North America Termite Control Market Size, Share, Growth, Trends, And Forecasts Report, Segmented Report, Segmented By Type, Control Method, Application, And By Country (US, Canada, Mexico and Rest of North America), Industry Analysis From (2026 to 2034)

North America Termite Control Market Size

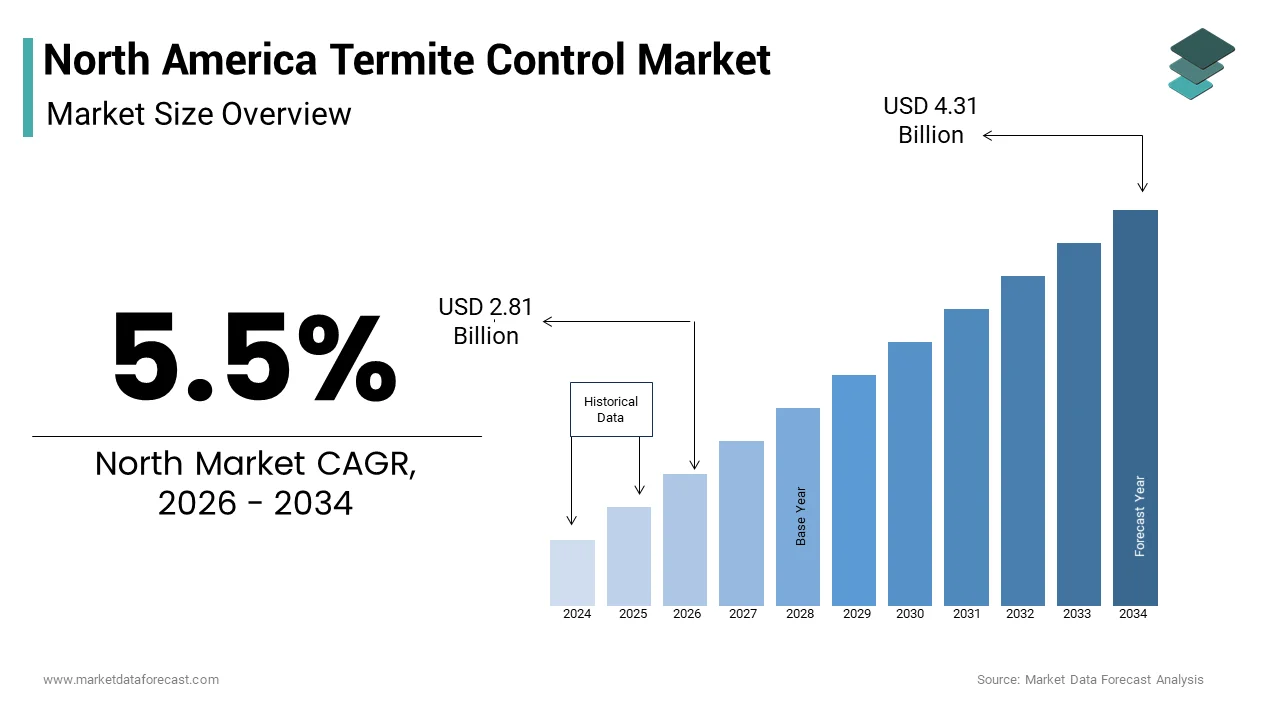

The North America termite control market size was valued at USD 2.66 billion in 2025 and is anticipated to reach USD 2.81 billion in 2026 to reach USD 4.31 billion by 2034, growing at a CAGR of 5.5% during the forecast period from 2026 to 2034.

The North America Termite Control Market encompasses a range of chemical and biological solutions aimed at managing termite infestations in residential, commercial, and industrial structures. Termites, often referred to as "silent destroyers," cause significant structural damage by feeding on wood and other cellulose-based materials. According to the National Pest Management Association, termites inflict over $5 billion in property damage annually across the United States alone. The market is primarily driven by the increasing frequency of termite infestations due to shifting climatic conditions and rising construction activities. As per data from the U.S. Census Bureau, over 1.6 million housing units were authorized for construction in the U.S. in 2023, amplifying the need for preventive pest control measures. Additionally, heightened consumer awareness regarding integrated pest management practices has led to greater adoption of eco-friendly and long-term termite control solutions.

