North America Air Conditioning Systems Market Size, Share, Trends & Growth Forecast Report By Product Type, By End-User, and By Country (U.S., Canada & Rest of North America) – Industry Analysis and Forecast, 2026 to 2034

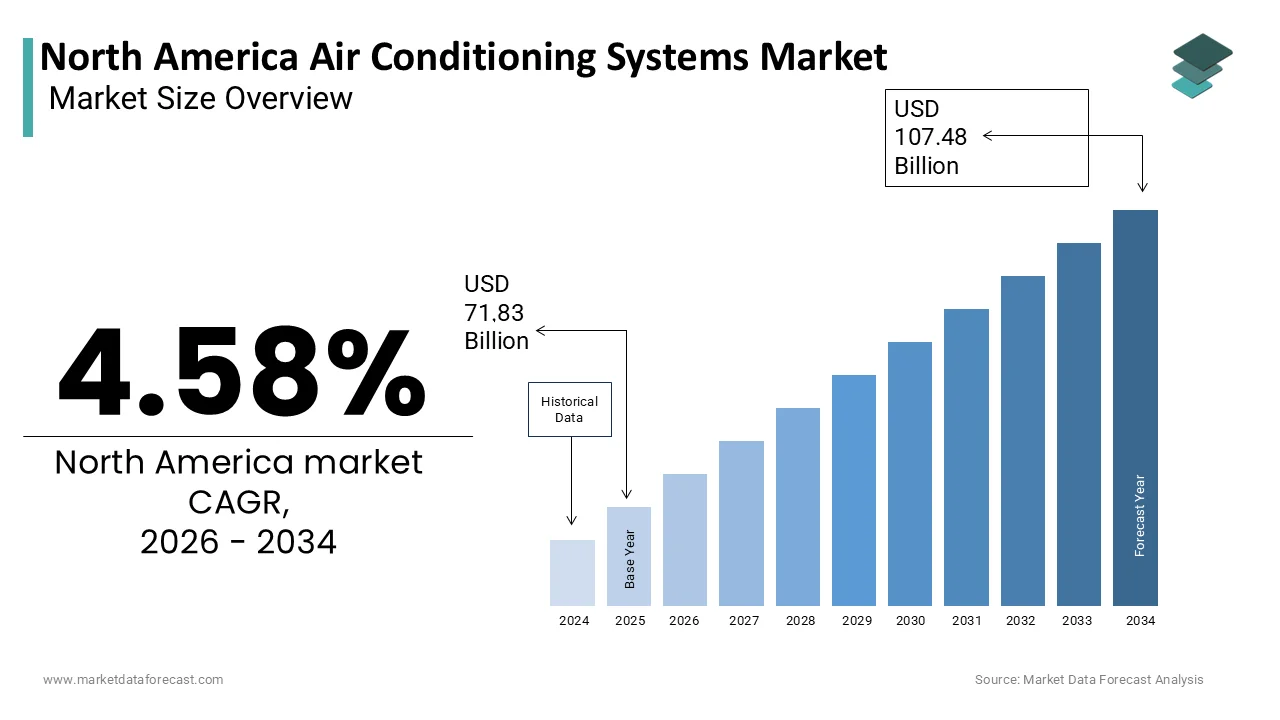

Market Size, 2025

$71.83 BnMarket Estimate, 2026

$75.12 BnMarket Forecast, 2034

$107.48 BnCAGR, 2026–2034

4.58%North America Air Conditioning Systems Market Size

The North America air conditioning systems market was worth USD 71.83 billion in 2025 and is anticipated to reach a valuation of USD 107.48 billion by 2034 from USD 75.12 billion in 2026, and it is predicted to register a CAGR of 4.58% 2026 to 2034.

The North America air conditioning systems market encompasses a broad range of cooling technologies designed for residential, commercial, and industrial applications. These systems include central air conditioners, ductless mini-splits, window units, packaged systems, and industrial chillers that regulate temperature and humidity in enclosed environments. The market is shaped by technological advancements, energy efficiency standards, and evolving consumer expectations regarding indoor climate control.Beyond residential demand, commercial infrastructure such as office buildings, hospitals, retail centers, and data centers increasingly rely on advanced HVAC systems to maintain operational efficiency and occupant comfort.

