North America Automated Breast Ultrasound Systems (ABUS) Market Size, Share, Trends & Growth Forecast Report By Product (Automated Breast Volume Scanner, Automated Breast Ultrasound (ABUS)), End Use (Hospital, Diagnostics Imaging Laboratories, Others), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis, 2026 to 2034

North America Automated Breast Ultrasound Systems (ABUS) Market Size

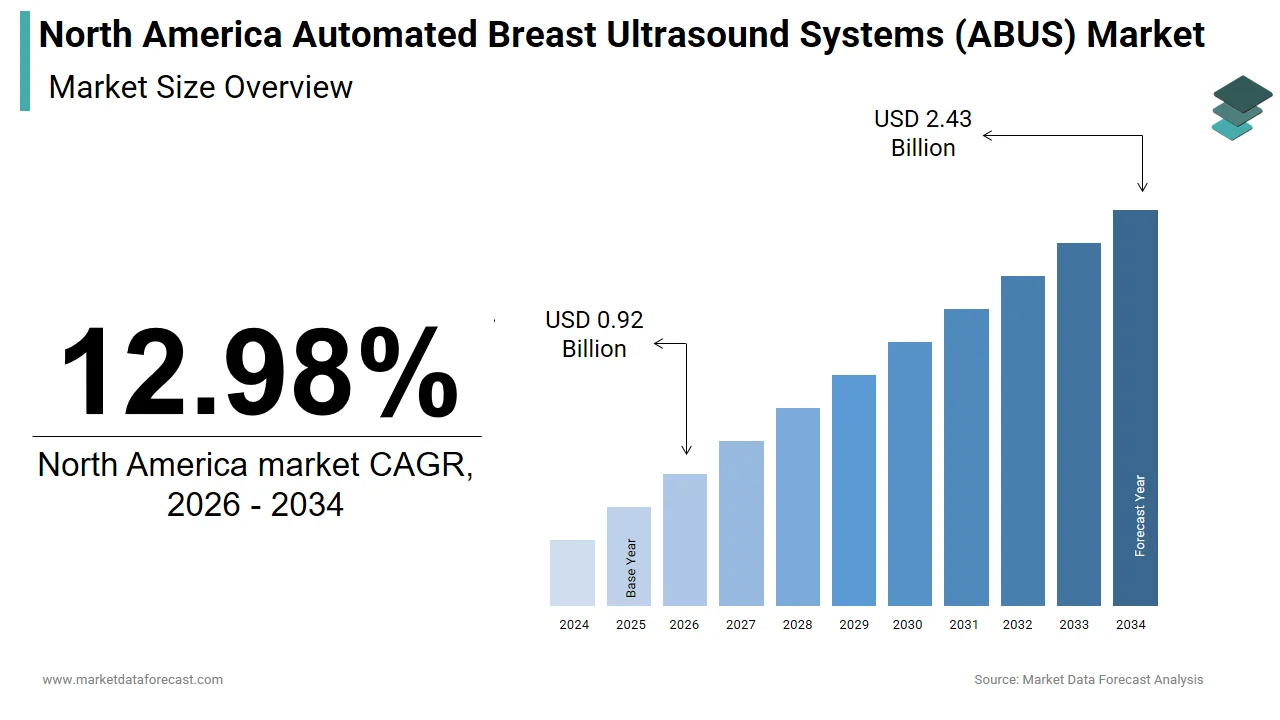

The North America automated breast ultrasound systems market was valued at USD 0.81 billion in 2025, is estimated to reach USD 0.92 billion in 2026, and is projected to reach USD 2.43 billion by 2034, growing at a CAGR of 12.98% from 2026 to 2034.

The automated breast ultrasound systems (ABUS) are advanced imaging platforms designed to deliver standardized, reproducible, and high-resolution ultrasound scans of the breast without reliance on operator-dependent techniques. These systems are increasingly integrated into diagnostic workflows for women with dense breast tissue, where mammography sensitivity declines significantly. As per the American College of Radiology, over 40% of women in the United States have heterogeneously or extremely dense breasts, a condition that affects more than 40 million individuals nationwide. This physiological factor reduces the effectiveness of traditional mammography, prompting state-mandated breast density notification laws in 38 U.S. states as of 2023, which require clinicians to inform patients of their tissue composition and recommend supplemental screening. The U.S. Food and Drug Administration has cleared multiple ABUS platforms, including those by GE Healthcare and Koios Medical, for use as adjunctive tools in breast cancer detection.

