North America Industrial Boilers Market Size, Share, Trends & Growth Forecast Report, Segmented By Fuel (Natural Gas, Oil, Coal, and Others), Capacity, Technology, Product, Application, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

North America Industrial Boilers Market Size

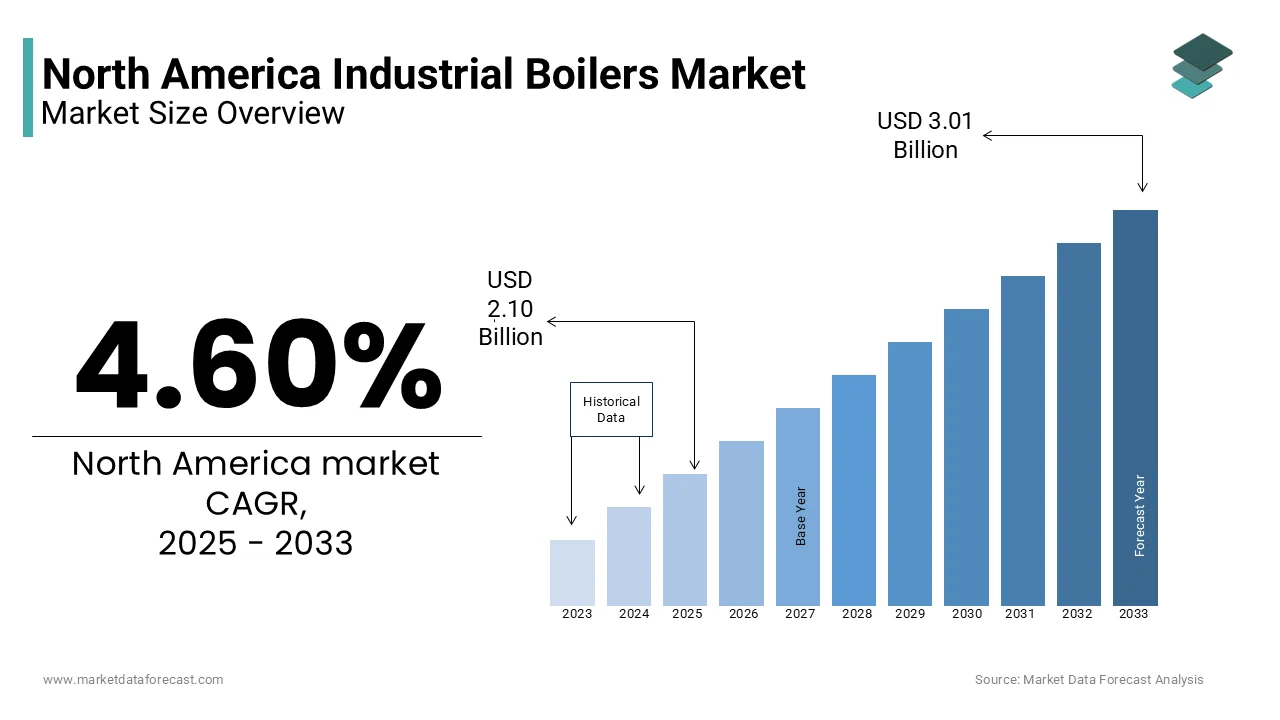

The North American industrial boilers market size was valued at USD 2.10 billion in 2025 and is projected to reach USD 2.20 billion in 2026 to reach USD 3.15 billion in 2034, rising at a CAGR of 4.60% from 2026 to 2034.

The industrial boiler is a component of the continent's manufacturing and energy infrastructure, which is encompassing steam and hot water generation systems used across diverse industrial sectors. These specialized pressure vessels serve as essential thermal energy sources for processes including power generation, chemical processing, food production, and textile manufacturing. Industrial boilers operate under stringent safety regulations established by the American Society of Mechanical Engineers and the National Board of Boiler and Pressure Vessel Inspectors, ensuring compliance with pressure, temperature, and material specifications. According to the U.S. Energy Information Administration, industrial sector energy consumption accounted for 32% of total energy use in North America in 2023, with steam generation systems representing a significant portion of this demand. Manufacturing industries collectively operate over 180,000 industrial boilers across the region, with the chemical sector alone utilizing approximately 45,000 units for process heating applications.

