North America Combine Harvester Market Size, Share, Trends & Growth Forecast Report, Segmented By Product (Self-Propelled, Tractor Pulled And PTO Powered), Class (Class 4 And 5, Class 6, Class 7, Class 8 And Class 9 And 10), And By Country (The U.S, Canada, Mexico and Rest of North America), Industry Analysis From 2026 to 2034

North America Combine Harvester Market Size

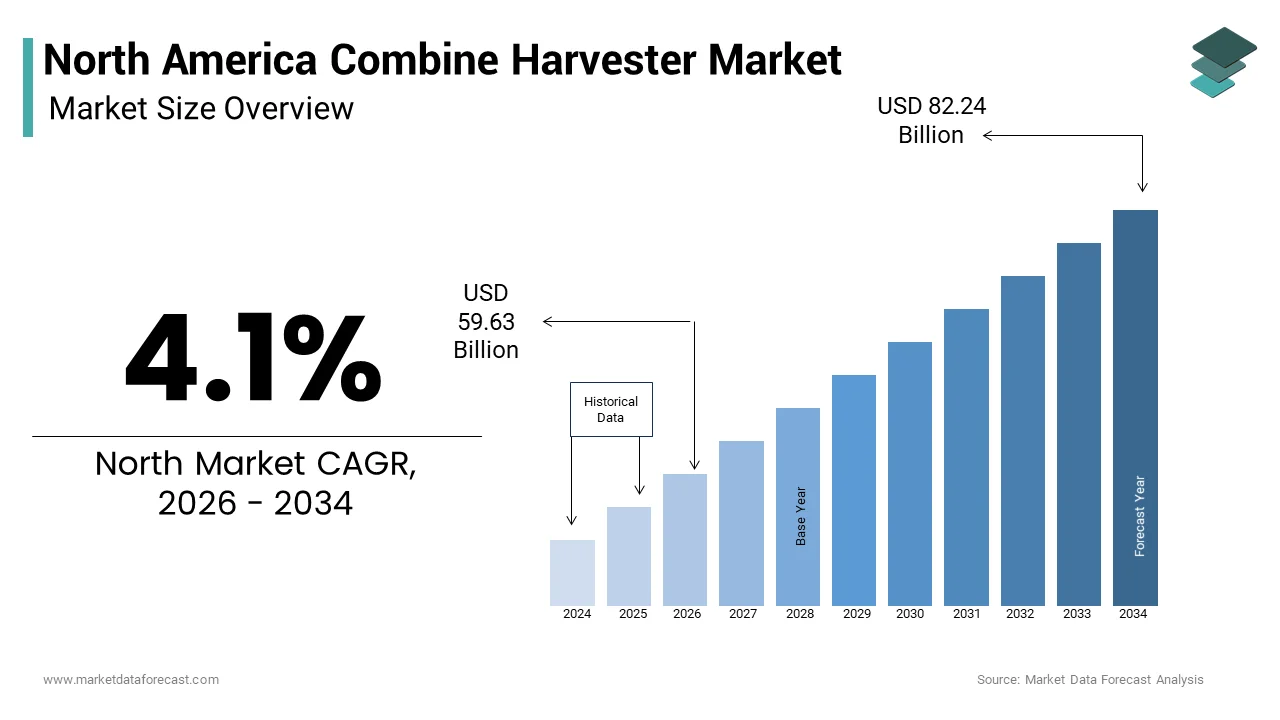

The North American combined harvester market size was valued at USD 57.28 billion in 2025 and is expected to reach USD 59.63 billion in 2026 from USD 82.24 billion by 2034, growing at a CAGR of 4.1% during the forecast period from 2026 to 2034.

The increasing need for efficient harvesting solutions to meet growing food demands is solely propelling the growth of the North American combine harvester market. The market is particularly robust in the Midwest, often referred to as the "Corn Belt," where large-scale farming operations rely heavily on advanced machinery. Canada, with its vast prairies, also contributes significantly, especially in wheat and barley production, as stated by Statistics Canada. The adoption of self-propelled combine harvesters has surged, with the American Farm Bureau Federation reporting that over 70% of large farms now use these machines. Despite this growth, challenges such as high equipment costs and the need for skilled operators persist. Additionally, the push for precision agriculture has spurred demand for technologically advanced models equipped with GPS and automation features by reshaping the competitive landscape.