MARKET DRIVERS

Rising Prevalence of Dense Breast Tissue and Associated Diagnostic Limitations of Mammography

The high incidence of dense breast tissue among women, which significantly compromises the diagnostic accuracy of conventional mammography, is driving the growth of the North America automated breast ultrasound systems (ABUS) market. According to the Centers for Disease Control and Prevention, mammography sensitivity drops from approximately 84% in women with fatty breasts to as low as 48% in those with extremely dense tissue, creating a substantial diagnostic gap. The University of California, San Francisco Breast Imaging Division found that in a 2022 multicenter study, supplemental ABUS screening detected an additional 3.5 cancers per 1,000 women with dense breasts who had negative mammograms. This enhanced detection capability is particularly critical given that over 50% of women aged 40–74 in the U.S. fall into the dense breast category, as reported by the National Institutes of Health. Furthermore, the passage of breast density inform laws in 38 states by 2023 has catalyzed patient awareness and demand for alternative imaging methods. The Avon Foundation for Women notes that post-notification, 68% of women sought additional screening beyond mammography, with ABUS emerging as a preferred non-invasive option.

Expansion of Breast Cancer Screening Programs and Health Policy Initiatives

Government-backed and institutionally led breast cancer screening initiatives are significantly accelerating the growth of the North America automated breast ultrasound systems (ABUS) market. The U.S. Department of Health and Human Services’ Healthy People 2030 initiative includes a specific objective to increase the proportion of women aged 50–74 who receive regular breast cancer screening, while also emphasizing the need for risk-stratified approaches. In alignment, the Centers for Disease Control and Prevention administers the National Breast and Cervical Cancer Early Detection Program (NBCCEDP), which expanded coverage to include supplemental ultrasound for underserved women with dense breasts in 17 states by 2023. This program serves over 150,000 women annually, many of whom lack access to an MRI due to cost or availability. Additionally, the Patient Protection and Affordable Care Act mandates coverage for FDA-approved screening technologies without patient cost-sharing when recommended by professional guidelines. The American Cancer Society estimates that 72% of private insurance plans now reimburse ABUS when medically indicated, reducing financial barriers. In Canada, provincial health authorities such as Ontario Health have initiated pilot programs integrating ABUS into regional screening frameworks, particularly for high-risk cohorts.

MARKET RESTRAINTS

Limited Reimbursement Coverage for Automated Breast Ultrasound Procedures

The expansion of automated breast ultrasound systems is hindered by inconsistent and fragmented reimbursement policies across public and private payers in North America. As of 2023, the Centers for Medicare & Medicaid Services does not provide a dedicated Current Procedural Terminology (CPT) code for ABUS, forcing providers to bill under general diagnostic ultrasound codes, which often results in claim denials or reduced payments. Private insurers exhibit variable policies; a 2023 analysis by the Conference of Women’s Health Insurance Directors found that 41% of major insurers required prior authorization for ABUS, with approval rates averaging 58%. This administrative burden discourages widespread adoption, especially in smaller imaging centers. In Canada, while provincial health systems cover mammography universally, ABUS remains largely excluded from public funding, limiting its use to research or self-pay settings.

High Capital Cost and Infrastructure Requirements for ABUS Implementation

The financial and operational burden associated with acquiring and deploying the system is hindering the growth of the North America automated breast ultrasound systems (ABUS) market. In addition to the initial investment, facilities must allocate dedicated space, ensure electromagnetic compatibility, and upgrade IT infrastructure to handle large 3D imaging datasets, which can exceed 1 gigabyte per scan. According to the Society for Imaging Informatics in Medicine, integrating ABUS into existing Picture Archiving and Communication Systems (PACS) requires middleware customization, increasing deployment complexity and cost. Training radiologic technologists to operate ABUS platforms also demands time and resources; the American Registry of Radiologic Technologists indicates that certification in breast ultrasound requires a minimum of 40 supervised procedures, which smaller centers may struggle to fulfill. Furthermore, maintenance contracts and software licensing renewals add recurring expenses that strain operational budgets.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in ABUS Image Analysis and Interpretation

