Global Food Allergen Testing Market By Source (Peanuts & Soy, Wheat, Milk, Eggs, Tree Nuts, Seafood), Technology , and By Region - Global Industry Analysis, Size, Share, Growth, Trends, And Forecast 2026 to 2034

Global Food Allergen Testing Market Report Summary

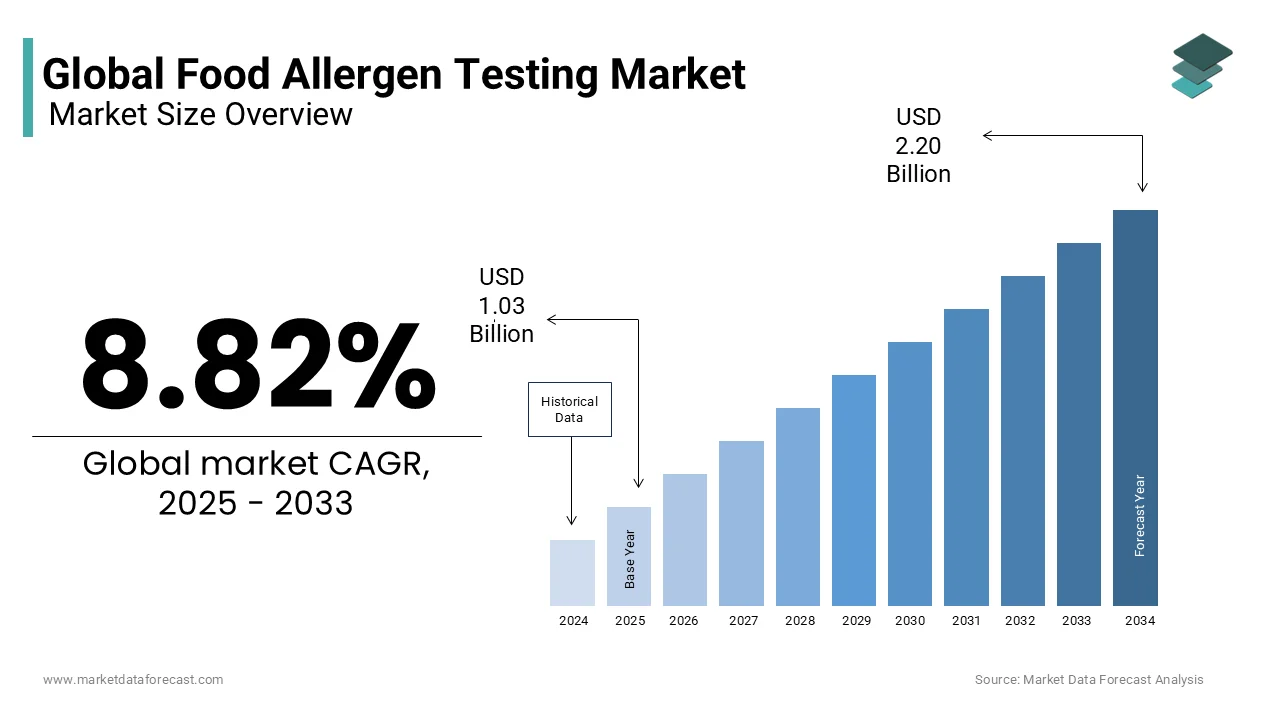

The global food allergen testing market was valued at USD 1.03 billion in 2025, is estimated to reach USD 1.12 billion in 2026, and is projected to reach USD 2.20 billion by 2034, growing at a CAGR of 8.82% during the forecast period. Market growth is driven by increasing prevalence of food allergies, stringent food safety regulations, rising consumer awareness regarding allergen labeling, and growing demand for quality assurance across the food industry. Food manufacturers are increasingly adopting advanced testing methods to ensure regulatory compliance and consumer safety. The expansion of global food trade and the growing emphasis on traceability are further supporting market growth.

Key Market Trends

- Growing prevalence of food allergies and intolerances is driving market growth.

- Increasing regulatory requirements for allergen labeling and food safety are boosting market expansion.

- Rising demand for accurate and rapid allergen detection technologies is supporting industry development.

- Expansion of processed and packaged food production is enhancing market opportunities.

- Advancements in testing technologies and laboratory automation are influencing market advancement.

