North America Industrial Centrifuges Market Size, Share, Trends & Growth Forecast Report By Product, Operation, Design, End User and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis From 2026 to 2034.

North America Industrial Centrifuges Market Report Summary

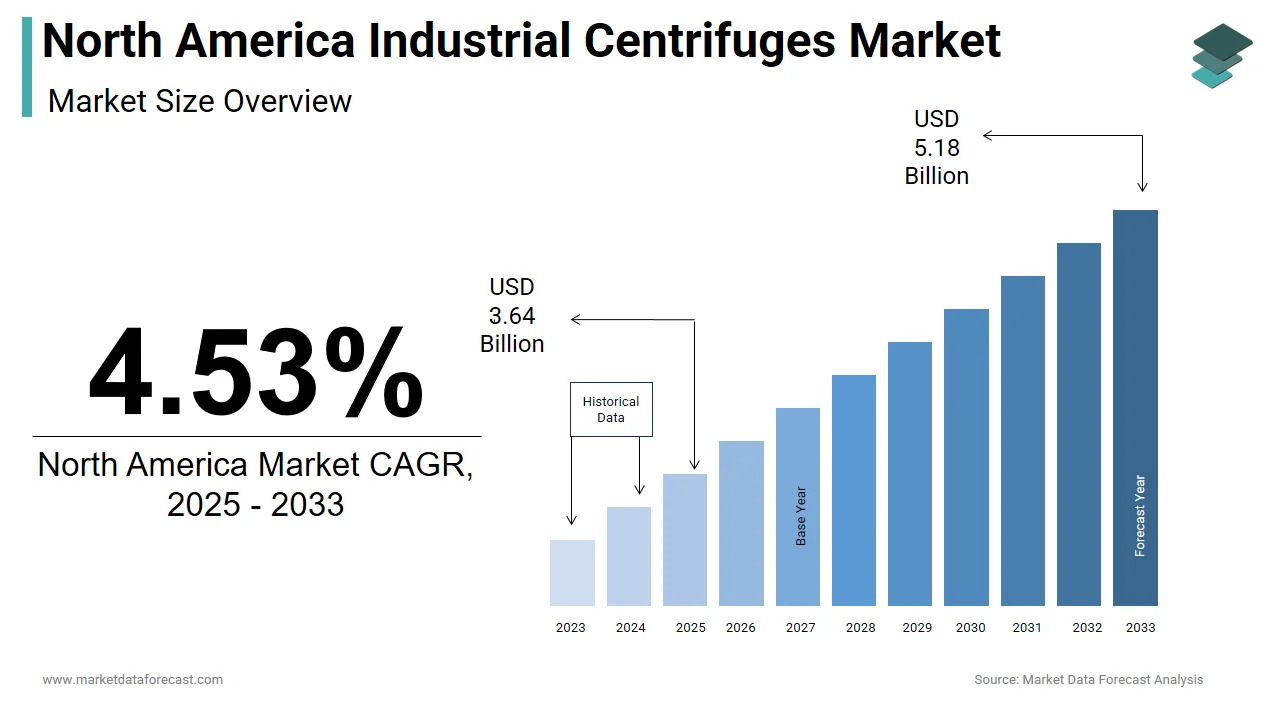

The North America industrial centrifuges market was valued at USD 3.64 billion in 2025 and is projected to grow from USD 3.80 billion in 2026 to USD 5.42 billion by 2034, registering a CAGR of 4.53% from 2026 to 2034. Market growth is driven by increasing demand for efficient separation technologies across wastewater treatment, chemical processing, pharmaceuticals, food and beverage, mining, and oil & gas industries. Industrial centrifuges improve process efficiency, reduce operational costs, and support compliance with stringent environmental regulations. Continued investments in industrial automation, resource recovery, and advanced separation technologies are further contributing to market expansion across North America.

Key Market Trends

- Rising investments in municipal and industrial wastewater treatment infrastructure.

- Growing adoption of high-efficiency centrifuge technologies in pharmaceutical and chemical manufacturing.

- Increasing focus on industrial automation and process optimization.

- Expansion of resource recovery and sustainable industrial processing initiatives.

- Continuous advancements in energy-efficient and digitally monitored centrifuge systems.