The integration of artificial intelligence with automated breast ultrasound systems is unlocking transformative potential in diagnostic accuracy, workflow efficiency, and accessibility is leveraging the growth of the North America automated breast ultrasound systems (ABUS) market. AI-powered algorithms are being developed to analyze volumetric ABUS datasets, identifying suspicious lesions, characterizing masses, and prioritizing cases for radiologist review. As per the Radiological Society of North America, AI-assisted interpretation can reduce reading time by up to 30% while maintaining or improving sensitivity. Companies such as Koios Medical and Aidoc have launched FDA-cleared AI platforms that integrate directly with ABUS workstations, offering real-time decision support. The U.S. Food and Drug Administration’s Digital Health Center of Excellence has fast-tracked several AI-ABUS combinations under its Pre-Cert program, accelerating clinical availability. Furthermore, AI can standardize interpretation across varying expertise levels, addressing the shortage of subspecialized breast imagers, particularly in rural areas.

Growing Emphasis on Personalized and Risk-Based Breast Cancer Screening

The shift from population-wide screening to individualized, risk-adapted breast cancer detection strategies is also expected to promote the growth of the North America automated breast ultrasound systems (ABUS) market. Traditional mammography follows a one-size-fits-all approach, but emerging guidelines from the American College of Medical Genetics and Genomics advocate for risk stratification based on genetic predisposition, breast density, family history, and lifestyle factors. The National Comprehensive Cancer Network recommends annual supplemental screening for high-risk patients, a category that includes over 2.8 million BRCA carriers and survivors of childhood cancer in North America. ABUS is particularly suited for longitudinal monitoring due to its reproducibility and lack of cumulative radiation exposure. The Breast Cancer Surveillance Consortium found that women undergoing ABUS screening had a 28% higher rate of early-stage cancer detection compared to those receiving mammography alone. Moreover, digital health platforms are now incorporating ABUS into personalized screening pathways, which leverage electronic health records and genetic data to recommend tailored imaging schedules.

MARKET CHALLENGES

Variability in Clinical Workflow Integration and Standardization of Protocols

The lack of standardized protocols for patient positioning, scanning parameters, and image interpretation across clinical settings is quietly limiting the growth of the North America automated breast ultrasound systems (ABUS) market. While ABUS eliminates operator dependency in data acquisition, variations in patient preparation, transducer calibration, and table alignment can still affect image quality and diagnostic consistency. The Society of Breast Imaging notes that 34% of ABUS studies performed in community centers in 2023 required repeat scans due to suboptimal positioning, increasing patient wait times, and operational inefficiencies. Unlike mammography, which follows tightly regulated ACR Mammography Accreditation Program guidelines, ABUS lacks uniform national standards for acquisition and reporting, leading to discrepancies in lesion classification and follow-up recommendations. Additionally, the integration of ABUS into radiology workflows often disrupts existing scheduling systems, as each scan takes 15–20 minutes, compared to 5–7 minutes for mammography.

Limited Long-Term Clinical Outcome Data and Adoption Resistance Among Referring Physicians