MARKET DRIVERS

Increasing Demand for High-Yield Crops

The rising global population and the subsequent demand for high-yield crops are key drivers of the combine harvester market in North America. As per the Food and Agriculture Organization (FAO), the global population is projected to reach 9.7 billion by 2050, necessitating a 70% increase in agricultural productivity. In North America, staple crops like corn, soybeans, and wheat are central to meeting this demand, with the USDA estimating that corn production alone exceeds 380 million metric tons annually. Combine harvesters enable farmers to maximize efficiency during the critical harvesting period, reducing losses caused by delays or manual inefficiencies. For instance, modern harvesters can cover up to 20 acres per hour, as per Purdue University, significantly improving productivity compared to traditional methods. This capability is particularly crucial in regions like Iowa and Illinois, which produce over 30% of the U.S. corn supply.

Adoption of Precision Agriculture Technologies

The integration of precision agriculture technologies into combine harvesters is another major driver, transforming the way crops are harvested and managed. According to the Association for Unmanned Vehicle Systems International (AUVSI), precision agriculture technologies are expected to generate $32 billion in annual revenue by 2030, with combine harvesters being a critical component. Modern harvesters equipped with GPS, yield mapping, and real-time data analytics allow farmers to optimize field operations, reduce fuel consumption, and enhance crop quality. For example, John Deere’s latest models feature automated steering systems that reduce overlap during harvesting, saving up to 10% in fuel costs, as reported by the University of Nebraska-Lincoln. These innovations appeal to tech-savvy farmers seeking to maximize yields while minimizing environmental impact. Furthermore, government incentives promoting sustainable farming practices have encouraged the adoption of such technologies, particularly in Canada, where the Agricultural Climate Solutions program supports investments in precision machinery.

MARKET RESTRAINTS

High Initial Investment Costs

One of the most significant barriers to the widespread adoption of combine harvesters in North America is their high initial cost. According to the USDA Economic Research Service, the average price of a new self-propelled combine harvester ranges from 300,000 to 500,000, depending on specifications and brand. This financial burden is particularly challenging for small and medium-sized farms, which constitute approximately 90% of all U.S. farms, as stated by the National Sustainable Agriculture Coalition. While leasing options and financing programs exist, they often come with interest rates that further strain budgets. Additionally, the costs associated with maintenance, spare parts, and operator training add to the overall expense. For instance, a study by Kansas State University found that annual maintenance costs for high-end models can exceed $15,000, deterring many farmers from upgrading to newer technologies.

Limited Awareness Among Small-Scale Farmers

Another key restraint is the limited awareness and technical knowledge about advanced combine harvesters among small-scale and traditional farmers. A survey conducted by the National Farmers Union reveals that nearly 40% of farmers in the Southeastern U.S. are either unfamiliar with the latest technological advancements in combine harvesters or perceive them as overly complex to operate. This knowledge gap is exacerbated by insufficient outreach programs and training initiatives tailored to the needs of local farming communities. In Canada, a study by the Canadian Federation of Agriculture found that only 25% of small-scale farmers in Atlantic provinces had received formal training on modern harvesting equipment. Without adequate education and demonstration of the machine's benefits, farmers remain reluctant to transition from older models or manual methods.

MARKET OPPORTUNITIES

Integration with Autonomous Farming Solutions

The integration of autonomous farming solutions presents a transformative opportunity for the North American combine harvester market. Innovations such as driverless combine harvesters and remote operation capabilities are gaining traction as labor shortages persist across the agricultural sector. According to the American Farm Bureau Federation, the U.S. agricultural industry faces a labor shortfall of approximately 20%, with many farmers struggling to find skilled operators for heavy machinery. Autonomous combine harvesters, equipped with AI and machine learning algorithms, can address this issue by performing tasks with minimal human intervention. For instance, Case IH’s autonomous concept harvester has demonstrated the ability to navigate fields and adjust settings based on real-time data. These advancements not only enhance operational efficiency but also reduce dependency on manual labor, which is making them particularly appealing in labor-scarce regions like California and Texas.