Segmental Insights

- Based on product, the sedimentation centrifuges segment dominated the North America industrial centrifuges market in 2025 and is expected to maintain its leadership throughout the forecast period, driven by its extensive use in municipal wastewater treatment and industrial solid-liquid separation processes.

- Based on technology, the biological and pharmaceutical purification segment held the leading market share in 2025, supported by growing pharmaceutical manufacturing, biotechnology research, and increasing demand for high-purity separation processes.

- Based on processing mode, the batch centrifuges segment accounted for the largest share of the market in 2025 and is projected to retain its leadership during the forecast period due to its precise process control and widespread use in pharmaceutical and fine chemical manufacturing.

- Based on application, the continuous centrifuges segment led the North America industrial centrifuges market in 2025, driven by the need for uninterrupted, high-volume processing across chemical, wastewater treatment, and industrial manufacturing operations.

Regional Insights

The North America industrial centrifuges market continues to experience steady growth, supported by strong industrial infrastructure, environmental regulations, and increasing investments in process optimization.

-

The United States dominated the regional market in 2025, driven by its extensive chemical processing industry, well-established municipal water treatment infrastructure, advanced manufacturing capabilities, and ongoing investments in industrial automation.

-

Canada is expected to maintain a significant position in the regional market, supported by its large mining sector, oil sands operations, and increasing demand for advanced separation technologies in natural resource industries.

-

Mexico is projected to strengthen its presence in the North American market during the forecast period, driven by rapid industrialization, expansion of manufacturing facilities, and growing investments in industrial processing infrastructure.

Competitive Landscape

The North America industrial centrifuges market is characterized by the presence of leading global manufacturers focusing on product innovation, energy efficiency, automation, and customized separation solutions. Market participants are investing in advanced centrifuge technologies, digital monitoring capabilities, and sustainable processing systems to improve operational performance across multiple industries. Strategic partnerships, capacity expansion, and continuous technological innovation continue to shape the competitive landscape.

Prominent companies operating in the North America industrial centrifuges market include Thomas Broadbent & Sons, Andritz AG, Alfa Laval AB, GEA Westfalia Separator Group GmbH, FLSmidth & Co. A/S, MI SWACO, Flottweg SE, Flottweg Separation Technology, Hiller GmbH, Ferrum AG, Pieralisi Group, and TEMA Systems, Inc.

North America Industrial Centrifuges Market Size

The size of the North America industrial centrifuges market was worth USD 3.64 billion in 2025. The North America market is anticipated to grow at a CAGR of 4.53% from 2026 to 2034 and be worth USD 5.42 billion by 2034 from USD 3.80 billion in 2026.

According to the United States Environmental Protection Agency, public wastewater treatment facilities in the nation process approximately 34 billion gallons of sewage daily, requiring immense mechanical separation capabilities to manage sludge and recover clean water. Furthermore, the integration of these mechanical separators into daily industrial routines is supported by the colossal scale of the regional energy sector. As per the United States Energy Information Administration, domestic crude oil production often averages 13 million barrels per day, necessitating extensive purification and dehydration processes at extraction sites and refineries. The World Bank indicates that global industrial production has expanded significantly over the last decade, driving an increased demand for reliable solid-liquid separation technologies. Consequently, the intersection of massive industrial throughput and stringent environmental compliance mandates defines the dynamic landscape of this vital mechanical separation sector across the continent.

MARKET DRIVERS

Rising Prevalence of Municipal Sludge Management

The expansion of municipal wastewater treatment facilities and the strict enforcement of sludge management regulations are expected to drive procurement as cities prioritize efficient waste recovery, which is majorly driving the expansion of the North American industrial centrifuges market. According to the United States Environmental Protection Agency, public wastewater treatment facilities in the nation process approximately 34 billion gallons of sewage daily, creating an immense and continuous demand for high-capacity decanter centrifuges. These massive machines are essential for the sludge dewatering process, which reduces the volume of solid waste by up to 95% before final disposal or agricultural application. The World Bank indicates that the urban population in the region is projected to continue its upward trajectory, further escalating the volume of municipal sewage requiring treatment. Furthermore, the Association of Metropolitan Water Agencies emphasizes that aging municipal infrastructure requires continuous upgrades to meet stringent federal discharge limits, forcing treatment plants to invest heavily in advanced solid-liquid separation technologies. Consequently, the relentless expansion of urban populations and the uncompromising regulatory push for environmental protection guarantee a steady and robust demand for industrial centrifuges across regional water management networks.

