North America Food Allergen Testing Market Size, Share, Trends & Growth Forecast Report By Source (Peanuts & Soy, Wheat, Milk, Eggs, Tree Nuts, Seafood), Technology, Food Tested, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2025 to 2033

North America Food Allergen Testing Market Summary

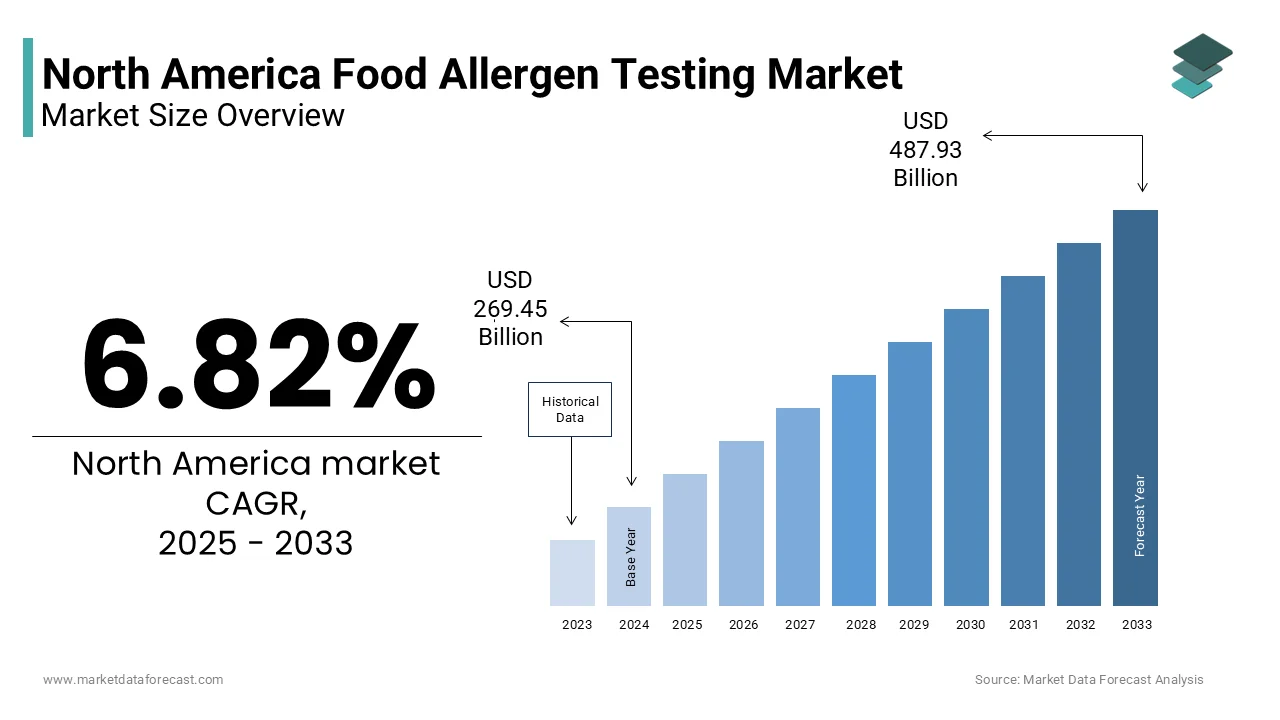

The North America food allergen testing market size was estimated at USD 269.45 billion in 2024 and is projected to reach USD 487.93 billion by 2033, growing at a CAGR of 6.82% from 2025 to 2033. The key driver fueling the growth of the North America Food Allergen Testing Market is the implementation of stringent regulatory frameworks and mandatory allergen labeling laws.

Key Market Trends & Insights

The U.S. led North America's food allergen testing market with 75.4% share in 2024.

Canada has strong allergen laws and growing focus on food risk mitigation.

Based on source, the milk segment held the largest share in the North America food allergen testing market.

Based on technology, ELISA technology dominated North America’s allergen testing market at 45.6% in 2024.