MARKET DRIVERS

Rising Frequency of Heatwaves and Extreme Weather Events

One of the primary drivers fueling the growth of the North America air conditioning systems market is the increasing frequency and intensity of heatwaves and extreme weather events across the region. According to the National Oceanic and Atmospheric Administration (NOAA), the number of heatwave days in the contiguous United States has increased significantly since the 1960s , with 2023 recorded as one of the hottest years on record. These climatic changes have significantly heightened the demand for reliable cooling solutions in both residential and commercial settings.

In response to rising temperatures, homeowners are increasingly investing in permanent cooling systems rather than relying on temporary or portable alternatives. As per a 2025 survey conducted by the National Association of Home Builders, over 70% of prospective homebuyers consider air conditioning a necessity when purchasing new housing , particularly in southern states like Texas, Florida, and Arizona where summer temperatures regularly exceed 100°F. Similarly, public health agencies such as the Centers for Disease Control and Prevention have emphasized the importance of indoor cooling in reducing heat-related illnesses and fatalities, further reinforcing consumer adoption.

Also, city governments and utility providers are promoting energy-efficient AC installations through rebate programs and incentives, encouraging consumers to upgrade aging systems. This convergence of climate pressures, health concerns, and policy support is driving sustained demand for modern air conditioning systems across North America.

Expansion of Smart and Energy-Efficient Cooling Technologies

Another key driver of the North America air conditioning systems market is the rapid expansion of smart and energy-efficient cooling technologies. Consumers are increasingly adopting intelligent HVAC systems equipped with Wi-Fi connectivity, programmable thermostats, and remote monitoring capabilities to enhance comfort while reducing energy consumption. According to the Consumer Technology Association, sales of smart thermostats in the U.S. grew by more than 18% in 2023 , reflecting a broader shift toward connected home automation.

Manufacturers such as Carrier, Lennox, and Trane have introduced next-generation air conditioning units featuring variable-speed compressors, adaptive learning algorithms, and compatibility with voice assistants like Alexa and Google Assistant. These innovations allow users to optimize cooling performance based on occupancy patterns and outdoor conditions, leading to significant reductions in electricity bills and carbon footprints. As per the U.S. Department of Energy, upgrading to an ENERGY STAR-certified system can result in annual energy savings, making these units increasingly attractive to cost-conscious buyers.

Moreover, federal and state-level regulatory frameworks, including the Environmental Protection Agency’s updated refrigerant management rules and building code updates under ASHRAE Standard 90.1, are pushing manufacturers to develop more sustainable products. With greater awareness around energy conservation and rising electricity costs, the transition to smart and energy-efficient air conditioning systems is expected to continue accelerating throughout the region.

MARKET RESTRAINTS

High Initial Installation and Maintenance Costs

A significant restraint affecting the North America air conditioning systems market is the high initial installation and ongoing maintenance costs associated with advanced cooling technologies. While demand for energy-efficient and smart air conditioning units continues to rise, many consumers remain hesitant due to the substantial upfront investment required.

Even among those who opt for smaller, room-based cooling solutions, the cumulative expenses of regular servicing, filter replacements, and potential repairs pose a financial burden. Data from the National Association of Home Builders indicates that nearly 40% of homeowners delay HVAC upgrades due to affordability concerns , especially in economically vulnerable communities. This trend limits market penetration, particularly in rural areas and lower-income neighborhoods where disposable incomes are constrained.

Furthermore, supply chain disruptions and rising material costs—especially for copper, aluminum, and refrigerants—have contributed to inflationary pressures on AC equipment pricing. As reported by the Bureau of Labor Statistics, HVAC equipment prices increased between 2022 and 2025 , further dampening consumer adoption rates. Unless financing options, government subsidies, and leasing models expand significantly, these cost barriers will continue to hinder broader market growth.

Regulatory Restrictions on Refrigerants and Environmental Compliance

Another critical restraint influencing the North America air conditioning systems market is the tightening regulatory landscape surrounding refrigerant usage and environmental compliance. Governments at both federal and state levels are implementing stringent policies to phase out hydrofluorocarbons (HFCs) and other greenhouse gases linked to global warming. According to the U.S. Environmental Protection Agency, HFCs have a global warming potential thousands of times greater than carbon dioxide , prompting aggressive legislative action under the American Innovation and Manufacturing (AIM) Act of 2020.

