North America Confectionery Market Size, Share, Trends & Growth Forecast Report By Type, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

North America Confectionery Market Size

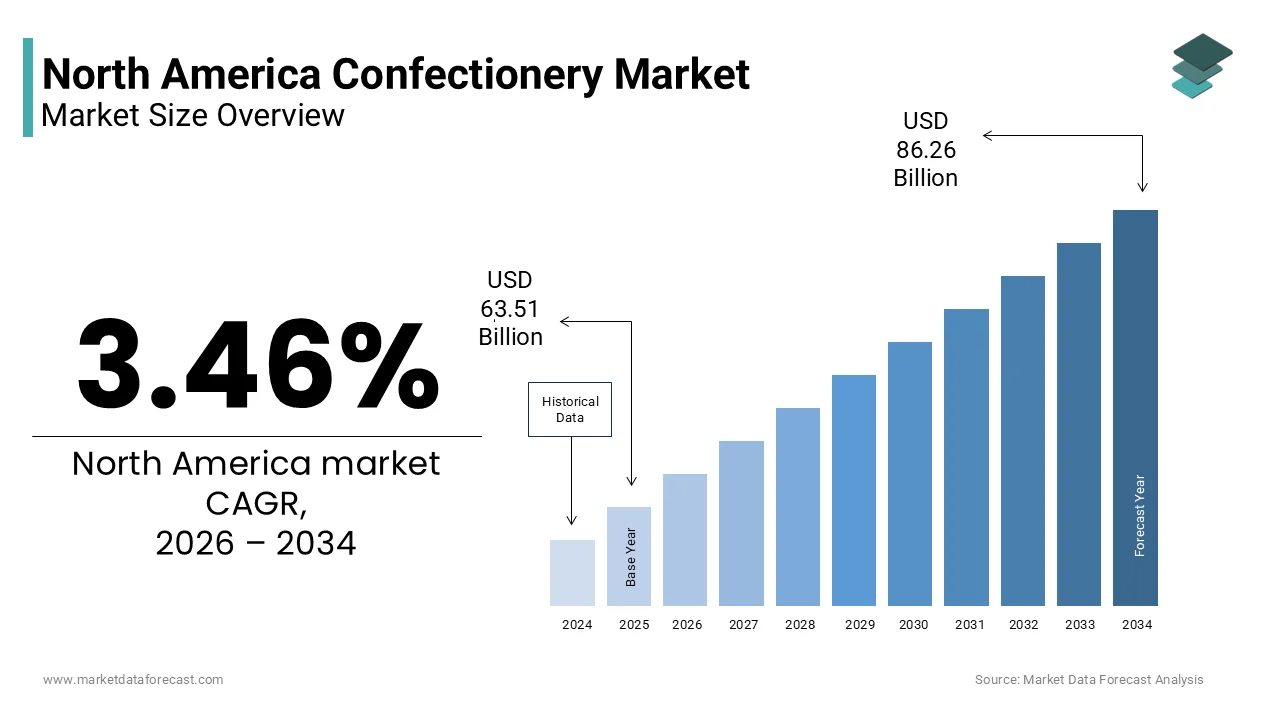

The confectionery market size in North America was valued at USD 63.51 billion in 2025 and is predicted to be worth USD 86.26 billion by 2034 from USD 65.71 billion in 2026 and grow at a CAGR of 3.46% from 2026 to 2034.

The confectionery is deeply embedded in consumer culture, with seasonal promotions, gifting traditions, and impulse purchasing playing significant roles in driving sales. The United States and Canada are key contributors, where confectionery items are not only consumed as indulgences but also integrated into daily snacks, health-focused formulations, and premium gourmet offerings.

According to the U.S. Department of Agriculture (USDA), per capita consumption of confectionery products in the United States has remained relatively stable over the past decade, with an average annual intake of approximately 25 pounds per person. The ris2e of e-commerce and direct-to-consumer retail models has further expanded accessibility, allowing niche and artisanal brands to reach wider audiences. Additionally, growing partnerships between confectionery companies and foodservice operators have broadened product distribution through cafes, vending machines, and convenience stores. As per the International Food Information Council, more than half of surveyed consumers in North America indicated a preference for healthier snack alternatives, influencing manufacturers to innovate while maintaining taste appeal.