MARKET DRIVERS

Rising Urbanization and Construction Activities

One of the primary drivers fueling the North America Termite Control Market is the surge in urbanization and construction activities across the region. According to the U.S. Census Bureau, approximately 1.6 million housing units were authorized for construction in the United States in 2023, reflecting a consistent upward trend in new residential development. This growth directly correlates with an increased demand for termite prevention and control solutions, as newly built structures are highly susceptible to infestation. In Canada, the Canadian Mortgage and Housing Corporation reported that over 240,000 housing starts occurred in 2023, which further reinforces the necessity for proactive pest management strategies.

Urban expansion into forested or rural areas, where termites are more prevalent, has exposed more buildings to potential infestation risks. The southeastern United States, in particular, is known for its high termite activity due to favorable climatic conditions. As per the University of Florida’s Department of Entomology, states like Florida, Georgia, and Louisiana report some of the highest termite-related damages annually. These factors have prompted homeowners, developers, and property managers to invest heavily in preventive and curative termite control measures. Moreover, stringent building codes now require pre-construction termite treatments in many jurisdictions, further boosting market growth.

Increasing Consumer Awareness and Demand for Eco-Friendly Solutions

Another significant driver shaping the North America Termite Control Market is the growing consumer awareness regarding sustainable and environmentally friendly pest control methods. As public concern over chemical exposure and ecological impact intensifies, homeowners and businesses are increasingly opting for green alternatives. According to a 2023 survey conducted by the National Pest Management Association, nearly 68% of homeowners expressed a preference for non-toxic or low-chemical treatment options when selecting pest control services. This shift aligns with broader environmental trends and is supported by regulatory bodies promoting reduced pesticide usage.

Innovations such as baiting systems and biological termiticides have gained traction due to their minimal environmental footprint and targeted action against termite colonies. For instance, companies like BASF and Syngenta have introduced bio-based termite control formulations that comply with EPA guidelines while maintaining high efficacy. Additionally, the U.S. Environmental Protection Agency has been actively encouraging the adoption of Integrated Pest Management (IPM) strategies, which combine physical barriers, monitoring, and selective chemical use to reduce overall environmental impact.

MARKET RESTRAINTS

High Cost of Advanced Termite Control Technologies

A significant restraint impeding the growth of the North American termite control Market is the high cost associated with advanced termite control technologies. While innovations such as baiting systems, remote monitoring devices, and non-repellent termiticides offer enhanced efficiency and long-term protection, their premium pricing often deters price-sensitive consumers. According to a 2023 report by the Joint Center for Housing Studies at Harvard University, nearly 40% of American homeowners cited affordability as a major barrier to investing in comprehensive pest control services. Moreover, professional termite inspections and preventative treatments can range from $1,200 to $2,500 on average, depending on the size and location of the property. For small property owners and landlords operating on tight budgets, this represents a considerable financial burden. Additionally, the lack of standardized insurance coverage for termite damage exacerbates the situation, leaving homeowners fully responsible for treatment expenses.

Stringent Regulatory Requirements and Compliance Burdens

Stringent regulatory requirements represent another major challenge for the North American termite Control Market. The use of chemical pesticides and termiticides is heavily regulated by agencies such as the U.S. Environmental Protection Agency (EPA) and Health Canada’s Pest Management Regulatory Agency (PMRA). These organizations enforce rigorous testing, registration, and labeling protocols to ensure human and environmental safety. These regulatory hurdles not only slow down the introduction of new products but also elevate operational costs for pest control service providers. Companies must invest significantly in compliance training, documentation, and safety measures to meet federal and state-level mandates. For example, California’s Department of Pesticide Regulation enforces some of the strictest guidelines in the country, requiring extensive environmental impact assessments before approving any new termite control product. Such constraints disproportionately affect smaller firms with limited resources, reducing market competition and limiting innovation.

MARKET OPPORTUNITIES

Expansion of Smart Termite Monitoring Systems

A promising opportunity emerging in the North American termite Control Market is the rapid advancement and adoption of smart termite monitoring systems. These technology-driven solutions integrate IoT-enabled sensors, real-time data analytics, and cloud-based reporting to detect early signs of termite activity with high precision. According to a 2023 report by the global smart pest control market is projected to grow at a compound annual growth rate (CAGR) of 14.7% between 2023 and 2030, with North America leading in early adoption. This trend is being fueled by increasing demand for predictive maintenance solutions in both residential and commercial properties. Smart monitoring systems offer a proactive alternative to traditional inspection methods by continuously tracking underground termite movement and transmitting alerts to pest control professionals and property owners. Companies such as Sentricon and Nisus Corp have already introduced sensor-based bait stations that enhance detection accuracy while minimizing chemical usage. Additionally, the integration of AI algorithms for pattern recognition allows for more efficient identification of infestation hotspots.