MARKET DRIVERS

Increasing Industrial Manufacturing Activities

The resurgence of industrial manufacturing activities is propelling the growth of the North American industrial boiler market. The United States has experienced a notable manufacturing renaissance, with the Federal Reserve reporting that industrial production index values reached 110.3 in 2023, representing a 4.2% increase from the previous year. Food processing represents another substantial demand driver, as the Institute of Food Technologists reports that North American food manufacturers invested $42 billion in facility improvements and capacity expansions in 2023. These projects consistently require steam generation systems for cooking, sterilization, and cleaning applications. Additionally, the reshoring trend, where companies relocate manufacturing operations back to North America, has intensified boiler demand as new facilities require comprehensive thermal energy infrastructure.

Stringent Environmental Regulations and Emission Standards

The implementation of increasingly stringent environmental regulations and emission standards is fuelling the growth of the North American industrial boiler market. The EPA estimated that over 35,000 industrial boilers in North America must comply with updated emission standards by 2025, creating substantial replacement and upgrade opportunities. Additionally, regional air quality initiatives such as the California Air Resources Board's stringent emission requirements have accelerated boiler modernization programs across the western United States. Carbon reduction commitments made by various states and provinces further amplify this trend, as industrial facilities seek boiler systems that can operate with lower carbon intensity and improved fuel flexibility. The Canadian Council of Ministers of the Environment reports that industrial sector greenhouse gas reduction targets require a 30% decrease in emissions by 2030, prompting extensive boiler replacement initiatives. Furthermore, the integration of renewable fuel capabilities in modern boiler designs has attracted investment from companies seeking to reduce their environmental footprint while maintaining operational efficiency.

MARKET RESTRAINTS

High Capital Investment and Installation Costs

The substantial capital investment requirements associated with industrial boiler procurement, installation, and commissioning are restricting the growth of the North American industrial boiler market. Modern industrial boilers, especially those incorporating advanced emission control technologies and automated control systems, command premium pricing that can range from $500,000 to several million dollars, depending on capacity and complexity. The total installed cost often exceeds the equipment purchase price by 50-100%, encompassing engineering, installation, permitting, and commissioning expenses that create financial barriers for potential adopters. According to the National Association of Chemical Distributors, small chemical processors often allocate less than 15% of annual revenue for capital expenditures, limiting their ability to invest in major boiler system upgrades or replacements. Additionally, the specialized nature of industrial boiler installation requires certified contractors and extended project timelines, further increasing overall implementation costs. Labor costs for qualified boiler installation technicians have risen significantly, with the Bureau of Labor Statistics reporting a 12% increase in specialty trade contractor wages since 2020. Furthermore, regulatory compliance requirements necessitate additional expenditures for emissions monitoring equipment, safety systems, and permit acquisition that can increase total project costs by 20-30%. These financial constraints particularly impact smaller industrial facilities that may defer necessary boiler replacements or upgrades, potentially compromising operational efficiency and regulatory compliance.