Expansion into Rental and Leasing Models

The growing popularity of rental and leasing models offers another lucrative opportunity for the North American combine harvester market. For example, companies like AgDirect and CNH Industrial have introduced tailored leasing programs that allow farmers to access state-of-the-art harvesters without significant capital investment. These models also cater to seasonal farming operations by enabling farmers to rent equipment only during peak harvest periods. Furthermore, rental services facilitate the adoption of cutting-edge technologies, as farmers can experiment with advanced models without long-term commitments. This shift toward accessibility ensures broader market penetration and aligns with the evolving needs of diverse farming communities.

MARKET CHALLENGES

Rapid Technological Obsolescence

A significant challenge facing the North American combine harvester market is the rapid pace of technological obsolescence. As manufacturers continuously introduce advanced features such as AI-driven analytics, IoT connectivity, and enhanced automation, older models quickly become outdated. According to the American Society of Agricultural and Biological Engineers, the average lifespan of a combine harvester with cutting-edge technology is shrinking to just 5-7 years, when compared to 10-15 years for traditional models. This accelerated obsolescence poses a dilemma for farmers who must balance the need for innovation with the financial burden of frequent upgrades. For instance, a study by Iowa State University found that over 60% of farmers delay adopting new technologies due to concerns about return on investment. Additionally, the lack of standardized components across brands complicates repairs and upgrades, further exacerbating the issue. Addressing this challenge requires manufacturers to offer more flexible upgrade paths and emphasize the long-term value of their products.

Environmental Concerns and Regulatory Pressures

Another pressing challenge is the increasing scrutiny on the environmental impact of agricultural machinery, including combine harvesters. Regulatory bodies like the Environmental Protection Agency (EPA) have imposed stringent emissions standards, which require manufacturers to develop cleaner engines and more energy-efficient designs. According to the EPA, non-road diesel engines, commonly used in agricultural equipment, must comply with Tier 4 emissions regulations, which mandate a 90% reduction in particulate matter and nitrogen oxides. While these measures aim to mitigate environmental harm, they increase production costs and complexity for manufacturers. According to a report by the University of Missouri, compliance with Tier 4 standards has raised the cost of engine development by up to 30%. Additionally, public concerns about soil compaction and habitat disruption caused by heavy machinery further pressure manufacturers to innovate. Navigating these regulatory and environmental challenges remains a critical task for industry players striving to maintain sustainability and profitability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.1% |

| Segments Covered | By Product, Class, and Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | The USA, Canada, Mexico, andthe Country |

| Market Leaders Profiled | AGCO, CLAAS, CNH Industrial, Deere & Company, Dewulf, Kubota Agricultural Machinery, Kuhn Group, Lely Group, Lovol Heavy Industry, Ploeger, Pottinger, Preet Group, SDF, Sampo Rosenlew |

SEGMENTAL ANALYSIS

By Product Insights

The self-propelled segment is expected to hold a dominant share of the North American combine harvester market in 2024 due to its unmatched efficiency and versatility in handling large-scale farming operations. According to Purdue University, self-propelled models can cover up to 20 acres per hour, which is making them indispensable for high-yield crops like corn and soybeans, which are central to North American agriculture. The USDA estimates that over 80% of large farms in the Midwest rely on self-propelled harvesters due to their ability to reduce labor costs and minimize crop wastage during peak harvesting seasons. Additionally, advancements in technology, such as GPS-guided navigation and real-time yield mapping, have amplified the growth of the segment.

The PTO-powered (Power Take-Off) segment is expected to grow with a CAGR of 6.8% in the coming years, owing to their affordability and suitability for small-scale farmers who cannot justify the high costs of self-propelled models. Additionally, their compatibility with existing tractors allows farmers to maximize the utility of their current equipment. For example, in regions like the Southeastern U.S., where small farms dominate, PTO-powered harvesters have seen a 25% increase in adoption over the past five years, as stated by the National Farmers Union.

By Class Insights

The Class 7 segment held 40.3% of the North America combine harvest market share in 2024 due to their optimal balance of power, capacity, and versatility, making them ideal for medium to large-scale farming operations. Additionally, manufacturers like Case IH and AGCO have introduced advanced features such as precision farming integration and enhanced grain-handling capabilities, further boosting their popularity.