MARKET DRIVERS

Rising Demand for Premium and Artisanal Confectionery Products

One of the primary drivers of the North America confectionery market is the increasing consumer preference for premium and artisanal confectionery products. According to the National Confectioners Association, premium chocolate and specialty candy accounted for over 30% of total confectionery sales growth in the United States in 2023, reflecting a shift away from mass-produced offerings toward high-quality, small-batch, and ethically sourced confections. This trend is being supported by the proliferation of boutique confectionery shops, online retailers, and experiential retail formats that emphasize craftsmanship and storytelling.

Expansion of E-Commerce and Direct-to-Consumer Distribution Channels

Another major driver fueling the North America confectionery market is the rapid expansion of e-commerce and direct-to-consumer (DTC) distribution channels. Consumers are increasingly opting for digital platforms to access limited-edition releases, subscription boxes, and global confectionery imports that may not be available in traditional retail outlets. Companies like Hershey’s and Mars have launched branded e-commerce sites, while independent brands are leveraging platforms such as Amazon and Etsy to reach niche audiences. Additionally, social commerce via Instagram and TikTok has played a role in promoting visually appealing confectionery items, especially among younger demographics. The e-commerce channel is expected to remain a key growth avenue for both established and emerging confectionery brands across North America as logistics networks become more efficient and digital marketing strategies evolve.

MARKET RESTRAINTS

Growing Health Awareness and Regulatory Pressure on Sugar Consumption

A significant restraint affecting the North America confectionery market is the rising consumer awareness regarding health risks associated with excessive sugar consumption, coupled with increasing regulatory scrutiny. According to the Centers for Disease Control and Prevention (CDC), more than 40% of adults in the United States suffer from obesity, which is prompting public health initiatives aimed at reducing sugar intake. The CDC and the American Heart Association have both issued guidelines recommending lower daily sugar limits, which has influenced consumer behavior toward seeking reduced-sugar or alternative sweetener-based confectionery options.

Additionally, regulatory bodies such as Health Canada and the U.S. Food and Drug Administration (FDA) have implemented labeling reforms requiring front-of-package warning labels for high-sugar products. In 2023, Health Canada introduced new nutritional labeling standards mandating clearer indications of added sugars, compelling manufacturers to reformulate products or risk losing market share. A 2023 study published in the Journal of Nutrition Education and Behavior found that 68% of surveyed consumers in North America actively avoided confectionery items with high sugar content, indicating a behavioral shift that poses challenges for traditional candy and chocolate producers. While some companies have responded by introducing low-calorie or natural sweetener-infused products, the overall impact of health-conscious consumer choices continues to constrain growth in certain segments of the confectionery market.

Supply Chain Disruptions and Ingredient Cost Volatility

Another critical constraint impacting the North America confectionery market is the ongoing volatility in raw material costs and supply chain disruptions, which affect production efficiency and pricing stability. According to the U.S. Department of Agriculture’s Economic Research Service, the price of cocoa beans a primary ingredient in chocolate confectionery increased by over 25% in 2023 due to adverse weather conditions in West African producing regions and geopolitical instability. Similarly, sugar prices saw fluctuations driven by supply shortages in major exporting countries such as Brazil and India. These cost increases have placed pressure on manufacturers to either absorb expenses or pass them on to consumers, potentially dampening demand. In Canada, the Canadian Federation of Independent Grocers reported that confectionery retailers faced a 15% rise in procurement costs for key ingredients in late 2023, leading to selective price hikes and product downsizing strategies. Smaller confectionery brands, in particular, struggle to manage these financial risks without economies of scale, which is limiting their ability to compete effectively in a market dominated by large multinational corporations.

