North America Over the Counter (OTC) Drugs Market Size, Share, Trends & Growth Forecast Report By Product Type (Analgesics, Cough, Cold, and Flu Products, Vitamins and Minerals, Dermatological Products, Gastrointestinal Products, Ophthalmic Products, Sleep Aid Products, Weight Loss/Diet Products, Others), Formulation Type, Distribution Channels & Country (The United States, Canada and Rest of North America), Industry Analysis From 2024 to 2033

North America Over the Counter Drugs Market Size

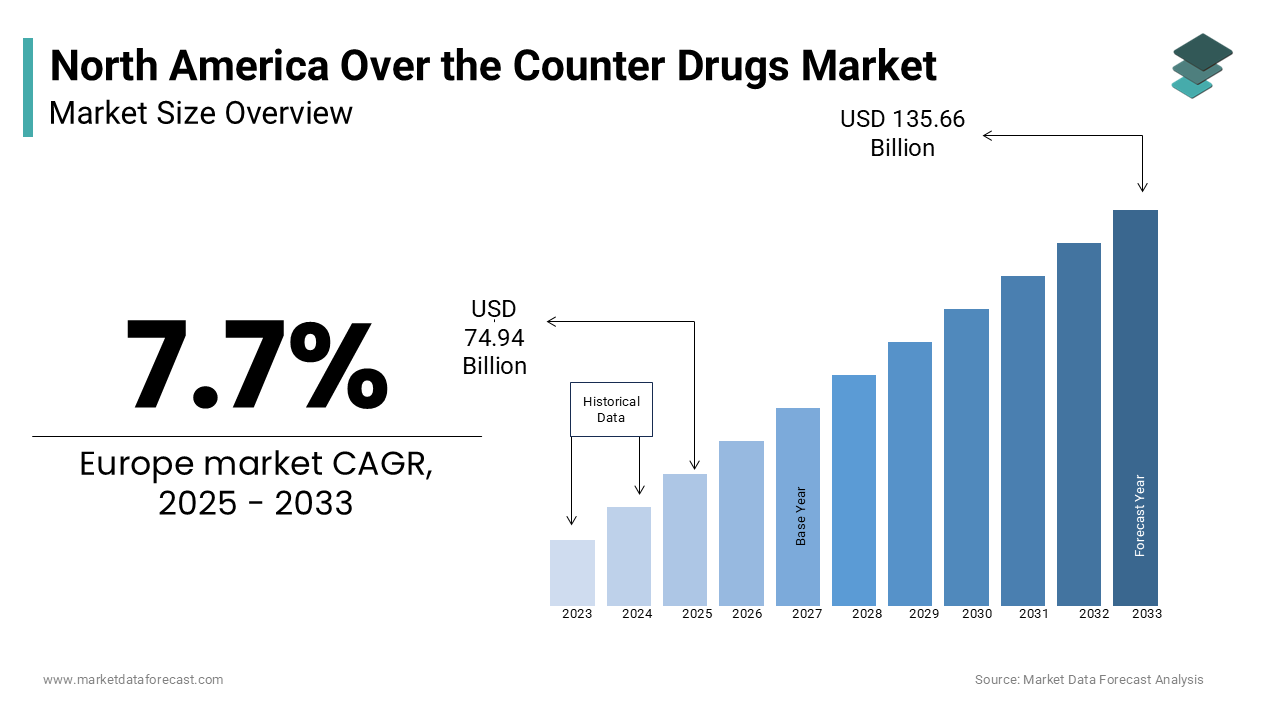

The over the counter (OTC) drugs market is anticipated to rise from USD 69.58 billion in 2024 to USD 135.66 billion in 2033, growing at a CAGR of 7.7%.

