Global Artificial Sweetener Market Size, Share, Trends, & Growth Forecast Report Segmented By Type (Aspartame, Acesulfame-K, Monosodium Glutamate, Saccharin, And Sodium Benzoate), Application (Bakery Items, Dairy Products, Confectionery, Beverages, And Other), Distribution Channel (Supermarkets & Hypermarkets, Departmental Stores, Convenience Stores, And Others), And Region (North America, Europe, APAC, Latin America, Middle East And Africa) – Industry Analysis From 2026 To 2034

Global Artificial Sweetener Market Size

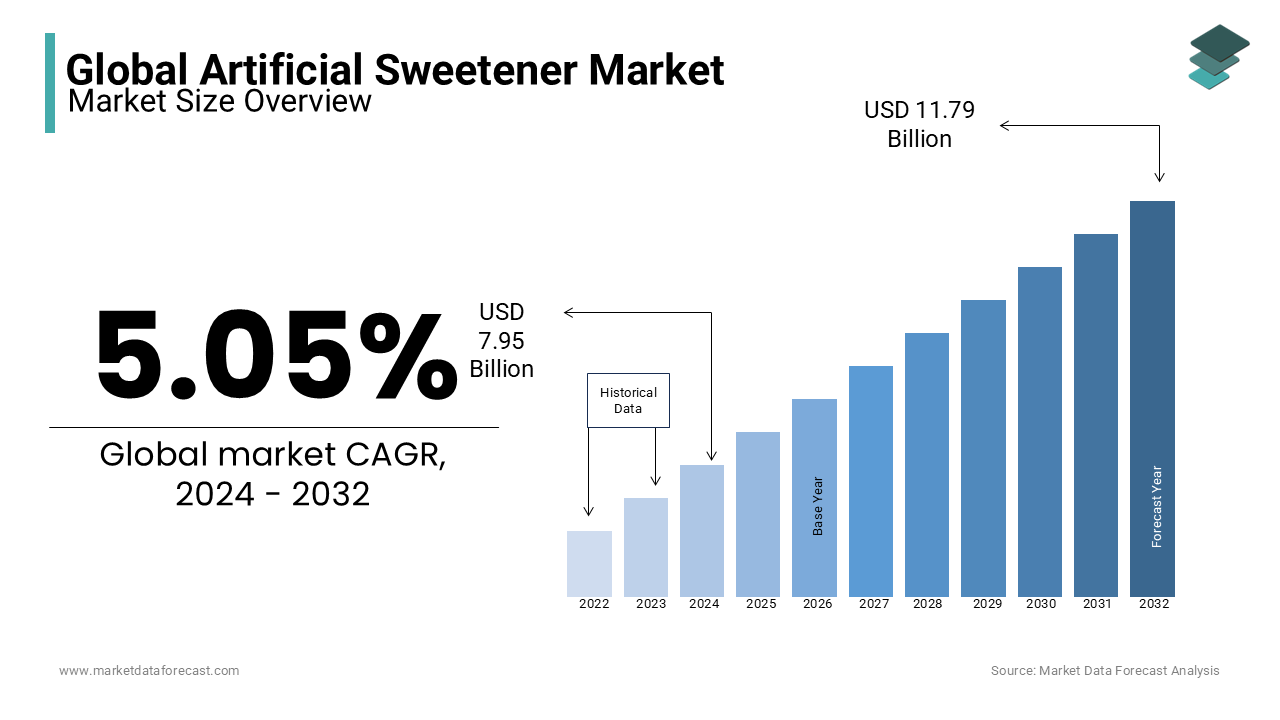

The global artificial sweetener market size was worth USD 8.35 billion in 2025 and is predicted to be worth USD 8.77 billion in 2026 to USD 13.01 billion by 2034, growing at a CAGR of 5.05% during the forecast period.

Artificial sweetener is a high-intensity sweetening agents that provide a sugary taste with minimal or zero caloric content. These synthetic and natural non-nutritive substances include aspartame, sucralose, saccharin, acesulfame potassium (Acesulfame-K), and stevia derivatives. They are extensively utilized in the food and beverage industry to reduce sugar content while maintaining palatability, catering to a growing demographic of health-conscious consumers. The market is driven by the urgent need to combat lifestyle diseases associated with excessive sugar consumption. According to the World Health Organization, global obesity has nearly tripled since 1975, with over 650 million adults classified as obese, creating a critical public health imperative for reduced-calorie alternatives. Furthermore, as per the International Diabetes Federation, approximately 537 million adults are living with diabetes worldwide, a number projected to rise to 643 million by 2030. This escalating prevalence of metabolic disorders necessitates dietary interventions, positioning artificial sweeteners as essential components in therapeutic and preventive nutrition. In Europe, the European Food Safety Authority rigorously evaluates these additives, ensuring their safety for human consumption while enabling manufacturers to reformulate products. The shift towards low-glycemic-index diets has further entrenched these sweeteners in daily consumption patterns, from soft drinks to pharmaceutical syrups. The regulatory landscape continues to evolve, balancing safety concerns with the undeniable demand for sugar reduction strategies in modern food systems.

