Neotame Market Size, Share, Trends & Growth Forecast Report – Segmented By Application (Pharmaceuticals, Food and Beverage, Cosmetics, Agriculture/Feed and Others), Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2025 to 2033)

Global Neotame Market Size

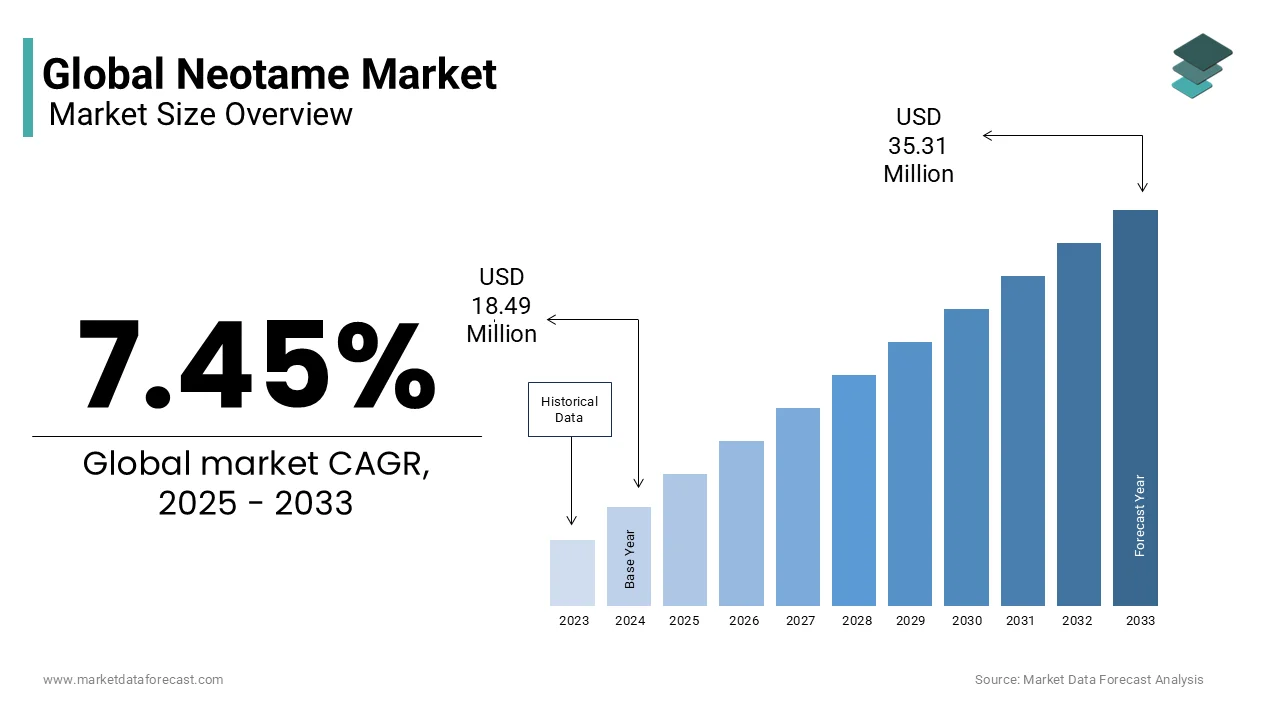

The global neotame market size was valued at USD 18.49 million in 2024, and the market size is expected to reach USD 35.31 million by 2033 from USD 19.87 million in 2025. The market's promising CAGR for the predicted period is 7.45%.

Neotame is a high-intensity artificial sweetener derived from aspartame but with significantly greater sweetness potency—approximately 7,000 to 13,000 times sweeter than sucrose. Developed by NutraSweet and later acquired by Nexira, neotame functions effectively in a broad range of food and beverage formulations, including baked goods, dairy products, chewing gum, and carbonated beverages, due to its thermal stability and prolonged shelf-life performance. Unlike other sweeteners, neotame does not contribute to dental caries and is metabolized differently, rendering it suitable for individuals managing phenylketonuria (PKU), as it does not yield phenylalanine in significant amounts upon breakdown. Regulatory approvals have been secured from major health authorities, including the U.S. Food and Drug Administration (FDA), the European Food Safety Authority (EFSA), and Japan’s Ministry of Health, Labour and Welfare. The integration of neotame into clean-label initiatives, despite its synthetic origin, is facilitated by its minimal usage levels, which allow manufacturers to list it under broader categories such as “artificial flavor” or “flavor enhancer,” thus maintaining consumer-perceived label simplicity.