Segmental Insights

- Based on source, the milk segment accounted for the largest share of the global food allergen testing market in 2025. This dominance is attributed to the high prevalence of milk allergies and strict regulatory requirements for dairy allergen declaration in food products.

- Based on technology, the immunoassay based ELISA segment held the leading share of the global market in 2025. Its widespread adoption is driven by high sensitivity, reliability, cost effectiveness, and ease of implementation for allergen detection.

- Based on food tested, the bakery and confectionery products segment accounted for the largest share of the global food allergen testing market in 2025, supported by the extensive use of allergenic ingredients such as milk, eggs, nuts, and wheat in these products.

Regional Insights

- North America accounted for the leading share of the global food allergen testing market in 2025 and is expected to maintain its dominant position throughout the forecast period. Strong food safety regulations, advanced laboratory infrastructure, and high consumer awareness regarding food allergies continue to support regional market growth.

Competitive Landscape

The global food allergen testing market is highly competitive, with companies focusing on advanced testing technologies, laboratory network expansion, and regulatory compliance solutions to strengthen their market position. Market participants continue to invest in rapid testing platforms, automation technologies, and comprehensive food safety services.

Key companies operating in the global food allergen testing market include SGS S.A., Intertek Group plc, TUV SUD Psb Pte. Ltd., ALS Limited, Eurofins Scientific SE, Merieux Nutrisciences Corporation, AsureQuality Ltd., Microbac Laboratories Inc, Romer Labs Diagnostic GmbH, and Symbio Laboratories.

Global Food Allergen Testing Market Size

The global food allergen testing market size was valued at USD 1.03 billion in 2025, and is expected to reach USD 2.20 billion by 2034 from USD 1.12 billion in 2026. The market is growing at a CAGR of 8.82% during the forecast period.

Food allergen testing comprises a specialized suite of analytical technologies and services designed to detect trace amounts of allergenic proteins in food products. These testing solutions are critical for ensuring consumer safety and regulatory compliance by identifying contaminants such as peanuts milk eggs soy wheat fish shellfish and tree nuts. The market encompasses various methodologies including enzyme linked immunosorbent assay polymerase chain reaction and mass spectrometry which offer varying levels of sensitivity and specificity. In Europe, the urgency for robust testing frameworks is driven by the high prevalence of food allergies and stringent labeling laws. As per the European Academy of Allergy and Clinical Immunology, approximately 17 million people in Europe suffer from food allergies with children being disproportionately affected. Furthermore, according to the Centers for Disease Control and Prevention, food allergies affect an estimated 5.3% of children in the United States highlighting the global scale of the health concern. The World Health Organization emphasizes that accurate labeling is essential to prevent accidental exposure which can lead to severe anaphylactic reactions. According to the European Food Safety Authority, undeclared allergens remain one of the most common reasons for food recalls across the continent. This regulatory and health landscape necessitates rigorous testing protocols throughout the supply chain from raw material sourcing to final product verification. The integration of rapid testing kits in manufacturing facilities allows for real time quality control minimizing the risk of cross contamination and protecting brand reputation in an increasingly conscious consumer market.

MARKET DRIVERS

Stringent Global Regulatory Frameworks and Labeling Mandates

The implementation of rigorous regulatory frameworks and mandatory labeling laws is primarily fuelling the expansion of the global food allergen testing market. Governments worldwide are enforcing stricter guidelines to ensure transparency and protect consumers from accidental allergen exposure. As per the Food and Drug Administration in the United States, the Food Allergy Safety Treatment Education and Research Act requires clear labeling of major food allergens effective from 2023. This legislation mandates that manufacturers verify the absence of undeclared allergens through regular testing protocols. In the European Union, the Food Information for Consumers Regulation mandates the declaration of 14 specific allergens driving demand for comprehensive testing services. As per the European Commission, non-compliance with these regulations can result in substantial fines and product recalls which incentivizes companies to invest in robust testing infrastructure. Additionally, the Codex Alimentarius Commission provides international standards for food labeling which influences national policies globally. The increasing number of regulatory inspections and audits forces food producers to adopt standardized testing methods to demonstrate due diligence. The Global Food Safety Initiative emphasizes that allergen management is a critical component of food safety certification schemes such as ISO 22000 and BRCGS. Consequently, the legal imperative to comply with diverse and evolving regulations ensures sustained demand for accurate and reliable allergen testing technologies across the global food industry.