MARKET DRIVERS

Rising Prevalence of Diabetes and Obesity Globally

The rising global burden of diabetes and obesity is majorly fuelling the widespread adoption of artificial sweeteners and is one of the key drivers of the global market. Governments and health organizations are actively promoting sugar reduction initiatives to mitigate the economic and social costs associated with these chronic conditions. According to the Centers for Disease Control and Prevention, more than 37 million people in the United States have diabetes, representing about 11% of the population, with 90% to 95% having type 2 diabetes. This significant health crisis drives individuals to seek dietary alternatives that allow them to manage blood glucose levels without sacrificing sweetness. As per the World Obesity Federation, global obesity is predicted to affect 1 billion people worldwide by 2030, highlighting the urgency for early dietary intervention. Artificial sweeteners enable the production of low-calorie beverages and foods that align with medical recommendations for weight management and glycemic control. The integration of these sweeteners into everyday products allows consumers to adhere to restrictive diets more sustainably. Healthcare providers frequently recommend replacing sugar with non-nutritive sweeteners as part of comprehensive lifestyle modification programs. This medical endorsement reinforces consumer confidence and drives consistent demand across various food categories. The direct correlation between public health crises and the search for viable sugar substitutes ensures that the artificial sweetener market remains robust and expanding in response to demographic health trends.

Stringent Government Regulations on Sugar Content in Food Products

Governments worldwide are implementing stringent regulations and fiscal policies to curb sugar consumption, which is further boosting the expansion of the global artificial sweetener market. Sugar taxes and mandatory labeling requirements have compelled companies to reformulate their products using artificial sweeteners to maintain taste profiles while complying with legal standards. According to the Organisation for Economic Co-operation and Development, over 50 countries have implemented taxes on sugar-sweetened beverages, aiming to reduce consumption and generate revenue for health programs. These fiscal measures have proven effective, with studies showing a significant decline in the sales of high-sugar drinks in taxed jurisdictions. As per Public Health England, the Soft Drinks Industry Levy led to a 50% reduction in the amount of sugar per liter in soft drinks within two years of its introduction, primarily through reformulation. Manufacturers increasingly turn to high-intensity sweeteners such as sucralose and aspartame to achieve the desired sweetness without incurring tax liabilities or facing negative consumer perception associated with high sugar content. Additionally, front-of-pack warning labels in countries like Chile and Mexico have heightened consumer awareness, driving demand for healthier alternatives. The regulatory pressure creates a favorable environment for artificial sweetener producers, as food companies seek compliant ingredients to avoid penalties and maintain market share. This legislative landscape acts as a powerful structural driver for the artificial sweetener industry.

MARKET RESTRAINTS

Growing Consumer Preference for Natural and Organic Ingredients

The shifting consumer preference towards natural and organic ingredients due to skepticism regarding synthetic additives is primarily impeding the expansion of the global market. Many consumers perceive artificial sweeteners as unnatural and potentially harmful, leading them to favor plant-based alternatives such as stevia, monk fruit, and erythritol. According to the International Food Information Council, 60% of consumers are trying to limit or avoid sugars, but a growing subset specifically seeks out natural sources rather than synthetic compounds. This trend is particularly pronounced among millennials and Gen Z shoppers who prioritize clean-label products. As per a NielsenIQ Global Health and Wellness Survey, sales of products with natural claims have outpaced those with artificial ingredients, reflecting a broader distrust of processed food additives. The term "artificial" often carries negative connotations related to chemical processing and long-term health risks, despite scientific evidence supporting the safety of approved sweeteners. This perception gap limits the growth potential of traditional synthetic sweeteners like aspartame and saccharin. Manufacturers are responding by blending synthetic sweeteners with natural ones or transitioning entirely to natural portfolios, which marginalizes pure artificial options. The demand for transparency and simplicity in ingredient lists challenges the dominance of established artificial sweeteners, forcing companies to innovate or risk losing market relevance to natural competitors.

