- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

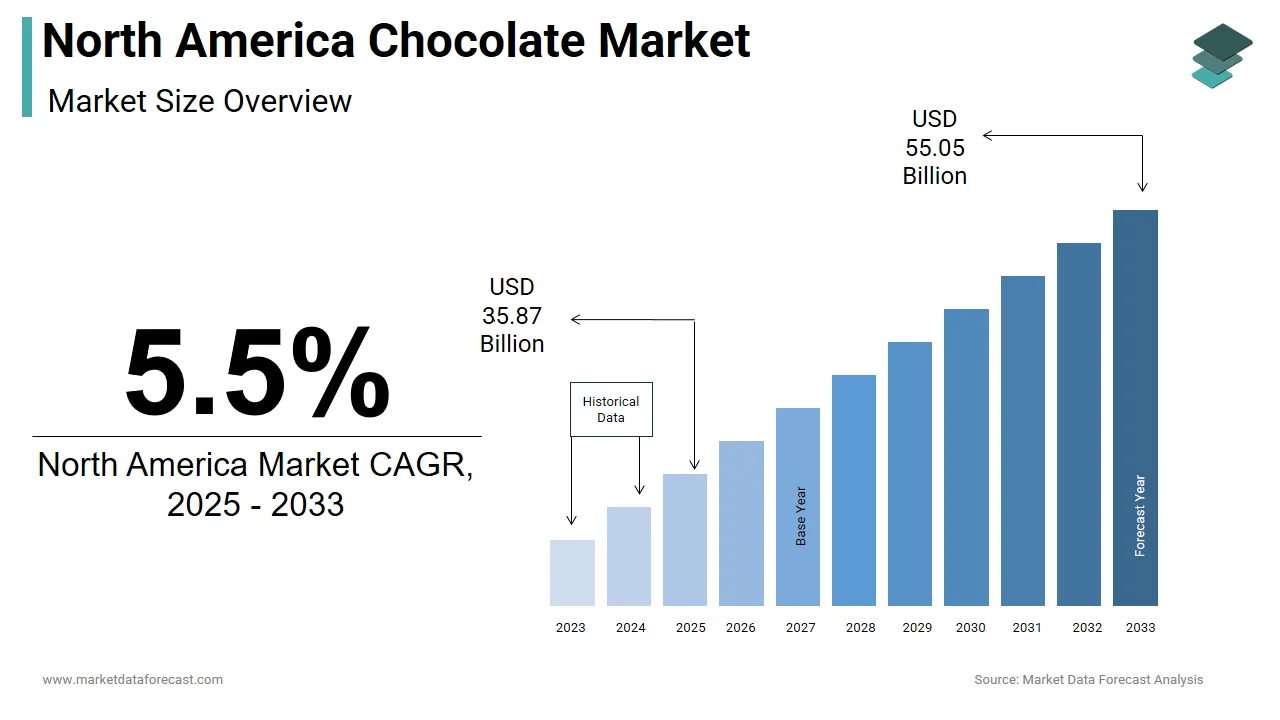

Market Size, 2025

$35.87 BnMarket Estimate, 2026

$37.84 BnMarket Forecast, 2034

$58.08 BnCAGR, 2026–2034

5.5%North America Chocolate Market Size

The size of the North America chocolate market was worth USD 35.87 billion in 2025. The North America market is anticipated to grow at a CAGR of 5.5% from 2026 to 2034 and be worth USD 58.08 billion by 2034 from USD 37.84 billion in 2026.

The chocolate encompasses a wide range of products from mass-produced candy bars to premium, bean-to-bar artisanal chocolates. This market is shaped by evolving consumer preferences, including a growing emphasis on health-conscious consumption, sustainability, and indulgence with purpose. As per the National Confectioners Association (NCA), chocolate remains a staple in American households, with over two-thirds of consumers purchasing chocolate at least once a month, which is often driven by seasonal promotions and gifting occasions. In Canada, chocolate consumption has been influenced by increasing demand for ethically sourced and organic products. According to Agriculture and Agri-Food Canada, there has been a notable rise in imports of fair-trade-certified cocoa, reflecting shifting consumer values and regulatory support for sustainable sourcing practices. The country also hosts a growing number of boutique chocolatiers who cater to niche markets with handcrafted and locally sourced offerings. Meanwhile, Mexico contributes to the regional chocolate landscape through both traditional and modern consumption patterns. The Mexican government has supported local cocoa production initiatives in southern states like Chiapas and Tabasco, which is reinforcing domestic supply chains while maintaining strong export ties with the U.S. and Europe.