Growing Demand for Preventive Termite Management in Commercial Real Estate

An emerging opportunity within the North America Termite Control Market is the increasing emphasis on preventive termite management in the commercial real estate sector. Property developers, facility managers, and institutional investors are recognizing the importance of proactive pest control strategies to safeguard asset value and avoid costly repairs. Preventive termite control programs, including soil treatments, perimeter barriers, and regular monitoring contracts, are gaining traction among commercial property stakeholders. In particular, large-scale office complexes, retail centers, and hospitality establishments are prioritizing scheduled inspections to maintain structural integrity and comply with health and safety regulations. As per the Building Owners and Managers Association (BOMA), over 60% of commercial property managers in North America have incorporated termite prevention into their annual facility maintenance plans.

Furthermore, the rise in green building certifications such as LEED (Leadership in Energy and Environmental Design) is influencing the adoption of sustainable yet effective termite management techniques. This shift is prompting pest control service providers to develop customized preventive packages tailored to commercial clients, thereby unlocking a high-growth segment within the termite control market.

MARKET CHALLENGES

Climate Change and Expanding Termite Habitats

One of the foremost challenges facing the North American termite Control Market is the impact of climate change on termite proliferation and habitat expansion. Rising temperatures, prolonged warm seasons, and shifting precipitation patterns have created more conducive environments for subterranean and drywood termites to thrive beyond their traditional geographic ranges. This warming trend has allowed termites to establish colonies in previously inhospitable regions, including northern U.S. states and parts of southern Canada. Encountering new infestation patterns that require adaptive treatment strategies and expanded service territories. The growing unpredictability of termite behavior due to climate variability complicates conventional control methods and necessitates ongoing research and investment in resilient mitigation technologies. This evolving scenario poses a persistent challenge for market players striving to keep pace with changing infestation dynamics.

Public Misconceptions and Lack of Awareness About Termite Risks

A significant challenge affecting the North American termite Control Market is the prevalence of public misconceptions and inadequate awareness regarding termite risks and the importance of professional pest management. Many homeowners underestimate the severity of termite infestations, believing them to be rare or easily manageable through DIY solutions. According to a 2023 survey conducted by the National Pest Management Association, nearly 35% of American homeowners were unaware that standard homeowners' insurance policies typically do not cover termite damage. This knowledge gap results in delayed or insufficient treatment, which is allowing infestations to escalate and cause extensive structural harm. Additionally, misinformation about the effectiveness of over-the-counter sprays and home remedies leads to ineffective control measures. A study published by the Journal of Economic Entomology found that 42% of homeowners who attempted self-treatment failed to eliminate active termite colonies, ultimately requiring more expensive professional intervention later. The lack of education on preventive termite control further hampers market growth, as many property owners only seek services after visible damage occurs. Addressing these misconceptions requires sustained consumer outreach and collaboration between industry players and regulatory agencies to promote informed decision-making and encourage proactive termite management practices.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2023 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.5% |

| Segments Covered | By Type, By Control Method, By Application |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | U.S.A, Canada |

| Market Leaders Profiled | BASF SE (Germany), The Dow Chemical Company (U.S.), Bayer CropScience AG (Germany), Syngenta AG (Switzerland), Sumitomo Chemical Co. (Japan), FMC Corporation (U.S.), Nufarm Limited (Australia), United Phosphorus Limited (India), Rentokil Initial plc. (U.K.), ADAMA Agricultural Solutions Ltd. (Israel), Nippon Soda (Japan), Control Solution plc. (U.S.), and Ensystex (U.S.). |

COUNTRY ANALYSIS

By Species Insights

The subterranean termites segment was the dominant shareholder in the North American termite control market in 2024. Although not explicitly listed as a standalone category, subterranean termites fall under the “Other” segment and are by far the most destructive and widespread termite species across the continent. According to the University of Florida’s Department of Entomology and Nematology, subterranean termites are responsible for more than 80% of all termite-related property damage in the United States. Unlike drywood termites, which infest only dry wood, subterranean termites construct mud tubes to access above-ground structures, making them particularly challenging to detect and eradicate. The U.S. Environmental Protection Agency reported that approximately 1 in 20 homes inspected in high-risk regions like the Southeastern U.S. showed signs of active subterranean termite infestation in 2023. This high prevalence necessitates robust chemical treatments, baiting systems, and soil barriers, contributing significantly to market growth.