Health Concerns and Negative Perception Regarding Safety

Persistent health concerns and negative media coverage regarding the safety of artificial sweeteners are further hindering the global market growth. Despite regulatory approvals, ongoing debates about potential links to cancer, metabolic disruption, and gut microbiome alterations create consumer hesitation. According to a study published in the British Medical Journal, high consumption of artificial sweeteners was associated with an increased risk of cardiovascular events, sparking renewed scrutiny and public concern. Although causality remains debated, such findings influence consumer behavior and purchasing decisions. As per the European Food Safety Authority, while current data support the safety of approved sweeteners within acceptable daily intake levels, public perception often lags behind scientific consensus. Social media amplifies anecdotal reports and controversial studies, fostering a climate of uncertainty. Some consumers report headaches, digestive issues, or other adverse reactions, further deterring usage. The controversy surrounding specific sweeteners, such as aspartame, has led to voluntary removal from certain product lines by major brands seeking to avoid reputational damage. This volatile trust environment restricts the expansion of artificial sweeteners in premium and health-focused segments. Manufacturers must invest heavily in consumer education and rigorous safety testing to counteract these perceptions, yet the lingering doubt continues to suppress demand among health-conscious demographics who prefer to avoid potential risks altogether.

MARKET OPPORTUNITIES

Expansion in Pharmaceutical and Personal Care Applications

The pharmaceutical and personal care industries offer lucrative opportunities for the artificial sweetener market due to the rising need for palatable medication and cosmetic formulations. Artificial sweeteners are essential in masking the bitter taste of active pharmaceutical ingredients in syrups, chewable tablets, and lozenges, improving patient compliance, particularly among children and the elderly. According to the World Health Organization, the global prevalence of chronic diseases requiring long-term medication is rising, increasing the demand for patient-friendly drug delivery systems. As per the United States Pharmacopeia, sweetening agents like sucralose and saccharin are widely used in oral care products such as toothpaste and mouthwash because they do not contribute to tooth decay. This non-cariogenic property is a significant advantage over sugar, aligning with dental health recommendations. The growing aging population, which often requires multiple medications daily, further boosts the demand for flavored pharmaceutical preparations. Additionally, the personal care sector utilizes these sweeteners in lip balms and oral hygiene products to enhance sensory appeal without compromising product stability. The expansion of telemedicine and home healthcare services also drives the need for easy-to-administer and pleasant-tasting medications. By diversifying into these specialized applications, artificial sweetener manufacturers can reduce dependency on the volatile food and beverage sector and tap into stable, high-value markets with stringent quality requirements.

Innovation in Blended Sweetener Formulations

Innovation in blended sweetener formulations offers significant opportunities for the expansion of the global artificial sweetener market. By combining different sweeteners, manufacturers can achieve a synergistic effect that mimics the taste profile of sugar more closely while minimizing undesirable side effects. According to the Institute of Food Technologists, blending aspartame with acesulfame potassium or sucralose with stevia can enhance sweetness potency and improve temporal profile, resulting in a more satisfying consumer experience. As per recent patent filings in the food technology sector, there is a surge in proprietary blends designed to mask metallic or bitter notes associated with high-intensity sweeteners. These customized formulations allow food and beverage companies to reduce overall sweetener usage while maintaining sweetness intensity, offering cost efficiencies. The ability to tailor sweetness profiles for specific applications, such as baked goods or acidic beverages, expands the utility of artificial sweeteners in diverse product categories. Furthermore, blended solutions can improve stability under heat and pH variations, addressing technical challenges in processing. This technological advancement enables manufacturers to meet the dual demands of sugar reduction and taste quality, appealing to discerning consumers. The development of next-generation blends represents a key area for differentiation and growth, allowing companies to offer superior sensory experiences that drive product adoption and loyalty.

MARKET CHALLENGES

Regulatory Uncertainty and Varying Global Standards

Navigating the complex and often inconsistent regulatory landscape for artificial sweeteners poses a significant challenge for global manufacturers. Approval status, acceptable daily intake levels, and labeling requirements vary significantly across regions, complicating international trade and product formulation. According to the Codex Alimentarius, while international standards exist, individual countries often implement stricter or divergent regulations based on local risk assessments and political pressures. For instance, while aspartame is approved in the United States and Europe, it faces restrictions or bans in certain other jurisdictions, limiting market access. As per the European Commission, recent re-evaluations of sweetener safety have led to updated labeling requirements and reduced acceptable daily intake levels for some additives, forcing manufacturers to reformulate products. This regulatory fragmentation increases compliance costs and creates uncertainty for long-term investment planning. Companies must maintain multiple product versions to meet different regional standards, reducing economies of scale. Furthermore, sudden regulatory changes, such as the reclassification of certain sweeteners by health agencies, can disrupt supply chains and damage brand reputation. The lack of harmonization hinders the seamless global distribution of products containing artificial sweeteners. Manufacturers must invest heavily in regulatory affairs and legal expertise to navigate this fragmented landscape, yet the risk of unexpected regulatory shifts remains a persistent challenge that impedes market stability and growth.

