North America Golf Cart Market Size, Share, Trends & Growth Forecast Report By Product Type (Electric, Gasoline, Solar), Application (Golf Course, Personal Services, Commercial Services), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis, 2026 to 2034

North America Golf Cart Market Size

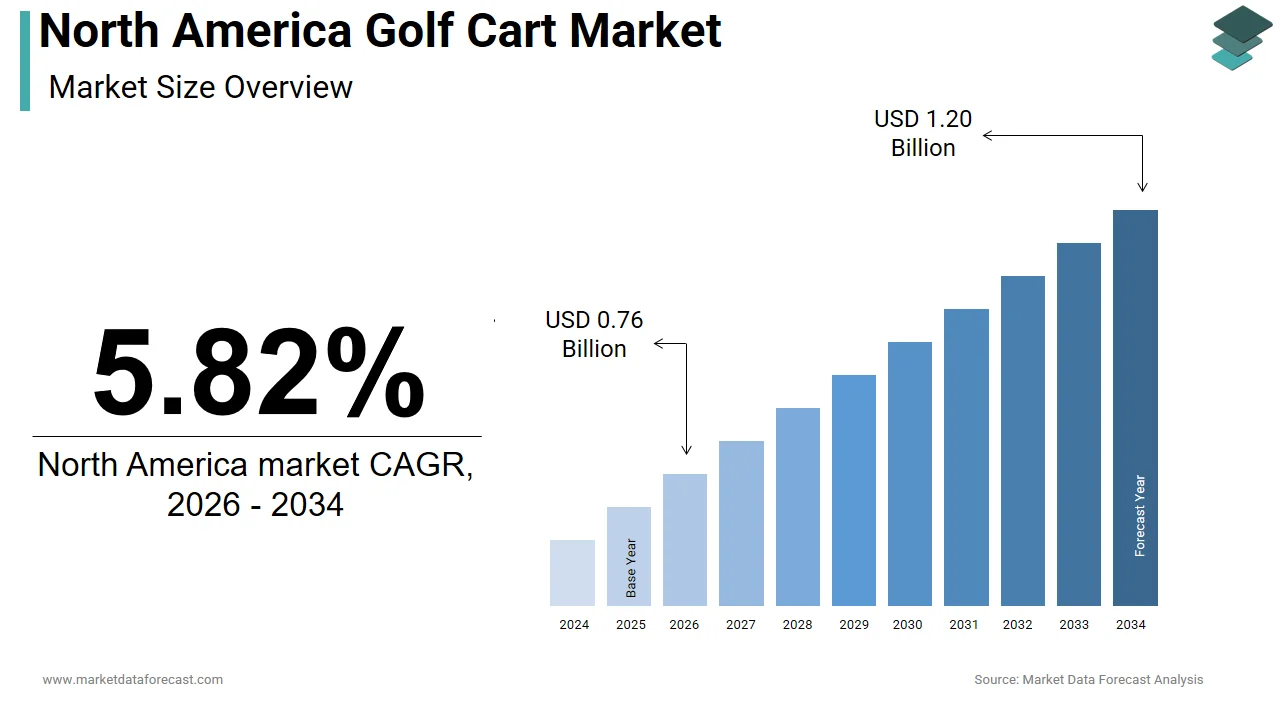

The size of the North America golf cart market was worth USD 0.72 billion in 2025. The regional market is anticipated to grow at a CAGR of 5.82% from 2026 to 2034 and be worth USD 1.20 billion by 2034 from USD 0.76 billion in 2026.

The golf carts are increasingly used in residential communities, resorts, industrial sites, and recreational facilities. The market has evolved significantly with technological advancements such as electric propulsion systems, GPS integration, and enhanced battery efficiency. As per data from the National Golf Foundation, over 24 million Americans played golf on a course in 2023, which is marking a sustained interest in the sport post-pandemic, which has contributed to the continued demand for golf carts. In addition to recreational usage, non-golf applications have gained traction. For instance, as reported by IBISWorld, the rise of gated communities and large-scale commercial complexes in the U.S. has driven alternative uses for golf carts as eco-friendly transportation solutions. Moreover, environmental concerns have accelerated the shift from gasoline-powered carts to electric models. According to the Electric Drive Transportation Association, more than 60% of newly sold carts in North America in 2023 were electric variants. This transition aligns with broader sustainability goals across the continent.