The drywood termite segment is swiftly emerging with an estimated CAGR of 7.4% in the coming years. One key driver behind this rapid growth is the expansion of housing developments in warmer, drier climates where drywood termites thrive. These termites do not require contact with soil and can infest wooden structures directly, making them difficult to detect until significant damage occurs. Additionally, the rise in imported wooden furniture and construction materials has inadvertently introduced drywood termite colonies into new regions.

By Control Method Insights

The chemical control methods were the largest and held 55.3% of the North America Termite Control Market share in 202,4, with the widespread reliance on liquid termiticides, soil treatments, and residual sprays that offer long-term protection against termite infestations. A primary factor driving the continued preference for chemical controls is their proven efficacy in creating protective barriers around structures. Industry leaders such as BASF, Syngenta, and Dow AgroSciences have developed advanced formulations like fipronil- and chlorantraniliprole-based termiticides that provide multi-year protection with minimal reapplication needs. Furthermore, regulatory support has reinforced the safety and effectiveness of modern chemical formulations. The EPA’s registration process ensures that only environmentally compliant products enter the market, fostering consumer confidence.

The biological control methods segment is likely to grow with an esteemed CAGR of 9.2% in the coming years. This surge is largely attributed to heightened environmental concerns and a shift toward sustainable pest management practices. Biological agents such as entomopathogenic fungi (e.g., Metarhizium anisopliae and Beauveria bassiana ) and nematodes are gaining traction due to their low toxicity to humans and non-target organisms. Government initiatives promoting eco-friendly pest control strategies are also fueling adoption. The U.S. Department of Agriculture has funded multiple research projects exploring microbial-based termite suppression techniques. Additionally, consumer demand for green-certified buildings and pesticide-free environments is pushing commercial and residential developers to integrate biological control into their pest management protocols, further propelling this segment’s rapid ascent.

By Application Insights

The residential application segment is expected to hold a prominent share of the North America Termite Control Market in 2024, with the vast number of single-family homes, townhouses, and condominiums vulnerable to termite infestations, particularly in warm and humid regions. According to the U.S. Census Bureau, there were over 140 million housing units in the United States in 2023, with more than 80% constructed using wood or wood-based materials ideal food sources for termites. Homeowners’ increasing awareness of the financial implications of undetected termite damage has led to higher adoption of both preventive and curative termite control services. The National Pest Management Association estimates that nearly 13 million American homes undergo termite inspections annually, with a significant portion opting for long-term treatment plans. Moreover, lending institutions often mandate termite inspections before mortgage approvals, especially in high-risk states like Texas, Louisiana, and Georgia. In Canada, the Canadian Mortgage and Housing Corporation reported that termite-related insurance claims rose by 18% between 2019 and 2023, underscoring the growing concern among residential property owners. Coupled with rising home values and stricter building codes requiring pre-construction termite treatments, the residential sector continues to be the most lucrative and dominant application area in the termite control market.

The commercial and industrial application segment is deemed to grow with a CAGR of 8.1% from 2025 to 2033. Facility managers and institutional investors are increasingly integrating termite control into routine maintenance contracts to safeguard asset value and ensure uninterrupted operations. The Building Owners and Managers Association (BOMA) reported that over 60% of commercial property managers in North America now include annual termite inspections as part of their facility maintenance strategy. Additionally, the rise in green building certifications such as LEED has encouraged the adoption of environmentally friendly yet effective termite control measures in commercial spaces. Technological advancements, including remote monitoring systems and baiting stations tailored for large facilities, are further enhancing the appeal of commercial termite management.

COUNTRY-LEVEL ANALYSIS

United States Termite Control Market Analysis

The United States was the top performer in the 80.2% of the North America Termite Control Market share in 2024. As the largest economy and one of the most developed real estate markets globally, the U.S. experiences significant termite activity due to its diverse climate zones and extensive use of wooden structures in residential and commercial construction. Termites cause over $5 billion in structural damage annually in the U.S., as reported by the National Pest Management Association, making termite control a critical component of property management. High consumer awareness, stringent building regulations, and the presence of major pest control service providers such as Orkin, Terminix, and Rollins Inc. contribute to the country’s market dominance. Additionally, the Federal Housing Administration mandates termite inspections for FHA-insured loans, further boosting service demand across real estate transactions.