Market Size & Forecast

2024 Market Size: USD 269.45 Billion

2033 Projected Market Size: USD 487.93 Billion

CAGR (2025-2033): 6.82%

United States: Largest market in 2024

Canada: Fastest growing market

North America Food Allergen Testing Market Size

The Food Allergen Testing market size in North America was valued at USD 269.45 billion in 2024 and is predicted to be worth USD 487.93 billion by 2033, at a CAGR of 6.82%.

Food allergen testing refers to the analytical procedures used to detect and quantify specific allergenic proteins in food products. This process is critical for ensuring consumer safety, particularly for individuals with food allergies, and for complying with regulatory labeling requirements. In North America, food allergen testing has become a cornerstone of food safety protocols across manufacturing, processing, and retail sectors.

The market covers a range of technologies such as enzyme-linked immunosorbent assay (ELISA), polymerase chain reaction (PCR), lateral flow devices, and mass spectrometry. These methods help identify common allergens like milk, eggs, peanuts, tree nuts, soy, wheat, fish, and shellfish.

Like, according to the Centers for Disease Control and Prevention (CDC), approximately 4 to 6 percent of children in the U.S. suffer from food allergies, contributing to an increased demand for accurate allergen detection systems. Similarly, as per data published by FARE (Food Allergy Research & Education), over 32 million Americans have food allergies, including nearly 5.6 million under the age of 18.

Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and Health Canada mandate clear labeling of allergenic ingredients. So, food producers are investing heavily in robust allergen control measures.

MARKET DRIVERS

Rising Prevalence of Food Allergies Among Children and Adults

Among the most significant drivers of the North America Food Allergen Testing Market is the increasing prevalence of food allergies among both children and adults.

Likewise, according to the Centers for Disease Control and Prevention (CDC), food allergies among children in the U.S. increased by approximately 50% between 1997 and 2011. Also, more recent data from FARE (Food Allergy Research & Education) indicates that over 32 million Americans live with food allergies, including nearly 5.6 million children under the age of 18. This sharp rise in allergic conditions has heightened public awareness and regulatory scrutiny around food labeling and contamination.

As a result, food manufacturers are under pressure to ensure their products are accurately labeled and free from cross-contamination. According to the FDA, undeclared allergens remain one of the leading causes of food recalls in the United States. For instance, in 2022 alone, the FDA recorded over 200 food recalls related to undeclared allergens, many of which involved major brands. These incidents underscore the urgent need for advanced allergen testing solutions across the supply chain.

In response, companies are increasingly adopting rapid and sensitive detection technologies such as ELISA and PCR-based assays to meet quality assurance standards. The growing demand for safe food products, combined with stricter regulatory enforcement, is driving innovation and investment in the food allergen testing sector across North America.

Stringent Regulatory Frameworks and Labeling Requirements

Another key driver fueling the growth of the North America Food Allergen Testing Market is the implementation of stringent regulatory frameworks and mandatory allergen labeling laws. Both the U.S. Food and Drug Administration (FDA) and Health Canada enforce comprehensive guidelines requiring food manufacturers to clearly declare the presence of major allergens on product labels.

The Food Allergen Labeling and Consumer Protection Act (FALCPA), enacted in 2006, mandates the disclosure of the eight most common allergens—milk, eggs, fish, crustacean shellfish, tree nuts, peanuts, wheat, and soybeans—on packaged foods sold in the U.S.

According to the FDA, failure to comply with these regulations can lead to severe consequences, including product recalls, financial penalties, and legal action. In fact, as per the FDA’s Recall Enterprise System, allergen-related recalls accounted for more than 40% of all food recalls in recent years. This trend underscores the critical role of allergen testing in risk mitigation and brand protection.

Moreover, the Canadian Food Inspection Agency (CFIA) maintains rigorous allergen control policies, requiring food producers to implement preventive controls and undergo regular audits. So, food processors are investing heavily in advanced allergen testing technologies to ensure compliance and maintain consumer trust.

MARKET RESTRAINTS

High Cost of Advanced Testing Technologies and Equipment

A notable restraint impeding the growth of the North America Food Allergen Testing Market is the high cost associated with advanced testing technologies and equipment. Sophisticated methods such as polymerase chain reaction (PCR) and mass spectrometry require substantial capital investment, not only in instrumentation but also in trained personnel, maintenance, and consumables.

