Global Biopesticides Market Size, Share, Trends & Growth Forecast Report, Segmented ByType (Bio Insecticides, Bio Fungicides, Bionematicides and Bio Herbicides), Source (Microbial, Biochemical and Beneficial Insects), Mode of Application (Seed treatment, Soil treatment, Foliar Spray and Others), Formulation (Liquid and Dry), Crop (Grains and Cereals, Pulses and Oilseeds, Vegetables and Fruits, Others) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis from 2026 to 2034

Global Biopesticides Market Size

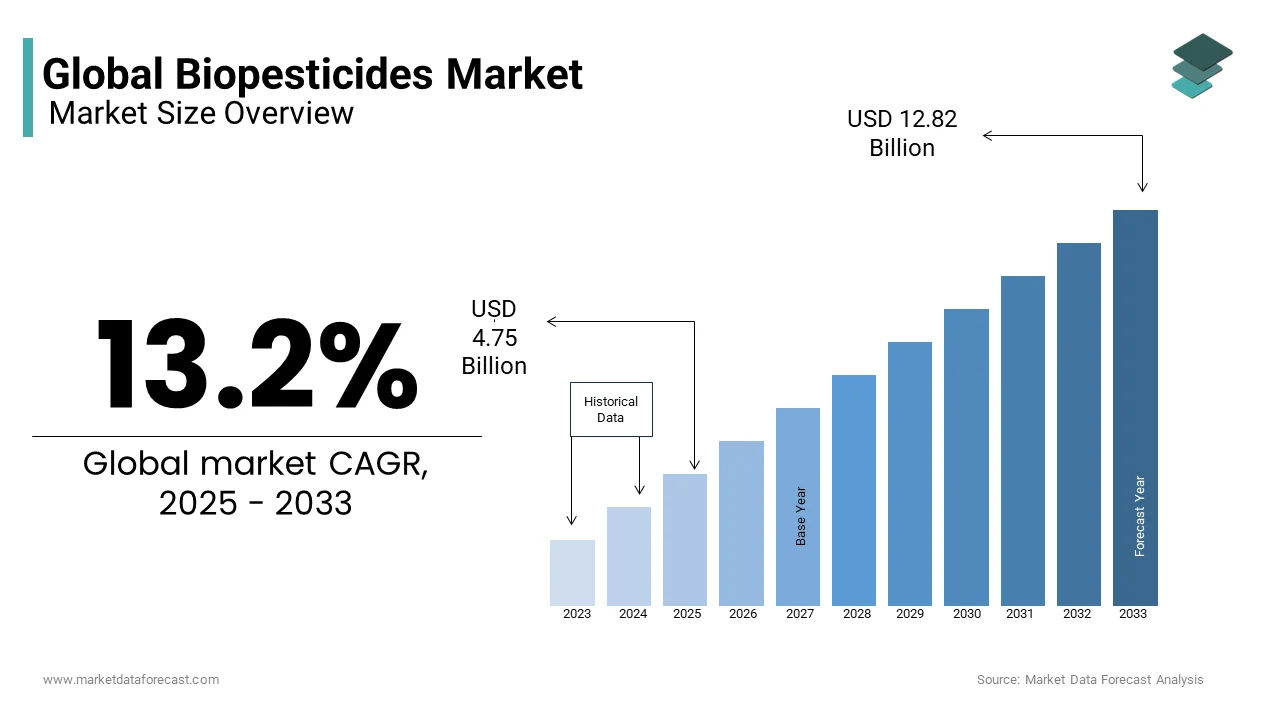

The global biopesticides market was valued at USD 4.75 billion in 2025 and is anticipated to reach USD 5.38 billion in 2026 from USD 14.50 billion by 2034, growing at a CAGR of 13.2% during the forecast period from 2026 to 2034.

Biopesticides are naturally derived pest management agents sourced from microorganisms plants or minerals that target agricultural pests with minimal disruption to non-target species and ecosystems. Unlike synthetic chemical pesticides they degrade rapidly reduce residues in food and water and align with integrated pest management principles. According to the Food and Agriculture Organization of the United Nations, over 500 million smallholder farms globally rely on low cost and locally adaptable pest control methods yet only 5% currently use registered biopesticides due to awareness and access gaps. The United States Environmental Protection Agency has approved over 430 biopesticide active ingredients as of 2025 reflecting accelerated regulatory pathways under the Reduced Risk Pesticide Initiative. Meanwhile, the International Biocontrol Manufacturers Association estimates that over 800 commercial biopesticide products are now available worldwide targeting insects fungi nematodes and weeds. These contextual dynamics position biopesticides not as niche alternatives but as essential tools in the global transition toward resilient and residue free food systems amid tightening toxicological standards and biodiversity conservation imperatives.