Canada Termite Control Market Analysis

Canada termite control Market, with steady growth in recent years. Though historically less affected by termites compared to the U.S., Canada has witnessed a noticeable increase in termite infestations, particularly in southern provinces like Ontario, Quebec, and British Columbia. According to the Canadian Food Inspection Agency, termite sightings have risen by over 25% since 2018, largely due to warming temperatures linked to climate change.

The Canadian housing market held 12.3% of the share in 2024. In 2023, Statistics Canada reported over 240,000 housing starts, many of which incorporated wood-frame construction methods susceptible to termite attack. According to the Canadian Mortgage and Housing Corporation, a 15% increase in termite-related insurance claims between 2020 and 2023, indicating growing homeowner vulnerability. While awareness remains lower than in the U.S., the introduction of advanced baiting systems and regulatory support for integrated pest management strategies is gradually transforming the landscape. Municipalities in high-risk areas are beginning to enforce pre-construction termite barriers, which signals a shift toward proactive prevention and strengthening Canada’s position in the regional termite control market.

COMPETITIVE LANDSCAPE

The competition in the North American termite Control Market is characterized by a mix of established national brands, regional pest control firms, and emerging technology-driven service providers. While industry leaders dominate due to their strong brand presence, wide service networks, and advanced product portfolios, smaller players are gaining traction by offering niche solutions and localized expertise. The market remains highly fragmented, with numerous companies competing based on service quality, technological adoption, and pricing strategies. Innovation is a key battleground, as firms strive to develop more effective, sustainable, and cost-efficient termite control methods. Additionally, customer trust and brand reputation play a critical role in shaping competitive dynamics, particularly in the residential sector, where word-of-mouth and reliability are essential.

KEY MARKET PLAYERS

The key players in this market include

- BASF SE (Germany)

- The Dow Chemical Company (U.S.)

- Bayer CropScience AG (Germany)

- Syngenta AG (Switzerland)

- Sumitomo Chemical Co. (Japan)

- FMC Corporation (U.S.)

- Nufarm Limited (Australia)

- United Phosphorus Limited (India)

- Rentokil Initial plc. (U.K.),

- ADAMA Agricultural Solutions Ltd. (Israel)

- Nippon Soda (Japan)

- Control Solution plc. (U.S.)

- Ensystex (U.S.).

Top Players in the Market

Orkin, a subsidiary of Rollins Inc., stands as one of the leading pest control service providers in North America. With decades of expertise, Orkin has built a strong reputation for delivering comprehensive termite inspection, prevention, and treatment services. The company leverages advanced technologies such as baiting systems and remote monitoring to offer tailored solutions for residential and commercial clients.

Terminix International Company, now part of Anticimex, is another major player known for its extensive experience in termite control. Terminix has been instrumental in developing long-term protection plans that include regular inspections and guaranteed treatments. Their focus on eco-friendly products and digital integration in service delivery has enhanced their appeal among environmentally conscious consumers and large property managers.

BASF SE, while primarily a chemical manufacturing giant, plays a crucial role in the termite control ecosystem by supplying active ingredients used in termiticides. The company supports pest control professionals with high-performance formulations that enhance the efficacy of liquid barriers and baiting systems. Through continuous R&D investments, BASF contributes significantly to innovation in termite management across North America.

Top Strategies Used By Key Market Participants

One major strategy employed by key players in the North America Termite Control Market is product innovation and the development of eco-friendly solutions. Companies are increasingly focusing on introducing bio-based and low-chemical formulations to align with environmental regulations and consumer preferences for sustainable pest management.

Another key approach is strategic acquisitions and partnerships. Leading firms are acquiring regional pest control businesses or forming alliances with technology providers to expand their service reach and integrate smart monitoring systems into their offerings, enhancing service efficiency and customer retention.

The digital transformation and customer engagement initiatives are being prioritized. Market participants are leveraging mobile applications, online scheduling platforms, and AI-driven diagnostics to improve customer experience, streamline operations, and ensure timely termite inspections and interventions.

RECENT MARKET NEWS

- In March 2024, Orkin launched a new digital platform allowing customers to schedule termite inspections, track service history, and receive real-time alerts regarding termite activity. This initiative aimed at improving customer engagement and reinforcing Orkin’s dominance in digital-enabled pest control services.

- In February 2024, Terminix expanded its service footprint by entering into a partnership with a regional pest control provider in the Pacific Northwest. This collaboration enabled Terminix to strengthen its presence in underpenetrated markets while enhancing its ability to deliver customized termite management solutions.