Skilled Labor Shortage and Technical Expertise Gaps

The shortage of skilled technicians and engineers capable of designing, installing, maintaining, and operating complex boiler systems is fuelling the growth of the North American industrial boiler market. The aging workforce within the industrial sector has created a knowledge gap that threatens the market's ability to support growing demand for boiler installations and maintenance services. The National Institute for Metalworking Skills reports that the industrial equipment maintenance sector faces a shortage of over 200,000 qualified technicians across North America, with boiler specialists representing a particularly constrained talent pool. This shortage directly impacts project execution timelines and operational reliability, as facilities struggle to maintain adequate staffing levels for boiler operation and preventive maintenance activities. Educational institutions have not kept pace with the evolving technical requirements of modern boiler systems, resulting in graduates lacking experience with advanced control systems, emission monitoring technologies, and safety protocols. The American Society of Mechanical Engineers indicates that only 35% of mechanical engineering graduates possess the specialized knowledge required for industrial boiler applications, creating a significant gap between industry needs and available talent. Additionally, the complexity of modern boiler systems, which integrate advanced sensors, automated controls, and emission reduction technologies, requires technicians with multidisciplinary skills spanning mechanical, electrical, and instrumentation disciplines.

MARKET OPPORTUNITIES

Integration of Renewable Energy and Hybrid Systems

The growing emphasis on renewable energy integration and hybrid thermal systems presents a significant opportunity for the growth of the NorAmericanica industrial boiler market. This emerging trend focuses on creating flexible thermal systems that can operate using multiple fuel sources, including biomass, biogas, solar thermal, and hydrogen, providing industrial facilities with enhanced energy security and reduced carbon intensity. The National Renewable Energy Laboratory reports that hybrid thermal systems incorporating renewable energy sources can reduce fossil fuel consumption by 40-60% while maintaining process heating reliability and operational flexibility. Biomass-fired boiler systems have gained particular attention, as the U.S. Forest Service indicates that sustainable biomass resources could provide heating energy for over 15,000 industrial facilities across North America. The integration of solar thermal systems with conventional boilers represents another promising development, with pilot projects demonstrating the feasibility of using solar energy to preheat boiler feedwater and reduce natural gas consumption by 25-35%. Additionally, the development of hydrogen-compatible boiler systems creates opportunities for industrial facilities to transition toward zero-emission heating solutions as green hydrogen production scales.

Advanced Automation and IoT Integration

The integration of advanced automation technologies and Internet of Things connectivity within industrial boiler systems is anticipated to boost the growth of the North American industrial boiler market. Modern boiler systems increasingly incorporate sensors, wireless communication modules, and predictive analytics platforms that enable real-time monitoring of combustion efficiency, emission levels, and equipment health parameters. The Industrial Internet Consortium reports that IoT-enabled boiler systems can achieve 8-15% improvements in fuel efficiency while reducing unplanned maintenance events by 30-40%. Predictive maintenance capabilities, powered by machine learning algorithms and sensor data analysis, allow facilities to optimize maintenance schedules and prevent costly equipment failures. The integration of artificial intelligence with boiler control systems enables dynamic optimization of combustion parameters based on real-time load requirements, fuel characteristics, and environmental conditions. Cloud-based monitoring platforms provide facility managers with comprehensive visibility into boiler performance across multiple locations, facilitating centralized control and benchmarking activities. Additionally, the development of digital twin technologies for boiler systems enables virtual testing and optimization of operational parameters before implementing changes in actual equipment.

MARKET CHALLENGES

Regulatory Compliance Complexity and Permitting Delays

The increasingly complex regulatory environment governing industrial boiler operation is likely to restrict the growth of the North American industrial boiler market. The permitting process for new boiler installations or major modifications has become increasingly time-consuming and resource-intensive, with approval timelines extending 12-18 months in many jurisdictions. The Environmental Protection Agency's multi-pollutant emission standards, combined with state-level air quality regulations and local permitting requirements, create a labyrinthine compliance landscape that requires extensive technical expertise and documentation. The National Association of Clean Air Agencies reports that the average time required to obtain comprehensive boiler permits increased by 40% between 2018 and 2023, creating project delays and cost overruns that impact market development. Additionally, the frequent updates to emission standards and safety requirements necessitate continuous monitoring and adaptation of boiler designs and operational procedures.