Under this framework, the EPA has mandated an 85% reduction in HFC production and consumption by 2036 , necessitating a complete overhaul of existing AC manufacturing processes. Manufacturers must now invest heavily in research and development to adopt alternative refrigerants such as hydrofluoroolefins (HFOs) and natural refrigerants like propane and CO₂, which come with technical complexities and higher production costs. As per the Air-Conditioning, Heating & Refrigeration Institute, industry-wide compliance expenditures related to refrigerant transitions exceeded $2 billion in 2023 alone , placing financial pressure on both large and small-scale producers.

These regulatory shifts also impact end-users, as older HFC-based systems face obsolescence and reduced service availability. Consequently, while environmentally responsible, these mandates create short-term economic friction, slowing down consumer replacement cycles and limiting the rate of technology adoption in the market.

MARKET OPPORTUNITIES

Growth in Commercial and Industrial Infrastructure Development

An emerging opportunity within the North America air conditioning systems market is the robust growth in commercial and industrial infrastructure development. Across sectors such as healthcare, logistics, data centers, and advanced manufacturing, there is an increasing need for precision cooling solutions to maintain optimal operating conditions.

Data centers, in particular, represent a rapidly expanding segment requiring high-efficiency HVAC systems to manage heat generated by servers and computing hardware. As reported by the Uptime Institute, North America accounts for over 40% of global data center investments , with hyperscale operators like Amazon Web Services, Microsoft Azure, and Google Cloud actively deploying advanced cooling technologies to enhance energy efficiency and reduce operational downtime.

Similarly, the healthcare sector is witnessing heightened demand for climate-controlled environments in hospitals, laboratories, and pharmaceutical storage facilities. As business investment in infrastructure continues to rise, air conditioning manufacturers are well-positioned to capitalize on this growth by offering tailored, high-performance cooling solutions for diverse commercial and industrial applications.

Increasing Adoption of Ductless Mini-Split Systems in Residential Applications

A significant opportunity gaining traction in the North America air conditioning systems market is the rising adoption of ductless mini-split systems in residential applications. Unlike traditional central air conditioning systems, mini-splits offer zoned cooling without the need for extensive ductwork, making them ideal for retrofitting older homes, multi-family dwellings, and energy-efficient housing developments. According to the Air-Conditioning, Heating & Refrigeration Institute, shipments of ductless mini-split systems in the U.S. grew by over 12% in 2023 , outpacing overall market growth.

This surge is driven by several factors, including improved system efficiency, flexible installation options, and better alignment with green building certifications such as LEED and ENERGY STAR.

State-level incentive programs have also played a crucial role in boosting consumer interest. For example, California’s Self-Generation Incentive Program offers rebates for homeowners who install high-efficiency mini-split units, encouraging wider adoption. With increasing urban density, rising energy costs, and a growing preference for personalized climate control, ductless mini-split systems are poised to become a mainstream solution, offering manufacturers a lucrative avenue for long-term market expansion.

MARKET CHALLENGES

Complexity in Refrigerant Transition and Supply Chain Constraints

A pressing challenge confronting the North America air conditioning systems market is the complexity involved in transitioning to next-generation refrigerants and managing ongoing supply chain constraints. The phasedown of hydrofluorocarbons (HFCs) under the AIM Act requires manufacturers to redesign existing systems to accommodate newer, low-global-warming-potential (GWP) alternatives such as hydrofluoroolefins (HFOs) and natural refrigerants. However, these substitutes often require modifications to compressors, lubricants, and safety protocols, increasing engineering and production costs.

According to the Air-Conditioning, Heating & Refrigeration Institute, the retooling of manufacturing lines to support HFO-compatible systems has led to delays in product launches and increased time-to-market, disrupting inventory cycles and customer fulfillment timelines. Moreover, the availability of trained technicians capable of handling new refrigerants remains limited, posing challenges for installation and post-sale servicing.