MARKET OPPORTUNITIES

Surge in Demand for Functional and Health-Conscious Confectionery

An emerging opportunity in the North America confectionery market is the growing demand for functional and health-conscious confectionery products, which combine indulgence with wellness benefits. According to the International Food Information Council, over 60% of consumers in North America expressed interest in snacks that provide additional health benefits beyond basic nutrition in a 2023 survey. This shift has led to the development of confectionery items infused with protein, vitamins, adaptogens, and plant-based ingredients designed to support energy, immunity, and mental well-being. Major confectionery companies such as Nestlé and Mondelez have launched fortified chocolate bars and gummies containing collagen, fiber, and probiotics to cater to this evolving consumer mindset. In Canada, the Canadian Health Food Association reported a 25% increase in the number of certified health-focused confectionery brands entering the market in 2023, signaling strong regional adoption. Startups and artisanal producers are also capitalizing on this trend by offering organic, keto-friendly, and CBD-infused candies that align with modern dietary preferences.

Growth of Seasonal and Limited-Edition Product Launches

Another significant opportunity shaping the North America confectionery market is the strategic emphasis on seasonal and limited-edition product launches, which drive consumer excitement and repeat purchases. According to the National Confectioners Association, more than 75% of confectionery sales in the U.S. occur around key holidays such as Halloween, Easter, Valentine’s Day, and Christmas, making seasonality a core component of brand marketing and product planning strategies. Companies are increasingly leveraging limited-time offers (LTOs) to create urgency and differentiate themselves in a competitive marketplace. A 2023 report by Mintel found that 58% of North American consumers were more likely to try a new confectionery product if it was marketed as a seasonal or exclusive variant. Brands such as Reese’s and Cadbury have successfully capitalized on this trend by releasing themed packaging and unique flavor combinations tailored to specific holidays and cultural events.

MARKET CHALLENGES

Changing Consumer Preferences Toward Clean Label Ingredients

A pressing challenge currently facing the North America confectionery market is the evolving consumer demand for clean label ingredients, which necessitates extensive reformulation efforts and transparency in sourcing practices. According to the Institute of Food Technologists, over 70% of consumers in North America prioritize products with recognizable, minimally processed ingredients when making snack purchases. This shift has compelled confectionery manufacturers to eliminate artificial colors, preservatives, and high-fructose corn syrup from their formulations, often at the expense of texture, shelf life, and cost-efficiency.

In response, companies are investing in alternative natural colorants derived from beet juice, spirulina, and turmeric, as well as plant-based sweeteners such as stevia and monk fruit extract. However, these substitutions come with technical challenges related to consistency, flavor balance, and manufacturing scalability. Additionally, consumer skepticism about ingredient claims and greenwashing has led to calls for stricter regulatory oversight.

Intensifying Competition from Alternative Snack Categories

Another significant challenge impeding the growth of the North America confectionery market is the intensifying competition from alternative snack categories, particularly those perceived as healthier or more functional. This shift is particularly evident among health-conscious demographics such as millennials and Gen Z, who are more inclined to choose yogurt-covered almonds, dark chocolate with added fiber, or gummy candies fortified with vitamins rather than traditional sugar-laden confections. A 2023 report by the Hartman Group found that 62% of surveyed consumers preferred snacks that contributed to their daily wellness goals, pushing confectionery brands to redefine their value propositions. In response, many companies have introduced hybrid products that blend indulgence with functionality, though success varies depending on taste perception and pricing competitiveness.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.46% |

| Segments Covered | By Type, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, and Rest of North America |

| Market Leaders Profiled | Delfi Limited (Singapore), Ezaki Glico Co., Ltd. (Japan), Ferrero SpA (Italy), Lindt & Sprüngli AG (Switzerland), Lotte Confectionery Co. Ltd. (South Korea), Mars, Incorporated (U.S.), Mondelez International, Inc. (U.S.), Nestlé S.A. (Switzerland), The Hershey Company (U.S.), Wm. Wrigley Jr. Company (U.S.), and others |

SEGMENTAL ANALYSIS

By Type Insights

The chocolate was the largest and held 45.3% of the North America confectionery market share in 2025 due to its widespread consumer appeal, cultural significance in seasonal gifting, and integration into various snack and dessert formats. One of the key factors driving this segment’s dominance is the strong presence of major chocolate manufacturers such as Hershey’s, Mars, and Lindt & Sprüngli, which continuously innovate with new product lines and packaging strategies.