MARKET DRIVERS

MARKET DRIVERS

Rising Prevalence of Metabolic Disorders Driving Neotame Adoption

The escalating incidence of metabolic syndromes, particularly type 2 diabetes and obesity stands as a pivotal force behind the increased demand for neotame across food and pharmaceutical sectors. According to the International Diabetes Federation, approximately 537 million adults worldwide were living with diabetes in 2021, a figure projected to rise to 643 million by 2030, with over half of these cases concentrated in the Asia-Pacific region. This surge necessitates dietary interventions that reduce caloric intake without compromising taste, positioning neotame as an ideal alternative to sugar. With a negligible impact on blood glucose levels and no contribution to insulin spikes, neotame supports glycemic control. The Global Burden of Disease Study published by the Institute for Health Metrics and Evaluation reveals that excess sugar consumption contributes to over 184,000 deaths annually, primarily due to cardiovascular complications and diabetes. In response, governments across India, China, and Thailand have implemented sugar taxation policies—Food manufacturers are reformulating products using neotame to comply with these regulations while retaining palatability.

Expansion of Functional Foods and Beverages Market Fueling Neotame Utilization

The burgeoning functional foods and beverages sector, characterized by products designed to deliver health benefits beyond basic nutrition, is significantly amplifying the demand for advanced sweetening agents like neotame. Consumers are increasingly prioritizing products that support weight management, oral health, and metabolic wellness, creating fertile ground for innovation in sugar-free formulations.

Neotame’s compatibility with high-temperature processing makes it especially valuable in fortified baked goods and nutritional bars, segments experiencing rapid expansion. Moreover, neotame’s synergistic effect when blended with other sweeteners such as erythritol or stevia allows for improved taste profiles without aftertaste, enhancing consumer acceptance. These developments underscore how the convergence of technological formulation capabilities and evolving consumer expectations is elevating neotame’s strategic importance in next-generation functional product development.

MARKET RESTRAINTS

Stringent Regulatory Hurdles Limiting Neotame Penetration in Emerging Economies

Neotame faces substantial regulatory barriers in several emerging economies, significantly impeding its widespread adoption. Unlike established sweeteners such as sucralose or aspartame, neotame remains unapproved or subject to prolonged evaluation processes in countries including Indonesia, Vietnam, and Nigeria. As per the ASEAN Food Handbook, only six out of ten member states have officially authorized neotame for use in food products, creating fragmented market access across Southeast Asia. Manufacturers report lead times exceeding several months to secure ingredient clearances for cross-border product launches involving neotame. Additionally, public skepticism toward artificial additives persists, fueled by misinformation and limited scientific literacy. This perception gap complicates marketing efforts and reduces retailer willingness to stock neotame-sweetened items. These inconsistencies increase compliance costs for multinational producers and constrain the scalability of neotame-based innovations in high-growth but regulation-sensitive regions.

High Production Costs and Limited Manufacturing Infrastructure Constraining Supply Chain Efficiency

Its elevated production cost relative to alternative sweeteners, compounded by limited global manufacturing capacity, is a critical restraint affecting the neotame market. Neotame synthesis involves a complex hydrogenation process requiring palladium-catalyzed reactions and stringent purification protocols, making it more expensive than simpler sweeteners like sucralose or acesulfame-K.

This cost disparity discourages small and mid-sized food processors from adopting neotame, particularly in price-sensitive markets such as South Asia and Sub-Saharan Africa. Moreover, global production remains highly concentrated, with only three primary manufacturing facilities located in the United States, France, and China—operated respectively by Heartland Food Products Group, Nexira, and Shandong Qiaochang Chemical.