Rising Prevalence of Food Allergies and Consumer Awareness

The escalating prevalence of food allergies coupled with rising consumer awareness significantly drives the demand for advanced food allergen testing, which is further contributing to the food allergen testing market expansion. Medical studies indicate a steady increase in the incidence of allergic reactions particularly among pediatric populations which has raised public concern regarding food safety. As per the World Allergy Organization, food allergies have become a significant public health issue, affecting over 220 million people globally. This trend has led to a more vigilant consumer base that actively scrutinizes ingredient lists and seeks certified allergen free products. According to the Centers for Disease Control and Prevention, the reported food allergy rate among all children younger than 18 years in 2007 was 18% higher than in 1997, underscoring the severity of the issue. Consumers are increasingly willing to pay a premium for products that guarantee safety through third party testing and certification. As per the International Food Information Council, 70% of consumers check labels for allergens before purchasing packaged foods. This shift in consumer behavior pressures manufacturers to implement rigorous testing protocols to maintain brand trust and loyalty. Retailers are also demanding higher standards from suppliers to mitigate liability risks. The rise of social media and advocacy groups further amplifies the importance of transparent allergen management. Consequently, the combination of medical trends and consumer activism creates a powerful market force driving the adoption of sophisticated allergen testing solutions.

MARKET RESTRAINTS

High Costs Associated with Advanced Testing Methodologies

The substantial financial investment required for advanced food allergen testing methodologies is impeding the food allergen testing market expansion, particularly for small and medium sized enterprises. Technologies such as liquid chromatography tandem mass spectrometry offer high sensitivity and specificity but involve expensive equipment reagents and skilled personnel. As per the American Chemistry Council, the initial capital expenditure for setting up a fully equipped allergen testing laboratory can exceed 500,000 dollars. This cost barrier limits the ability of smaller food producers to conduct in house testing forcing them to rely on external laboratories which incur recurring service fees. As per the European Small Business Portal, compliance costs can account for up to 10% of total operational expenses for small food manufacturers. Additionally, the need for regular calibration maintenance and validation of testing instruments adds to the long term financial burden. The complexity of sample preparation and analysis requires trained technicians whose salaries contribute to higher operational costs. For companies operating on thin margins these expenses can be prohibitive leading to potential gaps in testing frequency or coverage. The lack of affordable rapid testing options for certain allergens further exacerbates the issue. While regulatory compliance is mandatory the economic strain of maintaining high standards can hinder market participation for smaller players. Until cost effective alternatives become widely available the high expense of advanced testing will continue to restrain broader market adoption.

Complexity of Matrix Effects and Cross Contamination Risks

The technical complexity associated with matrix effects and the risks of cross contamination are further inhibiting the expansion of the food allergen testing market. Food matrices vary widely in composition including fats proteins and carbohydrates which can interfere with the detection of allergenic proteins. As per the Association of Official Analytical Chemists, matrix effects can lead to false negative or false positive results compromising the validity of testing outcomes. Processed foods undergo various treatments such as heating fermentation and extrusion which can alter the structure of allergenic proteins making them difficult to detect using standard antibody based methods. The European Food Safety Authority highlights that the lack of standardized reference materials for processed foods complicates the validation of testing methods. Cross contamination during production processing and packaging further complicates testing requirements as trace amounts of allergens can be introduced at multiple stages. The Institute of Food Technologists notes that detecting allergens at parts per million levels requires highly sensitive techniques that are susceptible to interference. The variability in allergen distribution within bulk ingredients also makes representative sampling challenging. These technical hurdles require continuous method development and validation which increases the time and cost of testing. The uncertainty surrounding detection limits in complex matrices can lead to inconsistent results affecting consumer safety and regulatory compliance. Until standardized methods for complex matrices are established these technical limitations will remain a persistent restraint.