Surge in Petroleum Refining and Energy Extraction

The surge in domestic crude oil extraction and the scale of petroleum refining operations are likely to accelerate the adoption of specialized separation equipment, which is further boosting the regional market expansion. As per the United States Energy Information Administration, domestic crude oil production often reaches 13 million barrels per day, which requires extensive purification and dehydration processes at extraction sites and refineries. Industrial centrifuges are deployed extensively to separate drill cuttings from drilling muds, allowing companies to recover expensive synthetic fluids and minimize hazardous waste disposal costs. The American Petroleum Institute states that the regional refining sector processes millions of barrels of crude oil daily, requiring continuous mechanical separation to remove catalyst fines and purify final fuel products. Furthermore, the International Energy Agency notes that the transition toward heavier crude oil grades requires more intensive separation processes to achieve the desired fuel specifications. By providing the essential mechanical force required to separate dense solids from viscous hydrocarbons, these advanced machines have become an indispensable component of the regional energy extraction ecosystem, guaranteeing sustained and robust demand.

MARKET RESTRAINTS

High Capital Expenditure and Maintenance Protocols

Financial barriers are expected to continue influencing procurement strategies as smaller industrial facilities balance high costs with the need for modern technology, which is hindering the industrial centrifuges market growth in North America. For instance, the total installed cost of a custom-engineered industrial separation system can represent a significant portion of the capital budget allocated for facility upgrades. For regional chemical manufacturers and small municipal treatment plants operating on tight profit margins, these upfront financial barriers are often challenging without significant government subsidies or favorable financing arrangements. Furthermore, industry reports indicate that the balance of system costs and specialized installation labor expenses remain remarkably high. Smaller industrial facilities often face difficulties justifying the return on investment timeline associated with enterprise-grade separation solutions. Consequently, the prohibitive costs and the learning curve associated with deploying these advanced mechanical environments act as a substantial bottleneck preventing many smaller operators from fully leveraging modern separation technologies.

Operational Challenges and Energy Consumption

Operational efficiency will remain a critical focus as manufacturers work to mitigate the impact of abrasive materials and energy costs, which is further hampering regional market expansion. According to the International Energy Agency, the average power consumption of a large industrial separation system is substantial, drawing significant amounts of electricity continuously. When processing highly abrasive slurries such as mining tailings or silica sands, the internal bowls and scroll conveyors experience rapid degradation, requiring frequent and expensive replacements. Data indicates that the rising cost of industrial electricity across the region has inflated operational expenditures, severely compressing profit margins for energy-intensive separation processes. Furthermore, professional engineering societies state that unplanned downtime caused by catastrophic mechanical failure or excessive vibration can halt entire production lines, resulting in millions of dollars in lost revenue. Consequently, the relentless battle against mechanical degradation and the financial burden of energy consumption act as substantial restraints limiting the unrestricted expansion of the market.

MARKET OPPORTUNITIES

Strategic Integration of Predictive Maintenance

The strategic integration of advanced automation sensors and predictive maintenance algorithms is expected to enhance operational reliability and reduce unplanned downtime, which is a promising opportunity for the North American market. According to the International Society of Automation, the implementation of advanced vibration and temperature sensors in rotating equipment can reduce unplanned downtime by over 40%, significantly improving overall plant productivity. Manufacturers are now embedding Internet of Things connectivity into their centrifuges, allowing operators to monitor real-time performance metrics and adjust rotational speeds remotely via centralized control systems. Research emphasizes that the adoption of artificial intelligence-driven predictive models can analyze historical operational data to optimize maintenance schedules, extending the lifespan of critical components like bearings and seals. Furthermore, engineering associations note that automated lubrication systems integrated into modern designs ensure that internal components remain protected even under extreme operational loads. By transforming traditional mechanical separators into intelligent connected data nodes, equipment providers can offer premium subscription-based monitoring services, creating a profitable recurring revenue stream while simultaneously elevating the standard of industrial processing.