Additionally, the scarcity of skilled labor trained in high-purity organic synthesis further limits new entrants.

MARKET OPPORTUNITIES

Growing Demand for Clean-Label Sugar Replacements in Plant-Based Products

The rapid ascent of plant-based and vegan food products presents a compelling opportunity for neotame integration, particularly in applications where natural sweeteners fall short in functionality. While stevia and monk fruit extracts dominate the "natural" sweetener narrative, they often exhibit bitterness and poor heat stability, limiting their utility in extruded snacks, dairy alternatives, and baked vegan goods. Neotame, though synthetic, is used at such minute concentrations—typically between 5 to 30 mg/kg—that it can be declared under generic labeling terms in certain jurisdictions, aligning with clean-label trends. Furthermore, neotame’s ability to enhance fruit flavors allows for reduced fruit concentrate usage, lowering both cost and microbiological risk in shelf-stable products. This functional versatility positions neotame as a silent enabler in the next wave of plant-forward innovation.

Increasing R&D Investment in Taste Modulation Technologies

Advancements in taste science and molecular flavor design are unlocking novel applications for neotame beyond simple sugar replacement, transforming it into a multifunctional ingredient in sensory optimization. Modern food technology firms are leveraging neotame not merely as a sweetener but as a flavor modulator capable of suppressing bitterness and enhancing mouthfeel in complex matrices. Firmenich and Givaudan, global leaders in flavor innovation, have integrated neotame into proprietary taste-enhancing systems aimed at improving the palatability of protein-fortified beverages and medicinal syrups. Additionally, biotech startups such as Shiru and TasteTech are incorporating neotame into AI-driven flavor prediction models to design optimized sweetening blends for specific consumer demographics. These developments indicate that neotame is transitioning from a commodity additive to a precision tool in the emerging field of digital gastronomy and personalized nutrition.

MARKET CHALLENGES

Consumer Skepticism Toward Artificial Sweeteners Despite Scientific Validation

Entrenched consumer resistance to artificial ingredients, even in the face of rigorous safety assessments, is one of the most persistent challenges confronting the neotame market. Although neotame has been affirmed as safe by the FDA, EFSA, and Joint FAO/WHO Expert Committee on Food Additives (JECFA), public distrust endures, largely influenced by social media narratives and misinterpretations of scientific studies. This sentiment is amplified by advocacy groups promoting "chemical-free" diets, despite the lack of evidence linking neotame to adverse effects at approved usage levels. Marketing campaigns emphasizing "no artificial sweeteners" now dominate supermarket shelves, marginalizing effective but misunderstood compounds like neotame. Even when clinical trials confirm safety public perception lags. Educational deficits exacerbate the issue. Until transparent science communication bridges this cognitive gap, neotame will struggle to gain equitable consumer consideration alongside so-called "natural" alternatives.

Supply Chain Vulnerabilities Due to Geopolitical and Environmental Factors

The neotame supply chain is increasingly exposed to geopolitical instability and environmental disruptions, threatening consistent global availability. Primary manufacturing hubs are located in regions susceptible to trade tensions, energy volatility, and climate-related events. For instance, the U.S.-China trade conflict has led to fluctuating tariffs on key intermediates such as methyl esters and hydrogenation catalysts, raising input costs since 2021. Additionally, the Rhône Valley facility in France, responsible for nearly a quarter of European supply, faced operational interruptions during the 2022 drought, when water restrictions limited cooling capacity essential for exothermic reactions. Furthermore, reliance on rare metal catalysts like palladium introduces additional risk. Climate change is also altering agricultural patterns for precursor materials: phenylalanine, a base compound for neotame synthesis, is primarily produced via microbial fermentation using corn-derived glucose. These interdependencies illustrate how neotame’s production resilience is contingent on broader macroeconomic and ecological stability, making it vulnerable to cascading systemic shocks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.48% |

| Segments Covered | By Application, and Region. |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Jk sucralose Inc., Foodchem International Corporation, A & Z Food Additives Co., Ltd., Sweetener India., Shaoxing Marina Biotechnology Co., Ltd., H & A Canada Inc., JJD Enterprises, Prinova Group LLC, Sweetner Holdings, Inc., Fooding Group Limited, and among others. |