MARKET OPPORTUNITIES

Development of Rapid Point of Care Testing Solutions

The emergence of rapid point of care testing solutions is a significant opportunity for growth in the food allergen testing market. These portable devices allow for real time detection of allergens directly on the production floor or in retail environments reducing the turnaround time for results. As per the Global Point of Care Testing Market Report, the demand for rapid diagnostic tools in the food industry is expected to grow by 12% annually through 2030. Rapid tests utilize lateral flow immunoassay technology which provides results within minutes enabling immediate decision making regarding product release or rejection. The International Association for Food Protection emphasizes that rapid testing enhances operational efficiency by minimizing downtime and preventing contaminated batches from entering the supply chain. The convenience and ease of use of these devices make them accessible to non-specialized staff reducing the need for extensive training. The expansion of e commerce and food delivery services also drives the need for quick verification of allergen claims at distribution centers. Manufacturers are investing in the development of multiplex rapid tests that can detect multiple allergens simultaneously further enhancing their utility. The ability to conduct frequent testing without sending samples to external laboratories reduces costs and improves quality control. As technology advances the sensitivity and specificity of rapid tests are improving making them a viable alternative to traditional laboratory methods. This shift towards decentralized testing offers substantial growth potential for market participants.

Expansion into Emerging Markets with Growing Food Safety Standards

The expansion of food allergen testing services into emerging markets offers a lucrative opportunity driven by rising income levels and improving food safety regulations. Countries in Asia Pacific Latin America and the Middle East are experiencing rapid urbanization and changes in dietary habits leading to increased consumption of processed foods. As per the World Bank, the middle class in emerging economies is expanding creating a demand for higher quality and safer food products. Governments in these regions are increasingly adopting international food safety standards to facilitate trade and protect public health. The Asian Food Federation reports that several Asian countries are updating their labeling laws to include mandatory allergen declarations. This regulatory shift creates a new market for testing services and equipment as local manufacturers strive to comply with export requirements. The presence of multinational food companies in these regions also drives the adoption of global best practices including rigorous allergen management. Local testing laboratories are expanding their capabilities to meet the growing demand for accredited services. The increasing awareness of food allergies among consumers in emerging markets further supports market growth. Partnerships between global testing firms and local distributors can facilitate market entry and expansion. The untapped potential in these regions provides a significant avenue for revenue growth and market diversification for industry players.

MARKET CHALLENGES

Lack of Harmonized Global Standards and Reference Materials

The absence of harmonized global standards and validated reference materials for food allergen testing creates significant inconsistencies and challenges for the global market expansion. Different countries and regions employ varying thresholds for allergen labeling and detection which complicates international trade and compliance. As per the Codex Alimentarius Commission, there is no universally agreed upon threshold level for allergen labeling leading to discrepancies in regulatory requirements. The lack of standardized reference materials makes it difficult to compare results across different laboratories and testing methods. The European Committee for Standardization notes that variations in extraction protocols and antibody specificities can yield different results for the same sample. This inconsistency undermines confidence in testing outcomes and creates uncertainty for manufacturers exporting to multiple markets. The development of validated reference materials for processed foods is particularly challenging due to the complexity of food matrices. The International Organization for Standardization is working towards harmonizing methods but progress is slow due to technical and regulatory differences. The lack of uniformity increases the burden on manufacturers who must navigate a complex web of regulations. It also hinders the development of universal testing kits that can be used globally. Until global standards are established the fragmentation of regulatory frameworks will remain a major challenge for the food allergen testing market.

Technical Limitations in Detecting Processed and Hidden Allergens

The technical limitations in detecting processed and hidden allergens are further challenging the global market expansion. Thermal processing and other manufacturing techniques can denature allergenic proteins altering their structure and reducing their detectability by antibody based assays. As per the Journal of Agricultural and Food Chemistry, heat treatment can mask epitopes leading to false negative results in enzyme linked immunosorbent assays. This poses a significant risk as denatured proteins may still retain their allergenicity despite being undetectable. The complexity of multi ingredient foods further complicates detection as interactions between ingredients can interfere with assay performance. The Institute of Food Technologists highlights that current methods often struggle to quantify allergens accurately in highly processed matrices such as chocolates and baked goods. The presence of hidden allergens in spices flavorings and additives adds another layer of difficulty as these ingredients may not be clearly labeled. The lack of sensitive and specific methods for detecting hydrolyzed proteins remains a gap in the industry. Mass spectrometry offers promise but is not yet widely adopted due to cost and complexity. The inability to reliably detect all forms of allergens undermines the effectiveness of testing programs. Addressing these technical limitations requires ongoing research and innovation which is resource intensive and time consuming.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.82% |

| Segments Covered | By Source, By Technology, By Food Tested, and By Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | SGS S.A., Intertek Group plc, TUV SUD Psb Pte. Ltd., ALS Limited, Eurofins Scientific SE, Merieux Nutrisciences Corporation, AsureQuality Ltd., Microbac Laboratories Inc, Romer Labs Diagnostic GmbH, and Symbio Laboratories |