- In January 2024, BASF introduced a next-generation termite bait formulation designed for improved colony elimination efficiency. The product was developed in response to increasing demand for sustainable yet effective termite control options and supported pest control professionals in delivering superior outcomes.

- In December 2023, a leading independent pest control firm acquired a tech startup specializing in AI-powered termite detection software. This move allowed the firm to integrate predictive analytics into its service offerings, enabling early infestation identification and proactive intervention.

- In November 2023, a prominent termite control service provider launched a nationwide awareness campaign focused on educating homeowners about the risks of undetected termite infestations and the benefits of preventive treatment plans.

MARKET SEGMENTATION

This research report on the North American termite control Market is segmented and sub-segmented into categories.

By Species Type

- Dry wood termites

- Damp wood termites

- Other

By Control Method

- Chemical control methods

- Physical and mechanical control methods

- Biological control methods

- Botanicals

- Other Control Methods

By Application

- Commercial and industrial

- Residential

- Agriculture

- Livestock farms

- Other applications

By Country

- U.S.A

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

Why is the termite control market significant in North America?

The termite control market in North America is crucial due to the high prevalence of subterranean termites, especially in warm and humid regions like the southeastern United States. Termites cause billions of dollars in property damage annually, often not covered by standard homeowners' insurance, which makes preventive and corrective treatments essential for both residential and commercial structures.

How is consumer awareness impacting the termite control industry in North America?

Consumer awareness about the hidden dangers of termite infestations — including structural compromise and long-term financial loss — is increasing. Home inspections during real estate transactions have become standard practice, prompting more homeowners to invest in regular termite inspections and ongoing protection plans offered by pest control companies.

Which regions in North America see the highest demand for termite control services?

The southern and southeastern U.S., including states like Texas, Florida, Georgia, and Louisiana, experience the highest termite activity and therefore the greatest demand for control services. However, northern states are also seeing rising needs due to climate change extending active termite seasons further north.

Are there regulatory standards governing termite control products and services in North America?

Yes, in the U.S., the Environmental Protection Agency (EPA) regulates the registration and use of termiticides under the Federal Insecticide, Fungicide, and Rodenticide Act (FIFRA). Additionally, individual states have their own licensing requirements for pest control applicators and businesses. In Canada, Health Canada’s Pest Management Regulatory Agency (PMRA) oversees pesticide use and safety protocols.

Is there a shift toward green or natural termite control methods in North America?

Yes, there’s a noticeable trend among environmentally conscious consumers and commercial clients seeking greener alternatives. Products such as botanical extracts, nematodes (natural predators), and low-impact bait systems are gaining traction, especially in residential markets across California, Oregon, and British Columbia.

How important is the role of pest control professionals in managing termite infestations?

Pest control professionals play a vital role in early detection, accurate diagnosis, and effective treatment of termite problems. Their expertise ensures safe application of chemicals, proper installation of baiting systems, and long-term monitoring, which can prevent costly repairs and protect property value over time.

How does climate change affect termite activity and control efforts in North America?

Climate change is extending the geographic range and active season of termites. Warmer winters allow colonies to survive longer, while increased humidity and rainfall in some regions create ideal conditions for termite proliferation. This has led to a rise in infestations in areas previously considered low-risk, such as parts of the Pacific Northwest and southern Canada, prompting pest control companies to adapt their strategies accordingly.

What role do real estate transactions play in driving the termite control market?

Termite inspections have become a standard part of real estate transactions in many U.S. states and Canadian provinces. Buyers often require proof of termite-free status or ongoing protection plans before closing deals. This demand has created a steady stream of business for pest control providers, especially those offering certified inspection reports and long-term warranties.

Are homeowners increasingly opting for long-term termite protection plans instead of one-time treatments?

Yes, there's a growing preference among homeowners for ongoing protection plans that include regular inspections, monitoring, and maintenance. These plans offer peace of mind and financial protection against future infestations, which can be far more costly than preventive care. Many pest control companies now bundle these services with digital tracking and customer alerts for added convenience.

How are termite control companies adapting to the trend of smart home technology?

Termite control firms are integrating smart technology into their service offerings by using IoT-enabled monitoring stations, mobile apps for customer communication, and automated alert systems that notify homeowners and technicians about potential termite activity. This shift enhances responsiveness, improves customer satisfaction, and allows for more data-driven decision-making in managing infestations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com