SEGMENTAL ANALYSIS

By Application Insights

The food and beverage sector commanded the largest share of the global neotame market of 65.2% of total consumption in 2024. The dominance of this segment is anchored in the escalating demand for low-calorie, sugar-free food products amid rising health consciousness and regulatory pressure to reduce added sugars. An additional key driver propelling this segment is the rapid reformulation of carbonated soft drinks and dairy-based beverages to meet evolving nutritional standards. Additionally, the baked goods industry has increasingly adopted neotame due to its thermal stability—retaining sweetness even at temperatures exceeding 200°C. With governments from Thailand to Canada implementing tiered sugar taxes, the economic incentive for large-scale substitution continues to grow, solidifying food and beverage as the cornerstone of neotame application.

The pharmaceuticals segment is emerging as the fastest-growing application area for neotame and is projected to expand at a CAGR of 9.4% between 2025 and 2033. The accelerated adoption of this segment is due to the increasing integration of neotame into pediatric and geriatric formulations where palatability directly influences treatment adherence. A further pivotal driver is the need to mask bitterness in liquid medications without adding calories or affecting glycemic control—critical for diabetic patients. Another transformative factor is neotame’s compatibility with active pharmaceutical ingredients (APIs) and its stability across pH ranges, enabling extended shelf life. The U.S. Pharmacopeia has included neotame in its excipient compendium, facilitating broader regulatory acceptance. Neotame’s potency allows usage at microgram levels, minimizing formulation interference—an advantage unmatched by bulk sweeteners like sorbitol or xylitol.

REGIONAL ANALYSIS

North America

North America held a commanding position in the global neotame market by securing an estimated 34.5% share in 2024. The region's lead position is rooted in advanced food science infrastructure, robust regulatory clarity, and high consumer receptivity to functional foods. The United States, in particular, serves as both a major production hub and a center for innovation in sweetener applications. Neotame was first approved by the FDA in 2002, and since then, it has been integrated into over 4,500 commercial food and pharmaceutical products, according to the GRAS Notice Inventory. The prevalence of obesity has intensified demand for zero-calorie alternatives, with retail giants like Kroger and Walmart expanding their private-label sugar-free product lines. Moreover, the rise of personalized nutrition platforms such as Habit and Nutrisense has increased demand for precise sweetening solutions, where neotame’s dose efficiency offers formulation flexibility. Canada complements this ecosystem with stringent yet supportive regulatory frameworks. These converging factors—scientific maturity, policy alignment, and consumer behavior—cement North America’s role as the epicenter of neotame innovation and consumption.

Europe

Europe maintained a mature and highly regulated presence in the neotame landscape. While growth is moderate compared to Asia-Pacific, the region exhibits strong penetration in premium food categories and pharmaceutical development. France and Germany lead in industrial utilization, with French-based Nexira playing a critical role in refining and distributing neotame across EU member states. A key driver is the European Commission’s Farm to Fork Strategy, which aims to reduce sugar consumption by 30% by 2030; this policy impetus has led companies like Danone and Nestlé to reformulate yogurts and plant-based drinks using neotame blends. Additionally, the pharmaceutical sector in Belgium and Switzerland uses neotame in sublingual tablets and chewable antacids due to its rapid dissolution and lack of metabolic impact. Despite this, stringent labeling laws and scientific transparency have created a balanced environment where neotame thrives in niche, high-value applications rather than volume-driven segments.