SEGMENTAL ANALYSIS

By Source Insights

The milk segment had the leading share of the global market in 2025. The dominance of milk segment in the global market can be driven by its widespread presence in processed foods and its status as one of the most common allergens globally. Dairy proteins such as casein and whey are integral ingredients in a vast array of products including bakery items confectionery sauces and infant formulas. As per the European Academy of Allergy and Clinical Immunology, cow's milk allergy affects approximately 2% to 3% of infants in Europe making it the most prevalent food allergy in early childhood. The ubiquity of milk derivatives in industrial food processing necessitates rigorous testing to prevent cross contamination and ensure accurate labeling. The United States Department of Agriculture states that dairy consumption remains high across all age groups driving continuous demand for safe and compliant products. Regulatory bodies such as the Food and Drug Administration mandate strict labeling for milk containing products which compels manufacturers to implement robust testing protocols. The complexity of detecting milk proteins in highly processed matrices where heat treatment may denature the proteins requires advanced analytical methods. This technical challenge drives the adoption of sensitive testing technologies such as mass spectrometry and polymerase chain reaction. Furthermore the global expansion of the dairy industry and the introduction of new dairy based products increase the scope for allergen testing. The high volume of milk based ingredients in the supply chain ensures that this segment remains the largest contributor to market revenue. The critical need to protect vulnerable populations particularly infants and young children further reinforces the dominance of milk allergen testing.

On the other hand, the tree nuts segment is estimated to register a CAGR of 9.5% during the forecast period in the global market owing to the increasing incorporation of tree nuts such as almonds walnuts and cashews into health focused snacks plant-based milks and gourmet food products. As per the Global Tree Nut Association, the consumption of tree nuts has risen by 15% in the last decade due to their perceived health benefits and versatility in culinary applications. The rising prevalence of tree nut allergies which are often severe and lifelong has heightened consumer awareness and regulatory scrutiny. According to the Centers for Disease Control and Prevention, tree nut allergies are among the top causes of fatal anaphylactic reactions in the United States. This severity prompts manufacturers to adopt stringent testing measures to ensure product safety and avoid costly recalls. The diversity of tree nut species requires specific and sensitive detection methods as cross reactivity between different nuts can complicate testing. The expansion of the vegan and vegetarian markets has led to increased use of nut based alternatives for dairy and meat further driving demand for testing. Additionally the global trade of tree nuts involves complex supply chains with multiple sourcing points increasing the risk of cross contamination. Manufacturers are investing in advanced testing technologies to detect trace amounts of various tree nuts simultaneously. These factors collectively accelerate the growth of the tree nut allergen testing segment.

By Technology Insights

The immunoassay-based (ELISA) segment dominated the market by capturing the highest share of the global market in 2025 due to their high sensitivity specificity and cost effectiveness. ELISA methods are widely adopted in food manufacturing facilities and quality control laboratories for routine screening of allergenic proteins. As per the Association of Official Analytical Chemists, ELISA is the gold standard for allergen detection offering reliable results for a wide range of food matrices. The technology’s ability to detect low levels of allergens at parts per million concentrations makes it indispensable for compliance with regulatory thresholds. The European Food Safety Authority recognizes ELISA as a validated method for monitoring allergen presence in processed foods. The widespread availability of commercial ELISA kits for major allergens such as milk eggs peanuts and gluten facilitates easy implementation by food producers. The relatively low cost of equipment and reagents compared to molecular methods makes ELISA accessible to small and medium sized enterprises. The ease of use and rapid turnaround time allow for high throughput testing which is essential for large scale production environments. Furthermore the continuous development of multiplex ELISA kits enables the simultaneous detection of multiple allergens enhancing operational efficiency. The established infrastructure and technical expertise surrounding immunoassay technologies ensure their continued dominance. The reliability of ELISA in providing quantitative data supports effective allergen management programs. These attributes cement the position of immunoassay-based methods as the primary technology in the food allergen testing market.