MARKET DRIVERS

Expansion of Recreational and Tourism Infrastructure

The expansion of recreational and tourism infrastructure is primarily prompting the growth of the North America golf cart market. Golf remains a popular sport across the United States and Canada, with many resorts, country clubs, and private communities integrating golf courses into their offerings. According to the American Recreation Coalition, outdoor recreation contributes over $450 billion annually to the U.S. economy, supporting millions of jobs. Additionally, the trend of "stay-and-play" destinations has surged in recent years, particularly following the pandemic, where travelers seek all-inclusive experiences combining leisure with sports. This has led to increased investment in resort-based golf courses, especially in states like Florida, Arizona, and California, where golf tourism thrives year-round. As per Golf Digest, Florida alone added over 20 new golf courses between 2020 and 2023, each requiring an average of 50–100 carts. The proliferation of such facilities directly correlates with rising demand for both new and replacement carts.

Adoption of Electric Golf Carts Due to Environmental Regulations

The widespread adoption of electric golf carts is due to stringent environmental regulations and a growing consumer preference for sustainable transportation options. Governments across the U.S. and Canada have implemented policies aimed at reducing carbon emissions, encouraging the shift from internal combustion engine (ICE) vehicles to cleaner alternatives. According to Environment and Climate Change Canada, over 80% of new golf cart purchases in Canada during 2023 were electric models, reflecting a strong regulatory push toward zero-emission mobility.

In the U.S., several states including California and New York have introduced mandates restricting the use of gas-powered vehicles in enclosed or semi-enclosed environments such as parks, campuses, and residential areas. These regulations have spurred manufacturers like Club Car, E-Z-GO, and Yamaha to prioritize electric models in their product lines. In fact, as per a report published by Freedonia Focus Reports, sales of electric golf carts accounted for nearly 70% of total unit sales in the U.S. in 2023. Additionally, improvements in lithium-ion battery technology have extended operational range and reduced charging times, enhancing the appeal of electric carts for commercial users. The U.S. Department of Energy notes that lithium-ion batteries now offer up to 40% greater energy density compared to lead-acid alternatives, making them more viable for frequent, long-duration usage.

MARKET RESTRAINTS

High Initial Purchase Cost of Advanced Electric Models

The high initial purchase cost associated with advanced electric models is an attribute that is restricting the growth of the North America golf cart market. While these carts offer long-term benefits such as lower maintenance expenses and reduced fuel dependency, their upfront costs remain significantly higher than traditional gas-powered alternatives. This cost disparity poses a barrier to entry for smaller golf facilities, independent operators, and budget-conscious consumers. A survey conducted by the National Golf Course Owners Association found that nearly 40% of small club owners cited affordability as a major challenge when considering fleet upgrades to electric models. Additionally, while federal and state-level incentives exist to promote clean energy adoption, they often do not fully offset the initial expenditure. For example, the U.S. Department of Energy’s Clean Vehicle Rebate Project offers limited subsidies for certain low-speed electric vehicles but excludes many standard golf cart configurations.

Limited Regulatory Clarity for On-Road Use

The lack of uniform regulatory clarity regarding the legal operation of golf carts on public roads is also limiting the growth of the North America golf cart market. While some jurisdictions allow low-speed vehicles (LSVs), including modified golf carts, on designated roadways under specific conditions, others impose strict limitations or outright prohibitions. According to the Governors Highway Safety Association, only 28 U.S. states had established formal laws permitting LSVs on public roads as of early 2023. For instance, in Florida, golf carts can be driven on roads with speed limits of up to 35 mph if registered and equipped with necessary features like turn signals and seat belts. However, in neighboring Georgia, similar use is restricted to local ordinances, meaning access is inconsistent across counties. This patchwork of regulations creates uncertainty for manufacturers and consumers alike, limiting the potential for widespread adoption of street-legal golf carts. As per a study published by the Insurance Institute for Highway Safety, inconsistent compliance standards have also led to increased accident risks, prompting further hesitancy among policymakers to expand permissions.

MARKET OPPORTUNITIES

Growth of Smart and Connected Golf Cart Technologies

The development and adoption of smart and connected technologies integrated into modern carts is an effective factor fuelling the growth of the North America golf cart market. Manufacturers are increasingly embedding advanced features such as GPS tracking, telematics, mobile app integration, and autonomous navigation capabilities to enhance user experience and operational efficiency. Leading companies such as Club Car and Yamaha have introduced models equipped with touchscreen displays, real-time performance monitoring, and cloud-based analytics tools. These innovations allow golf course managers to optimize fleet usage, track maintenance schedules, and even monitor player activity to improve course design and engagement. For example, Club Car's “OnCommand” system enables remote diagnostics and software updates, reducing downtime and repair costs. Moreover, the integration of Internet of Things (IoT) sensors allows for predictive maintenance, helping facility operators avoid unexpected breakdowns and costly repairs.

