Global New Crop Protection Generics Market Size, Share, Trends, COVID-19 Impact & Growth Forecast Report, Segmented By Type (Insect Growth Regulators, Insecticide, Fungicide, Herbicide), Crop Type (Vegetables, Nuts, Fruits, Oilseeds & Pulses, Grains & Cereals, Others), And Region Region (North America, Europe, Asia Pacific, Latin America, and Middle East - Africa), Industry Forecast From 2026 to 2034

Market Size, 2025

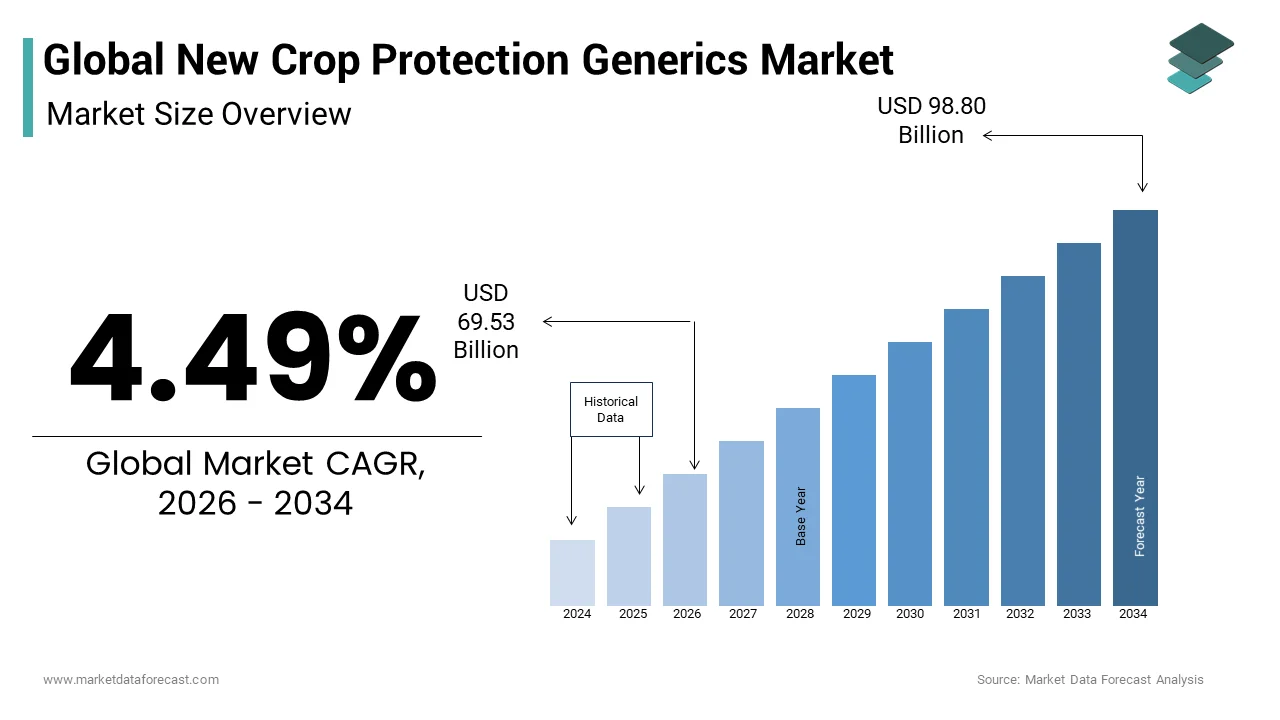

$66.54 BnMarket Estimate, 2026

$69.53 BnMarket Forecast, 2034

$98.80 BnCAGR, 2026–2034

4.49%Global New Crop Protection Generics Market Size

The global new crop protection generics market size was valued at USD 66.54 billion in 2025 and is anticipated to reach USD 69.53 billion in 2026 to reach USD 98.80 billion by 2034, growing at a CAGR of 4.49% from 2026 to 2034.

Other key research and development (R&D) areas of interest include selectivity in its control action against target pests, low application rate per hectare, broad-spectrum control to cover a diverse group of pests and diseases, and compliance with the regulatory mandates of regional and local markets.