On the other side, the PCR-based technology segment is anticipated to showcase a promising CAGR of 10.5% during the forecast period owing to the superior ability of PCR to detect allergenic DNA even in highly processed foods where proteins may be denatured or degraded. As per the International Organization for Standardization, PCR methods offer high specificity and sensitivity making them ideal for identifying trace amounts of allergenic ingredients. The technology is particularly effective for detecting allergens such as celery mustard and sesame which are difficult to analyze using immunoassays due to protein instability. The European Committee for Standardization has validated several PCR methods for allergen detection encouraging their adoption in regulatory compliance testing. The increasing complexity of food formulations and the presence of hidden allergens drive the demand for more robust detection techniques. PCR allows for the identification of specific plant or animal species providing definitive proof of ingredient presence. The advancement of real time PCR and digital PCR technologies has improved quantification capabilities and reduced analysis time. The growing acceptance of molecular methods by regulatory agencies and industry standards bodies further supports market growth. Additionally the ability of PCR to distinguish between closely related species reduces the risk of false positives. The integration of PCR into routine testing workflows is facilitated by automated systems that enhance throughput and reduce human error. These technological advantages position PCR as the fastest expanding segment in the market.

By Food Tested Insights

The bakery and confectionery products segment led the market with the highest share of the global market in 2025 due to the extensive use of common allergens such as wheat eggs milk and nuts in these categories. These products are staple items in diets worldwide and are often produced in facilities that handle multiple allergenic ingredients increasing the risk of cross contamination. As per the American Bakers Association, the bakery industry is one of the largest segments of the food manufacturing sector with billions of units produced annually. The complex nature of bakery formulations which often include multiple layers fillings and coatings requires comprehensive allergen testing to ensure safety. As per the European Bakery Confederation, allergen management is a top priority for bakeries due to the high incidence of wheat and egg allergies. The thermal processing involved in baking can alter protein structures making detection challenging and necessitating advanced testing methods. The widespread consumption of confectionery items particularly among children who are more susceptible to allergies drives the need for strict quality control. Retailers and consumers demand clear and accurate labeling which compels manufacturers to implement rigorous testing protocols. The high volume of production and the diversity of products in this category ensure consistent demand for allergen testing services. The prevalence of shared equipment in bakeries further increases the likelihood of cross contact requiring frequent monitoring. These factors collectively establish bakery and confectionery as the dominant segment in the food allergen testing market.

On the other hand, the infant food segment is the fastest growing segment in the food allergen testing market and is estimated to record a CAGR of 11.4% during the forecast period owing to the extreme vulnerability of infants to allergic reactions and the stringent regulatory requirements governing baby food safety. As per the World Health Organization, infancy is a critical period for the development of the immune system and exposure to allergens can have long term health consequences. Parents and caregivers are increasingly vigilant about the ingredients in infant formulas purees and snacks demanding highest safety standards. The European Commission has implemented strict regulations on the composition and labeling of infant foods requiring thorough allergen screening. The Centers for Disease Control and Prevention notes that early introduction of allergenic foods is being studied but requires precise control and testing to prevent adverse reactions. The high value placed on infant health drives manufacturers to invest in advanced testing technologies to guarantee product purity. The growing trend of organic and specialized infant foods introduces new ingredients that require validation for allergen content. The global expansion of the baby food market particularly in emerging economies creates new opportunities for testing services. The emotional and financial stakes for parents ensure that zero tolerance for allergen contamination is the norm. These dynamics fuel the rapid expansion of allergen testing in the infant food sector.

