North America Digital Camera Market Size, Share, Trends & Growth Forecast Report By Lens (Built-in, Interchangeable), Product, End-Use, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2024 to 2033

North America Digital Camera Market Size

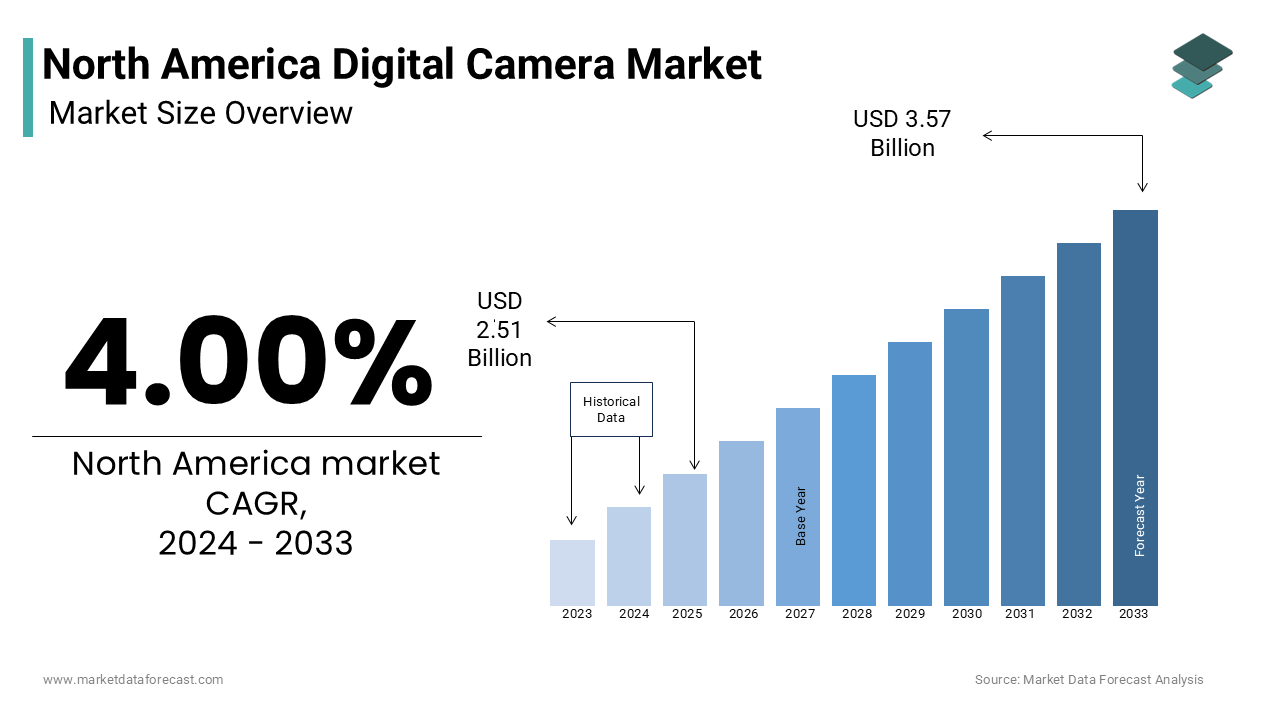

In 2024, the North America digital camera market was valued at USD 2.51 billion and is forecasted to grow to USD 3.57 billion by 2033, at a CAGR of 4.00%.

The digital camera devices include DSLRs (Digital Single-Lens Reflex), mirrorless cameras, compact point-and-shoot models, and action cameras tailored for both professional and consumer use. The market has undergone a structural transformation over the past decade, driven by technological advancements and shifting consumer behavior. While smartphone integration has significantly reduced demand for entry-level digital cameras, high-end models continue to find relevance among professional photographers, content creators, and niche industries such as real estate, cinematography, and industrial imaging. As of 2024, the U.S. remains the dominant contributor within the region, accounting for over 85% of total unit sales. According to data from the Consumer Technology Association, approximately 3.2 million digital cameras were sold in the U.S. in 2023, with an average selling price exceeding $750, indicating a shift toward premium product categories. Meanwhile, Canada’s digital camera market reported a year-over-year growth of 1.7% in 2023, driven largely by increased adoption among freelance videographers and small-scale media houses. The presence of major manufacturers like Canon, Sony, and Nikon, alongside robust after-sales services and repair networks, further supports market resilience despite broader headwinds.