MARKET DRIVERS

Rising Regulatory Restrictions on Synthetic Pesticide Residues

Governments worldwide are imposing stricter limits on synthetic pesticide residues in food and water, which is accelerating the adoption of biopesticides as compliant alternatives. The rising regulatory rstrictions on syntehetic pesticide residues is solely propelling the growth of bipoesticides market. According to the European Union’s 2023 amendment to Regulation EC 396 2005 maximum residue levels for chlorpyrifos and imidacloprid were reduced by 90% in fruits and leafy vegetables triggering withdrawal of over 200 conventional products. In the United States, the Environmental Protection Agency banned chlorpyrifos for all food uses in 2023 following neurodevelopmental risk assessments affecting over 80 million acres of cropland. Brazil’s National Health Surveillance Agency ANVISA reclassified 36 synthetic pesticides as highly toxic in 2024 restricting their use in coffee and citrus sectors. These regulatory shifts compel growers to seek alternatives that meet international trade standards without sacrificing pest control efficacy.

Expansion of Organic and Regenerative Farming Systems

The global proliferation of organic and regenerative agriculture, which are among the few pest control options permitted under certification standards is majorly fuelling the growth of biopesticides market. The European Commission’s target of 25% organic land by 2030 is driving national subsidies for biocontrol inputs with France allocating 45 million euros in 2024 for biopesticide adoption among fruit and vegetable growers. Similarly, India’s Paramparagat Krishi Vikas Yojana supported 700000 organic farming clusters by 2024 where biopesticides derived from pongamia and garlic are locally produced. Retailers like Aldi and Whole Foods now mandate residue free certification for fresh produce further incentivizing conventional growers to integrate biopesticides into transition strategies. This systemic alignment between farming philosophy certification requirements and market access ensures sustained demand beyond short term pest outbreaks.

MARKET RESTRAINTS

Limited Field Efficacy Under High Pest Pressure Conditions

The variable performance in environments with intense or prolonged pest infestations, where synthetic pesticides offer more immediate and broad-spectrum control is limiting the growth of biopesticides market. According to the International Rice Research Institute, field trials in Southeast Asia showed that Bacillus thuringiensis reduced leaffolder damage by only 45% compared to 85% achieved by synthetic pyrethroids during peak monsoon outbreaks. The United States Department of Agriculture noted in 2024 that biopesticide application in cotton required 2 to 3 times more frequent treatments than conventional alternatives to maintain bollworm control increasing labor and operational costs. Additionally, the narrow target spectrum of many biopesticides means multiple products must be tank mixed to address complex pest complexes which complicates registration and increases application complexity.

Stringent and Fragmented Registration Requirements Across Jurisdictions

The regulatory approval process for biopesticides remains a major barrier due to inconsistent data requirements high costs and lengthy timelines that disproportionately affect small innovators. This is another attribute hampering the growth of biopesticides market. In contrast, the United States Environmental Protection Agency’s Biopesticides and Pollution Prevention Division offers expedited review but still requires over 100 study guidelines for full approval. India’s Central Insecticides Board mandates separate state level trials in three agroclimatic zones adding 18 to 24 months to national registration. This fragmentation stifles innovation and delays access, particularly for region specific biological solutions that could address local pest challenges.

MARKET OPPORTUNITIES

Advancements in Formulation Science Enhancing Shelf Life and Field Stability

Recent innovations in microencapsulation nanoemulsions and adjuvant technology are overcoming historical limitations of biopesticides related to UV degradation temperature sensitivity and short residual activity. The advancements in formulation science enhancing shelf life and field stability is creating new opportunities for the growth of biopesticides market. In India, the Council of Scientific and Industrial Research developed a nano neem formulation that improved rainfastness and foliar adhesion increasing whitefly control efficacy by 38% in tomato crops. The European Commission’s Horizon Europe program funded six formulation projects in 2024 focused on stabilizing baculoviruses for lepidopteran control in Mediterranean climates. Companies like Bayer and BASF have commercialized dry flowable and oil dispersion formats that enable tank mixing with conventional pesticides while maintaining microbial viability. These advances transform biopesticides from fragile biologicals into robust field tools compatible with standard spraying equipment and spray schedules thereby removing adoption barrier for mainstream growers.