REGIONAL ANALYSIS

North America Food Allergen Testing Market Analysis

North America held the leading share of the global market in 2025 and is expected to experience steady development and maintain its leading position over the next few years. The United States dominates the regional market due to the prevalence of food allergies and strict labeling laws enforced by the Food and Drug Administration. According to the Centers for Disease Control and Prevention, food allergies affect millions of Americans driving demand for rigorous testing and compliance. The implementation of the Food Allergy Safety Treatment Education and Research Act has further strengthened labeling requirements prompting manufacturers to enhance their testing protocols. Canada also contributes significantly with its robust food safety regulations under the Canadian Food Inspection Agency. The region benefits from a well developed infrastructure for analytical testing and a strong presence of key market players. The high level of healthcare expenditure and public health initiatives supports the adoption of advanced testing technologies. The prevalence of processed and convenience foods in North American diets increases the need for allergen monitoring. The active involvement of patient advocacy groups raises awareness and influences policy decisions. The region’s focus on innovation and quality assurance ensures sustained market growth. The integration of rapid testing solutions in manufacturing facilities is gaining traction. North America remains the benchmark for food allergen safety and testing standards globally.

Europe Food Allergen Testing Market Analysis

Europe is projected to undergo consistent growth and strengthen its enforcement mechanisms over the next few years. The European Union’s Food Information for Consumers Regulation requires the declaration of 14 major allergens driving extensive testing activities across member states. According to the European Academy of Allergy and Clinical Immunology, food allergies are a significant public health concern in Europe affecting millions of individuals. Countries such as Germany France and the United Kingdom are key markets due to their large food processing industries and strict enforcement of safety standards. The European Food Safety Authority provides scientific guidance and risk assessments that shape national policies and testing practices. The region’s emphasis on consumer protection and transparency fosters a culture of rigorous allergen management. The presence of leading testing laboratories and technology providers supports market development. The increasing popularity of organic and natural foods drives demand for certified allergen free products. Cross border trade within the EU necessitates harmonized testing standards to ensure compliance. The region’s investment in research and development leads to innovative testing solutions. Europe’s commitment to high food safety standards ensures steady demand for allergen testing services. The collaborative approach among stakeholders enhances the effectiveness of allergen control measures.

Asia Pacific Food Allergen Testing Market Analysis

Asia Pacific is anticipated to exhibit rapid expansion and record the highest developmental growth rate over the next few years. China India and Japan are the primary contributors to the regional market with increasing awareness of food safety and allergies. According to the World Bank, the growing middle class in Asia Pacific is demanding higher quality and safer food products. The Asian Food Federation reports that several countries are updating their labeling laws to include mandatory allergen declarations. The expansion of the processed food industry and the entry of multinational companies drive the adoption of global testing standards. The prevalence of seafood and soy allergies in the region influences testing priorities. The lack of standardized testing infrastructure in some areas presents challenges but also opportunities for market expansion. Local laboratories are upgrading their capabilities to meet international accreditation requirements. The increasing export of food products from Asia Pacific to regulated markets like the US and EU necessitates rigorous testing. Consumer education campaigns are raising awareness about food allergies. The region’s dynamic economic growth and evolving regulatory landscape support market development. Asia Pacific represents a high potential market for future expansion.

Latin America Food Allergen Testing Market Analysis

Latin America is poised to show gradual regulatory alignment and steady market maturation over the next few years. Brazil and Mexico are the largest markets in the region due to their significant food processing sectors and growing consumer demand for safe products. According to the Pan American Health Organization, food borne illnesses and allergic reactions are public health concerns prompting governments to enhance safety regulations. The adoption of international standards such as those from the Codex Alimentarius is influencing local policies. The expansion of retail chains and the presence of multinational food companies drive the implementation of rigorous quality control measures. The growing middle class is increasingly concerned about ingredient transparency and allergen labeling. Local manufacturers are investing in testing capabilities to comply with export requirements and domestic regulations. The region faces challenges related to infrastructure and technical expertise but training programs are addressing these gaps. The popularity of traditional foods containing common allergens such as peanuts and shellfish necessitates careful monitoring. The increasing incidence of food allergies is raising public awareness. Government initiatives to improve food safety surveillance support market growth. Latin America is gradually aligning with global best practices in allergen management. The potential for growth is significant as regulatory frameworks mature.