The fine bakery wares segment is swiftly emerging with a CAGR of 6.2% throughout the forecast period. A primary driver behind this growth is the increasing preference for premium and experiential food offerings among millennials and affluent urban consumers. A 2023 report by Mintel found that 54% of surveyed consumers in North America were willing to pay a premium for handcrafted, small-batch bakery items that emphasized quality ingredients and unique flavors. Additionally, the rise of direct-to-consumer e-commerce platforms has enabled niche bakeries to reach national audiences, bypassing traditional retail constraints. In the U.S., Shopify reported a 20% surge in online orders for gourmet bakery products during peak holiday seasons, reinforcing the digital shift in purchasing behavior.

REGIONAL ANALYSIS

The United States was the top performer in the North America confectionery market with 78.2% of the share in 2025. As the global epicenter of confectionery innovation and consumption, the U.S. boasts a mature and diverse industry driven by established brands, seasonal purchasing habits, and a strong retail and e-commerce infrastructure. Additionally, the rise of premium and health-focused confectionery segments has allowed manufacturers to cater to evolving consumer preferences while maintaining volume growth. Companies like Hershey’s and Mondelez have expanded their portfolios to include plant-based, organic, and functional candies, capturing a broader audience.

Canada ranked next to the Unite States by capturing 17.3% of share in the North America confectionery market. One of the key drivers of market expansion is the rising popularity of artisanal and small-batch confectionery brands, particularly in urban centers like Toronto, Vancouver, and Montreal. The Canadian Specialty Food Association noted a 20% increase in registrations of independent confectionery businesses in 2023, signaling strong entrepreneurial activity and consumer support for local producers. Additionally, cross-border trade agreements and partnerships with U.S.-based manufacturers have facilitated greater variety and availability of products in the domestic market. In response to changing dietary preferences, Canadian retailers such as Loblaw and Sobeys have introduced exclusive lines of reduced-sugar, non-GMO, and vegan confectionery items.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key Players in North America Confectionery Market are Delfi Limited (Singapore), Ezaki Glico Co., Ltd. (Japan), Ferrero SpA (Italy), Lindt & Sprüngli AG (Switzerland), Lotte Confectionery Co. Ltd. (South Korea), Mars, Incorporated (U.S.), Mondelez International, Inc. (U.S.), Nestlé S.A. (Switzerland), The Hershey Company (U.S.), Wm. Wrigley Jr. Company (U.S.).

The competition in the North America confectionery market is highly dynamic, shaped by the presence of established multinational corporations and a growing number of niche, artisanal, and health-focused brands vying for consumer attention. Major players dominate through brand equity, broad distribution networks, and continuous product innovation in response to evolving health and wellness trends. However, smaller and independent brands are gaining traction by emphasizing craftsmanship, sustainability, and unique flavor profiles that appeal to discerning consumers.

Market participants must navigate an increasingly complex landscape influenced by changing dietary preferences, regulatory scrutiny around sugar content, and rising demand for clean-label and functional confectionery. As consumers seek more transparency and purpose-driven products, companies are repositioning their offerings to balance indulgence with perceived health benefits. Additionally, the rise of e-commerce and social commerce has introduced new competitive dynamics by enabling emerging brands to challenge industry giants through targeted digital marketing and direct engagement strategies. This evolving environment fosters innovation but also intensifies pressure on traditional players to adapt and differentiate themselves effectively.

TOP PLAYERS IN THE MARKET

The Hershey Company

Hershey is a dominant force in the North America confectionery market, known for its iconic chocolate brands such as Hershey’s Kisses, Reese’s, and Kit Kat. The company has built a strong legacy through innovation, brand loyalty, and extensive distribution networks across retail, foodservice, and e-commerce platforms. Hershey consistently adapts to consumer trends by introducing products that cater to health-conscious consumers, including sugar-free and plant-based options. Its strategic acquisitions and sustainability initiatives have also strengthened its position both regionally and globally.

Mars, Incorporated

Mars plays a pivotal role in shaping the North American confectionery landscape with globally recognized brands like M&M’s, Snickers, Twix, and Orbit gum. The company emphasizes product diversification, responsible sourcing, and digital engagement to maintain consumer relevance. Mars invests heavily in research and development to meet evolving dietary preferences while maintaining indulgence as a core value. Its commitment to sustainability and ethical cocoa sourcing enhances its global reputation and long-term competitiveness.