This economic barrier limits widespread adoption, especially among smaller manufacturers who rely on cost-effective alternatives such as rapid test kits. While these kits are more affordable, they may lack the sensitivity and accuracy required for detecting trace allergens. As per the U.S. Department of Agriculture (USDA), SMEs account for a significant portion of the food production sector, yet many struggle to integrate advanced allergen testing into their quality control processes due to budget constraints.

Also, ongoing operational costs—including reagents, calibration, and staff training—further strain limited resources. Consequently, despite the regulatory imperative for precise allergen detection, cost considerations continue to hinder full-scale implementation of high-end testing solutions across the industry.

Lack of Standardization Across Testing Methods and Protocols

Another significant restraint affecting the North America food allergen testing market is the lack of standardization across testing methods and protocols. Various laboratories and food manufacturers employ different techniques—ranging from ELISA to PCR to lateral flow assays—each with its own detection thresholds, sample preparation methods, and validation criteria.

For instance, differences in extraction efficiency and antibody specificity can significantly impact the accuracy of ELISA-based tests. According to a study published by the Journal of AOAC International, commercial ELISA kits for peanut detection showed variability in sensitivity levels, with some kits failing to detect certain processed forms of peanut protein. Such inconsistencies pose challenges for regulatory agencies and food producers striving for uniform compliance.

Furthermore, international variations in allergen thresholds complicate matters. While the Codex Alimentarius provides general guidance, individual countries set their own action levels, creating confusion for multinational food companies. The absence of universally accepted standards hampers harmonization efforts and delays the development of reliable, cross-platform testing protocols. This fragmentation remains a persistent challenge in achieving consistent allergen management across the food supply chain.

MARKET OPPORTUNITIES

Expansion of Plant-Based and Alternative Protein Products

An emerging opportunity within the North America food allergen testing market lies in the rapid growth of plant-based and alternative protein products. The plant-based food sector has seen exponential growth in recent years, driven by shifting consumer preferences toward sustainable and health-conscious diets.

Many of these products incorporate novel ingredients such as pea protein, lupin, and chickpea flour, which may introduce new allergenic risks.

Despite being marketed as healthier alternatives, these products are not inherently hypoallergenic. For example, pea protein, widely used in plant-based meat substitutes, has been identified as a potential allergen source. As per a 2022 study published in Clinical and Translational Allergy, an increasing number of documented cases of pea protein allergy among consumers.

Consequently, manufacturers must conduct thorough allergen testing to ensure product safety and avoid mislabeling. Regulatory agencies such as the FDA are closely monitoring this evolving landscape, urging manufacturers to assess allergenicity during product development.

Integration of Digital Platforms and Automation in Allergen Testing

The integration of digital platforms and automation into allergen testing presents a transformative opportunity for the North America food allergen testing market. As food safety regulations grow more complex and consumer expectations for transparency rise, the need for faster, more accurate, and scalable testing solutions becomes imperative. Automation technologies, including robotic sample handling and AI-driven data analysis, are increasingly being adopted to enhance throughput and reduce human error in laboratory settings.

In North America, where food safety modernization is a top priority, companies are investing in smart diagnostic platforms capable of real-time allergen detection. For instance, Luminex Corporation has introduced multiplex testing systems that allow simultaneous detection of multiple allergens in a single run, improving efficiency and reducing turnaround time.

Moreover, cloud-based data management systems are enabling better traceability and compliance reporting. By leveraging digital innovations, the food allergen testing sector is poised for significant advancement, offering enhanced precision and scalability to meet evolving industry demands.

MARKET CHALLENGES

Complexity of Detecting Allergens in Highly Processed or Refined Ingredients

One of the foremost challenges facing the North America Food Allergen Testing Market is the difficulty in detecting allergens within highly processed or refined ingredients. During food processing, allergenic proteins can undergo structural modifications through heat treatment, enzymatic digestion, or chemical alterations, making them harder to identify using conventional testing methods. For instance, studies have shown that the Maillard reaction, which occurs during baking or frying, can mask allergenic epitopes, thereby reducing the efficacy of immunoassay-based detection techniques such as ELISA.