Fuel Price Volatility and Supply Chain Disruptions

The fuel price volatility and supply chain disruptions that impact operational costs and system reliability are likely to limit the growth of the North American industrial boiler market. Natural gas, which serves as the primary fuel source for approximately 70% of industrial boilers in North America, has experienced significant price fluctuations due to geopolitical tensions, weather events, and infrastructure constraints. The Energy Information Administration reports that natural gas prices varied by more than 60% between peak and trough periods in 2023, creating budgeting uncertainties and operational planning challenges for industrial facilities. Alternative fuel sources, including propane, fuel oil, and biomass, also experience price volatility that affects boiler operating economics and fuel switching decisions. Supply chain disruptions affecting boiler components, spare parts, and consumables have become increasingly common, with global logistics challenges and manufacturing bottlenecks extending lead times for equipment. The American Boiler Manufacturers Association indicates that average lead times for custom industrial boilers increased from 16 weeks to 32 weeks in 2023 due to supply chain constraints affecting steel, refractory materials, and control components. International trade tensions and import restrictions have further complicated procurement strategies, particularly for specialized components sourced from overseas manufacturers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.60% |

| Segments Covered | By Fuel, Capacity, Technology, Product, Application, and Country |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | The United States, Canada, Mexico, and the Rest of North America |

|

Market Leaders Profiled | AERCO, Babcock & Wilcox Enterprises, Inc., Burnham Commercial Boilers, Clayton Industries, Cleaver-Brooks, Doosan Corporation, Groupe Atlantic, Hurst Boiler & Welding Co., Inc., IHI Corporation, John Cockerill, John Wood Group PLC, Mitsubishi Heavy Industries, Ltd., Miura America Co., Ltd., Rentech Boiler Systems, Inc., SofinterS.p.a.a, The Fulton Companies, Thermax Limited, and VIESSMANN. |

SEGMENTAL ANALYSIS

By Fuel Insights

The natural gas segment dominated the North American industrial boiler market share in 2025. The abundance of domestic natural gas reserves, particularly following the shale gas revolution, has ensured d reliable supply and competitive pricing that makes natural gas-fired boilers economically attractive for industrial applications. The American Gas Association reports that natural gas accounts for 32% of total U.S. energy consumption, with industrial sector usage representing 35% of this total, creating substantial demand for efficient boiler systems. Natural gas infrastructure development has been extensive, with the Energy Information Administration documenting over 300,000 miles of transmission pipelines and millions of miles of distribution networks that provide reliable access to industrial facilities. The environmental benefits of natural gas combustion, including reduced particulate emissions and lower carbon intensity compared to coal and oil, align with regulatory requirements and corporate sustainability objectives. Additionally, natural gas boiler systems offer operational advantages including rapid start-up capabilities, precise load modulation, and simplified emission control requirements that enhance operational flexibility and reduce compliance costs. The integration of combined heat and power systems utilizing natural gas further amplifies demand, as industrial facilities seek to maximize energy efficiency and reduce operational costs through cogeneration applications.

The biomass and renewable fuel segment is lucratively to grow lucratively with an anticipated CAGR of 8.4% from 2025 to 2033. Government incentives and regulatory frameworks supporting renewable energy deployment have accelerated market development, with the Inflation Reduction Act providing $370 billion in clean energy investments that include substantial funding for biomass energy projects. Corporate sustainability initiatives have emerged as significant growth drivers, as major industrial companies commit to carbon neutrality targets that require a transition away from fossil fuel dependence. The Carbon Trust indicates that over 200 Fortune 500 companies have established renewable energy procurement targets that include biomass boiler installations for industrial process heating. Additionally, waste-to-energy initiatives in the pulp and paper, food processing, and agricultural sectors create opportunities for facilities to utilize organic waste streams as boiler fuel while reducing disposal costs and environmental impact.