Crop protection products are used to reduce yield losses caused by diseases and pests. According to the Royal Society of Chemistry, around 800 chemically active ingredients are registered for use as crop protection solutions worldwide. These chemicals are broadly classified into the groups of herbicides, fungicides, and insecticides. In recent years, research in crop protection chemicals has focused on developing compounds that are safer than their older counterparts to meet the demand for new molecular solutions to control pests that have developed resistance to older compounds.

MARKET DRIVERS AND RESTRAINTS

According to the International Food Policy Research Institute, nearly 690 million people suffered from hunger worldwide in 2019, an increase of 10 million since 2018, and the COVID-19 pandemic could push 83 million -132 million more into hunger in 2020, according to the 2020 report on the state of food security and nutrition in the world (SOFI), published on July 13. The State of Food Security and Nutrition in the World (SOFI) 2020 predicts that 841.4 million people will go hungry worldwide by 2030 if these trends continue and the world does not meet its targets. Goals for 2025 and 2030 to overcome malnutrition. According to the FAO chief economist, he attributed the alarming results to the inability to access healthy food, noting that around the world, 3 billion people cannot afford and do not have access to good nutrition. These factors are anticipated to fuel the growth rate of the new crop protection generics market.

To transform food systems to reduce these costs, policymakers must consider both supply and demand. Policies should improve the efficiency of the food supply chain and subsidize the production of nutritious food; at the same time, expanding social safety nets and policies that encourage behavior change can promote healthier diets. People are considered to be food secure when they have access to healthy, nutritious, and sufficient food at all times to maintain a healthy life. Due to the continuous increase in the population and the limited arable land to satisfy the increasing food needs, the food security of the population is reduced. To meet future demand for food, it is necessary to increase food production worldwide. In such a scenario, the use of phytosanitary products is unavoidable. This situation has caused the growth of the market of chemical products for the protection of crops. Biopesticides are naturally produced pesticides with minimal use of chemicals. As environmental considerations and the potential for contamination and health risks associated with many conventional pesticides increase, the demand for biopesticides has steadily increased in all regions of the world. Biopesticides are gaining popularity due to their less toxic or non-toxic nature compared to synthetic pesticides.

These pesticides enter the human body through the consumption of contaminated fruits and vegetables. The main health effects associated with pesticide residues include cancer, birth defects, neurological disorders, endocrine disruptors, and reproductive effects. The effect of a pesticide is determined by the duration of exposure and the toxicity of the pesticide. The effects that can occur are acute or chronic. Due to the potential health risks associated with the consumption of pesticides, continuous monitoring of fruits and vegetables is necessary during cultivation. Pesticides such as glyphosates, difenoconazole, imidacloprid, and bifenthrin are common pesticides found in fruits and vegetables that reach consumers in the market.

Impact of COVID-19 on New Crop Protection Generics Market

The COVID-19 epidemic has affected public health and the global economy. The impact of COVID-19 on the global economy has resulted in socioeconomic disruption. Along with other industries, the spread of COVID-19 has affected the agricultural inputs sector. The coronavirus has impacted critical processes involved in the production and distribution of agrochemicals, from the importation of raw materials to the manufacture of the final product. China is one of the leading producers of active ingredients and pesticide products. Thus, the closure of Chinese factories has caused a massive shortage of active ingredients (necessary for the manufacture of pesticides) and phytosanitary products. This supply chain disruption was mainly due to lockdowns that have been declared in many countries to contain the spread of the coronavirus. In addition, these closures have limited the transport of raw materials and phytosanitary products in the most affected areas. Many shipping companies have also suspended their services. Due to these major problems in the supply chain, sales of pesticides for crops and other agricultural products are expected to be lower than last year, which will cause a decrease in the market value of phytosanitary products.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.49% |

| Segments Covered | By Type and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | New Crop Protection Generics Market includes Hansen, BASF, Cheminova, PI Industries, Corteva, Bayer Crop Science, and Syngenta. |