Simultaneously, supply chain bottlenecks—particularly in sourcing raw materials like copper, aluminum, and rare earth components—continue to affect production capacity. These combined pressures create operational uncertainties, forcing companies to navigate a complex regulatory and logistical environment while maintaining competitive pricing and service reliability.

Rising Electricity Demand and Grid Capacity Limitations

Another critical challenge facing the North America air conditioning systems market is the increasing strain on electricity grids during peak cooling seasons. As urban populations grow and climate change intensifies heatwaves, the demand for air conditioning surges, placing unprecedented pressure on power generation and distribution networks. According to the U.S. Energy Information Administration, electricity use for air conditioning in the residential and commercial sectors accounted for nearly 12% of total U.S. electricity consumption in 2023 , contributing to seasonal grid instability.

Several states, including California and Texas, have experienced rolling blackouts and emergency energy alerts during extreme heat events, prompting utilities to implement demand-response programs and peak-load management strategies.

To address this issue, regulators and utility providers are incentivizing the adoption of smart thermostats, time-of-use pricing, and grid-responsive HVAC systems that adjust cooling output based on real-time energy availability. However, achieving widespread consumer participation and technological integration remains a formidable hurdle.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type ,End-user and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Daikin Industries Ltd., Carrier Corporation, Mitsubishi, and Hitachi |

SEGMENTAL ANALYSIS

By Type Insights

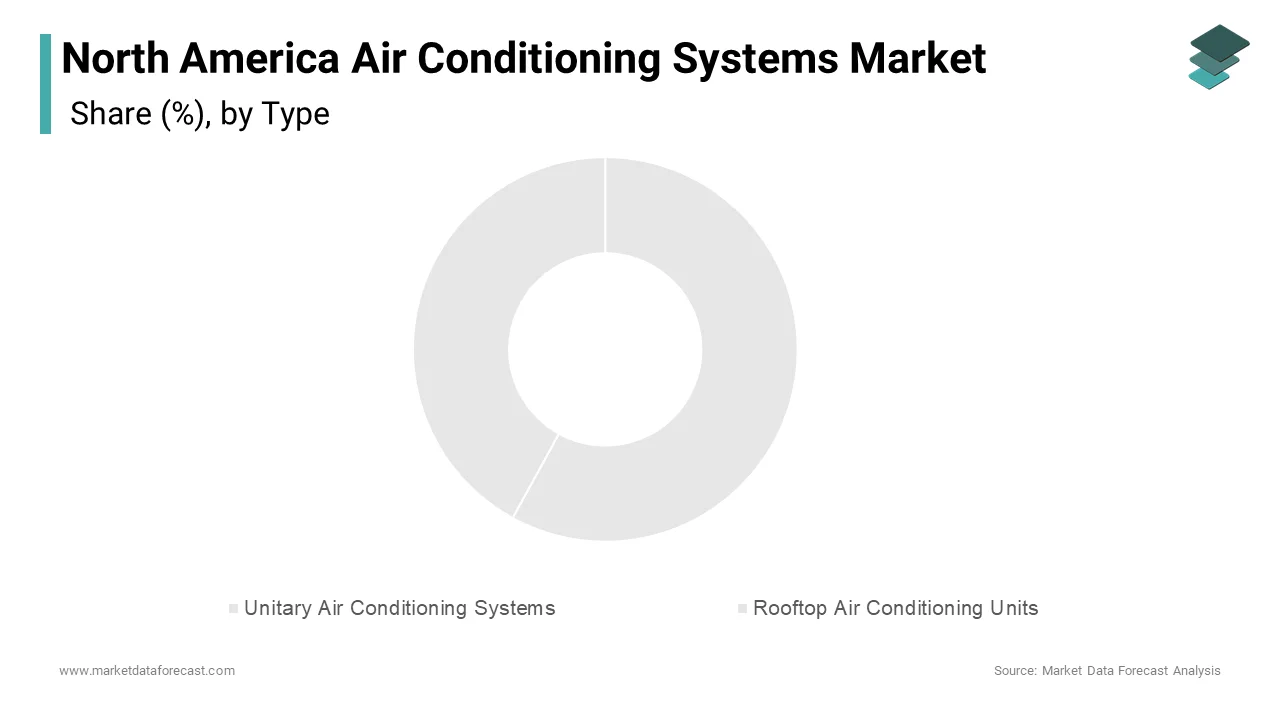

The Unitary AC systems account for the largest share at 58.3% in 2025. These systems are widely used across residential and small commercial applications due to their versatility, ease of installation, and cost-effectiveness.