The class 9 combine harvesters segment is lucratively growing with a CAGR of 8.2% in the coming years, owing to the increasing demand for ultra-high-capacity machines capable of handling large-scale industrial farming operations. According to the USDA Economic Research Service, Class 9 harvesters, equipped with engines exceeding 500 horsepower, are becoming essential for mega-farms in states like Illinois and Indiana, where average farm sizes exceed 1,000 acres. Additionally, the integration of autonomous technologies, such as AI-driven analytics and remote operation capabilities, has further enhanced their appeal.

COUNTRY ANALYSIS

Top Countries In The Market

The United States was positioned top by holding 85.6% of the North American combine harvester market share in 20,24, owing to the country’s vast agricultural landscape, spanning diverse regions like the Midwest and the North Great Plains, which creates a fertile ground for the adoption of advanced harvesting technologies. States like Iowa and Illinois, known as major corn and soybean producers, have embraced self-propelled and high-capacity harvesters to meet global food demands. According to the American Farm Bureau Federation, U.S. farmers produce over 380 million metric tons of corn annually, relying heavily on combine harvesters for efficient collection. Federal programs like the Environmental Quality Incentives Program (EQIP) provide subsidies for machinery upgrades, encouraging the adoption of eco-friendly models. These initiatives ensure that the U.S. remains the epicenter of innovation and growth in the combine harvester market.

Canada's combine harvester market was next with 12.3% of the North American combine harvester market share in 2024. The country’s expansive prairies, particularly in Alberta and Saskatchewan, are key contributors to its wheat and barley production, driving demand for reliable harvesting equipment. The Canadian Federation of Agriculture reports that over 60% of grain farmers in Western Canada use combine harvesters, with a growing preference for technologically advanced models. Government initiatives like the Agricultural Climate Solutions program promote sustainable farming practices, encouraging investments in energy-efficient machinery. These efforts position Canada as a significant player in advancing combine harvester technologies.

COMPETITIVE LANDSCAPE

The North American combine harvester market is highly competitive, characterized by the presence of both multinational corporations and regional players striving to differentiate themselves through innovation and customer-centric strategies. Leading companies leverage their technological expertise and robust distribution networks to maintain dominance, while smaller firms focus on niche markets and localized solutions. The market’s dynamics are shaped by increasing demand for precision agriculture technologies, regulatory pressures on emissions, and the push for sustainable farming practices. Collaborations with agtech startups and government initiatives play a crucial role in shaping industry trends, fostering advancements in automation and eco-friendly machinery. Despite intense rivalry, collaboration among players is common, particularly in research initiatives aimed at developing next-generation harvesting solutions. This blend of competition and cooperation underscores the market’s dynamic nature, which is driving innovation and growth across the region.

KEY MARKET PLAYERS

These are some of the market players that dominate the North American combine harvester market.

- AGCO

- CLAAS

- Case IH

- CNH Industrial

- John Deere

- Deere & Company

- Dewulf

- Kubota Agricultural Machinery

- Kuhn Group

- Lely Group

- Lovol Heavy Industry

- Ploeger

- Pottinger

- Preet Group

- SDF

- Sampo Rosenlew

Top Players In The Market

- John Deere is a global leader in agricultural machinery, renowned for its innovative combine harvesters that cater to diverse farming needs. The company’s commitment to precision agriculture has positioned it at the forefront of technological advancements, with features like GPS integration and AI-driven analytics enhancing operational efficiency. John Deere’s extensive distribution network and customer-centric approach ensure widespread accessibility in large-scale farming regions like the Midwest.

- Case IH is a prominent player known for its high-capacity combine harvesters designed to meet the demands of industrial farming operations. The company emphasizes innovation through partnerships with agtech startups, integrating IoT-enabled sensors and real-time data monitoring into its machinery. Case IH’s focus on versatility ensures its products are suitable for a wide range of crops, from corn to wheat. Additionally, its commitment to customer education and training programs fosters trust and loyalty among farmers.