SEGMENTAL ANALYSIS

By Type Insights

The herbicide is expected to be the fastest-growing segment due to a large number of herbicide products that will no longer be patented in the next few years. In 2018-22, Pinoxaden, Aminopyralid, and Tembotrione, these herbicides with worldwide sales of almost 950 million dollars, will be withdrawn from the patent. Other herbicides that will no longer be patented during the forecast period include Amino-pyralid, Fluopicolide, and Flucetosulfuron. Insecticides like Flubendiamide and Spirotetramat, with combined global sales of nearly $ 595 million, will no longer be patented during the forecast period. Fungicidal products that will no longer be patented during the forecast period are Amisulbrom, Fenpyrazamine, Fluopicolide, etc.

REGIONAL ANALYSIS

North America Market Analysis

North America was the main market with consumption of 11.20 million tons in 2019. The region includes several agriculture-based economies and is home to several multinational agricultural companies, especially in the United States. The region is driven by the rapid adoption of technological advancements by the agricultural community, along with a series of regulatory frameworks that monitor positive growth. It has always been a pioneer in terms of crop protection solutions and the promotion of agricultural practices around the world. The presence of emerging economies such as India, Indonesia, China, Malaysia, the Philippines, and Thailand has boosted regional demand. Changing economic conditions have paved the way for advanced technological interventions, especially in West Asia. India and China have established themselves as powers of various agricultural products and are also part of the high export community in the region.

KEY MARKET PLAYERS

These are some of the market players that dominate the global new crop protection generics market.

- Hansen

- BASF

- Cheminova

- PI Industries

- Corteva

- Bayer Crop Science

- Syngenta

RECENT MARKET NEWS

- In November 2024, BASF and TECNALIA, a European center for technological research and development, collaborated on digitization to accelerate global research and the development of new phytosanitary products. This contributes to the faster development of innovations that meet the needs of farmers around the world to control weeds, fungal diseases, and insect pests in their crops.

- In September 2024, Sumitomo Chemical Co., Ltd announced that it had agreed with Nufarm Ltd., Australia's leading crop protection company, to acquire all of the shares of Nufarm's four South American companies.

MARKET SEGMENTATION

This research report on the global new crop protection market is segmented and sub-segmented into the following categories.

By Type

- Herbicides

- Fungicides

- Insecticides

- Crop Growth Regulators

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the new crop protection generics market?

The new crop protection generics market comprises off-patent agrochemical products—including herbicides, insecticides, fungicides, and bio-based alternatives—that are manufactured and sold by multiple companies once original patents expire.

Why are crop protection generics important?

Generics increase affordability and accessibility of crop protection products for farmers, support competitive pricing, and enhance crop yield protection without the high cost of patented chemicals.

What drives growth in the crop protection generics market?

Growth is driven by patent expirations, rising global food demand, increasing adoption of cost-effective solutions, regulatory support for generics, and budget constraints among smallholder farmers.

What types of generics are included in this market?

Common crop protection generics include herbicides, insecticides, fungicides, nematicides, and plant growth regulators that are equivalent to branded products in formulation and efficacy.

How do crop protection generics differ from branded agrochemicals?

Generics are off-patent, competitively priced, and bioequivalent to branded products, while branded products are often protected by patents and supported by proprietary R&D and marketing.

Which crops commonly use crop protection generics?

Generics are widely used in cereals, oilseeds, fruits, vegetables, pulses, and commercial crops where cost-effective pest, weed, and disease control is needed.

How do regulations impact the crop protection generics market?

Regulatory frameworks determine data requirements, registration processes, equivalence standards, and safety approvals, which can speed up or restrict generic product entry.

What are the key trends in the crop protection generics market?

Trends include increased generic registrations, formulation innovations, integrated pest management (IPM) compatibility, and expansion in emerging markets.

What role does sustainability play in crop protection generics?

Sustainability drives development of lower-toxicity generics, bio-based alternatives, and products compatible with precision agriculture and environmental safety goals.

Which regions lead the crop protection generics market?

North America and Europe have mature markets due to established regulatory pathways, while Asia-Pacific and Latin America are high-growth regions with expanding agriculture and cost-sensitive demand.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com