According to research published in the Journal of Agricultural and Food Chemistry , up to 30% of allergen-positive samples containing thermally processed milk or egg proteins were undetected by commercial ELISA kits. This limitation raises concerns about the reliability of current testing methodologies when applied to complex food matrices. Besides, refining processes such as hydrolysis used in producing fish sauces or nut oils can fragment allergenic proteins into smaller peptides, further complicating detection.

However, developing standardized methods that can consistently identify allergens in processed foods remains a scientific and logistical hurdle. Until such advancements are realized, the risk of false negatives persists, posing serious implications for consumer safety and regulatory compliance.

Supply Chain Complexity and Cross-Contamination Risks

A further critical challenge confronting the North America Food Allergen Testing Market is the complexity of modern food supply chains and the associated risk of cross-contamination. Today’s food manufacturing environment involves extensive ingredient sourcing, multi-step processing, and shared production lines, all of which heighten the likelihood of unintended allergen introduction. According to the Grocery Manufacturers Association (GMA), approximately 60% of food recalls in the U.S. are attributed to cross-contact with allergens, highlighting the pervasive nature of this issue.

Cross-contamination often occurs during raw material handling, storage, or transportation, particularly when facilities process multiple allergenic ingredients. Even minute traces of allergens—sometimes less than 1 part per million—can trigger severe reactions in sensitive individuals. As per a study conducted by the Canadian Food Inspection Agency (CFIA), nearly 20% of pre-packaged foods tested contained undeclared allergens, underscoring the limitations of current preventive controls.

To mitigate these risks, food producers must implement stringent allergen control plans, including dedicated equipment, thorough cleaning protocols, and frequent environmental swabbing. However, maintaining such high standards across diverse and geographically dispersed operations proves logistically demanding.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.82% |

| Segments Covered | By Source, Technology, Food Tested, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, and Rest of North America |

| Market Leaders Profiled | SGS S.A., Intertek Group plc, TUV SUD Psb Pte. Ltd., ALS Limited, Eurofins Scientific SE, Merieux Nutrisciences Corporation, AsureQuality Ltd., Microbac Laboratories Inc, Romer Labs Diagnostic GmbH, and Symbio Laboratories, and others |

SEGMENTAL ANALYSIS

By Source Insights

The milk segment held the largest share in the North America food allergen testing market, accounting for a 28.6% of total market revenue in 2024. This dominance is primarily attributed to the widespread prevalence of milk allergy among children and adults, coupled with its extensive use across a broad range of food products such as dairy alternatives, baked goods, infant formula, and processed snacks.

Like, according to the Centers for Disease Control and Prevention (CDC), approximately 1 in every 50 children in the U.S. suffers from a milk allergy, making it one of the most common food allergens. Also, as per the U.S. Department of Agriculture (USDA) reports that dairy-based ingredients are present in over 40% of packaged food items sold in supermarkets, increasing the risk of cross-contamination and necessitating rigorous allergen testing protocols.

Moreover, regulatory authorities like the U.S. Food and Drug Administration (FDA) mandate strict labeling laws under the Food Allergen Labeling and Consumer Protection Act (FALCPA), which includes milk among the top eight major allergens. These factors collectively drive the demand for advanced milk allergen testing solutions across food production facilities, reinforcing the segment’s leading position in the regional market.

The tree nuts segment is projected to be the fastest-growing source category in the North America food allergen testing market, registering a CAGR of 9.6% between 2025 and 2033. This rapid growth is fueled by rising consumer awareness about tree nut allergies and the increased incorporation of tree nuts in health-focused food formulations.

As per the American College of Allergy, Asthma & Immunology (ACAAI), nearly 1.8% of the U.S. population suffers from tree nut allergies, many of which are severe and lifelong. Tree nuts—including almonds, walnuts, cashews, and pecans—are increasingly used in plant-based snacks, protein bars, alternative milks, and gluten-free products, expanding their exposure across diverse consumer demographics.