The dominance of this segment is primarily driven by the high demand from single-family homes and mid-sized buildings , where ducted or ductless unitary systems offer an efficient and scalable cooling solution. This reflects a deep-rooted consumer preference for whole-house cooling rather than localized or window-based solutions.

Moreover, manufacturers have been aggressively enhancing unitary system efficiency through ENERGY STAR certifications and smart thermostat integrations. With continued urban expansion and rising disposable incomes, particularly in southern states like Florida and Texas, the unitary air conditioning systems segment remains firmly entrenched as the market leader.

The Rooftop air conditioning systems segment is currently the fastest-growing within the North America market , projected to expand at a CAGR of 6.9%. While smaller in overall size compared to unitary systems, rooftop units are gaining momentum due to increasing adoption in the commercial sector, especially among retail stores, restaurants, and office complexes.

One key driver behind this growth is the increasing construction of single-story commercial buildings that favor rooftop HVAC installations for space optimization and aesthetic appeal.

Apart from these, technological advancements such as variable refrigerant flow (VRF) integration and smart zone control capabilities have made modern rooftop units more energy-efficient and adaptable to dynamic occupancy patterns. The American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) noted that rooftop systems incorporating smart controls saw a 15% improvement in energy performance in recent field trials. As businesses prioritize operational efficiency and sustainability, rooftop air conditioning systems are expected to maintain robust growth across North America.

By Technology Insights

As of 2025, Non-Inverter air conditioning systems continue to be held the biggest market share at 63.3%. Despite growing awareness around energy efficiency, non-inverter models remain dominant due to their lower upfront costs and widespread use in traditional residential and commercial settings.

A primary factor contributing to this segment’s leadership is the strong presence of legacy HVAC infrastructure across older housing stock and institutional buildings, particularly in regions with moderate cooling demands. According to the U.S. Department of Housing and Urban Development, nearly 45% of American homes were built before 1980 , many of which still operate on conventional fixed-speed AC units that do not incorporate inverter technology.

Also, non-inverter systems are preferred in budget-sensitive markets , including multi-family rental units and secondary cities, where initial affordability outweighs long-term energy savings considerations. While inverter technology is gaining traction, the existing installed base, coupled with price sensitivity in certain consumer segments, ensures that non-inverter systems will remain a significant portion of the market in the near term.

The Inverter air conditioning systems segment is experiencing the highest growth rate, expanding at a CAGR of 9.1%. This surge is fueled by growing consumer awareness about energy conservation, rising utility costs, and government incentives promoting high-efficiency appliances.

One of the major factors driving adoption is the superior energy efficiency offered by inverter-driven compressors, which modulate speed based on cooling demand rather than cycling on and off like traditional units. According to the U.S. Department of Energy, inverter AC systems can reduce electricity consumption by up to 30–50% compared to standard models , significantly lowering monthly energy bills.

Furthermore, the rise of green building standards such as LEED and ENERGY STAR has encouraged developers to integrate inverter-based HVAC systems into new constructions. With continued advancements in smart connectivity and zoning control, inverter air conditioning systems are poised to dominate future product innovation cycles, reinforcing their position as the fastest-growing segment in the North America market.

By End-use Insights

The residential end-use segment commanded the North America air conditioning systems market at 55.4% in 2025. This dominance stems from the widespread ownership of home cooling systems and the ongoing replacement cycle of aging equipment.

A key driver of this segment is the deep cultural and climatic necessity for indoor cooling in many parts of the United States and Canada , particularly during summer months. According to the U.S. Energy Information Administration, nearly 90% of American households own at least one form of air conditioning , with central AC being the most prevalent type in newly constructed homes.

Also, rising disposable incomes and increased emphasis on indoor comfort have led to higher penetration rates even in traditionally cooler regions.

Moreover, retrofitting and renovation activities, especially in the southern and southwestern U.S., are fueling demand for ductless mini-split and high-efficiency systems , allowing homeowners to upgrade without extensive structural modifications.