Over the Counter (OTC) Drugs refer to the non-prescription pharmaceuticals accessible directly to consumers for self-treatment of common ailments such as pain, allergies, colds, digestive issues, and sleep disorders. These products are regulated by national health authorities, primarily the U.S. Food and Drug Administration (FDA) and Health Canada, under monograph systems that define acceptable ingredients, dosages, and labeling. As per the Consumer Healthcare Products Association, over 800 OTC drug ingredients are approved under FDA monographs, forming the basis for more than 100,000 product variations available in retail and digital channels. The Centers for Disease Control and Prevention points out that 78% of American adults use at least one OTC medication annually, often as a first-line response to minor health concerns. These regulatory and behavioral frameworks underscore a mature, trust-driven market where accessibility and consumer education are paramount.

MARKET DRIVERS

The growing emphasis on healthcare cost containment and the shift toward preventive self-care are the primary drivers of the North America OTC Drugs Market. The Agency for Healthcare Research and Quality estimates that treating minor conditions like headaches, allergies, and heartburn with OTC medications saves the U.S. healthcare system a substantial amount annually in avoided consultations and diagnostic tests. In Canada, provincial health plans increasingly promote OTC use for non-urgent conditions to reduce primary care burden, as noted by the Canadian Institute for Health Information. Employers are integrating OTC allowances into health reimbursement arrangements. These economic incentives are institutionalizing OTC drugs as a sustainable component of healthcare efficiency.

The rising consumer preference for convenience and digital access to health products, accelerated by e-commerce and telehealth integration, is another significant driver. Major retailers like CVS, Walgreens, and Amazon have expanded digital health platforms that offer AI-powered symptom checkers, virtual pharmacist consultations, and same-day delivery. Additionally, telehealth providers recommend OTC treatments during virtual consultations, creating a seamless care-to-purchase pathway. This convergence of digital health infrastructure and consumer behavior is transforming OTC drugs from passive purchases into integrated elements of proactive health management across North America.

MARKET RESTRAINTS

The persistent risk of misuse, overuse, and adverse drug interactions due to limited consumer awareness is a major restraint in the North America OTC Drugs Market. In 2023, U.S. Poison Centers recorded 2.42 million exposure cases. These safety concerns necessitate enhanced labeling, public education, and pharmacist engagement to mitigate public health risks.

The regulatory complexity and lengthy approval timelines for Rx-to-OTC switches, which delay consumer access to newly available self-care options, are another critical restraint. Additionally, Health Canada requires post-switch monitoring programs, increasing the burden on manufacturers. These regulatory hurdles discourage investment in switch candidates, particularly for niche indications, limiting innovation and slowing the expansion of the OTC therapeutic landscape despite demonstrated consumer demand for greater autonomy.

MARKET OPPORTUNITIES

The expansion of personalized OTC products tailored to genetic, lifestyle, and demographic factors, is a transformative opportunity. Companies have begun integrating genetic insights with OTC recommendations, driven assessments to suggest supplements based on diet, age, and health goals, with sales increasing. These data-driven models enable targeted self-care, improve adherence, and reduce trial-and-error usage. With growing consumer comfort in sharing health data, the convergence of genomics, AI, and retail health positions personalized OTC products as a high-growth frontier in preventive medicine.

Another emerging opportunity is the integration of OTC drugs into value-based care and employer-sponsored wellness programs. Additionally, pharmacy benefit managers are incorporating OTC utilization data into health analytics platforms to identify early signs of chronic conditions. These integrations position OTC drugs not as isolated remedies but as strategic tools in population health management and preventive care ecosystems.

MARKET CHALLENGES

The increasing scrutiny over ingredient safety and long-term health impacts, particularly for widely used compounds, is a critical challenge facing the North American OTC Drugs Market. In 2023, the agency proposed stricter limits on pseudoephedrine-containing decongestants due to links with hypertension and stroke in vulnerable populations. These regulatory actions reflect growing scientific caution and may lead to consumer hesitancy. Additionally, litigation over alleged carcinogenic impurities in antacids containing ranitidine has resulted in class-action lawsuits and product recalls, undermining trust. Without continuous safety monitoring and transparent communication, such controversies can erode consumer confidence and trigger market volatility.