MARKET DRIVERS

Rising Demand for Premium and Artisanal Chocolate Varieties

The increasing preference for premium and artisanal chocolate varieties among discerning consumers is prompting the growth of the market. According to Mintel, nearly 45% of U.S. consumers expressed willingness to pay more for high-quality chocolate in 2024, reflecting a shift away from commodity-driven purchases toward experiential and value-added offerings. This trend is particularly pronounced among millennials and Gen Z, who prioritize transparency, craftsmanship, and storytelling when selecting food products. Artisanal chocolatiers have capitalized on this movement by offering small-batch, single-origin, and bean-to-bar products that emphasize traceability, unique flavor profiles, and ethical sourcing. Additionally, online platforms have expanded access to niche chocolate producers, allowing consumers to explore international flavors and limited-edition releases from around the world.

Increasing Health Consciousness and Functional Chocolate Consumption

Another significant driver shaping the North America chocolate market is the rising interest in health-conscious and functional chocolate consumption. According to the International Food Information Council (IFIC), over 60% of U.S. consumers actively seek healthier snack alternatives, which is prompting manufacturers to develop low-sugar, high-cocoa, and nutrient-enhanced chocolate options tailored to wellness-oriented lifestyles.

Dark chocolate has gained popularity due to its perceived health benefits, including antioxidant properties and potential cardiovascular advantages. In response to this demand, major chocolate brands and startups alike have introduced products infused with adaptogens, nootropics, plant-based proteins, and CBD to appeal to consumers seeking both indulgence and wellness.

MARKET RESTRAINTS

Growing Obesity Rates and Regulatory Pressure on Sugar Content

A major restraint affecting the North America chocolate market is the growing public health concern surrounding obesity and excessive sugar intake. Government agencies and health organizations have responded with initiatives aimed at reducing sugar consumption, such as front-of-package warning labels in Canada and proposed sugar taxes in several U.S. states. Health Canada reported that consumers are now reading nutrition labels more carefully, which is leading to a decline in impulse purchases of conventional chocolate products. Additionally, parents and caregivers are becoming more selective about children's snacking choices, favoring alternatives like fruit-based treats, protein bars, and low-sugar dairy desserts. The American Academy of Pediatrics emphasized the need for reduced sugar intake among children, further influencing purchasing behavior. These health-related concerns have forced chocolate manufacturers to reformulate products and promote portion-controlled packaging.

Volatility in Cocoa Prices and Supply Chain Disruptions

Another critical restraint impacting the North. These price fluctuations have directly affected manufacturing costs for chocolate producers, leading to higher retail prices and reduced profit margins. The U.S. Department of Agriculture (USDA) noted that chocolate confectionery prices increased by nearly 8% year-over-year in 2024l, which is making consumers more price-sensitive and less likely to purchase premium or non-essential chocolate items. Smaller chocolate manufacturers and independent chocolatiers have been disproportionately affected by these cost pressures, limiting their ability to compete with large-scale producers who can absorb input price increases through economies of scale.

MARKET OPPORTUNITIES

Expansion of Plant-Based and Vegan Chocolate Options

An emerging opportunity in the North America chocolate market is the rapid expansion of plant-based and vegan chocolate alternatives. According to the Plant Based Foods Association, the plant-based confectionery segment grew by over 18% in 2024 with chocolate-based products accounting for a significant share of this increase. This growth is fueled by the expanding adoption of vegan and flexitarian diets, particularly among younger consumers who seek indulgent yet health-aligned food choices. Manufacturers are responding by introducing innovative blends that replace dairy with plant-derived ingredients while maintaining texture and meltability. Brands such as Dang Brothers, Hu Kitchen, and Alter Eco have successfully positioned themselves in this space, which is leveraging clean-label positioning and eco-friendly packaging to attract conscious consumers. Moreover, mainstream chocolate companies have entered the category through acquisitions and internal product development.

Integration of Functional Ingredients into Chocolate Products

Another transformative opportunity in the North America chocolate market is the integration of functional ingredients such as adaptogens, nootropics, and CBD-infused chocolate products. This trend is being driven by a convergence of the wellness and indulgence markets, where consumers seek products that provide both sensory satisfaction and health benefits. Companies are capitalizing on this shift by developing chocolate bars infused with ingredients such as ashwagandha, L-theanine, magnesium, and MCT oil to support stress relief, focus, and energy management. Moreover, the legal cannabis market has spurred CBD and THC-infused chocolate edibles, particularly in states where recreational use is permitted.