The industrial air conditioning systems segment is emerging as the fastest-growing part of the North America market, projected to grow at a CAGR of 7.3%. This growth is attributed to the increasing need for precise temperature and humidity control in manufacturing, pharmaceuticals, data centers, and food processing facilities.

One of the main drivers behind this trend is the expansion of advanced industrial infrastructure , particularly in automation-heavy sectors requiring stable environmental conditions to ensure operational efficiency. Additionally, data center investments are surging , with hyperscale operators deploying large-scale cooling systems to manage heat generated by AI servers and cloud computing hardware.

Manufacturers are also adopting Industry 4.0 practices that rely on precision sensors and robotics , which require stable thermal conditions to function optimally. As industrial modernization accelerates, the demand for high-performance air conditioning systems tailored to these environments is set to grow rapidly.

COUNTRY LEVEL ANALYSIS

The United States held the largest share of the North America air conditioning systems market in 2025. This overwhelming dominance is driven by high household ownership, extreme regional weather variability, and a mature HVAC industry supported by leading manufacturers and distributors.

A key factor contributing to this leadership is the widespread integration of air conditioning into residential and commercial infrastructure, particularly in southern states where temperatures frequently exceed 100°F.

Additionally, urbanization and real estate development have sustained steady demand for both new installations and retrofitting projects.

Technological innovation is another major contributor, with companies like Carrier, Trane, and Lennox investing heavily in smart, energy-efficient systems. Government-backed initiatives such as ENERGY STAR certification and state-level rebate programs further encourage consumers to upgrade aging units.

Canada is positioning it as a growing but secondary market compared to the United States. Though historically less reliant on cooling due to its temperate climate, Canada is witnessing increased demand due to shifting weather patterns and rising urban density.

One of the primary growth drivers is the increased frequency of heatwaves in major cities like Toronto, Montreal, and Vancouver , prompting homeowners and municipalities to invest in residential and commercial cooling solutions. Moreover, urban apartment living is on the rise, especially in metropolitan areas, creating demand for ductless mini-split systems that can be easily retrofitted into multi-unit buildings.

Government support through energy efficiency rebates and municipal building code updates has also played a role in stimulating market growth. With climate change altering seasonal norms, Canada's air conditioning market is expected to see continued expansion in the coming years.

The Rest of North America is showing signs of gradual expansion due to economic development and infrastructure modernization efforts.

In Mexico, for instance, rising middle-class incomes and rapid urbanization have led to increased adoption of residential and commercial air conditioning systems , particularly in warmer regions such as Baja California and Yucatán.

However, market penetration remains uneven due to income disparities and limited access to reliable electricity grids in rural areas.

Despite these challenges, international HVAC brands are expanding their presence through local partnerships and distribution networks, aiming to capture growing demand in commercial and industrial sectors. As economic conditions improve and electrification expands, the Rest of North America could evolve into a more substantial contributor to the broader regional air conditioning market.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the north america air conditioning systems market include Ingersoll Rand, Daikin Industries Ltd., Carrier Corporation, Mitsubishi, and Hitachi, among others.

The competition within the North America air conditioning systems market is highly dynamic, shaped by the presence of established multinational corporations and a growing number of regional and niche players. Major global brands such as Carrier, Trane, and Lennox dominate due to their extensive product portfolios, robust R&D capabilities, and strong dealer networks. These firms continuously innovate to stay ahead, introducing smart and energy-efficient systems that cater to evolving consumer preferences and regulatory demands.

Simultaneously, smaller manufacturers and private-label brands are gaining traction by offering competitively priced alternatives, particularly in the residential and retrofit markets. This intensifies pressure on pricing and forces larger players to differentiate themselves through superior performance, branding, and post-installation services. Additionally, shifting climatic conditions and rising urbanization are expanding the scope of cooling needs, prompting companies to diversify into new application areas such as data centers and industrial facilities.

Competition is further influenced by supply chain resilience, access to skilled labor, and the ability to adapt to refrigerant phase-down regulations. Companies that can seamlessly integrate sustainability, digital connectivity, and customer-centric support models are better positioned to capture long-term market share in this rapidly evolving industry.