Mondelez International

Mondelez is a major contributor to the North America confectionery market, offering a diverse portfolio that includes Cadbury, Oreo, Trident, and Toblerone. Known for its global reach and innovation, Mondelez focuses on premiumization, digital marketing, and e-commerce expansion to drive growth. The company leverages its expertise in snack, bakery, and confectionery categories to capture new consumer segments and strengthen its regional foothold.

TOP STRATEGIES USED BY KEY PLAYERS

One of the most impactful strategies employed by leading players in the North America confectionery market is product innovation and portfolio diversification, where companies continuously introduce new flavors, formats, and functional attributes such as reduced sugar, plant-based ingredients, and fortified snacks to align with shifting consumer preferences while maintaining brand appeal.

Another key approach is strategic brand positioning through seasonal and limited-time offers , which helps sustain consumer excitement and drive impulse purchases. The expansion into digital and direct-to-consumer channels has become a crucial strategy, allowing manufacturers to engage directly with consumers, collect valuable data insights, and offer personalized experiences. This shift enables greater control over branding, pricing, and product availability, especially among younger, tech-savvy demographics seeking convenience and novelty.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, The Hershey Company launched a new line of plant-based chocolate bars made with oat milk and free from animal-derived ingredients, which is targeting vegan consumers and expanding its portfolio in the health-conscious snack segment.

- In August 2023, Mars Wrigley introduced a limited-edition Halloween candy collection featuring sustainable packaging made from 100% recyclable materials by aligning with the company’s environmental commitments and tapping into seasonal consumer demand.

- In January 2025, Mondelez International acquired a U.S.-based startup specializing in functional gummies infused with vitamins and adaptogens by aiming to enter the wellness confectionery space and attract health-oriented consumers.

- In June 2025, Nestlé expanded its North American presence by opening a new digital-first confectionery concept store in New York City, integrating augmented reality experiences and customizable candy stations to enhance consumer engagement.

- In November 2025, Ferrero Group partnered with a major U.S. coffee chain to co-develop exclusive confectionery items for in-store sale, which is leveraging cross-category synergies to boost brand visibility and drive impulse purchases among café-goers.

MARKET SEGMENTATION

This research report on the North America confectionery market has been segmented and sub-segmented based on the following categories.

Type

- Sugar

- Chocolate

- Fine Bakery Wares

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

1. What is the North America confectionery market?

The North America confectionery market includes the production, distribution, and sale of sweet food products such as chocolates, candies, gums, and sugar confectionery items.

2. What products are included in the confectionery market?

The market includes chocolates, hard candies, gummies, chewing gum, mints, caramel products, toffees, and sugar free confectionery products.

3. What factors are driving the growth of the North America confectionery market?

Rising demand for premium chocolates, increasing seasonal consumption, product innovation, and growing interest in convenient snack products are key growth drivers.

4. Which segment dominates the North America confectionery market?

Chocolate confectionery remains one of the leading segments due to strong consumer demand for premium, dark, and flavored chocolate products.

5. How are health trends influencing the confectionery market?

Manufacturers are introducing low sugar, organic, vegan, gluten free, and functional confectionery products to meet changing consumer preferences.

6. What role does product innovation play in the confectionery industry?

Companies are launching new flavors, healthier ingredients, attractive packaging, and limited edition products to attract consumers and increase brand engagement.

7. Which distribution channels are important in the confectionery market?

Major distribution channels include supermarkets, convenience stores, specialty stores, online retail platforms, and vending machines.

8. How does seasonal demand affect the confectionery market?

Sales increase significantly during holidays and celebrations such as Halloween, Christmas, Easter, and Valentine’s Day due to higher gifting and festive consumption.

9. What challenges affect the North America confectionery market?

Challenges include fluctuating raw material prices, health concerns related to sugar consumption, changing dietary preferences, and strict food labeling regulations.

10. What is the future outlook of the North America confectionery market?

The market is expected to grow steadily due to rising demand for premium products, increasing innovation in healthier confectionery options, and expanding digital retail channels.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com