The primary care providers and surgeons are due to the scarcity of long-term outcome studies demonstrating a reduction in breast cancer mortality. While ABUS has been shown to increase cancer detection rates, the impact on overall survival, overdiagnosis, and false-positive follow-ups remains inadequately documented in large-scale, longitudinal trials. The U.S. Preventive Services Task Force emphasizes that screening technologies must demonstrate mortality benefit to be widely endorsed, a threshold ABUS has not yet met. A 2023 review by the Dartmouth Institute for Health Policy found that only three prospective cohort studies tracking ABUS outcomes beyond five years exist, with none conducted in a population-based screening context. This evidence gap fuels skepticism among clinicians who are cautious about adopting technologies that may lead to unnecessary biopsies or patient anxiety. Additionally, radiologists face challenges in communicating ABUS findings to non-specialists, as volumetric data is less intuitive than 2D mammograms.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, End-use, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | GE HealthCare, Koninklijke Philips N.V., Siemens Healthcare Private Limited, Canon Medical Systems Corporation, TELEMED Medical Systems srl, Hologic, Inc., SuperSonic Imagine, Lunit Inc., and Delphinus Medical Technologies, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The Automated Breast Volume Scanner (ABVS) segment dominated the North America automated breast ultrasound systems market share in 2025 with its superior imaging capabilities, regulatory acceptance, and integration into structured breast screening protocols. ABVS technology, pioneered by systems such as GE Healthcare’s Invenia ABUS, provides full-field, three-dimensional volumetric imaging of the entire breast with high spatial resolution by enabling radiologists to navigate through tissue layers and assess lesion morphology in multiple planes. The American College of Radiology Imaging Network conducted a multicenter trial demonstrating that ABVS improves cancer detection rates by 35% in women with dense breasts compared to mammography alone, a finding that has influenced clinical adoption. Furthermore, the U.S. Food and Drug Administration has cleared ABVS platforms for use as a supplemental screening tool, reinforcing its legitimacy in diagnostic workflows. The National Cancer Institute reports that over 40 million women in the U.S. have dense breast tissue, a population for which ABVS is particularly effective.

The Automated Breast Ultrasound (ABUS) segment is likely to grow with an expected CAGR of 11.2% from 2026 to 2034, with the rising demand for cost-effective, compact, and operationally flexible imaging solutions in community clinics, mobile screening units, and rural healthcare settings. Unlike ABVS, which requires dedicated rooms and specialized tables, newer ABUS platforms employ semi-automated or robotic-assisted transducers that can be integrated into existing ultrasound systems, significantly lowering capital and spatial requirements. The U.S. Department of Health and Human Services reports that 77% of counties classified as rural lack access to advanced breast imaging, creating a critical gap that simplified ABUS systems are beginning to fill. The Centers for Disease Control and Prevention’s National Breast and Cervical Cancer Early Detection Program has funded pilot deployments of portable ABUS units in 12 states since 2022, citing their ease of use and rapid deployment. Manufacturers such as Koios Medical and Medison have introduced AI-enhanced ABUS platforms that provide real-time lesion assessment, further enhancing diagnostic efficiency without requiring volumetric reconstruction.

By End Use Insights

The hospitals segment was the largest by occupying 59.3% of the North America automated breast ultrasound systems market share in 2024. Hospitals, particularly academic medical centers and integrated health systems, possess the infrastructure, funding, and specialist workforce required to implement advanced imaging technologies like automated breast ultrasound. The American Hospital Association reports that over 6,000 hospitals in the U.S. offer diagnostic imaging services, with 82% of those providing dedicated breast health programs. These institutions are at the forefront of adopting risk-based screening protocols, where ABUS is integrated into pathways for high-risk and dense-breasted patients. The National Comprehensive Cancer Network guidelines recommend supplemental imaging for such populations, a directive that hospitals are uniquely positioned to execute. The U.S. Centers for Medicare & Medicaid Services reimburses ABUS procedures more readily in hospital outpatient departments than in freestanding clinics, reducing financial risk. The University of Pennsylvania Health System reported in 2023 that ABUS adoption in its network led to a 31% increase in early-stage cancer detection among dense-breasted patients.

The diagnostics imaging laboratories segment is lucratively to witness a CAGR of 10.8% from 2026 to 2034 with the increasing decentralization of breast cancer screening and the expansion of specialized, outpatient imaging networks that prioritize efficiency, patient convenience, and cost containment. Unlike hospitals, diagnostic imaging labs focus exclusively on imaging services, allowing them to optimize workflows, adopt cutting-edge technology faster, and achieve higher patient throughput. According to the American College of Radiology, over 1,200 imaging centers in the U.S. have achieved Breast Imaging Center of Excellence accreditation, a status that increasingly requires the availability of supplemental screening modalities like ABUS. These labs are strategically positioned in suburban and urban areas, improving access for women seeking timely follow-up after abnormal mammograms. The Patient Access and Affordability Act of 2022 incentivized outpatient imaging by capping patient out-of-pocket costs for diagnostic procedures, boosting demand for services in independent labs.