Proliferation of Biofuel Manufacturing

The proliferation of biofuel manufacturing facilities and the expansion of renewable energy production are projected to offer a lucrative channel for specialized separation applications, which is another notable opportunity for the North American industrial centrifuges market. According to the United States Department of Energy, the national production of biofuels recently reached over 18 billion gallons annually, creating a massive parallel demand for high-capacity disc stack centrifuges. These specialized machines are essential for the continuous purification of biomass slurries and the recovery of valuable catalysts used in the transesterification process. The International Energy Agency states that the global transition toward sustainable aviation fuels will require significant increases in biofuel production by the end of the decade, necessitating the deployment of thousands of advanced separation units. Furthermore, industry associations indicate that emerging sectors like algae-based biofuels rely entirely on continuous centrifugal harvesting to extract microscopic lipids from massive volumes of water. By capitalizing on the growth of the renewable energy sector, centrifuge manufacturers can unlock entirely new revenue streams and establish themselves as critical partners in the global energy transition.

MARKET CHALLENGES

Geopolitical Risks and Supply Chain Vulnerabilities

Geopolitical factors and supply chain vulnerabilities regarding critical raw materials are significant challenges to the North American industrial centrifuges market expansion. The manufacturing of high-performance industrial centrifuges relies heavily on the procurement of specialized corrosion-resistant alloys and high-strength materials, which are geographically concentrated. According to the World Bank, the global supply of critical metals required for heavy industrial machinery is susceptible to localized political instability and aggressive export restrictions. When international trade tensions escalate, the procurement costs of these essential materials surge, forcing manufacturers to either absorb the increased expenses or pass them on to clients. International financial institutions indicate that global freight costs and logistical bottlenecks have caused severe disruptions in the trade of specialized metals, leading to price volatility and extended lead times. Furthermore, metal institutes state that securing long-term supply agreements for these essential elements requires navigating complex international trade regulations and financial hedging strategies. Consequently, this inherent vulnerability to geopolitical shocks and supply chain bottlenecks complicates production planning and threatens the long-term economic viability of equipment manufacturing.

Stringent Environmental Compliance and Safety Standards

The implementation of stringent environmental regulations regarding industrial noise pollution and volatile organic compound emissions is further challenging the North American industrial centrifuges market growth. Industrial centrifuges operating at extreme rotational velocities generate significant acoustic noise and often handle volatile chemicals that can emit harmful vapors into the surrounding environment. According to the United States Environmental Protection Agency, federal mandates require industrial facilities to contain volatile organic compound emissions within specific thresholds, forcing centrifuge manufacturers to design completely sealed and heavily insulated enclosures. The Occupational Safety and Health Administration enforces rigorous workplace noise exposure limits, which necessitate the integration of advanced acoustic dampening materials and specialized vibration isolation mounts into every new machine design. Global health organizations emphasize that prolonged exposure to high-decibel industrial noise causes severe hearing damage and cardiovascular stress among plant workers, prompting authorities to continuously tighten permissible exposure limits. Furthermore, industry experts note that retrofitting older separation equipment to meet these modern environmental and safety standards requires extensive engineering modifications and expensive third-party certifications. Consequently, the financial and operational burden of maintaining absolute compliance with evolving regulations inflates development costs and complicates the commercialization of new mechanical separation technologies.

SEGMENTAL ANALYSIS

By Product Insights

The sedimentation centrifuges segment dominated the market in 2025 and is likely to maintain its market dominance throughout the forecast period as essential infrastructure for municipal and industrial wastewater treatment over the next few years. According to the United States Environmental Protection Agency, public wastewater treatment facilities in the nation process approximately 34 billion gallons of sewage daily, creating an immense and continuous demand for high-capacity decanter and clarifier centrifuges. These sedimentation machines are essential for the sludge dewatering process, which reduces the volume of solid waste by up to 80% before final disposal. The World Bank indicates that the urban population in the region is projected to exceed 300 million people by the end of the decade, further escalating the volume of municipal sewage requiring treatment. Furthermore, the Association of Metropolitan Water Agencies emphasizes that aging municipal infrastructure requires continuous upgrades to meet stringent federal discharge limits, forcing treatment plants to invest heavily in advanced solid-liquid separation technologies. The continuous modernization of these critical facilities ensures that sedimentation centrifuges will remain the foundational technology for municipal waste management across the continent.