Intense Competition from Natural Non-Nutritive Sweeteners

The artificial sweetener market faces intense competition from natural non-nutritive sweeteners, which are gaining rapid traction due to their clean-label appeal. Stevia, monk fruit, and allulose are increasingly preferred by consumers and manufacturers alike, eroding the market share of traditional synthetic sweeteners. According to the Mintel Global New Products Database, launches featuring stevia and monk fruit have grown significantly faster than those with aspartame or sucralose in recent years, reflecting a clear market shift. As per the American Botanical Council, the cultivation and processing of stevia have become more efficient, reducing costs and making it a viable competitor in price-sensitive segments. Natural sweeteners benefit from a positive health halo, allowing brands to market products as natural and wholesome, a claim artificial sweeteners cannot make. This competitive pressure forces artificial sweetener producers to lower prices or invest in marketing to defend their position. Additionally, many large food corporations are publicly committing to removing artificial ingredients from their portfolios, further marginalizing synthetic options. The innovation pipeline for natural sweeteners is robust, with new extraction technologies improving taste and functionality. This dynamic competitive environment challenges the long-term viability of pure artificial sweeteners, requiring strategic pivots towards natural blends or niche applications where synthetic options retain technical advantages.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.05% |

| Segments Covered | By Type, Application, Distribution Channel, & Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Zydus Wellness Ltd., Sunwin Stevia International, Inc., PureCircle, MORITA KAGAKU KOGYO CO., LTD, Hermes Sweeteners Ltd., NutraSweet Property Holdings, Inc., McNeil Nutritionals, JK Sucralose, Ajinomoto Co., Inc., and Roquette |

SEGMENTAL ANALYSIS

By Type Insights

The aspartame segment dominated the market by holding the highest share of the global market in 2025. The dominance of the aspartame segment in the global market is attributed to its widespread acceptance, cost-effectiveness, and extensive regulatory approval history across major global markets. According to the European Food Safety Authority, aspartame is one of the most extensively studied food additives, with rigorous safety assessments confirming its suitability for human consumption within established acceptable daily intake levels. This scientific validation has fostered trust among large-scale food and beverage producers who require reliable and consistent ingredients for mass production. As per the United States Food and Drug Administration, aspartame remains approved for use in a wide variety of products, including soft drinks, desserts, and chewing gum, ensuring its continued presence in supply chains. The economic advantage of aspartame is significant, as it is approximately 200 times sweeter than sugar, allowing manufacturers to achieve desired sweetness levels with minimal quantity. This efficiency reduces formulation costs and simplifies logistics. Furthermore, the established infrastructure for aspartame production supports stable pricing and availability, which is critical for high-volume applications. The integration of aspartame into iconic low-calorie brands has created strong brand loyalty and consumer familiarity, reinforcing its market leadership despite the emergence of newer alternatives.

On the other side, the acesulfame potassium segment is projected to be the fastest-growing segment in the artificial sweetener market and is anticipated to showcase a CAGR of 6.4% during the forecast period, owing to its exceptional stability under heat and varying pH levels, making it ideal for baked goods and processed foods that undergo thermal processing. According to the Joint FAO/WHO Expert Committee on Food Additives, Acesulfame-K is recognized for its safety and synergistic properties when blended with other sweeteners, enhancing overall sweetness perception while masking bitter aftertastes. As per industry data from major flavor houses, the demand for blended sweetener systems has increased significantly, with Acesulfame-K being a key component in these formulations due to its ability to improve the temporal profile of sweetness. The growing popularity of ready-to-eat meals and shelf-stable beverages, which require ingredients that maintain integrity over long storage periods, further boosts its adoption. Additionally, Acesulfame-K is not metabolized by the body and is excreted unchanged, appealing to health-conscious consumers seeking zero-calorie options. Its versatility allows it to be used in a broad spectrum of applications, from dairy products to pharmaceuticals. The increasing focus on sugar reduction in emerging markets, where cost-effective and stable sweetening solutions are needed, accelerates the growth of this segment.