The intensifying competition from private-label and store-brand OTC products, which pressure profit margins and brand loyalty, is another pressing challenge. These store brands often mirror active ingredients and dosages of leading national products, making differentiation difficult. Consumer trust in store brands is high. This shift forces manufacturers to invest more in marketing, packaging innovation, and clinical substantiation to justify premium pricing. Without clear therapeutic or experiential differentiation, even established brands face erosion in market share and pricing power.

SEGMENTAL ANALYSIS

By Product Type Insights

The Analgesics segment dominated the North America Over the Counter Drugs Market by capturing 25.2% of the total value in 2024. This lead position is primarily driven by the widespread prevalence of chronic and acute pain conditions across the population. According to the Centers for Disease Control and Prevention, over 51 million adults in the United States suffer from chronic pain, with 19 million experiencing high-impact pain that limits daily activities. As a result, non-prescription pain relievers such as ibuprofen, acetaminophen, and naproxen are among the most frequently purchased OTC drugs. The accessibility, fast onset, and multi-symptom formulations, such as those combining pain relief with cold or sleep aid components, further solidify analgesics as the cornerstone of self-care in North America.

The Vitamins and Minerals segment is the fastest-growing segment and is projected to expand at a CAGR of 9.6% from 2025 to 2033. This acceleration is fueled by rising consumer focus on preventive health, immune support, and personalized wellness. Also, a high percentage of U.S. adults take dietary supplements regularly, with multivitamins, vitamin D, and omega-3 fatty acids being the most consumed. Additionally, the integration of genetic testing and digital health platforms has enabled personalized vitamin regimens, with companies reporting year-over-year growth in subscription-based sales. These behavioral shifts, amplified by post-pandemic health consciousness, are transforming vitamins from basic supplements into high-value, data-driven health solutions.

By Formulation Type Insights

The Tablets segment led the North America OTC Drugs Market by accounting for 44.6% of total formulation-based sales in 2024. This dominance is driven by consumer preference for precise dosing, portability, and ease of storage. Tablets are the preferred form for analgesics, antihistamines, and gastrointestinal medications due to their stability and long shelf life. Additionally, manufacturers benefit from lower production and packaging costs compared to liquids or sprays, enabling competitive pricing. These factors, clinical reliability, consumer familiarity, and manufacturing efficiency, cement tablets as the dominant formulation in self-medication.

The Spray segment is the fastest-growing segment and is anticipated to grow at a CAGR of 10.2% through 2033. This surge is driven by increasing demand for rapid-acting, non-invasive delivery systems, particularly for nasal, oral, and topical applications. Additionally, oral sprays for pain and sleep, such as CVS Health’s dissolving mouth spray for migraines—offer alternatives for individuals with swallowing difficulties. The rise of portable, travel-friendly formats and innovations like metered-dose and pump sprays has enhanced usability. Hence, sprays are emerging as a preferred format for acute and on-the-go symptom management.

By Distribution Channels Insights

The Pharmacies segment commanded the North America OTC Drugs Market by contributing 52.7% of total distribution channel sales in 2024. This lead position is rooted in consumer trust, professional guidance, and strategic product placement. Additionally, pharmacy loyalty programs and digital integration, such as prescription-auto-refill linked to OTC recommendations, enhance customer retention. These factors position pharmacies as trusted hubs for informed self-care, far surpassing other retail environments in credibility and service depth.

The Others (online drug stores) segment is the fastest-growing segment and is projected to grow at a CAGR of 14.8% from 2025 to 2033. This rapid expansion is driven by the proliferation of e-commerce, telehealth integration, and mobile-first consumer behavior. Amazon Pharmacy reported a rise in OTC unit sales, driven by same-day delivery, AI-powered symptom checkers, and integration with Alexa health features. Additionally, telehealth platforms like Teladoc and PlushCare now recommend and directly link to OTC purchases post-consultation, creating seamless digital care pathways. With Walmart, Target, and Kroger expanding their digital pharmacy networks, online channels are transforming from supplemental to primary access points for self-care products.