By Technology Insights

The biological and pharmaceutical purification segment had the leading share of the North American market in 2025 and is expected to propel the expansion of disc stack centrifuges over the next few years. These highly specialized machines operate at extreme rotational velocities to separate delicate cellular debris from highly sensitive protein solutions without compromising the structural integrity of the active pharmaceutical ingredients. According to industry data, the regional biopharmaceutical sector continues to secure significant research funding, driving procurement of high-precision separation equipment. Regulatory bodies mandate that all biological therapeutics must undergo rigorous clarification processes to ensure absolute purity and patient safety before commercial distribution. Furthermore, global health organizations indicate that the push for pandemic preparedness has accelerated the construction of modular biomanufacturing facilities, which rely heavily on continuous disc stack centrifuges for rapid and scalable harvest operations. This reliance on high-speed biological separation guarantees a strong growth trajectory for this specific product category as manufacturers seek to maximize yield and ensure regulatory compliance in complex biological processes.

By Processing Mode Insights

The batch centrifuges segment had the major share of the regional market in 2025 and is predicted to sustain its leadership in pharmaceutical and fine chemical manufacturing due to its precise process control over the next few years. Fine chemical and pharmaceutical manufacturing often involve complex multi-step synthesis reactions where the final product must be separated from the reaction mother liquor with absolute precision to prevent cross-contamination. According to the American Chemical Society, the regional fine chemical sector generates significant annual revenue, relying on batch peeler and basket centrifuges to isolate high-purity active pharmaceutical ingredients. Regulatory authorities emphasize that batch processing allows manufacturers to validate and document every single separation step, ensuring strict compliance with current good manufacturing practice regulations. Furthermore, international engineering societies note that the flexibility of batch equipment allows facilities to rapidly switch between different product lines without requiring extensive mechanical reconfiguration. This operational flexibility, combined with strict regulatory compliance requirements, guarantees the continued market supremacy of batch centrifuges in high-value manufacturing.

By Application Insights

The continuous centrifuges segment accounted for the largest share of the North American industrial centrifuges market in 2025 and is likely to see rapid expansion as mining and mineral processing operations prioritize high-volume efficiency over the next few years. Modern mining operations process millions of tons of ore daily, requiring continuous solid-liquid separation to recover valuable minerals and manage volumes of hazardous waste slurry. According to the United States Geological Survey, the regional mining industry extracts billions of metric tons of raw materials, necessitating the deployment of high-capacity continuous decanter centrifuges. These continuous machines operate without interruption, providing a constant flow of separated solids and clarified liquids, which is essential for maintaining the throughput of mineral processing plants. The International Council on Mining and Metals states that the transition toward dry stack tailings requires continuous dewatering technologies to reduce the moisture content of waste slurry before environmental disposal. Furthermore, the World Bank indicates that the rising demand for critical minerals used in electric vehicle batteries is driving the expansion of continuous separation infrastructure to maximize resource recovery. This need for uninterrupted high-volume processing guarantees a rapid growth rate.

REGIONAL ANALYSIS

U.S. Industrial Centrifuges Market Analysis

The United States held the major share of the North American market in 2025 and is expected to remain the dominant market for centrifuge technologies due to its massive chemical processing and municipal water treatment infrastructure over the next few years. This nation commands a significant market share, reflecting its status as the primary hub for heavy industrial manufacturing and environmental management. The market status here is defined by the continuous integration of advanced separation technologies to ensure regulatory compliance and operational efficiency. According to the United States Environmental Protection Agency, public wastewater treatment facilities in the nation process approximately 34 billion gallons of sewage daily, requiring mechanical separation capabilities to manage sludge. The American Chemistry Council states that the regional chemical production output remains a pillar of the economy, demonstrating the scale of operations that rely on advanced mechanical separation technologies. Furthermore, the World Bank indicates that the total industrial production index in the region has expanded, driving an increased demand for reliable solid-liquid separation technologies. This commitment to technological modernization and massive industrial scale guarantees sustained and profitable market growth across the entire nation.