Integration of Biopesticides into Digital Pest Forecasting Platforms

The emergence of biopesticides with artificial intelligence driven pest monitoring systems is creating precision application models that maximize efficacy and cost efficiency. This factor is also to enhance the growth of biopesticides market. According to the research, over 120 farm advisory platforms now incorporate biopesticide recommendation engines triggered by real time trap data and weather based disease models. In California, the Department of Food and Agriculture partnered with startups like Trace Genomics to deploy DNA based pathogen detection that prescribes specific biofungicides before symptoms appear reducing crop loss by up to 30% in lettuce trials. In Kenya, the CABI-led PlantwisePlus program integrated SMS based pest alerts with localized biopesticide recipes reaching 2 million smallholders in 2024. Similarly, Brazil’s Embrapa launched an app that matches regional pest pressure levels with optimal bioinsecticide application windows based on historical climate and infestation data. This digitization transforms biopesticides from reactive treatments to proactive components of predictive integrated pest management enhancing their reliability and return on investment.

MARKET CHALLENGES

Lack of Standardized Efficacy Testing Protocols for Biologicals

A persistent challenge in the biopesticides sector is the absence of globally harmonized protocols to evaluate performance under field conditions leading to inconsistent results is likely to be a challenge for the growth of biopesticides market. According to the Organisation for Economic Co-operation and Development, only 8 countries have adopted standardized testing guidelines for microbial biopesticides as of 2024 resulting in variable trial designs that hinder cross study comparisons. The United States Department of Agriculture observed that efficacy claims for the same Bacillus subtilis strain varied by 40 to 75% across university trials due to differences in soil type application timing and pest pressure metrics. In India, the All India Coordinated Research Project on Biopesticides found that over 60% of commercial products failed independent validation under local conditions despite regulatory approval. This scientific ambiguity complicates extension services and retailer recommendations as agronomists cannot confidently predict field outcomes.

Supply Chain Vulnerabilities in Live Microbial Production

The biological nature of many biopesticides introduces unique logistical challenges related to viability maintenance cold chain requirements and limited shelf life that constrain distribution especially in tropical and remote regions, which is additionally to limit the growth of biopesticides market. According to the International Institute of Tropical Agriculture, up to 50% of microbial biopesticide potency is lost during transport in sub Saharan Africa due to ambient temperatures exceeding 35 degrees Celsius and lack of refrigerated storage. Even in developed countries, the United States Environmental Protection Agency requires strict temperature logs for live product shipments which increases costs and complicates e commerce fulfillment. Fermentation based production also faces batch to batch variability with the European Food Safety Authority noting that spore counts in commercial Bacillus thuringiensis products varied by 25% across lots. These supply chain fragilities limit scalability and reliability particularly for smallholder focused models where infrastructure is weakest.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 13.2% |

| Segments Covered | By Type, Source, Formulation, Mode of Application, Crop, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | BASF SE (Germany), BAYER AG (Germany), Biobest Group NV (Belgium), Certis USA LLC (US), Novozymes A/S(Denmark), Marrone Bio Innovations (US), Syngenta AG (Switzerland), Nufarm (Australia), Som Phytopharma India Ltd (India), Valent Biosciences LLC (US), and others. |

SEGMENTAL ANALYSIS

By Type Insights

By Type Insights

The bioinsecticides segment is expected to dominate the market during the forecast period. Bioinsecticides are safe for use and pose no hazards to the environment, and they do not leave behind any chemical residue on the plants. Also, the reduced product development cost and the time associated with bioinsecticides offer advantages to the manufacturers, and they can also register within a short duration, while chemical registration can take as long as three years.

By Source Insights

Based on sources, the global biopesticides market is segmented into Microbials, Biochemicals, and Beneficial Insects. Microbial biopesticides are estimated to dominate the biopesticides market in the forecast period, as microbial-origin pesticides are naturally composed of occurring viruses, fungi, or bacteria. The microbials are the most preferred organic and residue-free food production. Factors such as the higher advantage of selectivity, high affectivity, no adverse effects on humans, plants, and animals, and ease of use are propelling the growth of the biopesticides market.