Besides, incidents of cross-contact during processing and packaging have prompted stricter allergen control measures. With growing litigation risks and brand reputation concerns, manufacturers are investing heavily in accurate detection technologies for tree nut residues, thereby propelling this segment’s accelerated growth trajectory.

By Technology Insights

The immunoassay-based (ELISA) technology segment commanded the North America food allergen testing market, holding a 45.6% of the market share in 2024. ELISA (Enzyme-Linked Immunosorbent Assay) remains the preferred method due to its high sensitivity, specificity, and widespread adoption across food safety laboratories and manufacturing units.

The U.S. Food and Drug Administration (FDA) frequently references ELISA in its guidelines for allergen monitoring programs, further cementing its role in regulatory compliance.

Furthermore, industry players such as Thermo Fisher Scientific and Bio-Rad Laboratories continue to expand their ELISA kit portfolios, offering test kits tailored to specific allergens like milk, eggs, and peanuts. The combination of regulatory endorsement, technological maturity, and strong industry support ensures that immunoassay-based testing maintains its leadership in the region.

The PCR-based technology segment is the booming within the North America food allergen testing market, with a projected CAGR of 10.3% through 2033. Unlike traditional immunoassays, PCR (Polymerase Chain Reaction) detects allergenic DNA rather than proteins, offering advantages in identifying allergens in highly processed foods where proteins may be denatured.

According to a study published in Food Chemistry, PCR-based assays can detect allergenic DNA at concentrations as low as 10 parts per million (ppm), even after thermal processing or hydrolysis. This makes PCR particularly effective for detecting allergens in products like refined oils, canned foods, and fermented beverages—segments where ELISA often falls short.

In addition, the integration of real-time PCR platforms has enhanced speed and accuracy, allowing for multiplex detection of multiple allergens in a single test run. The U.S. Department of Agriculture (USDA) has increasingly adopted PCR-based screening in its inspection protocols, especially for imported food products. As manufacturers seek reliable tools to meet evolving regulatory demands and ensure supply chain transparency, the uptake of PCR-based testing continues to accelerate across North America.

By Food Tested Insights

The bakery & confectionery segment prevailed in the North America food allergen testing market, capturing 32.4% of total revenue in 2024. This dominance stems from the high usage of allergenic ingredients such as wheat, eggs, milk, and nuts in bakery products including breads, cookies, pastries, and cakes.

According to the U.S. Department of Agriculture (USDA), bakery products account for nearly 20% of all food recalls related to undeclared allergens. Ingredients like flour, butter, and chocolate often come into contact with shared equipment, increasing the risk of cross-contamination. In addition, as per the Grocery Manufacturers Association (GMA), over 60% of allergen-related recalls in the U.S. were linked to bakery and snack products.

Regulatory agencies such as the FDA emphasize the importance of allergen controls in these product categories, given their widespread consumption across all age groups. Also, the rise in artisanal and custom-baked goods produced in small-scale facilities—with less stringent allergen management systems—has heightened the need for comprehensive testing protocols. Consequently, the bakery & confectionery segment remains a focal point for allergen testing investments across North America.

The infant food segment is the rapidly expanding in the North America food allergen testing market, projected to grow at a CAGR of 11.2% in the coming years. This rapid expansion is driven by heightened parental awareness regarding early allergen introduction and the critical need for safe, hypoallergenic baby food formulations.

According to the American Academy of Pediatrics (AAP), early exposure to allergenic foods such as peanut and egg can reduce the risk of developing food allergies later in life. This shift in medical guidance has led to the inclusion of controlled allergen levels in infant nutrition products, necessitating precise and consistent allergen testing throughout production.

Moreover, the U.S. Food and Drug Administration (FDA) mandates strict quality checks for infant food manufacturers under the Infant Formula Act, ensuring nutritional adequacy and allergen safety. As per the data from the National Institute of Allergy and Infectious Diseases (NIAID), food allergies affect up to 8% of infants, making allergen contamination a serious public health concern.

With increasing scrutiny on child nutrition and rising recalls of contaminated baby food products, companies are adopting advanced allergen testing technologies to safeguard product integrity, driving robust growth in this high-priority market segment.