MARKET DRIVERS

Growth of Content Creation and Influencer Marketing

The surge in digital content creation has become a pivotal driver for the North America digital camera market. With the proliferation of social media platforms such as YouTube, Instagram, TikTok, and Twitch, there is a growing need for high-quality visual output that surpasses the capabilities of standard smartphone cameras. As per a report published by Edison Research, over 60 million Americans identified themselves as active content creators in 2023, representing a 22% increase compared to the previous year. This expanding creator ecosystem fuels demand for advanced digital cameras that offer superior resolution, low-light performance, and manual control features.

Additionally, the rise of influencer marketing has intensified the need for professional-grade equipment. A study by Statista revealed that U.S.-based brands allocated over $4.6 billion to influencer marketing campaigns in 2023, up from $3.9 billion in 2022. High-resolution visuals and cinematic video quality are now prerequisites for brand collaborations, prompting influencers to invest in interchangeable lens systems and mirrorless cameras. For instance, Sony’s Alpha series and Canon’s EOS R line have seen significant traction among this demographic due to their portability, fast autofocus, and 4K video capabilities.

Expansion of Professional Photography Services

The professional photography is propelling the growth of the North America digital camera market in commercial sectors such as real estate, fashion, journalism, and event coverage. Real estate agents, for example, increasingly rely on high-resolution imagery and virtual tours to showcase properties, which is leading to a corresponding rise in investment in DSLR and mirrorless systems. Moreover, the wedding and event photography segment remains robust. The Wedding Report estimated that over 2.1 million weddings took place in the U.S. in 2023, each typically requiring multiple photographers equipped with professional-grade cameras. Additionally, the news media sector, though facing challenges, still depends heavily on photojournalists using rugged and high-performance digital cameras to capture breaking stories.

MARKET RESTRAINTS

Proliferation of Smartphone Cameras with Advanced Imaging Capabilities

The rapid advancement of smartphone camera technology is restraining the growth of the North America digital camera market. Leading mobile manufacturers such as Apple, Samsung, and Google have integrated sophisticated imaging sensors, multi-lens setups, and AI-driven computational photography into their latest flagship models. This technological convergence has led to a notable decline in casual photography purchases. The U.S. Department of Commerce reported that digital camera shipments to retail outlets dropped by 11.3% in 2023 compared to the prior year, while smartphone sales rose by 5.8%. Consumers are increasingly opting for convenience and multifunctionality offered by smartphones, especially for travel, family events, and day-to-day documentation.

Economic Uncertainty and Declining Disposable Incomes

The economic volatility in North America has had a dampening effect on discretionary spending, including purchases of digital cameras, which is slowly hindering the growth of the North America digital camera market. Inflationary pressures, rising interest rates, and fluctuating employment conditions have collectively constrained consumer purchasing power. According to the Federal Reserve Economic Data (FRED), the U.S. personal savings rate fell to 3.9% in December 2023, down from 6.5% at the start of the year, signaling tighter household budgets. Moreover, the cost of high-end digital cameras, which often exceed $1,000, has placed them out of reach for many budget-conscious buyers. A Nielsen survey conducted in early 2024 found that only 14% of American households planned to purchase a digital camera within the next 12 months, down from 21% in 2022. This trend is further exacerbated by the availability of used and refurbished models, which although extend affordability, also reduce reliance on new camera purchases.

MARKET OPPORTUNITIES

Integration of AI and Machine Learning in Camera Systems

The incorporation of artificial intelligence (AI) and machine learning (ML) into digital cameras presents a transformative opportunity for the North America market. Modern cameras are increasingly embedded with AI-based processors that enhance autofocus precision, optimize exposure settings in real-time, and enable intelligent subject tracking. For example, Sony’s latest Alpha 7 IV model utilizes AI to recognize and focus on human eyes, animals, and vehicles with remarkable accuracy by improving usability for both professionals and enthusiasts. The integration of AI not only enhances image quality but also streamlines post-processing workflows by reducing editing time for photographers. Manufacturers are also leveraging AI to develop smart camera ecosystems that sync seamlessly with cloud storage and editing software. Canon’s integration of its AI-enhanced image management platform with Adobe Creative Cloud exemplifies this trend.