By Application Insights

The beverages segment led the market by holding the leading share of the global market in 2025. The growth of the beverages segment in the global market can be credited to the pervasive demand for low-calorie and diet soft drinks. According to the Centers for Disease Control and Prevention, sugary drinks are the largest source of added sugars in the American diet, prompting millions of consumers to switch to diet alternatives. As per the Beverage Marketing Corporation, sales of low-calorie and zero-sugar beverages have consistently outpaced regular soda categories in developed markets, reflecting a structural shift in consumer preferences. Major beverage corporations have reformulated their flagship brands using artificial sweeteners like aspartame and sucralose to retain taste while eliminating calories. The convenience and accessibility of these products in vending machines, restaurants, and retail outlets ensure high visibility and frequent purchase. Furthermore, the introduction of flavored sparkling waters and energy drinks sweetened with artificial agents has expanded the category beyond traditional colas. The ability of artificial sweeteners to provide immediate sweetness without affecting blood glucose levels makes them indispensable in this sector. The entrenched habit of consuming diet beverages among weight-conscious demographics ensures steady and recurring demand, solidifying the beverages segment as the cornerstone of the artificial sweetener industry.

However, the dairy products segment is experiencing the fastest growth in the artificial sweetener market and is predicted to witness a CAGR of 6.6% during the forecast period, owing to the rising popularity of flavored yogurts, ice creams, and milk-based desserts. Consumers are increasingly seeking indulgent yet healthy dairy options that align with weight management goals, creating a lucrative niche for low-sugar formulations. According to the International Dairy Federation, the global yogurt market is expanding, with a significant portion of new product launches featuring reduced-sugar claims achieved through artificial sweeteners. As per the National Yogurt Association, flavored yogurts often contain high amounts of added sugar, prompting manufacturers to replace sucrose with high-intensity sweeteners to maintain palatability while lowering calorie counts. The trend towards protein-rich diets has also boosted the consumption of Greek yogurt and cottage cheese, which are frequently sweetened artificially to enhance taste without compromising nutritional profiles. Additionally, the development of lactose-free and plant-based dairy alternatives often utilizes artificial sweeteners to mask off-flavors and improve sensory appeal. The versatility of sweeteners like sucralose and stevia blends in frozen applications ensures that texture and mouthfeel are preserved. This innovation in dairy formulation, combined with the health-conscious behavior of modern consumers, drives the rapid adoption of artificial sweeteners in this dynamic and evolving segment.

By Distribution Channel Insights

The supermarkets and hypermarkets segment held the largest share of the global market in 2025 due to their extensive product assortments, competitive pricing, and one-stop shopping convenience. These retail formats serve as the primary touchpoint for household grocery purchases, offering a wide range of artificial sweetener products from tabletop packets to bulk ingredients for baking. According to the Food Marketing Institute, supermarkets account for the majority of food and beverage sales in North America and Europe, providing unparalleled reach for sweetener brands. The ability of these large retailers to negotiate favorable terms with suppliers allows them to offer promotional discounts and private-label options that attract price-sensitive consumers. As per NielsenIQ data, the visibility of artificial sweeteners in dedicated diet or health food aisles enhances impulse purchases and brand discovery. The presence of knowledgeable staff and informative signage helps educate consumers about the benefits and usage of different sweetener types. Furthermore, the integration of loyalty programs and digital coupons in supermarket apps encourages repeat purchases and brand loyalty. The reliability of stock and consistent availability ensure that consumers can rely on supermarkets for their regular sweetener needs. These factors collectively sustain the dominance of the supermarket and hypermarket channel, making it the primary conduit for artificial sweetener distribution to end-users.

On the other hand, the online retail segment is estimated to record a CAGR of 8.2% during the forecast period in the global market, owing to the convenience of home delivery and the expanding e-commerce ecosystem. According to the United States Census Bureau, e-commerce sales continue to rise, with health and wellness products seeing significant traction among online shoppers. The ability of online retailers to offer a wider variety of niche and specialized artificial sweetener products, including organic and non-GMO options, appeals to discerning consumers who may not find these items in local stores. As per McKinsey & Company, the personalization capabilities of online platforms, such as subscription services and tailored recommendations, enhance customer retention and frequency of purchase. Additionally, online channels provide detailed product information, customer reviews, and comparison tools that empower consumers to make informed decisions. The direct-to-consumer model allows brands to bypass traditional retail margins and engage directly with their audience, fostering brand loyalty. The integration of seamless payment options and fast shipping services further reduces friction in the purchasing process. These advantages drive the rapid expansion of the online channel, making it a key growth engine for the artificial sweetener market.