REGIONAL ANALYSIS

United States held the dominant position in the North America Food Allergen Testing Market, commanding a 75.4% of the regional market share in 2024. The country's development is underpinned by a combination of high prevalence of food allergies, stringent regulatory frameworks, and a well-established food safety infrastructure.

The U.S. Food and Drug Administration (FDA) enforces rigorous allergen labeling requirements under the Food Allergen Labeling and Consumer Protection Act (FALCPA), mandating clear identification of the top eight allergens in packaged foods.

Besides, the FDA’s Recall Enterprise System recorded over 200 food recalls in 2022 linked to undeclared allergens, highlighting the critical need for robust allergen testing protocols. The presence of leading diagnostic and analytical solution providers, coupled with continuous innovation in testing technologies, reinforces the U.S.’s central role in shaping the regional market landscape.

Canada exhibits a mature regulatory environment and a growing focus on allergen risk mitigation in both domestic and export-oriented food industries.

Peanut, milk, and tree nuts are the most frequently cited allergens in these cases. Health Canada mandates strict allergen labeling under the Food and Drug Regulations (FDR), requiring explicit declaration of priority allergens on pre-packaged foods.

Furthermore, the prevalence of food allergies among Canadian children is rising. Coupled with the expansion of the organic and plant-based food sectors, which often introduce novel allergenic ingredients, Canada’s allergen testing market is witnessing steady growth driven by regulatory vigilance and public health imperatives.

Mexico, while currently a smaller contributor, represents an emerging segment within the North America Food Allergen Testing Market. Though not as mature as the U.S. or Canada, Mexico is experiencing growing awareness around food safety and allergen management, particularly in urban centers and export-driven food sectors.

Besides, Mexico’s participation in trade agreements such as USMCA has intensified pressure on local food producers to comply with U.S. and Canadian allergen control norms. The National Service of Agro-Alimentary Public Health, Safety and Quality (SENASICA) has ramped up inspections, leading to an uptick in allergen-related enforcement actions.

While still in its early stages, Mexico’s allergen testing market is gaining momentum due to regulatory modernization, increased consumer advocacy, and the expansion of multinational food processors seeking to align with global allergen safety benchmarks.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

SGS S.A., Intertek Group plc, TUV SUD Psb Pte. Ltd., ALS Limited, Eurofins Scientific SE, Merieux Nutrisciences Corporation, AsureQuality Ltd., Microbac Laboratories Inc, Romer Labs Diagnostic GmbH, and Symbio Laboratories are the key players in the North America food allergen testing market.

The competition in the North America Food Allergen Testing Market is characterized by the presence of well-established life science and diagnostics companies vying to provide accurate, efficient, and compliant testing solutions. With rising consumer awareness about food allergies and stricter regulatory enforcement, players are under pressure to deliver innovative and reliable products that ensure food safety across diverse supply chains. The market is highly fragmented, featuring a mix of large multinational corporations and specialized regional firms offering a broad spectrum of testing kits, instruments, and services. Technological differentiation, speed-to-result, and ease of use are key parameters influencing purchasing decisions among food manufacturers and testing laboratories. Additionally, the growing complexity of food formulations—especially with the rise of plant-based and alternative proteins—has intensified the demand for advanced allergen detection methods. To maintain a competitive edge, companies are focusing on expanding their R&D initiatives, forming strategic alliances, and enhancing their service offerings to support end-users throughout the production process. As the need for precision and traceability continues to grow, the competitive environment remains dynamic, with continuous advancements shaping the future of allergen testing in North America.

TOP PLAYERS IN THE MARKET

Thermo Fisher Scientific Inc

One of the leading companies in the North America Food Allergen Testing Market is Thermo Fisher Scientific Inc. The company offers a comprehensive portfolio of allergen testing solutions, including ELISA-based kits, PCR instruments, and rapid test strips. Thermo Fisher plays a pivotal role in setting industry standards by providing reliable and validated methods for detecting allergens across various food matrices. Their strong distribution network and continuous innovation in detection technologies make them a dominant player globally.

