- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

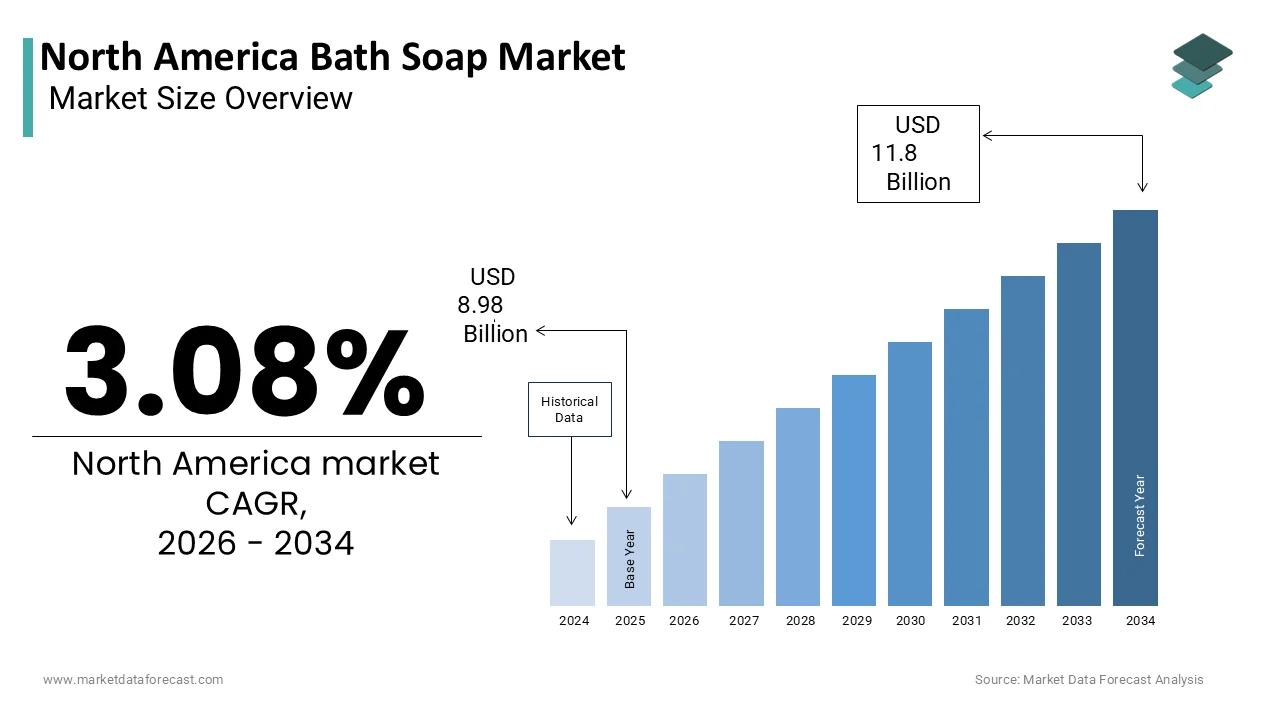

Market Size, 2025

$8.98 BnMarket Estimate, 2026

$9.25 BnMarket Forecast, 2034

$11.80 BnCAGR, 2026–2034

3.08%North America Bath Soap Market Size

The North America bath soap market size was valued at USD 8.98 billion in 2025 and is anticipated to reach USD 9.25 billion in 2026 to USD 11.8 billion by 2034, growing at a CAGR of 3.08% during the forecast period from 2026 to 2034.

The solid and semi-solid personal cleansing products are designed for daily hygiene, including bar soaps, syndet bars, and specialty formulations tailored to skin types and wellness needs. According to the American Academy of Dermatology, over 78% of U.S. adults report daily full-body washing, with bar soap remaining the preferred format for 34% of respondents, particularly among older demographics and in rural regions. Additionally, the National Institute of Environmental Health Sciences notes increasing consumer scrutiny over synthetic additives, driving demand for formulations free from parabens, sulfates, and artificial fragrances.