Rising Demand for Action and Drone Cameras in Adventure and Commercial Applications

The growing popularity of adventure sports, drone photography, and aerial videography has created a lucrative opportunity for expansion within the North America digital camera market. Action cameras, particularly those produced by GoPro and DJI, have gained widespread acceptance among outdoor enthusiasts and professional filmmakers alike. Drone-mounted cameras have also seen increased deployment across commercial sectors such as agriculture, construction, and infrastructure inspection. A report from Drone Industry Insights indicated that over 850,000 drones were registered in the U.S. in 2023, with more than 60% of them equipped with high-resolution digital imaging systems. Additionally, the entertainment industry’s reliance on aerial footage for film and television production has further fueled demand. Netflix and Disney+ have incorporated extensive drone-shot sequences in their original content, which is boosting demand for compatible digital camera modules.

MARKET CHALLENGES

Supply Chain Disruptions and Component Shortages

The supply chain instability is a challenging factor for the North America digital camera market players. The semiconductor shortage that began during the pandemic has evolved into a more complex issue involving logistics bottlenecks, geopolitical tensions, and raw material scarcity. According to the Semiconductor Industry Association, global chip inventories remained below pre-pandemic levels throughout 2023, directly impacting the manufacturing capacity of digital cameras that rely on advanced image sensors and processors. Camera manufacturers such as Nikon and Fujifilm faced extended lead times for essential components like CMOS sensors and lens elements, delaying product launches and affecting inventory levels. The U.S. Census Bureau reported that import delays at major ports, including Los Angeles and Long Beach, added an average of 14 days to component delivery times in 2023. Moreover, inflation in freight and energy prices has compounded the problem. The Drewry World Container Index recorded a 22% increase in shipping costs between Q1 2023 and Q4 2023, further straining operational margins. These disruptions not only hinder timely product availability but also deter potential buyers who perceive inconsistent supply as a risk factor.

Regulatory and Environmental Compliance Pressures

The environmental regulations and sustainability mandates are emerging as formidable challenges for digital camera manufacturers operating in North America. Governments and environmental agencies are imposing stricter guidelines regarding electronic waste (e-waste), energy efficiency, and hazardous materials used in electronics. In 2023, California updated its Electronic Waste Recycling Act, mandating that manufacturers meet specific recycling targets and phase out certain flame retardants and heavy metals commonly used in older camera models. Additionally, the U.S. Environmental Protection Agency (EPA) has introduced new Energy Star certification criteria for consumer electronics, including digital cameras, requiring them to consume less power during both active and standby modes. Companies like Canon and Sony have responded by launching trade-in programs and investing in closed-loop recycling initiatives.

REGIONAL ANALYSIS

By Lens Type Insights

The interchangeable lens segment was accounted in holding a dominant share of the North America digital camera market in 2024 due to the growing preference among professional and advanced amateur photographers who require versatility in capturing different subjects and environments. The demand from professional photographers across various industries such as fashion, real estate, and media production is also to boost the growth of the segment. Additionally, the rise of hybrid content creators those who blend professional and personal media output has further reinforced the need for customizable equipment. Manufacturers like Canon and Sony have responded by expanding their lens ecosystems, offering over 50 native lens variants each for their respective full-frame mirrorless platforms.

The built-in lens segment is projected to grow with a CAGR of 9.6% during the forecast period with the rising popularity of fixed-lens mirrorless and bridge-style cameras tailored for travel, vlogging, and street photography. These devices offer a balance between portability and performance, appealing to users who seek higher image quality than smartphones can provide without the bulk of an interchangeable system. One of the leading contributors to this trend is the adoption of these cameras by social media influencers and solo content creators who require lightweight yet capable gear. For example, Fujifilm’s X100 series and Sony’s RX100 line have gained traction due to their retro aesthetics, fast autofocus, and seamless integration with editing software. Moreover, the resurgence of film-inspired digital photography has spurred interest in compact fixed-lens systems that mimic analog shooting experiences.