Bio-Rad Laboratories

Another major contributor to the market is Bio-Rad Laboratories, Inc. Known for its advanced immunoassay platforms, Bio-Rad provides highly sensitive and specific allergen detection kits that cater to both research and industrial applications. The company’s commitment to developing robust testing protocols supports regulatory compliance and enhances food safety measures worldwide. Its long-standing reputation and extensive product line solidify its position as a key global player.

Neogen Corporation

Neogen Corporation is also a significant participant in the allergen testing space. The company specializes in rapid diagnostic solutions and offers a wide range of test kits for common allergens such as milk, peanuts, and gluten. Neogen's focus on user-friendly and time-efficient testing methodologies makes its products popular among food processors and quality control laboratories. Its strategic acquisitions and emphasis on R&D further strengthen its presence in the global allergen testing landscape.

TOP STRATEGIES USED BY KEY PLAYERS

Key players in the North America Food Allergen Testing Market are actively pursuing product innovation and development to enhance their testing capabilities and meet evolving regulatory demands. Companies are investing heavily in next-generation diagnostics that offer faster results, higher sensitivity, and compatibility with complex food matrices.

Another prevalent strategy is strategic partnerships and collaborations , particularly with academic institutions, regulatory bodies, and contract testing laboratories. These alliances help firms gain deeper insights into emerging allergenic risks and refine their detection methodologies accordingly.

Additionally, expansion through mergers and acquisitions is a key growth tactic employed by leading companies. By acquiring smaller firms with niche technologies or regional expertise, market leaders can broaden their product portfolios, enter new customer segments, and reinforce their competitive advantage in the allergen testing sector.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Thermo Fisher Scientific launched a new suite of digital allergen testing solutions designed to streamline data analysis and improve traceability across food production lines. This move aimed at enhancing real-time monitoring and compliance reporting for manufacturers.

- In June 2023, Bio-Rad Laboratories expanded its allergen testing portfolio with the introduction of a multiplex ELISA platform capable of detecting multiple allergens simultaneously, offering greater efficiency for high-volume testing facilities.

- In November 2024, Neogen Corporation acquired a biotech startup specializing in DNA-based allergen detection, reinforcing its capabilities in molecular testing and expanding its technological footprint in the North American market.

- In September 2023, PerkinElmer introduced a fully automated allergen testing system tailored for large-scale food processing plants, aiming to reduce manual errors and accelerate sample throughput.

- In March 2024, Sartorius AG formed a strategic partnership with a leading food safety certification body to integrate allergen testing protocols into third-party audit systems, promoting broader adoption across certified manufacturing units.

MARKET SEGMENTATION

This research report on the North America food allergen testing market has been segmented and sub-segmented based on the following categories.

By Source

-

Introduction

-

Peanuts & Soy

-

Wheat

-

Milk

-

Eggs

-

Tree Nuts

-

Seafood

By Technology

-

Introduction

-

PCR-Based

By Food Tested

-

Introduction

-

Diagnostics Development

-

Bakery & Confectionery

-

Infant Food

-

Disease Risk Assessment

-

Other Applications

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

1. What is the current size of the North America food allergen testing market?

The North America food allergen testing market was valued at USD 269.45 billion in 2024.

2. What are the key growth drivers for the food allergen testing market in North America?

Rising food safety concerns, increasing prevalence of food allergies, and stringent regulatory frameworks are major growth drivers.

3. Which technologies are commonly used in food allergen testing?

Common technologies include ELISA, PCR-based testing, mass spectrometry, and lateral flow assays.

4. What trends are shaping the food allergen testing market in North America?

Automation in testing, rise in allergen-free labeling, and growing demand for rapid detection kits are notable trends.

5. What are the major challenges facing the food allergen testingmarket?

High testing costs, complexity in detecting trace allergens, and lack of awareness among small-scale producers are key challenges.

6. Which countries lead the North American allergen testing market?

The United States leads the market, followed by Canada and Mexico, due to regulatory enforcement and consumer awareness.

7. who are the prominent players in the North America food allergen testing market?

Key players include Eurofins Scientific, Neogen Corporation, Thermo Fisher Scientific, SGS SA, and ALS Limited.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com