REGIONAL ANALYSIS

North America Artificial Sweetener Market Analysis

North America had 36.1% of the global market share in 2025. The supremacy of North America in the global market is primarily driven by high health awareness and a mature food and beverage industry. The United States is the primary contributor, with a significant portion of the population actively managing weight and blood sugar levels through dietary choices. According to the Centers for Disease Control and Prevention, the prevalence of obesity in the US remains high, prompting widespread adoption of low-calorie alternatives. The region benefits from strict regulatory frameworks enforced by the Food and Drug Administration, which ensure the safety and quality of artificial sweeteners, fostering consumer trust. As per the International Food Information Council, American consumers are increasingly reading labels and seeking out reduced-sugar options, driving demand for products containing aspartame, sucralose, and stevia blends. The presence of major sweetener manufacturers and innovative food technology companies in the region supports continuous product development and marketing initiatives. The well-established retail infrastructure, including widespread supermarket chains and robust e-commerce platforms, ensures easy accessibility of artificial sweetener products. Furthermore, the strong culture of convenience food consumption amplifies the need for effective sugar substitutes in processed items. These factors collectively maintain North America’s prominent market position, characterized by high per capita consumption and a willingness to adopt new sweetening technologies.

Europe Artificial Sweetener Market Analysis

Europe represents a significant share of the global market for artificial sweeteners due to the stringent health regulations and a strong emphasis on clean-label products. Countries like Germany, France, and the United Kingdom are key markets, where consumers are highly educated about nutrition and actively seek healthier food options. According to the European Food Safety Authority, rigorous safety assessments and labeling requirements guide the use of artificial sweeteners, ensuring high standards of consumer protection. The European Union’s initiatives to reduce sugar content in processed foods have prompted manufacturers to reformulate products using approved sweeteners. As per Eurostat, the aging population in Europe contributes to higher demand for diabetic-friendly and low-calorie products, supporting market growth. The region is also a hub for innovation in natural and blended sweeteners, appealing to environmentally conscious consumers. The presence of major beverage and confectionery companies drives consistent demand for high-quality sweetening agents. Additionally, the growing trend of veganism and plant-based diets in Europe increases the use of artificial sweeteners in alternative food products. The combination of regulatory support, health consciousness, and industrial innovation ensures that Europe remains a vital and dynamic region in the global artificial sweetener landscape.

Asia Pacific Artificial Sweetener Market Analysis

Asia-Pacific is the leading regional sector by revenue volume and stands out as the fastest-growing region in the global artificial sweetener market. This immense potential is driven by rapid urbanization, rising disposable incomes, and changing dietary habits. Countries such as China, India, and Japan are leading the adoption of artificial sweeteners, heavily influenced by growing health awareness and the rising prevalence of lifestyle diseases. According to the International Diabetes Federation, the Asia-Pacific region has the highest absolute number of adults living with diabetes, creating a substantial market for sugar-free alternatives. In China, the government’s Healthy China 2030 initiative actively promotes reduced sugar consumption, encouraging the widespread use of artificial sweeteners in mass-market food and beverages. As per the Indian Ministry of Health, rising obesity rates in urban areas are driving demand for low-calorie products, particularly among the expanding middle class. The region benefits from a massive population base and expanding retail infrastructure, which improves access to packaged foods containing artificial sweeteners. Local manufacturers are increasingly investing in production capabilities to meet domestic demand and exploit export opportunities. The growing influence of Western dietary trends and the proliferation of international food brands further accelerate market growth, signaling exceptionally strong future potential for the artificial sweetener sector in Asia-Pacific.

Latin America Artificial Sweetener Market Analysis

Latin America holds a modest but steadily growing share of the artificial sweetener market, primarily driven by increasing health awareness and the expansion of the food and beverage industry in countries like Brazil and Mexico. The region faces high rates of obesity and diabetes, prompting governments and health organizations to promote aggressive sugar-reduction strategies. According to the Pan American Health Organization, taxes on sugary drinks in several Latin American countries have successfully influenced consumer behavior, leading to increased demand for diet alternatives. In Brazil, the growing middle class is adopting healthier lifestyles, driving sales of low-calorie products across supermarkets and pharmacies. As per the Mexican Ministry of Health, strict front-of-pack labeling laws require clear warnings on high-sugar products, encouraging manufacturers to swap sugar for artificial sweeteners to avoid negative front-of-pack labels. The presence of international food and beverage companies introduces advanced sweetening technologies and formulations to the local market. However, economic volatility and lower purchasing power in some rural areas limit mass-market adoption. Despite these challenges, increasing urbanization and exposure to global health trends are fostering a gradual acceptance of artificial sweeteners, and strategic investments in regional production could unlock extensive new opportunities.