By End-use Insights

The professional photographers segment was accounted in holding 48.3% of the North America digital camera market share in 2024. According to the Bureau of Labor Statistics, there were over 134,000 employed photographers in the U.S. in 2023, with a notable portion engaged in fields such as real estate, wedding documentation, journalism, and product imaging. A report by the National Association of Realtors indicated that 89% of homebuyers considered professionally photographed listings more appealing, prompting real estate agents to invest in premium camera setups. Additionally, the event photography sector remained robust, with over 2.1 million weddings recorded in the U.S. in 2023, as per The Wedding Report. Moreover, the news and media industry continues to depend on photojournalists utilizing rugged, high-speed digital cameras for field reporting. According to a survey by the Professional Photographers of America, 78% of professionals upgraded or purchased new camera bodies between 2022 and 2023, demonstrating ongoing investment in top-tier equipment.

The prosumers enthusiast-level photographers who operate between casual hobbyists and full-time professionals—are emerging as the fastest-growing segment in the North America digital camera market, projected to expand at a compound annual growth rate (CAGR) of 11.2% from 2023 to 2030. This rapid growth is fueled by the increasing number of individuals engaging in semi-professional photography through online platforms, freelance work, and personal branding efforts.

The prosumers segment is likely to grow with an expected CAGR of 11.2% in the next coming years. According to Edison Research, over 60 million Americans identified themselves as active content creators in 2023, many of whom fall into the prosumer category. These individuals often require more advanced features than smartphones can provide but may not yet justify the cost or complexity of full professional-grade systems. Furthermore, the monetization of personal content channels has encouraged prosumers to invest in better equipment. Many micro-influencers and YouTubers categorized under prosumers rely on digital cameras to produce visually compelling content that meets brand expectations. As per a DPReview survey conducted in early 2024, 41% of respondents planning to upgrade their gear cited improved video capabilities and portability as primary motivators.

REGIONAL ANALYSIS

United States Digital Camera Market Insights

The United States was the largest contributor with 86.4% of the North America digital camera market share in 2024 with well-established photography ecosystem, strong presence of major manufacturers, and a large base of both professional and enthusiast photographers. As per the National Association of Realtors, 89% of homebuyers preferred listings with professionally captured images, which is reinforcing demand for high-resolution cameras among realtors. Additionally, the entertainment industry’s reliance on visual storytelling has maintained a steady demand for high-end imaging equipment. Moreover, the prosumer segment is rapidly expanding, driven by content creators leveraging platforms like YouTube, Instagram, and TikTok. Edison Research noted that over 60 million Americans identified as active content creators in 2023, many of whom invested in mirrorless and hybrid cameras for superior image quality.

Canada Digital Camera Market Insights

Canada digital camera market held 12.3% of share in 2024 with the increasing number of independent videographers and small-scale content creators entering the digital space. A survey conducted by the Canadian Media Producers Association found that over 14,000 freelancers were actively producing digital content in 2023, many of whom required professional-grade cameras for client projects. The utilization of digital cameras in scientific research and environmental monitoring is ascribed to fuel the growth of the market in this country. Environment and Climate Change Canada reported that drone-based surveillance and wildlife tracking initiatives expanded by 18% in 2023, necessitating the deployment of high-resolution imaging equipment.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

The key players in the North America Digital Camera Market include Canon Inc., Nikon Corporation, Sony Corporation, Panasonic Corporation, Fujifilm Holdings Corporation, Olympus Corporation, Leica Camera AG, and GoPro Inc.

The competition in the North America digital camera market is highly consolidated, with a few global giants dominating the landscape. Companies like Canon, Sony, and Nikon continue to lead due to their long-standing reputations, technological expertise, and strong brand recognition. However, emerging challengers such as Fujifilm, Panasonic, and Olympus are gaining traction by focusing on niche segments like retro-styled mirrorless cameras and hybrid photo-video devices. The market is witnessing increased rivalry as manufacturers strive to retain relevance amid declining consumer demand, largely attributed to the rise of smartphone photography. Additionally, the growing influence of prosumers and content creators has prompted companies to tailor products that bridge the gap between professional-grade performance and consumer accessibility.

Top Players in the North America Digital Camera Market

Canon Inc.

Canon is a dominant player in the North America digital camera market, known for its extensive lineup of DSLR and mirrorless cameras tailored to both professionals and enthusiasts. The company consistently innovates with advanced imaging sensors, dual-pixel autofocus technology, and seamless integration with professional workflows. Canon’s strong distribution network, coupled with its reputation for reliability and image quality will expand its portfolio. Its RF lens ecosystem continues to expand by reinforcing brand loyalty among photographers seeking high-performance optics.