MARKET DRIVERS

Rising Consumer Emphasis on Skin Health and Dermatological Wellness

The growing consumer focus on skin integrity and dermatological care, transforming soap from a commodity into a functional skincare product is accelerating the growth of the North American bath soap market. Increasing awareness of conditions such as eczema, xerosis, and barrier dysfunction has prompted individuals to seek out soaps with clinically validated benefits. According to the American Academy of Dermatology, approximately 16.5 million adults in the United States suffer from eczema, with 90% reporting that their choice of cleanser directly impacts flare frequency. Brands such as Cetaphil, Dove, and Vanicream have capitalized on this trend by aligning with dermatologists and obtaining endorsements from professional medical associations. The National Eczema Association reports that over 12,000 products have been formally accepted into its Seal of Acceptance program since 2010, with bar soaps comprising 28% of certified items in 2023.

Expansion of Natural, Organic, and Sustainable Product Offerings

The integration of eco-conscious values into personal care routines with sustainability and clean labeling is levelling up the growth of the North American bath soap market. Consumers are increasingly avoiding synthetic surfactants, petroleum-derived additives, and non-recyclable packaging, favoring products with plant-based ingredients and minimal environmental impact. The U.S. Department of Agriculture’s National Organic Program has certified over 1,800 personal care products with organic claims, including numerous artisanal and mass-market bar soaps. Additionally, the Environmental Working Group’s Skin Deep database now catalogs over 25,000 personal care items with ingredient safety ratings, influencing consumer trust—nearly 68% of surveyed shoppers in a 2023 NielsenIQ study stated they cross-referenced product scores before purchasing. Independent brands such as Dr. Bronner’s and ethical multinational initiatives like Unilever’s “Clean Future” program have driven innovation in biodegradable formulas and plastic-free packaging.

MARKET RESTRAINTS

Declining Preference for Traditional Bar Soaps Among Younger Demographics

The younger consumers such as Millennials and Generation Z, who exhibit a marked preference for liquid body washes and shower gels is restraining the growth of the North American bath soap market. According to a 2023 generational consumption survey conducted by the NPD Group, only 22% of consumers aged 18–34 regularly use bar soap, compared to 54% of those over 55. This shift is driven by perceptions of bar soap as outdated, less hygienic, or incompatible with modern bathroom aesthetics. The U.S. Food and Drug Administration notes that while no confirmed cases of pathogen transmission via personal bar soap have been documented, consumer skepticism remains high, particularly in multi-user households. Additionally, the sensory experience of liquid washes foaming action, fragrance diffusion, and pump dispensers is often perceived as more luxurious and indulgent. Social media influencers and beauty content creators predominantly feature liquid formulations in skincare routines, further marginalizing bar soap in digital discourse. Major retailers such as Target and Sephora have reduced bar soap shelf space by up to 30% in favor of premium body washes, reflecting evolving merchandising strategies.

Regulatory and Ingredient Safety Scrutiny on Synthetic Additives

The increasingly constrained by rigorous regulatory oversight and consumer skepticism regarding synthetic ingredients commonly used in cleansing formulations is inhibiting the growth of the North American bath soap market. Compounds such as triclosan, sodium lauryl sulfate (SLS), and synthetic fragrances have come under scrutiny for potential dermal irritation and endocrine disruption. According to the U.S. Food and Drug Administration, triclosan was banned from over-the-counter antiseptic soaps in 2016 due to insufficient evidence of efficacy and concerns about antimicrobial resistance. The Environmental Working Group’s analysis of 1,200 bar soaps revealed that 37% contained ingredients flagged as moderate to high hazard, including formaldehyde-releasing preservatives and synthetic musks. This has led to costly reformulations and supply chain adjustments for manufacturers aiming to meet clean beauty standards. The U.S. Congress introduced the Personal Care Products Safety Act in 2023, proposing stricter premarket ingredient reviews, which could delay product launches and increase compliance burdens.