Canada Industrial Centrifuges Market Analysis

Canada is projected to maintain an influential position in the regional market due to its expansive mining operations and oil sands extraction activities over the next few years. This country secures a notable market share, reflecting its status as a leader in natural resource extraction and mineral processing. The market status here is influenced by the deployment of high-capacity decanter centrifuges to manage volumes of tailings and recover valuable minerals. According to Natural Resources Canada, the national mining sector extracts significant amounts of critical minerals, necessitating mechanical dewatering and purification processes. The Mining Association of Canada states that the transition toward dry stack tailings requires continuous separation technologies to reduce the moisture content of waste slurry before environmental disposal. Furthermore, the World Bank indicates that rising global demand for battery metals is driving the expansion of continuous separation infrastructure to maximize resource recovery. This commitment to resource optimization and environmental stewardship ensures sustained market leadership and robust commercial expansion across the nation.

Mexico Industrial Centrifuges Market Analysis

Mexico is expected to strengthen its strategic position in the continental market due to rapid industrialization and the expansion of domestic manufacturing networks over the next few years. This nation captures a significant market share, highlighting its transition toward sophisticated production facilities and water management infrastructure. The market status here is defined by the integration of advanced filtering centrifuges into automotive and chemical manufacturing processes to ensure product purity and recover valuable solvents. According to the National Institute of Statistics and Geography, the national industrial sector generates hundreds of billions of dollars in annual output, requiring continuous solid-liquid separation to maintain production quality. The Mexican Institute of Water Technology states that the deployment of advanced centrifugal systems in municipal facilities has increased to meet federal discharge limits for industrial effluent. Furthermore, the World Bank notes that improving economic stability and nearshoring trends are accelerating the adoption of advanced separation technologies across diverse manufacturing sectors. This focus on industrial expansion and environmental compliance guarantees continuous and robust commercial growth across the nation.

COMPETITIVE LANDSCAPE

The competitive landscape of the regional industrial separation sector is defined by intense rivalry among established multinational engineering corporations and specialized regional manufacturers. Major global brands leverage massive financial resources to dominate heavy industrial procurement channels through aggressive research investments and extensive distribution networks. These industry leaders continuously develop advanced automated separation systems to ensure absolute compliance with stringent environmental regulations. Meanwhile, regional players compete fiercely by emphasizing localized manufacturing capabilities and highly cost-effective maintenance solutions that resonate deeply with budget-constrained chemical plants. The market also witnesses a surge in strategic mergers and acquisitions as companies seek to consolidate their technological capabilities and acquire emerging sensor startups. Furthermore, digitalization initiatives have become a critical competitive differentiator, with firms adopting advanced Internet of Things connectivity to appeal to modern industrial buyers seeking seamless data integration. Ultimately, the competitive environment demands continuous adaptation to rapid technological shifts, ensuring that only the most agile and innovative organizations maintain their extended profitability and brand loyalty across all international industrial markets today and tomorrow, globally right here and now across the entire continental manufacturing infrastructure network, ensuring absolute operational excellence and reliability for all global commercial clients every single day across the globe.

KEY MARKET PLAYERS

A few of the prominent companies operating in the North America industrial centrifuges market are

- Thomas Broadbent & Sons

- Andritz AG

- Alfa Laval AB

- GEA Westfalia Separator Group GmbH

- FLSmidth & Co. A/S

- MI SWACO

- Flottweg SE

- Flottweg Separation Technology

- Hiller GmbH

- Ferrum AG

- Pieralisi Group

- TEMA Systems, Inc.

TOP PLAYERS IN THE MARKET

- GEA Group stands as a premier global technology brand actively transforming the industrial separation landscape through deep expertise in food and pharmaceutical processing. The organization focuses heavily on producing highly reliable filtering centrifuges that cater to the exacting standards of modern chemical manufacturing. Recently, the company completed a massive upgrade to its regional service infrastructure designed to provide predictive maintenance solutions for heavy industrial clients. This operational enhancement significantly improves equipment uptime and guarantees superior performance for global partners. By prioritizing technological excellence, the enterprise successfully attracts loyal clients and maintains a highly competitive edge.