COMPETITIVE LANDSCAPE

The competition in the food allergen testing market is characterized by a mix of global laboratory service providers and specialized diagnostic kit manufacturers striving for dominance through accuracy and speed. Major players leverage their extensive networks and accredited facilities to offer comprehensive testing solutions that ensure regulatory compliance. The market sees intense rivalry in the development of rapid testing technologies that provide immediate results for quality control purposes. Companies differentiate themselves through the sensitivity and specificity of their assays particularly for complex food matrices. Price competition remains significant in the commodity testing segment prompting providers to optimize operational efficiencies. Strategic collaborations with technology firms enable the integration of artificial intelligence for data analysis and prediction. Intellectual property protection for proprietary antibodies and testing methods is crucial for maintaining technological leadership. The shift towards preventive food safety drives competitors to offer holistic risk management services beyond simple testing. Regulatory harmonization efforts influence competitive dynamics as companies adapt to global standards. The continuous push for innovation and reliability fosters a dynamic environment where quality and service excellence are paramount for success.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global food allergen testing market are

- SGS S.A.

- Intertek Group plc

- TUV SUD Psb Pte. Ltd.

- ALS Limited

- Eurofins Scientific SE

- Merieux Nutrisciences Corporation

- AsureQuality Ltd.

- Microbac Laboratories Inc

- Romer Labs Diagnostic GmbH

- Symbio Laboratories.

Top Players in the Market

- Eurofins Scientific SE is a global leader in bioanalytical testing services with a significant presence in the food allergen testing sector. The company offers comprehensive testing solutions including enzyme linked immunosorbent assay and polymerase chain reaction methods to detect trace allergens. Eurofins recently expanded its network of specialized food testing laboratories in North America and Europe to enhance service capacity. This expansion allows the company to provide faster turnaround times and localized support for food manufacturers. Eurofins invests heavily in research and development to improve the sensitivity and accuracy of its testing protocols. The company also focuses on digital integration offering clients real time access to test results through secure online platforms. By maintaining high accreditation standards and offering a wide range of analytical services Eurofins strengthens its position as a trusted partner for global food safety compliance.

- Neogen Corporation is a prominent provider of food safety solutions specializing in rapid allergen testing kits and diagnostic tools. The company offers a diverse portfolio of immunoassay based products that enable quick and reliable detection of major food allergens. Neogen recently launched new lateral flow devices designed for on site testing which allow food producers to monitor allergen presence in real time. This innovation enhances operational efficiency by reducing the need for external laboratory analysis. The company also expanded its manufacturing facilities to meet the growing demand for rapid testing solutions globally. Neogen collaborates with industry associations to educate stakeholders on best practices for allergen management. Their focus on user friendly technologies and robust customer support ensures widespread adoption of their products. By prioritizing innovation and accessibility Neogen maintains a strong competitive edge in the food allergen testing market.

- Merieux NutriSciences is a key player in the food testing industry offering specialized services for allergen detection and risk management. The company provides advanced analytical solutions including mass spectrometry and molecular biology techniques to identify allergenic proteins with high precision. Merieux NutriSciences recently acquired several regional testing laboratories to expand its global footprint and service capabilities. This strategic growth enables the company to offer comprehensive support to multinational food companies across different markets. The firm also develops customized testing protocols tailored to specific client needs and regulatory requirements. Merieux NutriSciences emphasizes sustainability and quality assurance in its operations aligning with global food safety standards. By integrating cutting edge technology with expert scientific consultation the company helps clients mitigate allergen risks effectively. Their commitment to excellence and continuous improvement solidifies their reputation as a leading provider in the food allergen testing sector.

Top Strategies Used by Key Market Participants

Key players in the Food Allergen Testing Market primarily focus on technological innovation and strategic expansions to maintain competitive advantage. Companies invest heavily in research and development to create more sensitive and rapid testing methods such as multiplex assays. Strategic acquisitions of regional laboratories allow firms to broaden their geographic reach and service offerings. Partnerships with food manufacturers and regulatory bodies facilitate the development of standardized testing protocols. Emphasizing digital solutions for data management enhances customer experience and operational efficiency. Expanding product portfolios to include rapid point of care tests addresses the need for immediate results in production environments. Training and educational initiatives help customers implement effective allergen management programs. These strategies collectively drive growth and establish long term leadership in the evolving food safety landscape.

MARKET SEGMENTATION

This research report on the global food allergen testing market is segmented and sub-segmented into the following categories.

By Source

- Peanuts & Soy

- Wheat

- Milk

- Eggs

- Tree Nuts

- Seafood

By Technology

- PCR Based

- Immunoassay Based (ELISA)

By Food Tested

- Bakery & Confectionery

- Infant Food

By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com