MARKET OPPORTUNITIES

Growth of Artisanal and Locally Sourced Handcrafted Soaps

The growing consumer demand for authenticity, craftsmanship, and community-based production is likely to pose new opportunities for the growth of the North American bath soap market. Small-batch soap makers utilizing cold-process methods, plant-based oils, and locally sourced botanicals have gained traction in farmers' markets, boutique retailers, and e-commerce platforms. Platforms like Etsy recorded a 68% increase in handmade soap sales from U.S.-based sellers in 2023, with premium pricing justified by perceived purity and ethical sourcing. Additionally, state-level craft certification programs, such as Vermont’s “Made in Vermont” label, enhance consumer trust. The rise of “slow beauty” and hyper-localism in personal care has enabled these brands to differentiate themselves from industrial manufacturers, creating niche markets in urban wellness communities and eco-conscious suburbs.

Integration of Functional Ingredients with Skincare and Aromatherapy Benefits

The personal care with wellness has unlocked new potential for bath soaps infused with bioactive and sensorial ingredients that extend beyond cleansing. Consumers increasingly seek multifunctional products that deliver hydration, anti-aging benefits, or mental well-being through aromatherapy. According to the Global Wellness Institute, the U.S. wellness economy was valued at $1.8 trillion in 2023, with personal care contributing a significant share. This has spurred innovation in soaps containing niacinamide, colloidal oatmeal, shea butter, and essential oils like lavender and eucalyptus. Clinical research from the University of Michigan’s Department of Dermatology indicates that oat-based bar soaps improve skin barrier function in 80% of atopic dermatitis patients within four weeks of use. Brands such as L’Occitane and Malin+Goetz have introduced premium bar lines with dermatologist-backed claims and spa-like sensory profiles. Furthermore, the American Herbalists Guild notes a resurgence in traditional botanicals such as calendula, chamomile, and plantain, now featured in evidence-based formulations.

MARKET CHALLENGES

Intensifying Competition from Liquid Body Washes and Syndet Formulations

The erosion from liquid body washes and synthetic detergent (syndet) bars, which dominate retail shelves and advertising narratives is to hamper the growth of the North American bath soap market. Liquid washes, often marketed as more luxurious, hygienic, and skin-friendly, have captured a larger share of consumer spending, particularly in premium segments. According to the U.S. Census Bureau’s Quarterly Retail E-Commerce Sales report, online sales of liquid body washes grew by 19% in 2023, outpacing bar soap e-commerce growth at 6%. Additionally, liquid dispensers are increasingly integrated into bathroom design trends, supported by home renovation data from the National Association of Home Builders, which shows 74% of new U.S. bathrooms include built-in shower caddies or pump systems.

Supply Chain Vulnerability to Natural Ingredient Sourcing and Climate Volatility

The growing reliance on plant-based and organic raw materials exposes the bath soap industry to supply chain disruptions driven by climate change and agricultural instability. Key ingredients such as palm oil, coconut oil, shea butter, and essential oils are predominantly sourced from tropical and subtropical regions vulnerable to extreme weather, deforestation, and geopolitical instability. According to the U.S. Department of Agriculture, global coconut oil production declined by 9% in 2023 due to prolonged droughts in the Philippines, a primary supplier, leading to a 34% price increase in North American markets. The Rainforest Alliance reports that over 60% of palm oil plantations face moderate to high climate risk, threatening sustainable sourcing commitments. Additionally, the International Trade Commission notes that import tariffs and sustainability certification requirements have increased compliance costs for small and mid-sized soap makers by up to 22%. The National Oceanic and Atmospheric Administration links rising sea surface temperatures to erratic monsoon patterns in West Africa, disrupting shea nut harvests—a critical input for moisturizing soaps. These fluctuations not only elevate production costs but also challenge brand promises of consistency and ethical sourcing.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Form, Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Unilever, Procter & Gamble (P&G), Colgate-Palmolive, Johnson & Johnson, Beiersdorf AG, Henkel AG & Co. KGaA, L’Oréal S.A., Reckitt Benckiser Group plc, Lush Retail Ltd., L’Amande, Fenjal, Ach. Brito, Lano., and others. |