Top Players in the Market

Carrier Global Corporation

Carrier is a leading force in the North America air conditioning systems market, known for its innovation and broad product portfolio spanning residential, commercial, and industrial cooling solutions. As a global HVAC brand, Carrier plays a pivotal role in shaping industry standards through its focus on energy efficiency, smart technology integration, and sustainable refrigerant transitions. The company’s commitment to research and development has enabled it to introduce next-generation systems that align with evolving environmental regulations and consumer expectations.

Trane Technologies plc

Trane Technologies is a major contributor to the North American air conditioning landscape, offering advanced climate control systems designed for both comfort and efficiency. With a strong presence in commercial and industrial sectors, the company leverages its expertise in building automation and high-performance HVAC equipment to meet diverse customer needs. Trane’s strategic emphasis on sustainability, digitalization, and long-term service partnerships positions it as a key player in driving market growth and technological advancement.

Lennox International Inc.

Lennox International holds a significant position in the North America air conditioning systems market by delivering reliable and innovative heating and cooling products tailored to residential and light commercial applications. Known for its durable, high-efficiency units, Lennox has built a reputation for quality and customer-centric design. The company actively supports energy conservation initiatives and collaborates with contractors and distributors to ensure widespread availability and after-sales support, reinforcing its competitive edge in the regional market.

Top Strategies Used by Key Players

Product Innovation and Technology Integration

Leading companies are heavily investing in R&D to develop technologically advanced air conditioning systems featuring smart controls, variable-speed compressors, and improved energy efficiency. These innovations aim to meet consumer demand for comfort, cost savings, and environmental responsibility while ensuring compliance with evolving regulatory standards.

Expansion of Sustainable Product Portfolios

With increasing emphasis on climate action, manufacturers are transitioning toward low-global-warming-potential (GWP) refrigerants and eco-friendly manufacturing processes. Companies are redesigning their product lines to align with green certifications and government mandates, reinforcing their commitment to sustainability.

Strengthening Distribution and Service Networks

To enhance market reach and customer satisfaction, key players are expanding their distribution channels and service infrastructure. This includes forging partnerships with HVAC contractors, leveraging digital sales platforms, and improving after-sales service capabilities to ensure long-term customer retention and brand loyalty.

RECENT HAPPENINGS IN THE MARKET

In January 2025, Carrier launched a new line of ultra-low GWP refrigerant-based residential air conditioners, designed to comply with upcoming EPA regulations while maintaining high efficiency and performance standards.

In March 2025, Trane Technologies introduced an AI-powered building management system integrated with its rooftop AC units, enabling real-time energy optimization and predictive maintenance for commercial clients.

In July 2025, Lennox International expanded its partnership network with independent HVAC contractors across the southern United States to improve installation and service accessibility for homeowners.

In October 2025, Daikin Industries acquired a minority stake in a U.S.-based smart thermostat startup to enhance its connected home ecosystem and strengthen its foothold in the residential cooling segment.

In December 2025, Mitsubishi Electric opened a new regional training center in Texas focused on equipping technicians with specialized knowledge on ductless mini-split installations and refrigerant handling procedures.

MARKET SEGMENTATION

This north america air conditioning systems market research report has been segmented and sub-segmented based on product type, end-user, and region.

By Type

- Unitary Air Conditioning Systems

- Rooftop Air Conditioning Units

By Technology

- Non-Inverter Air Conditioning Systems

- Inverter Air Conditioning Systems

By End-user

-

Residential Air Conditioning Systems

-

Industrial Air Conditioning System

By Country

- The U.S.

- Canada

- Rest of North America

Frequently Asked Questions

Which countries dominate the North America market?

The United States holds the largest share of the market, followed by Canada and Mexico, driven by a combination of extreme weather patterns and high HVAC system adoption rates.

What are the major challenges in the North American AC systems market?

Key challenges include high upfront costs of energy-efficient models, refrigerant transition compliance, skilled labor shortages, and fluctuating raw material prices.

What are the latest technological trends in in the North American AC systems market ?

Key trends include smart HVAC systems with IoT integration, use of eco-friendly refrigerants, solar-powered AC units, and AI-based climate control systems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com