Asia Pacific

Asia Pacific is rapidly ascending as the most dynamic region in the neotame market. China stands at the forefront, hosting one of only three dedicated neotame synthesis plants worldwide—operated by Shandong Qiaochang Chemical—which supplies not only domestic needs but also exports to Southeast Asia and the Middle East. Domestic demand is fueled by aggressive government action against metabolic diseases Meanwhile, Japan’s aging population has amplified demand for easy-to-swallow, palatable medicines. India, though still in early adoption phase, is witnessing a surge in nutraceutical startups utilizing neotame in protein bars and diabetic-friendly sweets. Coupled with improving regulatory clarity and rising urbanization, Asia Pacific’s confluence of demographic pressure, industrial capacity, and innovation intent positions it as the future growth engine of the neotame economy.

Latin America

Latin America displays uneven but promising progress in neotame adoption, with Brazil and Mexico serving as primary catalysts. The region’s significance lies not in current volume but in its transformative potential driven by public health crises linked to excessive sugar consumption. Brazil leads in regulatory modernization, including baked goods and flavored milks. The country’s sugary drink consumption annually is one of the highest in the world which is prompting multinational bottlers like Ambev to reformulate popular brands such as Guaraná Antarctica using neotame-sucralose systems. This regulatory shock has incentivized companies like Grupo Bimbo to introduce neotame-sweetened breads targeting school nutrition programs. Nevertheless, challenges remain: fragmented distribution networks and limited local manufacturing mean reliance on imported raw materials, increasing costs. Yet, with regional R&D initiatives gaining momentum, Latin America is gradually building the foundation for sustained neotame integration.

Middle East and Africa

The Middle East and Africa collectively represent a nascent but strategically evolving segment. Within this, the Gulf Cooperation Council (GCC) countries dominate uptake, particularly the UAE and Saudi Arabia, where urban affluence and healthcare modernization are reshaping dietary preferences. Majid Al Futtaim’s “MyCare” private label now includes neotame-sweetened herbal teas and wellness shots. In South Africa, although regulatory approval lags, private healthcare providers are experimenting with neotame in medical nutrition for HIV and TB patients who require calorie-dense yet palatable supplements. Nonetheless, with increasing foreign investment in food processing zones in Egypt and Kenya, and growing awareness of metabolic disease risks, the region is poised for incremental but meaningful expansion in neotame utilization.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key players in the Global Neotame Market include Jk sucralose Inc., Foodchem International Corporation, A & Z Food Additives Co., Ltd., Sweetener India., Shaoxing Marina Biotechnology Co., Ltd., H & A Canada Inc., JJD Enterprises, Prinova Group LLC, Sweetner Holdings, Inc., Fooding Group Limited, and among others.

The competitive environment in the neotame market is characterized by technological differentiation, niche specialization, and controlled supply dynamics. With only a handful of entities possessing the expertise and infrastructure to produce neotame at scale, the market remains concentrated, allowing major players to maintain influence over pricing and innovation trajectories. Rather than engaging in price wars, competitors focus on value-added services such as formulation support, regulatory guidance, and sensory optimization. Geographic reach and compliance with diverse food safety standards serve as key differentiators, especially in regions with evolving approval frameworks. Some firms emphasize integration with natural ingredients to overcome consumer bias against artificial compounds, while others leverage proprietary delivery technologies to enhance functionality. The absence of mass-market branding means competition unfolds behind the scenes, primarily within R&D departments and regulatory affairs units of food and pharma giants. Smaller chemical producers face barriers due to the complexity of synthesis and stringent purity requirements, limiting new entrants. As demand grows for precision sweetness in health-focused products, the rivalry is shifting toward intellectual property, application patents, and strategic alliances rather than volume-based dominance.

TOP PLAYERS IN THE MARKET

NutraSweet Company

NutraSweet Company stands as a pioneering force in the neotame landscape, originally developing the sweetener through advanced peptide modification technology. As the first entity to commercialize neotame, the company laid the foundational science that enabled its use across food, pharmaceutical, and beverage applications. Though ownership has transitioned over time, NutraSweet’s legacy persists in the compound’s regulatory acceptance and technical specifications. The company continues to influence formulation standards and supports global partners in optimizing taste profiles using neotame, maintaining its reputation as an innovator in high-intensity sweetening solutions.