- Flottweg SE functions as a highly innovative separation company dedicating significant resources toward the development of premium industrial centrifuges and decanters. The corporation utilizes its advanced research facilities to create unique, robust machines that perfectly separate dense solids from viscous liquids without compromising operational continuity. In a recent strategic initiative, the enterprise introduced a new series of corrosion-resistant separation equipment specifically engineered for harsh mining environments. This technological breakthrough enables the brand to capture the critical resource extraction segment without compromising on mechanical reliability. Through continuous product development, the company continues to solidify its formidable presence.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players employ strategic partnerships and technological integration to reinforce their competitive standing. Companies collaborate directly with automation software developers to embed advanced predictive maintenance algorithms directly into their centrifuge control systems. Mergers and acquisitions remain a common tactic, with major firms purchasing specialized sensor startups to instantly acquire advanced vibration monitoring capabilities. Investment in sustainable manufacturing methods, including the development of energy-efficient motors and recycled material components, helps meet strict environmental regulations. Geographic expansion, particularly into emerging industrial zones, allows access to new chemical and mining clients. Lastly, continuous investment in corrosion-resistant alloys ensures that all separation equipment remains perfectly optimized against evolving operational demands, ensuring extended commercial viability.

MARKET SEGMENTATION

This research report on the North America industrial centrifuges market is segmented and sub-segmented into the following categories.

By Product

- Sedimentation Centrifuges

- Clarifier Centrifuges

- Decanter Centrifuges

- Disc-Stack Centrifuges

- Hydrocyclones

- Other Sedimentation Centrifuges

- Filtering Centrifuges

- Basket Centrifuges

-

Scroll Screen Centrifuges

- Peeler Centrifuges

- Pusher Centrifuges

By Operation

- Batch Centrifuges

- Continuous Centrifuges

By Design

- Horizontal

- Vertical

By End User

- Chemical Industry

- Mining Industry

- Pharmaceutical and Biotechnology Industries

- Power Plants

- Food and Beverage Industry

- Pulp and Paper Industry

- Waste Water Treatment Plants

- Water Purification Plants

- Metal Processing Industry

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

What is the North America industrial centrifuges market?

The North America industrial centrifuges market is experiencing steady growth projected to maintain CAGR of 4.50% from 2025 to 2033 driven by increasing demand across key sectors such as food and beverage pharmaceuticals and water and wastewater treatment.

Why is the North America industrial centrifuges market growing?

The North America industrial centrifuges market expansion is driven by increasing demand across key sectors such as food and beverage pharmaceuticals water and wastewater treatment with advances in centrifuge technology including more efficient and automated systems fueling market growth.

What are the key applications of the North America industrial centrifuges market?

The North America industrial centrifuges market key sectors include food and beverage pharmaceuticals water and wastewater treatment chemical petrochemical industries renewable energy sustainable water management with centrifuges indispensable for exceptional ability to concentrate materials.

How is the North America industrial centrifuges market segmented?

The North America industrial centrifuges market is segmented by centrifuge type sedimentation filtering by design horizontal vertical by operation mode batch continuous and equipment type sedimentation centrifuges filtering centrifuges for tailored solutions across diverse applications.

What is the role of food and beverage in the North America industrial centrifuges market?

The North America industrial centrifuges market food and beverage sector is key driver with increasing demand for centrifuges in food processing beverage production and purification processes for efficient separation and quality control applications.

How does pharmaceutical impact the North America industrial centrifuges market?

The North America industrial centrifuges market pharmaceutical sector is key driver with centrifuges employed for several crucial jobs in biopharmaceutical industry where purity is utmost importance including isolating proteins separating cells from culture media and clarifying vaccines.

What is the role of water and wastewater treatment in the North America industrial centrifuges market?

The North America industrial centrifuges market water and wastewater treatment is primary growth trend with industries fighting to find affordable ways to maintain effluents sparkling cleanliness as environmental laws surrounding wastewater disposal become more stringent.

How does chemical industry benefit the North America industrial centrifuges market?

The North America industrial centrifuges market demand for centrifuges is rising due to expansion of chemical and petrochemical industries in North America with multipurpose devices indispensable because of exceptional ability to concentrate materials and separate impurities.

What is the role of sedimentation centrifuges in the North America industrial centrifuges market?

The North America industrial centrifuges market is segmented by centrifuge type including sedimentation centrifuges for solid liquid separation with superior efficiency in eliminating wide range of impurities including lumpy solids heavy metals and oily slicks.

How does filtering centrifuges impact the North America industrial centrifuges market?

The North America industrial centrifuges market is segmented by centrifuge type including filtering centrifuges for solid liquid separation with exceptional ability to eliminate impurities and outperform even the strictest environmental laws for wastewater disposal.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com