SEGMENTAL ANALYSIS

By Product Insights

The mass products segment dominated the North America bath soap market share in 2025with the widespread accessibility, affordability, and long-standing consumer familiarity with established household brands. Mass-market bath soaps, produced by industry giants such as Procter & Gamble, Unilever, and Colgate-Palmolive, are available in every major retail channel, from dollar stores to hypermarkets, ensuring consistent household penetration. According to the U.S. Bureau of Labor Statistics, the average American household spends $28 annually on bar soap, favoring economical multipacks that offer extended usage at minimal cost. The American Hotel & Lodging Association estimates that over 1.2 billion branded bar soaps are distributed annually in U.S. hotels, predominantly from mass-market lines.

The premium bath soap segment is expected to grow with 7.4% from 2025 to 2033 by rising consumer demand for luxury, wellness-infused, and ethically produced personal care products. Unlike mass-market alternatives, premium soaps emphasize natural ingredients, artisanal craftsmanship, dermatological benefits, and sustainable packaging attributes that resonate with affluent, health-conscious, and environmentally aware consumers. According to the Consumer Reports National Research Center, 62% of Americans earning over $100,000 annually prefer premium personal care items, citing skin sensitivity and ingredient transparency as key decision factors. The American Academy of Dermatology notes a 33% increase in consumer inquiries about fragrance-free and hypoallergenic soaps between 2020 and 2023, reflecting a shift toward medical-grade formulations. Brands such as Aesop, Malin+Goetz, and Dr. Bronner’s have capitalized on this trend, offering soaps enriched with shea butter, essential oils, and plant-based glycerin.

By Form Insights

The liquid bath soaps segment was accounted in holding 58.3% of the North America bath soap market share in 2025. Liquid soaps are perceived as more hygienic, easier to dispense, and better suited to contemporary bathroom aesthetics, particularly in urban and high-income households. The U.S. Census Bureau’s American Housing Survey indicates that over 80% of newly constructed homes in the United States include built-in liquid soap dispensers in showers and sinks, reinforcing habitual use. Additionally, liquid formulations allow for greater innovation in texture, fragrance, and skincare infusion, with brands incorporating hyaluronic acid, niacinamide, and botanical extracts to appeal to dermatological concerns. According to the NPD Group, premium liquid body washes grew by 9% in unit sales in 2023, driven by anti-aging and moisture-retention claims. The format also aligns with the broader trend of “shower as sanctuary,” where consumers seek spa-like experiences at home. A 2023 study by the Global Wellness Institute found that 47% of adults associate liquid body washes with relaxation and mental well-being, particularly those infused with aromatherapeutic essential oils. Moreover, major manufacturers invest heavily in pump design, refill systems, and eco-conscious packaging to enhance user experience.

The solid bath soaps segment is projected to grow with a CAGR of 6.2% from 2025 to 2033 with the increasing environmental awareness and a cultural shift toward low-waste, sustainable living. Solid soaps inherently require less packaging, generate no plastic waste, and have a smaller carbon footprint compared to liquid alternatives, which are water-heavy and often housed in non-recyclable bottles. According to the Environmental Protection Agency, plastic bottles from liquid body washes contribute to over 500 million units of plastic waste annually in the U.S., with only 29% being recycled. In contrast, solid soaps frequently use biodegradable or compostable wrappers, as evidenced by the 41% increase in FSC-certified paper packaging used by soap brands in 2023, as reported by the Forest Stewardship Council. The Zero Waste movement, supported by organizations like the Plastic Pollution Coalition, has amplified consumer demand for package-free personal care, with over 18 million Americans now actively reducing single-use plastics in their routines. Additionally, the rise of refill stations in grocery chains such as Whole Foods and Thrive Market has made solid soaps more accessible.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest and held 49.2% of the North America bath soap market share in 2025. Major chains such as Walmart, Kroger, and Safeway dedicate significant shelf space to both mass and premium bath soap brands by ensuring high visibility and accessibility. According to the Food Marketing Institute, over 80% of American households shop at supermarkets at least once a week, creating consistent opportunities for product exposure and repurchasing. These retailers leverage promotional pricing, multi-buy discounts, and end-cap displays to boost soap sales, particularly during seasonal campaigns like back-to-school and holiday gifting. The NielsenIQ Retail Measurement Service indicates that in-store promotions influence 64% of bath soap purchases, with supermarkets accounting for 72% of all promotional activity in the category. Additionally, private-label soap lines offered by retailers such as Costco (Kirkland Signature) and Target (Up & Up) provide cost-effective alternatives, capturing budget-conscious consumers without sacrificing perceived quality.