Middle East and Africa Artificial Sweetener Market Analysis

The Middle East and Africa region presents emerging opportunities for the artificial sweetener market, driven by a rising prevalence of diabetes and increasing urbanization. Countries in the Gulf Cooperation Council (GCC), such as Saudi Arabia and the United Arab Emirates, have some of the highest rates of metabolic disorders globally, creating a strong institutional and consumer demand for sugar-free products. According to the International Diabetes Federation, the Middle East and North Africa region requires urgent dietary interventions due to these soaring metabolic health statistics. In South Africa and Nigeria, growing awareness of health and wellness is steadily influencing consumer choices, particularly among affluent urban populations. As per the World Health Organization, regional initiatives to combat non-communicable diseases are promoting the use of artificial sweeteners in processed foods and beverages. The hospitality and luxury tourism sectors in the Middle East also drive a consistent demand for premium low-calorie options in hotels and restaurants. However, limited regional production capabilities mean that most artificial sweeteners are imported, resulting in higher localized retail prices. Culturally, while traditional, highly sweetened foods remain staples, the market is opening up to modern, health-conscious alternatives. Tightening thresholds by local health ministries are progressively driving B2B reformulation projects across domestic food and beverage manufacturers.

COMPETITION OVERVIEW

The competition in the global artificial sweetener market is intense and characterized by the presence of large multinational corporations and specialized regional producers. Leading companies compete on product quality, innovation, and cost efficiency while striving to meet evolving consumer preferences for health and sustainability. The market is fragmented with players differentiating themselves through proprietary blending technologies and unique ingredient portfolios. Price competition is significant in commodity segments, but value-added solutions command premium pricing. Regulatory approval and safety records serve as critical barriers to entry, influencing brand trust and market access. Innovation in natural sweeteners like stevia and monk fruit challenges traditional synthetic options, forcing established players to diversify. Strategic partnerships with major food and beverage brands secure long-term contracts and drive volume growth. Mergers and acquisitions are common as companies seek to consolidate market position and expand geographic reach. Consumer education and transparency initiatives are increasingly important for building loyalty. Overall, the landscape requires continuous adaptation to scientific findings, regulatory changes, and shifting dietary trends to maintain a competitive advantage and drive sustainable growth in the industry.

KEY MARKET PLAYERS

Major Key Players in the Global Artificial Sweetener Market are Zydus Wellness Ltd., Sunwin Stevia International, Inc., PureCircle, MORITA KAGAKU KOGYO CO., LTD, Hermes Sweeteners Ltd., NutraSweet Property Holdings, Inc., McNeil Nutritionals, JK Sucralose, Ajinomoto Co., Inc., and Roquette

Top Strategies Used by Key Market Participants

Key players in the artificial sweetener market focus on product innovation to develop blends that mimic sugar taste more accurately. Companies invest in research to create natural and synthetic hybrids that reduce aftertaste and improve stability. Strategic acquisitions enable firms to expand their portfolios and access new technologies or geographic markets. Sustainability initiatives are central to organizations sourcing raw materials responsibly and reducing carbon footprints. Partnerships with food and beverage manufacturers facilitate the co-development of customized solutions for specific applications. Regulatory compliance and safety advocacy help build trust with consumers and policymakers. Digital tools and consumer insights drive targeted marketing and education campaigns. These strategies allow participants to differentiate their offerings and capture value in a competitive landscape driven by health trends.

Leading Players in the Global Artificial Sweetener Market

- Cargill Incorporated is a global leader in the artificial sweetener market with a diverse portfolio that includes stevia-based and high-intensity sweeteners. The company leverages its extensive supply chain to provide sustainable and high-quality ingredients to food and beverage manufacturers worldwide. Recent actions include expanding its EverSweet stevia production capacity to meet rising demand for natural zero-calorie sweeteners. Cargill actively collaborates with customers to develop customized sweetness solutions that enhance taste profiles while reducing sugar content. The organization invests heavily in research and development to innovate new blending technologies that mask aftertastes. By focusing on transparency and sustainability, Cargill strengthens its position as a trusted partner for brands seeking clean-label and health-focused ingredient solutions in the competitive global marketplace.