COUNTRY-LEVEL ANALYSIS

United States Automated Breast Ultrasound Systems (ABUS) Market Insights

The United States was the top performer in the North America automated breast ultrasound systems market with 92.3% of the share in 2024. The country performs over 38 million mammograms annually, as reported by the Centers for Disease Control and Prevention, creating a vast foundation for supplemental screening technologies. This legal framework has catalyzed demand for ABUS, particularly in states like California, New York, and Texas, where large populations and progressive health policies converge. The U.S. Food and Drug Administration has cleared multiple ABUS platforms, including GE Healthcare’s Invenia system, which is installed in over 1,500 medical facilities nationwide. Academic institutions such as MD Anderson Cancer Center and Mayo Clinic have integrated ABUS into high-risk screening programs, setting clinical benchmarks.

Canada Automated Breast Ultrasound Systems (ABUS) Market Insights

Canada automated breast ultrasound systems market held 8.1% of the share in 2024. The country’s universal healthcare system, administered provincially, prioritizes cost-effective and evidence-based technologies, which has slowed the widespread integration of ABUS despite its clinical benefits. However, provinces such as Ontario, British Columbia, and Quebec have initiated pilot programs to evaluate ABUS in high-risk populations, particularly women with dense breasts or genetic predispositions.

COMPETITIVE LANDSCAPE

The competitive landscape in the North America automated breast ultrasound systems market is characterized by a blend of technological innovation, clinical validation, and strategic positioning. While a few established players dominate through product maturity and brand recognition, the market remains dynamic due to the evolving nature of breast cancer screening and the increasing demand for precision diagnostics. Competition is not solely based on hardware performance but extends to software intelligence, ease of integration, and support for clinical decision-making. Companies differentiate themselves by offering end-to-end solutions that combine imaging hardware with AI-powered analytics, training, and workflow optimization. The emphasis is shifting from standalone devices to comprehensive diagnostic ecosystems that enhance radiologist productivity and patient outcomes. Smaller innovators are challenging incumbents by focusing on affordability, portability, and AI integration, particularly for community and rural settings. Regulatory endorsement, reimbursement alignment, and physician education play pivotal roles in shaping market penetration.

KEY MARKET PLAYERS

Noteworthy Companies dominating the North America automated breast ultrasound systems market profiled in the report are

GE HealthCare, Koninklijke Philips N.V., Siemens Healthcare Private Limited, Canon Medical Systems Corporation, TELEMED Medical Systems srl, Hologic, Inc., SuperSonic Imagine, Lunit Inc., and Delphinus Medical Technologies, Inc.

TOP LEADING PLAYERS IN THE MARKET

- GE Healthcare has established itself as a pioneer in automated breast ultrasound technology, primarily through its Invenia ABUS system, which set the benchmark for volumetric breast imaging. GE Healthcare’s global influence is amplified by its extensive distribution network and legacy in diagnostic imaging, allowing it to position ABUS as a complementary modality within comprehensive breast care pathways. Its focus on standardization, image quality, and workflow integration has made its systems a preferred choice in academic hospitals and large health systems across North America.

- Koios Medical has emerged as a transformative force by merging artificial intelligence with automated breast ultrasound to enhance diagnostic precision and reduce radiologist workload. The company’s AI-powered platform, Koios DS Breast, integrates seamlessly with ABUS systems to provide real-time lesion characterization, supporting faster and more consistent interpretations. Koios has carved a niche in improving the efficiency and accessibility of breast cancer screening by focusing on decision support rather than standalone imaging. Its technology is increasingly adopted in outpatient imaging centers and community hospitals seeking to elevate diagnostic confidence without requiring subspecialty expertise.

- Medison America has strengthened its position by advancing compact, cost-effective automated breast ultrasound solutions tailored for diverse clinical environments. The company emphasizes user-friendly design, portability, and integration with existing ultrasound platforms, making its systems accessible to smaller clinics and rural facilities. Medison’s commitment to innovation in transducer technology and imaging software has enabled broader deployment beyond academic centers. The company is expanding the reach of automated breast ultrasound into underserved and decentralized care settings, which is contributing to more equitable access across the healthcare spectrum.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the most impactful strategies employed by leading companies is the integration of artificial intelligence into ABUS platforms to enhance diagnostic accuracy and streamline radiologist workflows. This approach not only reduces interpretation time but also minimizes variability, particularly in settings with limited subspecialty expertise.