- CLAAS is celebrated for its engineering excellence and cutting-edge combine harvester models that prioritize efficiency and durability. The company’s emphasis on sustainability is evident in its development of eco-friendly machinery, including biofuel-compatible engines and low-emission designs. CLAAS’s strong presence in North America is bolstered by its ability to cater to both small-scale and large-scale farmers, offering tailored solutions for diverse agricultural needs. Its focus on precision farming technologies, such as automated steering systems and yield mapping, positions CLAAS as a leader in advancing agricultural productivity. These innovations contribute significantly to the global adoption of advanced harvesting equipment.

Top Strategies Used By Key Players In The Market

Technological Innovation and Automation

Leading companies are investing heavily in developing autonomous and semi-autonomous combine harvesters equipped with AI, machine learning, and IoT capabilities. These innovations aim to address labor shortages and enhance operational efficiency. By integrating features like real-time data analytics and remote operation, manufacturers cater to the growing demand for precision agriculture solutions by ensuring their products remain competitive in a rapidly evolving market.

Expansion of Distribution Networks and After-Sales Services

To strengthen their market presence, key players are expanding their distribution networks and service centers, particularly in underserved regions. Offering comprehensive after-sales services, including maintenance, spare parts availability, and operator training, helps build long-term customer relationships. This strategy not only enhances brand loyalty but also ensures seamless adoption of advanced machinery by farmers.

Sustainability and Eco-Friendly Solutions

Manufacturers are increasingly focusing on sustainability to align with regulatory pressures and consumer preferences. By introducing biofuel-compatible engines, low-emission designs, and energy-efficient models, companies position themselves as leaders in environmentally responsible practices.

RECENT MARKET NEWS

- In April 2024, John Deere acquired an agtech startup specializing in AI-driven analytics for agricultural machinery. This acquisition is anticipated to allow John Deere to integrate advanced predictive capabilities into its combine harvesters by enhancing operational efficiency and strengthening its market presence.

- In July 2023, Case IH partnered with a Canadian precision farming solutions provider to develop IoT-enabled sensors for its Class 9 harvesters. This collaboration aims to improve real-time data monitoring and optimize field operations for large-scale farmers.

- In November 2023, CLAAS introduced a biofuel-compatible engine for its mid-range combine harvesters, aligning with regulatory pressures to reduce emissions. This move positions CLAAS as a pioneer in sustainable machinery and appeals to environmentally conscious consumers.

- In January 2024, AGCO expanded its rental program for combine harvesters, targeting small-scale farmers in the Southeastern U.S. This initiative is expected to provide affordable access to advanced machinery and expand AGCO’s customer base.

- In August 2023, CNH Industrial established new service centers in agricultural hubs like Culiacán, Mexico. This expansion is anticipated to tap into the growing demand for harvesting equipment in the region and strengthen CNH’s foothold in Latin America.

MARKET SEGMENTATION

The North America Combine Harvester Market is segmented and sub-segmented into the following categories.

By Product

- Self-Propelled

- Tractor Pulled

- PTO Powered

By Classes 4 and 5

- Class 6

- Class 7

- Class 8

- Class 9

- Class 10

By Country

- USA

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

Why are combine harvesters essential for large-scale farming in North America?

They allow harvesting, threshing, and grain separation to happen in one continuous operation.

What drives farmers to upgrade combines instead of repairing older machines?

New models improve fuel efficiency and reduce harvest-time downtime risks.

How does harvest timing influence combine harvester demand?

Short harvesting windows require reliable machines capable of covering large acreage quickly.

Why are precision agriculture features becoming standard in combines?

Farmers rely on yield data collected during harvesting to guide future planting decisions.

What advantage do larger grain tanks provide to operators?

They reduce unloading frequency and improve field productivity.

How does automation assist combine operators during long harvest days?

Guidance systems reduce fatigue by maintaining accurate field alignment automatically.

Why are North American farms suited for high-capacity harvesters?

Extensive field sizes make large machines more economically efficient.

How do weather uncertainties affect combine purchasing decisions?

Farmers prioritize machines that can harvest quickly before adverse weather damages crops.

What role does dealer support play in equipment selection?

Reliable service availability is critical during time-sensitive harvest seasons.

Why are data-monitoring systems valuable in modern combines?

Real-time performance tracking helps optimize machine settings while operating.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com