Expansion into Utility and Industrial Applications

The growing adoption of these vehicles in utility and industrial applications is also creating new opportunities for the growth of the North America golf cart market. Municipalities, universities, corporate campuses, and security services are increasingly utilizing modified golf carts for transport, surveillance, and logistics due to their compact size, ease of maneuverability, and low environmental impact. Furthermore, the rise of micro-mobility solutions in urban planning has prompted cities to explore lightweight, low-speed vehicles as alternatives for short-distance travel. For instance, as reported by the Urban Land Institute, several municipalities, including Austin, Texas, and Portland, Oregon, have incorporated electric carts into municipal operations for park management and downtown patrols. Additionally, industrial parks and large manufacturing facilities are repurposing golf carts for internal logistics, particularly in warehouse and inventory management.

MARKET CHALLENGES

Battery Supply Chain Constraints and Material Costs

The volatility in battery supply chains and escalating raw material costs for lithium-ion batteries used in electric models is likely to restrict the growth of the North America golf cart market. The global shift toward electrification has intensified demand for key components such as lithium, cobalt, and nickel, leading to supply shortages and price fluctuations. Manufacturers reliant on imported battery cells face additional hurdles due to geopolitical tensions and trade restrictions. North American producers are sourcing battery components from Asia, encountering logistical delays and increased tariffs, which is impacting production timelines and cost structures. These constraints have led some companies to delay product launches or reconsider investment plans. Moreover, recycling infrastructure for end-of-life lithium-ion batteries remains underdeveloped, raising concerns about long-term sustainability and disposal costs.

Seasonal Demand Fluctuations and Weather Dependency

The seasonal nature of demand, heavily influenced by weather patterns and climate conditions, is another factor impeding the growth of the North America golf cart market. Since the primary use of golf carts is tied to outdoor golf activities, sales and usage peak during warmer months, typically spanning from spring through early fall. According to the National Oceanic and Atmospheric Administration, prolonged winter seasons and unseasonably cold temperatures in regions such as the Northeast and Midwest in 2022–2023 led to a temporary decline in golf participation rates, directly impacting cart sales. Data from Golf Datatech indicates that Q1 2023 saw a 12% year-over-year drop in new cart registrations compared to the previous year, largely attributed to adverse weather conditions.

This seasonality creates cash flow challenges for manufacturers and dealers who must manage inventory and staffing levels accordingly. Moreover, extreme weather events linked to climate change, such as hurricanes, floods, and droughts, are becoming more frequent, disrupting both production cycles and retail availability. For example, Hurricane Ian in late 2022 caused extensive damage to golf courses in Florida, temporarily stalling new cart purchases until recovery efforts were completed.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Yamaha Golf-Car Company (Georgia, U.S.), Textron Inc. (Rhode Island, U.S.), Suzhou Eagle Electric Vehicle Manufacturing Co. Ltd. (Suzhou, China), CLUB CAR (Georgia, U.S.), Cruise Car, Inc. (Florida, U.S.), Garia, Inc. (Texas, U.S.), JH Global Services, Inc. (South Carolina, U.S.), SHOWA DENKO K.K. (Tokyo, Japan), and Columbia Vehicle Group Inc. (Wisconsin, U.S.). |

SEGMENTAL ANALYSIS

By Product Type Insights

The electric golf cart segment is expected to hold a dominant share of the North America golf cart market in 2025. According to a report published by Freedonia Focus Reports, over 75,000 electric golf carts were sold across the United States and Canada in that year alone. As per Environment and Climate Change Canada, more than 80% of new golf cart purchases in Canada are now electric, reflecting strong policy incentives and consumer preference shifts. Additionally, advancements in battery technology have significantly improved the performance and efficiency of electric models. According to the U.S. Department of Energy, lithium-ion batteries now offer up to 40% higher energy density compared to older lead-acid alternatives by enabling longer operational cycles and faster charging times.

The solar-powered golf carts segment is anticipated to grow with a CAGR of 14.2% during the forecast period. For instance, companies like Taylor-Dunn and Polaris have introduced hybrid solar-electric models capable of recharging via rooftop panels, which extends operational range without grid dependency. Also, the increasing adoption of solar-powered carts in eco-tourism and green community developments is anticipated to lead to the growth of the segment. As reported by the International Renewable Energy Agency, over 200 gated residential communities in the U.S. have integrated solar-assisted transport systems since 2021, including solar-charged golf carts for internal commuting. Additionally, government-backed sustainability initiatives, such as California’s Zero Emission Vehicle Program, have encouraged manufacturers to explore solar integration options.

