, particularly in Dubai and Abu Dhabi. The Centennial 2071 strategy emphasizes technological advancement and sustainability, encouraging the adoption of high-performance steel in skyscrapers, airports, and smart cities. Additionally, the UAE’s growing renewable energy sector, including solar farms and hydrogen facilities, is increasing the need for corrosion-resistant steel components.

Egypt Steel Market Analysis

Egypt steel market is likely to grow with a prominent CAGR in the coming years. In 2023, Ezz Steel reported a production capacity of 7.2 million metric tons annually, as stated in its corporate sustainability report. Egypt’s steel market benefits from a rapidly growing population, rising urbanization rates, and government-led housing programs. The Ministry of Housing announced that over 700,000 affordable housing units were delivered in 2023, significantly boosting demand for rebar and structural steel. Additionally, the development of the Suez Canal Economic Zone (SCZone) has attracted foreign direct investment in industries ranging from petrochemicals to automotive manufacturing, all of which rely on steel inputs.

COMPETITIVE LANDSCAPE

The Middle East steel market is marked by a dynamic and evolving competitive landscape shaped by both state-backed giants and privately owned enterprises. While large integrated producers dominate due to their scale, access to raw materials, and government support, mid-sized mills and mini-steel plants are gaining ground by leveraging flexibility and lower capital intensity. The market is witnessing increased competition from imported steel, especially from Turkey, China, and India, which often offer more competitively priced products. This has prompted regional players to focus on differentiation through product quality, value-added services, and localized customer engagement. Additionally, growing emphasis on environmental sustainability is influencing investment decisions, with top players racing to adopt cleaner production methods and align with global decarbonization standards. The entry of new private equity-backed ventures and the modernization of aging facilities further intensify rivalry.

KEY MARKET PLAYERS

These are the market players that are dominating the Middle East steel market.

- Emirates Steel

- SABIC Hadeed

- ArcelorMittal

- Tata Steel

- Ezz Steel

- Qatar Steel

- Jindal Steel & Power

- Al-Ittefaq Steel

- Bahrain Steel

- Liberty Steel Group

- Hyundai Steel

- United Iron & Steel Company

- Nippon Steel

- Essar Steel

- Suez Steel Company.

Top Players In The Market

- Emirates Steel Arkan is a leading integrated steel producer in the UAE and one of the largest in the Middle East. The company plays a crucial role in supplying construction, infrastructure, and industrial sectors with high-quality steel products. Its operations span from ironmaking to downstream processing, ensuring a vertically integrated supply chain. Emirates Steel Arkan has positioned itself as a regional hub for sustainable steel production, investing in cleaner technologies and carbon-efficient processes. Its strategic partnerships with international firms have enhanced its technological capabilities and expanded its export footprint across Africa and Asia.

- Saudi Steel Company is a cornerstone of the Kingdom’s industrial sector, contributing significantly to domestic steel demand and regional exports. Globally, the company is recognized for its role in advancing the Middle East’s steel market through innovation and localization efforts. It supports major national projects under Vision 2030, reinforcing Saudi Arabia's shift toward industrial self-sufficiency while aligning with global trends in green steel and digital manufacturing.

- Ezz Steel is Egypt’s largest steel producer and one of the most prominent players in the Middle East and Africa. Known for its rebar and long steel products, the company serves key construction and infrastructure markets. Globally, Ezz Steel has established itself as a reliable supplier to emerging economies, particularly in Sub-Saharan Africa, where demand for affordable and durable steel remains high. Its expansion strategy focuses on increasing production efficiency by enhancing product quality and strengthening logistics networks to maintain competitiveness in volatile markets.

Top Strategies Used By Key Players In The Market

Investment in Green and Sustainable Technologies

Major steel producers in the region are increasingly adopting environmentally friendly production methods, including hydrogen-based reduction, electric arc furnaces, and carbon capture systems. These initiatives align with national climate goals and enhance their positioning in global markets that prioritize sustainability.

Vertical Integration and Local Supply Chain Development

Steelmakers are expanding their control over raw material sourcing, logistics, and distribution to reduce dependency on imports and improve cost efficiency. This approach also strengthens resilience against global price fluctuations and supply chain disruptions.

Strategic Partnerships and Technology Transfer Agreements

Leading companies are forming alliances with global steel giants and research institutions to access cutting-edge technologies, improve operational efficiency, and support workforce development. These collaborations help bridge skill gaps and foster innovation within the region.

RECENT MARKET NEWS

- In March 2024, Emirates Steel Arkan announced a joint venture with a European clean technology firm to pilot hydrogen-based steel production at its Abu Dhabi facility, which is signaling a major step toward decarbonizing its operations and aligning with the UAE’s net-zero commitments.

- In July 2023, Saudi Steel Company launched an internal digital transformation initiative aimed at integrating AI-driven predictive maintenance and real-time process monitoring across its production units by improving efficiency and reducing downtime.

- In January 2024, Ezz Steel inaugurated a new regional logistics hub in Djibouti to enhance its distribution network and strengthen its presence in East African markets by supporting its export growth strategy.

- In October 2023, Industrial Development Group (IDG), a Bahrain-based steelmaker, signed a strategic partnership with a South Korean engineering firm to upgrade its rolling mill technology and expand product offerings in precision steel applications.

- In May 2024, Qatar Steel commissioned a new secondary processing line focused on coated and corrosion-resistant steel products by catering to the growing needs of the energy and infrastructure sectors across the GCC.

MARKET SEGMENTATION

This research report on the Middle East steel market is segmented and sub-segmented into the following categories.

By Type

- Flat Steel

- Long Steel

By Product

- Structural Steel

- Prestressing Steel

- Bright Steel

- Welding Wire and Rod

- Iron Steel Wire

- Ropes

- Braids

By Application

- Building and Construction

- Electrical Appliances

- Metal Products

- Automotive

- Transportation

- Mechanical Equipment

- Domestic Appliances

By Country

- Ksa

- Uae

- Israel

- Rest of the GCC Countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- Rest Of MEA