By Capacity Insights

The 10-25 MMBtu/hr capacity segment was the largest by accounting for 32.2% of the North America industrial boiler market share in 2024 due to the prevalence of medium-scale industrial facilities across North America that require balanced thermal energy capacity to support diverse manufacturing processes while maintaining operational efficiency and cost-effectiveness. Food processing facilities constitute a primary demand source, with the Institute of Food Technologists reporting that over 25,000 food processing plants in North America operate within this capacity range to meet production requirements for baking, cooking, sterilization, and drying applications. The Pharmaceutical Research and Manufacturers of America indicates that pharmaceutical manufacturing facilities investing in capacity expansion projects consistently select 10-25 MMBtu/hr boiler systems to support pilot production lines and flexible manufacturing configurations. The modular nature of boilers in this capacity range enables facilities to implement redundant systems and staged capacity additions that optimize capital deployment and operational flexibility. Additionally, the relatively lower capital investment requirements compared to larger capacity systems make this segment attractive to small and medium-sized enterprises that require industrial steam generation without extensive financial commitments. The standardized design characteristics of 10-25 MMBtu/hr boilers facilitate faster procurement, installation, and commissioning processes that reduce project timelines and implementation risks.

The >250 MMBtu/hr capacity segment is anticipated to grow with a CAGR of 7.1% from 2025 to 2033, with the chemical, refining, and primary metals sectors that require substantial thermal energy capacity to support continuous high-volume production operations. The petrochemical industry represents a primary growth driver, as North America's position as a leading shale gas producer enables cost-competitive ethylene and derivative production that necessitates large-capacity boiler systems for steam cracking and processing applications. Integrated steel manufacturing facilities also drive demand, as the Steel Manufacturers Association indicates that new electric arc furnace installations require extensive steam generation systems exceeding 250 MMBtu/hr capacity to support continuous casting, rolling, and finishing operations. Combined heat and power projects represent another significant growth catalyst, as large industrial facilities seek to maximize energy efficiency and reduce operational costs through cogeneration systems that require substantial boiler capacity to support both process heating and electrical generation requirements.

By Application Insights

The chemical segment held 28.5% of the North America industrial boiler market share in 2024, with the chemical sector's intensive reliance on steam and thermal energy for diverse process applications, including reaction heating, distillation, evaporation, and drying operations that require reliable and precise thermal energy systems. The diversity of chemical manufacturing processes creates a comprehensive demand for specialized boiler solutions that can accommodate varying pressure, temperature, and steam quality requirements across different production stages. The American Chemistry Council reports that the U.S. chemical industry represents the third-largest manufacturing sector by value, with over 13,000 facilities requiring extensive steam generation capabilities for continuous operations. Specialty chemical production, including pharmaceutical intermediates, agricultural chemicals, and advanced materials, demands high-purity steam and precise temperature control that necessitates sophisticated boiler systems with advanced monitoring and control capabilities.

The food processing segment is likely to grow with a CAGR of 6.8% from 2025 to 2033, with the expanding food manufacturing sector, increasing demand for processed foods, and evolving consumer preferences that drive facility expansions and capacity additions requiring steam generation systems. The Institute of Food Technologists reports that North American food processing investments exceeded $45 billion in 2023, with thermal processing equipment representing 15-20% of total capital expenditures for new facility construction and existing plant modernization projects. Consumer demand for convenience foods, ready-to-eat meals, and specialty dietary products has accelerated food manufacturing growth, creating substantial demand for steam-based cooking, sterilization, and packaging applications. Export market expansion has further amplified demand, as North American food manufacturers increase production capacity to serve international markets that require compliance with stringent food safety standards and quality certifications. The integration of automation and continuous processing technologies in food manufacturing creates opportunities for advanced boiler systems that can provide precise steam control and rapid response capabilities for flexible production scheduling.

REGIONAL ANALYSIS

United States Industrial Boiler Market Insights

The United States was the top performer of the North American industrial boiler market with 82.3% of share in 20,24, with the country's extensive industrial base, diverse manufacturing sectors, and robust infrastructure development that generates substantial demand for steam generation and thermal energy systems across multiple applications. The country's position as a leading manufacturing hub, supported by favorable business conditions and technological innovation, ensures sustained demand for efficient and reliable boiler systems that support competitive industrial operations. Federal and state-level initiatives supporting domestic manufacturing and energy independence have further amplified boiler demand through infrastructure investments and industrial development programs.