Sony Corporation

Sony has emerged as a key player by pioneering mirrorless camera technology and capturing a significant share of the enthusiast and prosumer markets. Its Alpha series is widely acclaimed for superior video capabilities, fast processing speeds, and compact form factors. Sony's commitment to full-frame sensors and AI-driven autofocus has made its cameras a favorite among content creators and videographers. The company also invests heavily in R&D to enhance connectivity and integrate cloud-based workflows, which is strengthening its appeal across creative industries.

Nikon Corporation

Nikon maintains a strong presence in North America through its Z-mount mirrorless system, which offers cutting-edge performance for professional photographers and serious hobbyists. The company emphasizes optical excellence, durable build quality, and user-friendly interfaces. Nikon continues to evolve its product line by introducing models that cater to both still photography and video production. Its legacy in the industry, combined with strategic partnerships and after-sales support that ensures continued relevance in a competitive landscape.

Top Strategies Used by Key Market Participants

Product Innovation and Technological Advancement

Leading players continuously invest in research and development to introduce next-generation cameras featuring enhanced sensors, faster autofocus systems, and improved video capabilities. These innovations help differentiate their offerings in a mature market and attract discerning users who prioritize performance over convenience.

Expansion of Ecosystem and Accessories

Manufacturers are expanding their lens lineups, battery options, and compatible software to create comprehensive ecosystems. Companies encourage brand loyalty and reduce the likelihood of customers switching platforms by offering a wide range of accessories and integrated solutions.

Strengthening Online Presence and Direct Engagement

Major brands are enhancing their e-commerce platforms and engaging directly with consumers through social media, tutorials, and community forums with shifting consumer behavior toward digital purchasing channels. This approach not only boosts visibility but also fosters customer retention through personalized experiences and post-purchase support.

RECENT MARKET DEVELOPMENTS

- In February 2024, Canon launched an expanded version of its RF lens lineup, introducing three new prime lenses designed specifically for portrait and low-light photography. This expansion aimed at reinforcing its ecosystem and encouraging existing users to stay within the Canon platform while attracting new customers seeking versatile optics.

- In May 2024, Sony introduced a new firmware update for its Alpha 7 IV series that significantly enhanced real-time tracking and AI-based subject recognition. This move was intended to improve user experience and maintain its stronghold among professional videographers and hybrid content creators in the North American market.

- In July 2024, Nikon announced a partnership with a leading U.S.-based photography education platform to offer bundled learning packages with select camera models. This initiative was designed to engage aspiring photographers and increase adoption of the Z-mount system among entry-level and intermediate users.

- In September 2024, Fujifilm unveiled a limited edition variant of its X100VI model, inspired by vintage film cameras, targeting enthusiasts and lifestyle-oriented photographers. This launch was part of a broader strategy to capture attention in the premium fixed-lens segment and strengthen brand identity in North America.

- In November 2024, Panasonic collaborated with Adobe to integrate its Lumix S-series cameras with Creative Cloud workflows more seamlessly. The goal was to streamline post-processing for creators and enhance the appeal of Panasonic’s full-frame mirrorless lineup among video-first content producers.

MARKET SEGMENTATION

This research report on the North American digital camera market is segmented and sub-segmented based on categories.

By Lens

- Built-in

- Interchangeable

By Product

- Compact Digital Camera

- DSLR

- Mirrorless

By End Use

- Pro Photographers

- Prosumers

- Hobbyists

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What is driving the digital camera market in North America?

The market is driven by the demand for high-resolution imaging, growing content creation trends (vlogging, social media), and professional photography needs.

What challenges does the market face?

Challenges include smartphone camera competition, high cost of advanced digital cameras, and market saturation.

What is the future outlook of the digital camera market in North America?

The market is expected to remain stable, with niche growth in premium, mirrorless, and professional camera segments due to demand for superior imaging and video quality.

What are the latest trends shaping the digital camera market in North America?

Key trends include the shift from DSLR to mirrorless cameras, integration of AI-powered features, growing demand for 4K/8K video recording, and enhanced connectivity options like Wi-Fi and Bluetooth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com