REGIONAL ANALYSIS

The United States held the dominant position in the North America Over the Counter Drugs Market by contributing 85.1% of the total regional value in 2024. The nation’s market status is defined by its vast consumer base, high healthcare costs, and deeply embedded self-care culture. As per the CDC, 78% of American adults use OTC medications annually. The U.S. Food and Drug Administration regulates over 800 OTC active ingredients under its monograph system, ensuring product safety and accessibility. Major retailers like CVS, Walgreens, and Walmart operate integrated health ecosystems that combine physical stores, digital platforms, and pharmacist consultations. In 2023, the U.S. accounted for over 95% of Rx-to-OTC switches in North America, including the recent transition of nasal spray Flonase from prescription to OTC. These structural advantages, scale, regulation, and innovation, solidify the U.S. as the global epicenter of OTC drug consumption and development.

Canada maintains a stable, regulated self-care environment. The country’s market status is characterized by strong public health guidance and pharmacist involvement in consumer decision-making. The market is dominated by national chains such as Shoppers Drug Mart and London Drugs, which offer private-label brands and digital health tools. In 2023, OTC sales in Canada reached CAD 3.2 billion, with analgesics and cold remedies leading demand. Health Canada’s rigorous safety monitoring has led to updated labeling for NSAIDs and sleep aids, reflecting a precautionary regulatory stance. Despite a smaller population, Canada’s high per capita OTC usage and integration with provincial health systems ensure its significance in the regional landscape.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

GlaxoSmithKline, Johnson and Johnson, Novartis, Bayer, Pfizer, Sanofi, and Takeda are companies that play a dominant role in the North American over-the-Counter (OTC) Drugs Market. GlaxoSmithKline, Johnson and Johnson, Novartis, and Sanofi possess the maximum market share.

The competition in the North America Over the Counter Drugs Market is characterized by a concentrated yet dynamic landscape dominated by multinational corporations with deep brand equity and distribution networks. While Kenvue, Procter & Gamble, and Bayer lead through scale and innovation, private-label brands from retailers like CVS, Walgreens, and Walmart are gaining traction by offering cost-effective alternatives. Differentiation is increasingly achieved through digital integration, personalized health solutions, and clean-label formulations rather than price alone. The market is highly sensitive to consumer trust, regulatory changes, and safety perceptions, making transparency and clinical credibility critical. Emerging players are leveraging e-commerce and telehealth partnerships to challenge incumbents. Competitive advantage lies in omnichannel presence, speed to market for new formulations, and the ability to align with preventive health trends. As self-care becomes integral to healthcare efficiency, the competitive frontier is shifting toward holistic, data-driven consumer engagement.

Top Players in the North America Over the Counter Drugs Market

Johnson & Johnson (Kenvue) has long been a dominant force in the North America OTC Drugs Market through its extensive portfolio of trusted brands such as Tylenol, Motrin, Benadryl, and Listerine. Following the spin-off of its consumer health division into Kenvue in 2023, the company has intensified its focus on digital engagement, personalized wellness, and e-commerce integration. Kenvue launched a direct-to-consumer platform offering AI-driven symptom assessments and tailored product recommendations, enhancing user experience across its pain, allergy, and oral care lines. The company has also invested in clean-label formulations, reformulating products to eliminate artificial dyes and preservatives in response to consumer demand. These initiatives reinforce its leadership in brand trust, innovation, and responsible self-care.

Procter & Gamble (P&G) plays a pivotal role in shaping the OTC landscape through flagship brands like Vicks, Pepto-Bismol, Metamucil, and Prilosec OTC, which are deeply embedded in American households. The company has leveraged its consumer insights engine to develop multi-symptom formulations that address complex conditions such as colds with congestion, fever, and sore throat in a single dose. It also expanded its e-commerce presence through Amazon Health and Walmart’s digital pharmacy, optimizing fulfillment speed and visibility. These strategies reflect a blend of technological integration, public health engagement, and omnichannel distribution.