- Ingredion Incorporated plays a significant role in the artificial sweetener sector by offering a wide range of plant-based and specialty sweetening solutions. The company focuses on helping manufacturers reformulate products to reduce sugar without compromising texture or flavor. Recent strategies involve acquiring innovative biotech firms to enhance its portfolio of rare sugars and natural sweeteners. Ingredion utilizes advanced application centers to assist clients in optimizing formulations for various food categories. The organization emphasizes sustainability by sourcing raw materials responsibly and reducing environmental impact in its operations. Through strategic partnerships and continuous innovation, Ingredion provides tailored solutions that address consumer preferences for healthier options. These efforts reinforce its reputation as a key enabler of sugar reduction initiatives across the global food and beverage industry.

- Tate and Lyle PLC is a prominent provider of specialty food ingredients, including sucralose and other high-intensity sweeteners. The company is known for its Splenda brand, which is widely recognized and used in numerous consumer products globally. Recent actions include divesting non-core assets to focus on higher growth areas such as health and wellness ingredients. Tate and Lyle invests in expanding its manufacturing capabilities for sucralose to ensure a consistent supply and quality. The organization collaborates with major food brands to develop next-generation sweetening systems that improve taste and stability. By prioritizing innovation and customer-centric solutions, Tate and Lyle maintains its leadership in the artificial sweetener market. Its commitment to scientific rigor and product excellence supports the evolving needs of health-conscious consumers and manufacturers worldwide.

SEGMENTAL ANALYSIS

This research report on the global artificial sweetener market has been segmented and sub-segmented based on type, application, distribution channel & region.

By Type

- Aspartame

- Acesulfame-K

- Monosodium Glutamate

- Saccharin

- Sodium Benzoate

By Application

- Bakery Items

- Dairy Products

- Confectionery

- Beverages

By Distribution Channel

- Supermarkets & Hypermarkets

- Departmental Stores

- Convenience Stores

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What factors are driving growth in the frozen meat market?

Market growth is driven by increasing consumer demand for convenient and long-shelf-life protein sources, expanding retail and foodservice sectors, rising urbanization, changing lifestyles with greater preference for ready-to-cook or pre-prepared foods, and improved cold-chain infrastructure.

2. Which product types are included in the frozen meat market?

Key product types include frozen poultry (chicken, turkey), frozen red meat (beef, lamb), frozen pork, frozen seafood (in some definitions), and value-added frozen meat products like nuggets, sausages, kebabs, and marinated cuts.

3. What are the primary distribution channels for frozen meat products?

Primary channels include supermarkets and hypermarkets, specialized meat retail outlets, wholesale markets, foodservice distribution (restaurants, hotels, catering), and online grocery channels. Modern retail and e-commerce are increasingly significant for consumer access.

4. Who are the main consumers of frozen meat products?

Consumers include households seeking convenience, working professionals with limited time for fresh meal preparation, foodservice operators, quick-service restaurants (QSRs), and institutional buyers such as schools and hospitals.

5. How does frozen meat compare to fresh meat?

Frozen meat is typically more convenient and has a longer shelf life than fresh meat due to low-temperature storage that slows down spoilage and microbial activity. While fresh meat may be preferred for taste and texture by some consumers, frozen meat offers cost savings and reduced food waste.

6. What role does cold-chain infrastructure play in the market?

Cold-chain infrastructure, including refrigerated transportation, storage facilities, and proper retail display freezers—is crucial for maintaining product quality, safety, and reducing spoilage. Investments in cold-chain enhancements are key to market expansion, especially in emerging regions.

7. What challenges does the frozen meat market face?

Challenges include the high cost of maintaining cold-chain logistics, fluctuating raw material prices, strict regulatory compliance for food safety and hygiene, consumer perception that fresh meat is superior, and energy costs associated with freezing and storage.

8. How do regulations affect the frozen meat market?

Government regulations influence hygiene standards, food safety testing, labeling, traceability, animal welfare compliance, and import/export controls. Compliance with such standards is essential to ensure consumer trust and cross-border trade.

9. What trends are shaping the frozen meat market?

Emerging trends include value-added frozen meat products, clean-label and natural ingredient formulations, convenience-oriented packaging, growth in frozen ethnic and ready meals, and increasing online grocery shopping.

10. What is the future outlook for the frozen meat market?

The future outlook is positive, with steady expansion anticipated due to increased adoption of frozen meat by households and foodservice outlets, advancements in cold-chain logistics, expanding retail reach, and continued demand for convenience foods. Ongoing innovations and alignment with health and sustainability trends will support long-term growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com