By Formulation Insights

Based on Formulation, the global biopesticides market is segmented into liquid and dry. Liquid biopesticides are estimated to record the highest CAGR during the forecast period. Liquid biopesticides have a longer term of action (up to 6 months) than dry biopesticides (up to 3 months) and provide effective and efficient disease control performance.

By Mode of Application Insights

Based on Formulation, the global biopesticides market is segmented into Seed treatment, Soil treatment, Foliar Spray, and Others. Foliar spray is widely used among farmers because it helps in the immediate recovery of the pests and insecticide parts of the plants. This is the most effective mode of application as it is a safe and easily handled application.

By Crop Insights

Based on Crop, the global biopesticides market is segmented into grains and cereals, Pulses and Oilseeds, Vegetables and Fruits, and Others. The vegetable and fruit segment is expected to boost market growth during the forecast period due to the growing trend of organic agriculture and the increasing demand for organic fruits and vegetables. Moreover, the farmers are using a combination of biopesticides with other chemicals to meet the demand for export-quality fruits and vegetables.

REGIONAL ANALYSIS

North America Market Analysis

North America accounts for the largest market share of the biopesticides market. Due to rising concerns over the harmful chemicals in the environment, the governments of several countries have imposed strict regulations associated with the environment. The United States is one of the leading countries for the export of various fruits and vegetables, which fuels the demand for biopesticides in the U.S. The increasing demand for organic and residue-free crops is leading to the adoption of bioinsecticides. Moreover, the presence of a huge number of key players in this region leads to investment in research and development in crop production and protection, which is contributing to the growth of the market in the projected period.

Asia Pacific Market Analysis

Asia-Pacific is expected to become the fastest-growing market for biopesticides during the forecast period. Countries like India, China, Japan, and others have high plant diversities and a large set of different climatic conditions. Furthermore, the increasing awareness of consumers towards the toxic substances in the food chain makes it imperative for crop producers to use non-toxic solutions such as bio-based pesticides, which are fueling the growth of the biopesticides market in the future.

Europe Market Analysis

Europe is also going to witness a steady growth rate during this period due to the growing demand for safe and quality food, increasing demand of consumers for organic food, and rising government initiatives in promoting biocontrol products.

COMPETITIVE LANDSCAPE

The biopesticides market features a dynamic competitive landscape blending multinational agrochemical giants specialized biological firms and agile biotech startups. Large corporations like Bayer and BASF leverage their regulatory expertise and global distribution to embed biopesticides into integrated crop protection programs while maintaining dominance in conventional chemistry. In contrast niche players such as Certis USA Marrone Bio Innovations and Koppert Biological Systems focus exclusively on biological solutions often targeting high value horticulture or organic niches with tailored products. The barrier to entry remains moderate due to complex living organism production but high due to fragmented global registration requirements. Competition centers less on price and more on field efficacy consistency and technical support as growers demand reliable performance comparable to synthetics. Regional players in India, Brazil, and Kenya, are also gaining traction by developing low cost locally adapted formulations for smallholders. This ecosystem fosters both collaboration and competition driving rapid innovation in microbial discovery formulation science and digital integration.

KEY MARKET PLAYERS

Some of the leading companies operating in the global biopesticides market are

- BASF SE (Germany)

- BAYER AG (Germany)

- Biobest Group NV (Belgium)

- Certis USA LLC (US)

- Novozymes A/S(Denmark)

- Marrone Bio Innovations (US)

- Syngenta AG (Switzerland)

- Nufarm (Australia)

- Som Phytopharma India Ltd (India)

- Valent Biosciences LLC (US)

Top Players In The Market

Bayer AG

Bayer AG is a global leader in the biopesticides market through its acquisition of AgraQuest and subsequent development of the Serenade and VOTiVO product lines which feature Bacillus and Pseudomonas strains for disease and nematode control. The company integrates biopesticides into its broader crop protection portfolio offering growers holistic integrated pest management solutions. In recent years Bayer has expanded its biologicals R&D center in California focusing on novel microbial discovery and fermentation scale up. It also launched the Biologicals Partner Program to co-develop and distribute biopesticides with regional innovators in Latin America and Asia. By embedding biologicals into its digital farming platform FieldView Bayer enables data driven application timing which enhances efficacy and farmer trust in biological solutiosns.