Heartland Food Products Group

Heartland Food Products Group emerged as a dominant manufacturer and distributor following its acquisition of the NutraSweet brand. With integrated production capabilities and a strong focus on research-driven applications, Heartland has expanded neotame’s reach into emerging markets and novel product categories. The company actively collaborates with food technologists and regulatory bodies to promote safe and effective usage, reinforcing its position as a central supplier in the global supply chain. Its commitment to quality control and sustainable manufacturing practices further strengthens trust among industrial clients.

Nexira

Nexira, a French-based natural ingredients specialist, plays a unique role by blending neotame with plant-derived excipients to create clean-label compatible formulations. While not a primary synthesizer, Nexira enhances neotame’s marketability by addressing consumer demand for transparency and functional performance. The company focuses on hybrid solutions that combine synthetic potency with natural perception, particularly in pharmaceuticals and premium confectionery. Its expertise in encapsulation and flavor modulation allows for tailored delivery systems, positioning Nexira as a strategic enabler in next-generation product development.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

One of the most impactful strategies employed by leading players is strategic collaboration with food and pharmaceutical formulators to co-develop customized sweetening systems. By working directly with end-product manufacturers, companies ensure that neotame integrates seamlessly into complex matrices such as protein bars, oral suspensions, and baked goods, enhancing sensory appeal while meeting regulatory and labeling requirements. These partnerships foster innovation and deepen customer loyalty.

Another critical approach involves expanding application portfolios beyond traditional sugar replacement. Companies are increasingly positioning neotame as a multifunctional ingredient capable of improving mouthfeel, masking bitterness, and enhancing fruit flavors. This shift from commodity additive to performance enhancer elevates its value proposition in premium and medical-grade products.

A third key strategy is advancing sustainability and transparency in production. Firms are investing in cleaner synthesis methods, reduced solvent usage, and greener catalytic processes to align with corporate ESG goals. Additionally, efforts to improve traceability and communicate safety data help counter consumer skepticism and strengthen brand credibility in competitive ingredient markets.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, Heartland Food Products Group launched a dedicated innovation center in Illinois focused on high-intensity sweetener applications, aiming to accelerate product development for global clients in the food and pharmaceutical sectors.

- In July 2023, Nexira introduced a new line of hybrid sweetening blends combining neotame with acacia fiber and botanical extracts, targeting clean-label trends in European functional foods and dietary supplements.

- In November 2023, NutraSweet Company partnered with a leading Indian nutraceutical manufacturer to co-formulate sugar-free diabetic snacks using neotame, expanding its footprint in South Asia’s growing health food market.

- In February 2024, Heartland Food Products Group upgraded its neotame purification process to reduce environmental impact, incorporating closed-loop solvent recovery systems to align with global sustainability benchmarks.

- In May 2024, Nexira acquired a specialty encapsulation firm based in Lyon to enhance controlled-release capabilities for neotame in oral medications and slow-dissolve confectionery products.

MARKET SEGMENTATION

This research report on the global neotame market has been segmented and sub-segmented based on application & region.

By Application

- Pharmaceuticals

- Food and Beverage

- Cosmetics

- Agriculture/Feed

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the neotame market?

The neotame market involves the production and sale of neotame, a high-intensity artificial sweetener used in food and beverages.

2. What drives growth in the neotame market?

Demand for low-calorie, sugar-free products and rising health awareness are key growth drivers.

3. Is neotame safe for consumption?

Yes, neotame is approved by the FDA, EFSA, and other global authorities as safe for human consumption.

4. Which region leads the neotame market?

North America leads due to high demand for diet beverages and low-calorie food products.

5. How is neotame different from aspartame?

Neotame is sweeter, more stable, and safer for people with phenylketonuria (PKU) than aspartame.

6. What challenges does the neotame market face?

Limited awareness and competition from natural sweeteners like stevia and monk fruit are key challenges.

8. Who are the key players in the neotame market?

Major players include The NutraSweet Company, Fooding Group, and Shaoxing Marina Biotechnology.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com