Another key strategy involves strategic partnerships with healthcare providers, radiology networks, and breast health advocacy groups to embed ABUS into standardized screening protocols. Companies are collaborating with hospitals and imaging centers to co-develop clinical pathways that incorporate ABUS for high-risk and dense-breasted populations, ensuring seamless integration into patient care workflows and reinforcing clinical legitimacy.

A third major strategy is the expansion of educational and training initiatives aimed at radiologists, technologists, and referring physicians. Manufacturers are building clinical confidence and addressing knowledge gaps that hinder adoption by offering certification programs, live demonstrations, and peer-reviewed case studies. These efforts are critical in overcoming resistance from providers unfamiliar with volumetric ultrasound interpretation and in aligning ABUS with evolving breast cancer screening guidelines.

RECENT MARKET DEVELOPMENTS

- In February 2024, GE Healthcare launched an upgraded version of its Invenia ABUS system with enhanced 3D rendering capabilities and improved patient positioning automation. This advancement is expected to streamline scanning procedures and improve image consistency across diverse clinical settings.

- In March 2024, Koios Medical announced a strategic collaboration with a leading U.S. radiology network to integrate its AI-powered decision support platform with existing ABUS systems by aiming to improve diagnostic accuracy and reduce interpretation variability.

- In January 2024, Medison America introduced a new portable automated breast ultrasound solution designed for outpatient clinics and mobile screening units, which is expanding access to underserved regions and reinforcing its focus on decentralized care.

- In May 2023, GE Healthcare partnered with a national breast health advocacy organization to fund educational programs for radiologists and primary care providers on the use of ABUS in dense breast screening by enhancing clinical adoption.

- In April 2024, Koios Medical received expanded FDA clearance for its AI algorithm to include real-time BI-RADS categorization within ABUS workflows, which is strengthening its position as a leader in intelligent breast imaging solutions.

MARKET SEGMENTATION

This North America automated breast ultrasound systems market research report is segmented and sub-segmented into the following categories.

By Product

- Automated Breast Volume Scanner

- Automated Breast Ultrasound (ABUS)

By End Use

- Hospital

- Diagnostics Imaging Laboratories

- Others

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What drives growth in the North America Automated Breast Ultrasound Systems (ABUS) Market?

Growth is driven by high breast cancer rates, advanced healthcare infrastructure, favorable FDA approvals, and increasing awareness of the benefits of supplemental dense breast screening.

2. Which countries lead the North America ABUS Market?

The United States is the dominant market, backed by FDA approvals, a focus on early detection, and extensive adoption by hospitals and diagnostic centers. Canada is steadily expanding ABUS installations as well.

3. Who are the key players in the North America Automated Breast Ultrasound Systems (ABUS) Market?

Major players include GE HealthCare, Siemens Healthineers, Hitachi Ltd., Koninklijke Philips N.V., Canon Medical Systems, Hologic, SonoCine Inc., and iSono Health.

4. What are the main applications of ABUS in North America?

Primary applications include breast cancer screening, detection in women with dense breast tissue, adjunct to mammography, and clinical decision support for radiologists.

5. How is AI transforming the North America ABUS Market?

AI-driven ABUS systems offer improved image accuracy, faster diagnostics, and workflow efficiencies, with AI expected to account for over 35% of market revenue by 2030.

6. What benefits does ABUS provide over traditional mammography in the North America market?

ABUS provides enhanced sensitivity in dense breast tissue, is non-invasive and radiation-free, and can identify small or hidden tumors that mammograms may miss.

7. What challenges face the North America ABUS Market?

Key challenges include high upfront equipment costs, variability in operator training, integration with existing PACS/HIS, and reimbursement restrictions for some procedures.

8. How are reimbursement policies evolving for ABUS in North America?

Reimbursement coverage is expanding, especially for high-risk populations, enabling broader clinical adoption and improving patient access to ABUS screening.

9. Which end users drive ABUS demand in North America?

Hospitals are the largest end users, followed by diagnostic imaging centers and specialized breast health clinics.

10. How is portable and point-of-care ABUS impacting the North America market?

Growing demand for portable and mobile ABUS devices is increasing accessibility in rural and underserved regions and supporting decentralized breast screening programs.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com