MARKET CHALLENGES

Ethical Sourcing and Sustainability Pressures

The increasing pressure to ensure ethical sourcing and environmental sustainability throughout the supply chain is impeding the growth of the North America chocolate market. According to the World Cocoa Foundation, over 90% of global cocoa production comes from smallholder farms, many of which face issues related to deforestation, child labor, and inadequate farmer compensation.

North American consumers, particularly millennials and Gen Z, are demanding greater transparency in sourcing practices. However, implementing sustainable sourcing models requires significant investment and logistical coordination. Moreover, climate change and environmental degradation are threatening cocoa yields, further complicating long-term sourcing strategies.

Regulatory Scrutiny Over Marketing to Children

A pressing challenge facing the North America chocolate market is the increasing regulatory scrutiny surrounding the marketing of chocolate products to children. Health advocacy groups and consumer watchdog organizations have raised concerns about the influence of branded characters, cartoon imagery, and interactive digital campaigns that may encourage frequent consumption of sugar-laden chocolate products. In response, some chocolate manufacturers have voluntarily revised packaging designs and promotional strategies, removing child-oriented branding from certain product lines and launching educational campaigns on responsible consumption. However, compliance with evolving advertising regulations remains complex as digital engagement channels become more sophisticated.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Confectionery Variant, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Ferrero International SA, Mars Incorporated, Mondelez International Inc., Nestle SA, and The Hershey Company. |

SEGMENTAL ANALYSIS

By Confectionery Variant Insights

The milk and white chocolate segment was the largest and held 58.3% of the North America chocolate market share in 2024. One of the key drivers behind the dominance of this segment is its deep-rooted presence in mainstream confectionery offerings. According to the National Confectioners Association (NCA), over 65% of all chocolate candy bars sold in the U.S. contain milk or white chocolate, which makes them integral to seasonal promotions, gifting trends, and impulse purchases at retail outlets. Furthermore, white chocolate has seen growing use in premium and novelty product lines, especially during holidays like Valentine’s Day and Easter. With major manufacturers continuously introducing new flavors and limited-edition packaging, milk and white chocolate variants continue to maintain their stronghold in the North American chocolate landscape.

The dark chocolate segment is expected to hold a CAGR of 9.4% throughout the forecast period. According to Mintel, sales of dark chocolate products in the U.S. grew by over 11% in 2023, outpacing other chocolate categories. Moreover, specialty retailers and online platforms have played a role in increasing accessibility to premium dark chocolate from global origins, including Ecuador, Venezuela, and Madagascar.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest and held 43.2% of the North America chocolate market share in 2024. One of the leading factors driving the dominance of this segment is the convenience and variety offered by large retail chains such as Walmart, Kroger, and Costco. In Canada, the Canadian Federation of Independent Grocers (CFIG) reported that supermarkets remained the top choice for chocolate buyers, with over 75% of surveyed consumers preferring these locations for bulk purchases and family-friendly options. Another contributing factor is the role of private label brands, which offer cost-effective alternatives to name-brand chocolates.

The online retail segment is swiftly emerging with an expected CAGR of 12.8% in the coming years. This rapid growth is fueled by the increasing popularity of direct-to-consumer (DTC) models, subscription services, and specialty e-commerce platforms focused on gourmet and artisanal chocolates. Subscription-based services like Cocoa & Co. and Gold Box Club have also gained traction, offering curated monthly selections tailored to individual taste preferences.

COUNTRY LEVEL ANALYSIS

United States Chocolate Market Insights

The United States was the top performer in the North America chocolate market with 80.2% of the share in 2024. The country's deep-rooted cultural association with chocolate consumption during holidays such as Halloween, Valentine’s Day, and Easter are to propel the growth of the market. Additionally, the rise of health-conscious consumers has led to a surge in demand for dark chocolate, organic variants, and functional chocolate products enriched with superfoods or adaptogens.

Canada Chocolate Market Insights

Canada was positioned second with a 16.1% of share in the North America chocolate market. One of the primary contributors to this growth is the increasing demand for Fair Trade and Rainforest Alliance-certified chocolates. According to Statistics Canada, over 55% of Canadian consumers prefer chocolate products with sustainability claims, a significantly higher proportion than the global average. Moreover, Canada’s multicultural population has contributed to a diverse chocolate market, with growing demand for ethnic and premium European-style chocolates. The Canadian Specialty Chocolate Association reported that artisanal chocolate makers in Quebec and British Columbia saw a 15% increase in sales in 2023, which indicates strong local engagement with high-quality chocolate experiences. Additionally, government-led initiatives promoting sustainable agriculture and traceable sourcing have encouraged domestic chocolate producers to differentiate themselves through transparency and ethical practices.