By Application Insights

The golf course application segment dominated the North America golf cart market share in 2025. According to Golf Digest, over 14,000 golf facilities operate across the United States, each typically maintaining fleets ranging from 20 to 150 carts, by depending on course size and visitor volume. In Florida alone a state with the highest concentration of golf courses, more than 2,000 facilities exist, which is collectively contribute to a significant portion of national cart demand. As per data from the National Golf Foundation, over 24 million Americans played on-course golf in 2023, marking a slight increase from the previous year and reversing a long-standing decline trend. Additionally, post-pandemic recovery has led to renewed interest in outdoor leisure activities, prompting many clubs to modernize their fleets. A survey conducted by the Golf Industry Association found that nearly 45% of club managers planned fleet upgrades between 2023 and 2025, prioritizing electric models with enhanced navigation and comfort features. Moreover, the rise of “golf tourism” has further bolstered demand.

The commercial services application segment is emerging with a CAGR of 11.8% from 2026 to 2034, with the increasing utilization of golf carts in non-traditional sectors such as security patrols, municipal operations, campus transportation, and industrial logistics. The growing emphasis on sustainable urban mobility solutions is ascribed to fuel the growth of the segment. Municipalities like Austin, Texas, and Portland, Oregon, have incorporated electric carts into city planning strategies for park maintenance and downtown surveillance, citing benefits such as zero tailpipe emissions and low noise levels, as reported by the Urban Land Institute. Additionally, warehouse operators and logistics firms are repurposing carts for short-distance material handling. Furthermore, the proliferation of micro-mobility initiatives in smart cities has prompted public and private sector entities to adopt lightweight, low-speed vehicles for designated zones.

COUNTRY-LEVEL ANALYSIS

United States Golf Cart Market Insights

The United States was the top performer in the North America golf cart market, with 83.3% of share in 202,4 with the country's vast golf infrastructure, extensive recreational culture, and widespread adoption of golf carts beyond traditional settings. As reported by the National Golf Foundation, the U.S. is home to over 15,000 golf facilities, more than any other nation, collectively driving substantial demand for both personal and commercial cart usage. The warm climate allows for year-round play, making it a hotspot for both domestic and international golf tourism. Moreover, states like Arizona, Nevada, and California have seen a surge in retirement communities where golf carts serve as primary modes of transport. According to the U.S. Department of Transportation, over 400 master-planned communities have integrated golf cart pathways into urban design, expanding utility beyond sports.

Canada Golf Cart Market Insights

Canada was positioned second with 14.3% of the North America golf cart market share in 2024. Though smaller in scale compared to the U.S., the Canadian market has demonstrated steady growth, particularly in urban and recreational applications. As per Golf Canada, the country hosts over 2,300 golf courses with provinces such as Ontario, British Columbia, and Alberta experiencing notable increases in golf-related activity post-pandemic. The increasing use of golf carts in university campuses and municipal parks is anticipated to fuel the growth of the market in this country. For example, the University of Toronto and McGill University have both expanded their fleet of electric carts for maintenance and security purposes, aligning with broader sustainability goals. Additionally, Environment and Climate Change Canada reports that over 75% of new golf cart purchases in the country in 2023 were electric, reflecting strong regulatory support for low-emission mobility solutions. The Canadian government has also been promoting green transportation through initiatives such as the Zero Emission Vehicle Infrastructure Program, which indirectly supports the adoption of electric carts in both recreational and commercial settings.

COMPETITIVE LANDSCAPE

The competition in the North America golf cart market is characterized by a mix of established players and emerging brands striving to capture market share through innovation, diversification, and strategic positioning. While a few dominant firms control the majority of the market, smaller manufacturers and local players are increasingly entering niche segments by offering specialized or cost-effective alternatives. The rivalry is particularly intense between leading brands like Club Car, E-Z-GO, and Yamaha, each focusing on enhancing product performance and expanding application areas. Competitive differentiation is achieved through technological advancements, superior design, and customer-centric services. Additionally, the growing trend of electrification and sustainability is pushing companies to invest heavily in R&D to develop cleaner, more efficient models.

KEY MARKET PLAYERS

Noteworthy Companies dominating the North America golf cart market profiled in the report are

- Yamaha Golf-Car Company

- Textron Inc.

- Suzhou Eagle Electric Vehicle Manufacturing Co. Ltd.

- CLUB CAR

- Cruise Car, Inc.