BASF SE

BASF SE plays a pivotal role in the biopesticides market with a diverse portfolio including biological seed treatments fungicides and insecticides under brands like Serifel and LifeGard. The company leverages its global distribution network to deliver microbial and biochemical solutions across field crops fruits and vegetables. Recently BASF invested in a dedicated fermentation facility in Limburgerhof Germany to increase production capacity for Bacillus amyloliquefaciens strains used in its biofungicides. It also formed strategic alliances with biotech startups to access novel modes of action such as RNA based biopesticides. Through its Agricultural Solutions division BASF promotes biologicals as essential components of sustainable crop protection systems that reduce chemical load while maintaining yield reliability.

Certis USA LLC

Certis USA LLC is a key innovator in the biopesticides sector offering a broad range of microbial biochemical and plant extract-based products including Double Nickel Cueva and Molt-X. The company specializes in developing residue free solutions for high value horticultural and organic farming systems. In recent years, Certis has expanded its manufacturing capabilities in Maryland to support global demand and accelerated regulatory registrations in over 30 countries. It launched the BioRise platform to provide technical support and efficacy data to distributors and growers ensuring proper use and performance. By focusing on practical field validation and rapid registration Certis strengthens accessibility and credibility of biopesticides particularly in export oriented fresh produce markets.

Top strategies Used By The Key Market Participants

Key players in the biopesticides market prioritize strategic acquisitions of biotech startups to access novel microbial strains and modes of action. They invest heavily in fermentation and formulation infrastructure to ensure scalable and stable production of live biologicals. Companies integrate biopesticides into digital agronomy platforms to provide data driven application guidance that enhances field performance. Geographic expansion focuses on regions with strong organic regulations or export driven horticulture such as Europe, Latin America, and Southeast Asia. Additionally, firms establish open innovation partnerships with research institutions and small developers to accelerate product pipelines and share regulatory burdens in fragmented approval landscapes.

MARKET SEGMENTATION

This research report on the global biopesticides market has been segmented and sub-segmented into the following categories.

By Type

- Bioinsecticides

- Bio fungicides

- Bio nematicides

- Bioherbicides

By Source

- Microbials

- Biochemicals

- Beneficial Insects

By Formulation

- Dry

- Liquid

By Mode of Application

- Seed treatment

- Soil treatment

- Foliar Spray

- Others

By Crop

- Grains and Cereals

- Pulses and Oilseeds

- Vegetables and Fruits

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the biopesticides market?

The biopesticides market includes biological pest control products derived from natural materials such as microbes, botanical extracts, and pheromones that protect plants from pests and diseases with minimal environmental impact.

Why is the biopesticides market growing?

Growth is driven by regulatory restrictions on synthetic pesticides, rising demand for sustainable agriculture, organic food trends, environmental concerns, and increasing investment in biological crop protection R&D.

What types of biopesticides are there?

Common types include microbial biopesticides (bacteria, fungi, viruses), biochemical biopesticides (plant extracts, pheromones), and botanical pesticides.

How do biopesticides work?

Biopesticides control pests by targeting specific insects, pathogens, or weeds through natural mechanisms such as infection, repulsion, hormone disruption, or competition, often improving soil and ecosystem health.

. What are the main applications of biopesticides?

Biopesticides are used in crops like fruits, vegetables, cereals, pulses, and specialty plants, both in field and greenhouse cultivation systems.

How do regulations impact the biopesticides market?

Government regulations promote biopesticide use by restricting harmful chemicals, fast-tracking registration of natural products, and incentivizing sustainable practices, which increases producer and farmer adoption.

Which regions lead the biopesticides market?

The Asia-Pacific, North America, Europe, and Latin America are key regions, with strong adoption in countries supporting organic farming and sustainable agriculture initiatives.

What are the benefits of using biopesticides?

Benefits include low toxicity to humans and wildlife, reduced chemical residues, specificity to target pests, improved soil health, and alignment with sustainable and organic farming standards.

What trends are shaping the biopesticides market?

Major trends include next-generation microbial formulations, integration with precision agriculture, seed treatment solutions, multi-mode action products, and digital pest monitoring tools.

What challenges does the market face?

Challenges include variable field performance, shorter shelf life, complex formulation requirements, higher costs compared to conventional pesticides, and limited farmer awareness.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com