Bayer Consumer Health maintains a strong presence in the North America OTC market with well-established brands including Aleve, Phillips’ Laxative, One A Day, and Bactine. The company has focused on science-based formulations and preventive health positioning, particularly in the vitamins and pain relief categories. It also enhanced its digital footprint by integrating with telehealth providers such as Teladoc to recommend Bayer products post-consultation. These efforts position Bayer as a leader in evidence-based, digitally enabled self-care solutions.

Top Strategies Used by Key Market Participants

Key players in the North America Over the Counter Drugs Market are deploying multifaceted strategies centered on digital transformation, brand trust, and consumer-centric innovation. Companies are integrating AI-powered symptom checkers, mobile apps, and e-commerce platforms to enhance accessibility and personalization. Direct-to-consumer models and subscription services are being expanded to improve retention and predictability. Firms are reformulating products to eliminate artificial ingredients, aligning with clean-label trends and health-conscious demand. Strategic partnerships with pharmacists, telehealth providers, and employers enable broader reach within preventive care ecosystems. Investment in Rx-to-OTC switches is accelerating, supported by consumer use studies and regulatory engagement. Private-label competition is being countered through packaging innovation, clinical substantiation, and loyalty programs. Sustainability is prioritized via recyclable materials and carbon-neutral manufacturing. Additionally, companies are leveraging real-world data from digital platforms to inform R&D and marketing. These strategies collectively aim to balance regulatory compliance, consumer trust, and technological agility in a highly competitive, trust-driven market.

RECENT MARKET DEVELOPMENTS

- In February 2023, Kenvue launched a direct-to-consumer digital platform offering AI-driven symptom assessments and personalized product recommendations for Tylenol and Benadryl, enhancing user engagement in the North America Over the Counter Drugs Market.

- In August 2023, Procter & Gamble introduced smart packaging for Vicks inhalers with scannable QR codes linking to dosage reminders and health content, strengthening patient adherence in the North America Over the Counter Drugs Market.

- In January 2024, Bayer Consumer Health integrated its One A Day brand with Teladoc’s telehealth platform, enabling personalized vitamin recommendations post-consultation in the North America Over the Counter Drugs Market.

- In June 2023, Kenvue achieved 100% recyclable packaging for its Listerine and Tylenol lines, reinforcing its sustainability leadership in the North America Over the Counter Drugs Market.

- In November 2023, Procter & Gamble expanded its digital pharmacy partnership with Walmart, optimizing e-commerce visibility and same-day delivery for Vicks and Pepto-Bismol in the North America Over the Counter Drugs Market.

MARKET SEGMENTATION

This research report on the North American over-the-counter drugs market has been segmented and sub-segmented into the following categories.

By Product Type

- Analgesics

- Cough, Cold, and Flu Products

- Vitamins and Minerals

- Dermatological Products

- Gastrointestinal Products

- Ophthalmic Products

- Sleep Aid Products

- Weight Loss/Diet Products

- Others

By Formulation Type

- Tablets

- Liquids

- Ointments

- Spray

By Distribution Channels

- Pharmacies

- Supermarkets/Hypermarkets

- Convenience store

- Others (online drug stores)

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

Which countries contribute the most to the North America OTC drugs market share?

The United States holds the largest market share in North America, followed by Canada and Mexico.

How has the COVID-19 pandemic impacted the North America OTC drugs market?

The market has witnessed a surge in demand for OTC drugs during the pandemic, driven by the need for at-home treatments and preventive healthcare measures.

What demographic factors are shaping the consumption patterns of OTC drugs in North America?

The aging population, coupled with a preference for self-care among millennials, is influencing the consumption patterns of OTC drugs in North America.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com