Canada Industrial Boiler Market Insights

Canada held 15.2% of the North American industrial boiler market share in 2024. The country's cold climate necessitates year-round industrial operations that require robust boiler systems capable of maintaining consistent performance despite temperature variations and seasonal demands. Natural Resources Canada reports that the industrial sector accounts for 25% of total energy consumption in the country, with steam generation representing a significant component of industrial energy use across various manufacturing processes. The government's commitment to carbon reduction and sustainable development has accelerated the adoption of renewable fuel boiler systems and energy-efficient technologies that support environmental objectives while maintaining industrial competitiveness. Provincial initiatives supporting clean technology adoption and industrial modernization have created opportunities for boiler system upgrades and replacements that incorporate advanced emission control and efficiency enhancement technologies. Additionally, the forestry sector's biomass utilization initiatives have driven demand for renewable fuel boiler systems that convert wood waste and forest residues into thermal energy for industrial processes.

COMPETITIVE LANDSCAPE

The North American industrial boiler market exhibits intense competitive dynamics characterized by the presence of established global players, regional specialists, and emerging technology-focused companies. Market competition is driven by factors including product differentiation, pricing strategies, customer service capabilities, and technological innovation. Large multinational corporations leverage their extensive resources, global supply chains, and brand recognition to maintain dominant market positions, while specialized regional manufacturers focus on niche applications and local market expertise to compete effectively. The competitive landscape is further complicated by the entry of international manufacturers offering cost-competitive solutions, creating price pressure and forcing established players to differentiate through quality, service, and innovation. Customer relationships play a crucial role in market competition, with long-term contracts and specification approvals creating barriers to entry for new competitors. Distribution channels significantly influence competitive positioning, as companies with strong relationships with engineering firms, contractors, and industrial end-users gain preferential access to project opportunities. The market also experiences competition from alternative heating technologies and energy sources that may substitute traditional boiler solutions in specific applications. Regulatory compliance requirements and safety standards create additional competitive dimensions, as companies with comprehensive certification capabilities and proven track records gain competitive advantages in project bidding and customer selection processes.

KEY MARKET PLAYERS

These are the market players that are dominating the North American industrial boiler market.

- AERCO

- Babcock & Wilcox Enterprises, Inc.

- Burnham Commercial Boilers

- Clayton Industries

- Cleaver-Brooks

- Doosan Corporation

- Groupe Atlantic

- Hurst Boiler & Welding Co., Inc.

- IHI Corporation

- John Cockerill

- John Wood Group PLC

- Mitsubishi Heavy Industries, Ltd.

- Miura America Co., Ltd

- Rentech Boiler Systems, Inc.

- Sofinter S.p.a.

- The Fulton Companies

- Thermax Limited

- VIESSMANN.

Top Players In The Market

- Babcock & Wilcox Enterprises stands as a prominent leader in the North American industrial boiler market, renowned for its comprehensive portfolio of steam generation systems and environmental technologies. The company's significant contribution to the global market encompasses large-scale utility boilers, industrial process boilers, and specialized thermal systems for diverse applications, including power generation, chemical processing, and waste-to-energy projects. Their expertise in advanced combustion technologies and emission control systems has established them as a preferred supplier for infrastructure projects requiring high-efficiency and low-emission boiler solutions. The company's commitment to innovation is evident through its development of ultra-super boiler technologies and renewable energy integration systems that support sustainable industrial operations.