The online distribution channel is projected to witness a CAGR of 10.8% from 2025 to 2033 owing to the changing consumer behavior, digital accessibility, and the proliferation of direct-to-consumer (DTC) brands that bypass traditional retail. The U.S. Department of Commerce reports that e-commerce accounted for 15.6% of total retail sales in 2023, with personal care products among the fastest-growing categories. Online platforms enable consumers to access niche, premium, and international soap brands that are unavailable in physical stores. According to a 2023 survey by the Digital Commerce 360, 68% of consumers prefer buying specialty soaps online due to broader selection, detailed ingredient transparency, and subscription options. DTC brands like Ethique and HiBAR have capitalized on this trend, offering plastic-free, concentrated solid soaps with carbon-neutral shipping.

COUNTRY LEVEL ANALYSIS

The United States was the top performer in the North American bath soap market with 91.2% of the share in 2025. The country’s vast and diverse population is exceeding 334 million generates high-volume demand across urban, suburban, and rural demographics. According to the U.S. Census Bureau, over 128 million households engage in routine personal care shopping, with bath soap remaining a staple in daily hygiene. The presence of major multinational manufacturers such as Procter & Gamble, Colgate-Palmolive, and Unilever ensures a steady flow of new product launches and marketing campaigns. The Food and Drug Administration’s oversight of labeling and ingredient safety also influences formulation standards across the continent. Additionally, the rise of wellness culture, dermatological awareness, and sustainability movements has accelerated the adoption of premium and natural soaps.

Canada bath soap market is likely to grow with an expected CAGR of 9.2% during the forecast period. The Canadian population of 40 million demonstrates high per capita spending on personal care, with a strong inclination toward premium and organic products. According to Statistics Canada, over 60% of households purchase personal care items from brands with third-party sustainability certifications, such as Leaping Bunny or EcoLogo. The country’s regulatory environment, overseen by Health Canada, enforces strict labeling requirements for cosmetic products, fostering consumer trust in ingredient claims. Retailers like Loblaws, Shoppers Drug Mart, and The Body Shop have expanded their clean beauty sections, reflecting shifting preferences.

KEY MARKET PLAYERS

Unilever, Procter & Gamble (P&G), Colgate-Palmolive, Johnson & Johnson, Beiersdorf AG, Henkel AG & Co. KGaA, L’Oréal S.A., Reckitt Benckiser Group plc, Lush Retail Ltd., L’Amande, Fenjal, Ach. Brito, Lano., and others. Are the market players that are dominating the North America bath soap market.

Top Players In The Market

Procter & Gamble is a cornerstone of the North American bath soap landscape, leveraging its extensive R&D infrastructure and deep consumer insights to maintain leadership across both mass and premium segments. The company’s portfolio includes iconic brands such as Ivory, Olay, and Old Spice, each engineered to balance efficacy, sensory appeal, and dermatological safety. P&G distinguishes itself through scientific formulation, investing heavily in skin barrier research and sustainable innovation. Its global influence extends beyond product development to shaping industry standards in biodegradability and responsible sourcing.