COMPETITIVE LANDSCAPE

The competition in the North America chocolate market is highly dynamic, featuring a mix of global confectionery giants, regional manufacturers, and a growing number of artisanal and specialty brands. Established players such as Hershey, Mondelez, and Nestlé maintain strong footholds through broad distribution networks, brand recognition, and continuous product development tailored to mainstream and niche markets alike.

Simultaneously, boutique chocolatiers and clean-label startups are gaining traction by focusing on bean-to-bar craftsmanship, fair-trade certifications, and innovative formats such as vegan and functional chocolates. These smaller players leverage social media, direct-to-consumer sales, and curated retail placements to carve out distinct identities and challenge industry leaders.

Retailers and private label brands also exert influence by offering competitively priced alternatives that mirror the taste and quality of national brands. This intensifies the race for shelf space and consumer loyalty across supermarkets, convenience stores, and online platforms. Innovation, brand storytelling, and supply chain ethics have become critical differentiators in this fiercely contested market.

MARKET KEY PLAYERS

Companies playing a dominant role in the North America chocolate market profiled in this report are

- Ferrero International SA

- Mars Incorporated

- Mondelez International Inc.

- Lindt & Sprüngli

- Nestle SA

- The Hershey Company

TOP LEADING PLAYERS IN THE MARKET

Hershey is a dominant force in the North America chocolate market and one of the most recognized confectionery brands globally. Known for its extensive portfolio that includes Hershey’s, Reese’s, and Kisses, the company plays a central role in shaping consumer preferences and seasonal gifting trends. Hershey’s influence extends beyond traditional confections with increasing focus on premium, organic, and plant-based offerings to align with evolving dietary habits.

Mondelez is a key player in the North American chocolate landscape, managing global brands such as Cadbury and Toblerone in the region. The company emphasizes innovation and brand consistency while adapting to local tastes. Mondelez has been instrumental in advancing sustainable sourcing initiatives and digital engagement strategies, which is reinforcing its dominant position in both mass-market and specialty segments.

Lindt has established itself as a leader in premium chocolate consumption across North America. Renowned for its high-quality Swiss chocolate, Lindt has successfully expanded its retail presence and introduced flagship stores in major cities. The company’s focus on luxury positioning, experiential retail, and limited-edition releases has strengthened its appeal among affluent and health-conscious consumers.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies adopted by leading players in the North America chocolate market is product innovation through flavor diversification and functional ingredient integration, where companies introduce new taste profiles, textures, and wellness-focused formulations to capture evolving consumer preferences.

Another key approach is leveraging sustainability narratives and ethical sourcing claims , allowing brands to differentiate themselves in a competitive marketplace and align with the values of environmentally conscious and socially responsible buyers who prioritize transparency in cocoa procurement.

Firms are increasingly investing in digital transformation and direct-to-consumer platforms by enhancing brand visibility through e-commerce, personalized subscriptions, and immersive storytelling that strengthens customer engagement and builds long-term loyalty beyond traditional retail channels.

RECENT MARKET DEVELOPMENTS

- In February 2024, Hershey announced the launch of a new line of plant-based chocolate bars made with oat milk and free from artificial additives, which is targeting health-conscious consumers and expanding its portfolio beyond traditional confections.

- In April 2024, Mondelez acquired a stake in a clean-label chocolate startup specializing in low-sugar and functional chocolate bars by aiming to enhance its wellness-oriented product offerings and attract younger demographics.

- In July 2024, Lindt & Sprüngli opened a flagship chocolate café in Chicago by combining retail and experiential elements to strengthen brand engagement and showcase its premium product range to a wider audience.

- In September 2023, Nestlé launched a blockchain-enabled traceability program for its chocolate supply chain by allowing consumers to verify the origins of cocoa used in its U.S. and Canadian product lines, reinforcing transparency and ethical sourcing.

- In November 2023, Guittard Chocolate Company expanded its B2B partnerships with independent bakeries and ice cream makers, which is supplying high-quality bulk chocolate to support the growth of premium dessert and confectionery businesses across North America.

MARKET SEGMENTATION

This research report on the North America chocolate market is segmented and sub-segmented into the following categories.

By Confectionery Variant

- Dark Chocolate

- Milk and White Chocolate

By Distribution Channel

- Convenience Store

- Online Retail Store

- Supermarket/Hypermarket

- Others

By Country

- United States

- Canada

- Mexico

- Rest of North America