- Garia, Inc.

- JH Global Services, Inc.

- SHOWA DENKO K.K.

- Columbia Vehicle Group Inc.

TOP LEADING PLAYERS IN THE MARKET

- Club Car is a leading name in the global golf cart industry and holds a significant presence in North America. Known for its innovation and product reliability, the company offers a wide range of electric and gas-powered carts tailored for both recreational and utility applications. Club Car has consistently invested in research and development to enhance performance, comfort, and sustainability. Its commitment to integrating smart technologies into carts has positioned it as a preferred choice among resorts, golf courses, and residential communities.

- E-Z-GO is another dominant player with a strong footprint across North America. The brand is recognized for its durable and high-performance golf carts that cater to diverse customer needs. E-Z-GO has focused on expanding beyond traditional golf use by offering customized solutions for commercial and industrial settings.

- Yamaha has established itself as a formidable competitor in the North America golf cart market by leveraging its reputation for engineering excellence. The company produces technologically advanced carts known for superior handling, durability, and user experience. Yamaha’s focus on innovation includes developing energy-efficient models and incorporating digital features for enhanced functionality. Its strong distribution network and after-sales service further support its competitive edge in the regional market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Product Innovation and Technology Integration Leading players prioritize continuous product development to introduce advanced features such as GPS navigation, telematics, and improved battery systems. Manufacturers aim to enhance user experience and operational efficiency by appealing to both recreational and commercial users by integrating smart technologies.

Expansion into Diverse Applications Beyond traditional golf course usage, companies are diversifying into utility, tourism, and municipal sectors. Customized carts for security patrols, campus transport, and logistics help firms tap into new revenue streams and reduce dependency on seasonal demand fluctuations.

RECENT MARKET DEVELOPMENTS

- In February 2023, Club Car launched an updated line of electric golf carts featuring integrated GPS and smartphone connectivity, which is aiming to enhance user experience and appeal to tech-savvy consumers.

- In June 2023, E-Z-GO introduced a new fleet management system designed for large-scale operations by allowing golf course managers to monitor cart performance and schedule maintenance remotely.

- In October 2023, Yamaha partnered with a renewable energy firm to pilot solar-charged golf cart stations at select resorts, which is aligning with broader sustainability goals and exploring alternative power sources.

- In January 2024, a major distributor in the U.S. Southwest expanded its dealership network by opening ten new service centers by improving accessibility and after-sales support for customers across multiple states.

- In May 2024, a joint initiative between two leading manufacturers and a university resulted in the deployment of autonomous electric carts for campus transportation by marking a step toward future mobility solutions in controlled environments.

MARKET SEGMENTATION

This North America golf cart market research report is segmented and sub-segmented into the following categories.

By Product Type

- Electric

- Gasoline

- Solar

By Application

- Golf Course

- Personal Services

- Commercial Services

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

What is driving growth in the North America Golf Cart Market?

Market growth is driven by rising golf participation, urban mobility needs, sustainable transport initiatives, and the adoption of electric carts

Which segment dominates the North America Golf Cart Market?

Electric golf carts are the leading segment, holding the largest share due to zero emissions, lower costs, and enhanced battery technologies

How are golf carts used beyond golf courses in North America?

Beyond golf, carts are widely used in hospitality, airports, gated communities, retirement living, resorts, and increasingly as urban mobility solutions

Who are the top manufacturers in the North America Golf Cart Market?

Key players include Yamaha Motor Co. Ltd., Textron Specialized Vehicles, Platinum Equity Advisors, Garia Inc., and Nordic Group of Companies

What role does sustainability play in the market?

Sustainability is a major factor, with demand rising for electric and solar-powered models that support emission reduction and green mobility goals

What technological innovations are shaping the North America Golf Cart Market?

Advancements include improved lithium-ion batteries, GPS navigation, IoT integration, smart controls, and luxury customization options

How is regulation affecting the North America Golf Cart Market?

Emission regulations and local mobility ordinances are encouraging electric and low-speed vehicle adoption, shaping purchasing decisions and product innovations

Which applications are expanding fastest in the North America Golf Cart Market?

Non-golf applications, hospitality, commercial services, airports, and short-distance transportation, show the fastest growth rates

What are the main challenges facing the North America Golf Cart Market?

Challenges include competition from alternative micro-mobility solutions, initial electric vehicle costs, and infrastructure development for charging

How do customization and luxury features impact the market?

Greater demand for luxury and personalized carts drives innovation, with enhanced sound systems, aesthetics, and multi-purpose utility carts increasing in popularity

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com