- Cleaver-Brooks emerges as a major force in the North American industrial boiler market, distinguished by its comprehensive solutions for steam and hot water generation across diverse industrial applications. The company's global market contribution encompasses complete boiler room solutions that integrate equipment, controls, and service capabilities to optimize industrial thermal energy systems. Their product portfolio includes fire-tube and water-tube boilers, waste heat recovery systems, and customized thermal solutions designed for specific industrial processes and operational requirements. The company's strength lies in its ability to provide end-to-end boiler system solutions that encompass design, manufacturing, installation, and ongoing maintenance services that ensure optimal performance and regulatory compliance. Their commitment to energy efficiency and environmental sustainability has driven the development of advanced boiler technologies that reduce fuel consumption and emissions while maintaining reliable operation. Cleaver-Brooks' extensive distribution network and factory-authorized service centers provide comprehensive support to industrial customers throughout North America by 4ensuring rapid response times and expert technical assistance.

- Hurst Boiler & Welding Company represents a significant player in the North American industrial boiler market, recognized for its specialized expertise in custom-engineered boiler systems and thermal solutions for challenging industrial applications. The company's contribution to the global market focuses on innovative boiler designs that address specific customer requirements for high-pressure, high-temperature, and specialized fuel applications. Their comprehensive capabilities encompass boiler manufacturing, system integration, and turnkey installation services that provide industrial facilities with complete thermal energy solutions tailored to unique operational needs. Hurst's reputation for quality and reliability stems from its commitment to engineering excellence and meticulous attention to safety standards and regulatory compliance requirements.

Top Strategies Used by Key Market Participants

Strategic Acquisitions and Technology Integration

Leading players in the North American industrial boiler market actively pursue acquisition strategies to expand their technological capabilities, enhance product portfolios, and strengthen market presence across diverse industrial sectors. These strategic moves enable companies to quickly enter new market segments, acquire specialized expertise, and broaden their geographic reach without the time and investment required for organic growth. Acquisition targets typically include companies with complementary technologies, established customer bases, or unique manufacturing capabilities that enhance the acquirer's competitive position. This approach allows market leaders to consolidate market share, eliminate competition, and achieve economies of scale that improve operational efficiency and cost competitiveness. Technology integration following acquisitions enables companies to offer comprehensive boiler system solutions that combine traditional steam generation capabilities with advanced control systems, emission monitoring technologies, and energy efficiency enhancements that meet evolving customer requirements and regulatory standards.

Product Innovation and Digital Transformation

Key market participants consistently invest in research and development to create innovative boiler solutions that address evolving industry requirements and customer needs. This strategy focuses on developing boilers with enhanced performance characteristics, improved safety features, and environmental sustainability through advanced materials, combustion technologies, and emission control systems. Companies prioritize innovation in digital technologies, incorporating Internet of Things connectivity, predictive analytics, and artificial intelligence to create smart boiler systems that optimize performance, reduce maintenance costs, and enhance operational safety. Advanced technologies such as remote monitoring, automated controls, and predictive maintenance capabilities represent key areas of development focus. The emphasis on innovation extends to manufacturing processes and quality control systems that improve production efficiency and product consistency. Market leaders also invest in developing specialized solutions for emerging applications such as renewable fuel utilization, hybrid thermal systems, and integration with combined heat and power technologies that support sustainable industrial operations and regulatory compliance requirements.

Strategic Partnerships and Customer Relationship Management

Major players in the industrial boiler market establish strategic partnerships with technology providers, system integrators, and industry stakeholders to enhance their competitive capabilities and market reach. These collaborative arrangements enable companies to leverage complementary strengths, share development costs, and access new market opportunities that would be difficult to pursue independently. Partnerships often focus on developing integrated solutions that combine boiler products with control systems, monitoring technologies, and installation services that provide comprehensive value to customers. Collaborative efforts also extend to research initiatives, standard development activities, and sustainability programs that advance industry best practices and technological advancement. These strategic relationships help companies stay current with emerging trends, regulatory developments, and customer requirements while reducing development risks and accelerating time-to-market for innovative solutions. Customer relationship management represents another strategy, with companies investing in comprehensive service networks, training programs, and technical support capabilities that ensure customer satisfaction and long-term loyalty through responsive support and proactive maintenance services.