Unilever commands a pivotal presence in the bath soap market through a diversified brand ecosystem that spans everyday affordability and purpose-driven premium lines. Brands like Dove, Lux, and Lifebuoy reflect the company’s dual focus on mass accessibility and health-conscious innovation. Unilever’s strength lies in its commitment to sustainability, with initiatives such as the “Clean Future” program reshaping formulations to eliminate fossil-fuel-derived chemicals. The company pioneers plastic-free packaging and waterless solid formats, setting benchmarks for environmental stewardship. Its global reach is amplified by localized product adaptations and partnerships with dermatological associations by ensuring relevance across diverse markets.

Colgate-Palmolive has established a resilient footprint in the bath soap sector by combining oral care dominance with strategic expansion into personal hygiene. Its Palmolive brand is synonymous with moisturizing bar and liquid soaps, emphasizing skin nourishment through plant-based glycerin and essential oils. The company excels in formulation science, prioritizing mildness, fragrance longevity, and compatibility with sensitive skin. Colgate-Palmolive differentiates itself through integrated household product portfolios, enabling cross-category retail visibility. Sustainability is central to its innovation pipeline, with advancements in recyclable packaging and carbon-neutral manufacturing. The company’s global distribution network ensures consistent availability in both urban centers and rural communities.

Top Strategies Used by Key Market Participants

A primary strategy among leading bath soap manufacturers is the repositioning of bar soap as a sustainable and premium personal care essential, countering the perception of obsolescence. Companies are reframing solid soaps as eco-luxury items by adopting minimalist design, plastic-free packaging, and natural ingredient narratives that appeal to environmentally conscious consumers. Another key approach is the integration of dermatological science into product development, with brands collaborating with skin experts and obtaining endorsements from medical associations to enhance credibility and consumer trust. This medicalization of personal care strengthens brand authority in an increasingly health-aware market. Additionally, firms are expanding direct-to-consumer channels and leveraging digital storytelling through social media and influencer partnerships to build community engagement and promote niche, high-margin products that align with wellness and ethical consumption trends.

COMPETITION OVERVIEW

The competitive environment in the North America bath soap market is defined by a dynamic interplay between legacy corporations and agile niche innovators, each vying for relevance in an evolving personal care ecosystem. Established players leverage brand equity, extensive distribution, and scientific research to maintain dominance, particularly in mass retail channels. However, their position is increasingly challenged by indie brands that emphasize transparency, sustainability, and artisanal authenticity, capturing the attention of younger, values-driven consumers. The market is no longer solely about cleansing efficacy but encompasses broader narratives of wellness, environmental responsibility, and self-expression. Differentiation occurs through formulation integrity, packaging innovation, and storytelling that connects with cultural movements such as zero-waste living and clean beauty. While multinational companies respond with eco-reformulations and sustainability pledges, smaller brands often lead in radical innovation, such as waterless bars and refillable systems.

RECENT HAPPENINGS IN THE MARKET

- In February 2023, Unilever launched a plastic-free is a solid body wash bar under its Love Beauty and Planet brand that designed to reduce single-use plastic waste and appeal to eco-conscious consumers across North America.

- In July 2023, Procter & Gamble introduced a new line of dermatologist-recommended Olay bar soaps enriched with niacinamide and glycerin, which is targeting consumers with dry and sensitive skin conditions.

- In October 2023, Colgate-Palmolive expanded its Palmolive Eco+ range with a biodegradable solid soap bar wrapped in compostable paper, which is reinforcing its commitment to sustainable personal care.

- In January 2025, Unilever partnered with a leading environmental certification body to validate the carbon footprint claims of its Lifebuoy and Dove soap lines by enhancing transparency and consumer trust.

In March 2025, Procter & Gamble rolled out a digital refill initiative for select Olay bar soaps through its e-commerce platform, which is offering reusable tins and subscription-based delivery to promote circular consumption.

MARKET SEGMENTATION

This research report on the North America bath soap market is segmented and sub-segmented into the following categories.

By Form

- Solid Bath Soaps

- Liquid Bath Soaps

By Distribution Channel

- Supermarkets and hypermarkets

- Convenience stores

- Pharmacies

- Specialty Stores

- Online

- Others

By Country

- The USA

- Canada

- Mexico