RECENT MARKET NEWS

- In February 2024, Babcock & Wilcox Enterprises acquired Thermax Limited's boiler business in North America, expanding their product portfolio to include waste heat recovery boilers and enhancing their capabilities in energy-efficient thermal solutions for industrial applications.

- In January 2024, Cleaver-Brooks launched its new CBExcel series of packaged boilers featuring advanced control systems and emission monitoring capabilities, specifically designed to meet stringent environmental regulations while providing enhanced operational efficiency for industrial customers.

- In March 2024, Hurst Boiler & Welding Company partnered with Siemens to integrate advanced digital control technologies into their custom boiler systems, enabling real-time performance monitoring and predictive maintenance capabilities for industrial facilities.

- In May 2024, Babcock & Wilcox Enterprises announced the establishment of a new research and development center in Ohio focused on developing hydrogen-compatible boiler technologies and renewable fuel utilization systems for industrial applications.

- In April 2024, Cleaver-Brooks acquired Combustion Engineering Services, a specialized provider of boiler optimization and emission control solutions, strengthening their position in the industrial boiler aftermarket services segment and expanding their technical expertise in regulatory compliance.

MARKET SEGMENTATION

This research report on the North American industrial boilers market is segmented and sub-segmented into the following categories.

By Fuel

- Natural Gas

- Oil

- Coal

- Others

By Capacity

- 10 MMBtu/hr

- 10 - 25 MMBtu/hr

- 25 - 50 MMBtu/hr

- 50 - 75 MMBtu/hr

- 75 - 100 MMBtu/hr

- 100 - 175 MMBtu/hr

- 175 - 250 MMBtu/hr

- > 250 MMBtu/hr

By Technology

- Condensing

- Non-Condensing

By Product

- Fire Tube

- Water Tube

By Application

- Food Processing

- Pulp & Paper

- Chemical

- Refinery

- Primary Metal

- Others

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What are industrial boilers used for?

Industrial boilers generate steam or hot water for heating, power generation, and manufacturing processes in sectors like food processing, chemicals, and energy. They are essential for operations requiring consistent thermal energy at large scale.

Why is the industrial boiler market active in North America?

Ongoing manufacturing activity, aging infrastructure upgrades, and demand for energy-efficient systems are driving steady market growth. The U.S. and Canada both rely on industrial boilers for reliable on-site power and process heat.

What types of industrial boilers are most common?

Fire-tube and water-tube boilers are widely used, with selection based on pressure needs and capacity. Packaged boilers dominate due to ease of installation and standardized design.

How are emissions regulations shaping the market?

Strict environmental standards from agencies like the EPA are pushing industries to replace old, inefficient boilers with low-emission, high-efficiency models. Compliance is a major factor in modernization decisions.

Are companies switching to cleaner fuel options?

Yes, many facilities are shifting from heavy fuel oil to natural gas, which burns cleaner and aligns with sustainability goals. Some are also exploring hybrid systems or integrating renewable fuels where feasible.

What role does maintenance play in boiler performance?

Regular maintenance prevents downtime, improves efficiency, and extends equipment life. Many companies now use predictive monitoring systems to detect issues before they lead to failures.

How is digitalization impacting industrial boilers?

Smart sensors and IoT-enabled controls allow real-time monitoring of pressure, temperature, and fuel use. These systems help optimize performance and reduce energy waste through data-driven insights.

Are modular boilers gaining popularity?

Yes, modular boiler systems are being adopted for their flexibility, scalability, and redundancy. They allow plants to match output to demand and reduce energy use during low-production periods.

What industries drive the most demand?

Food and beverage, pharmaceuticals, pulp and paper, and chemical manufacturing are top users due to their high steam requirements. Power plants and district heating systems also contribute significantly.

What’s next for the industrial boiler market?

The future lies in ultra-efficient condensing boilers, integration with carbon capture, and hydrogen-ready designs. As decarbonization goals intensify, the market will focus on cleaner, smarter, and more adaptive thermal solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com