North America Hair Styling Product Formulations Market Size, Share, Trends & Growth Forecast Report By Product (Pomade, Hair Spray), End-Use, Distribution Channel, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

Market Size, 2025

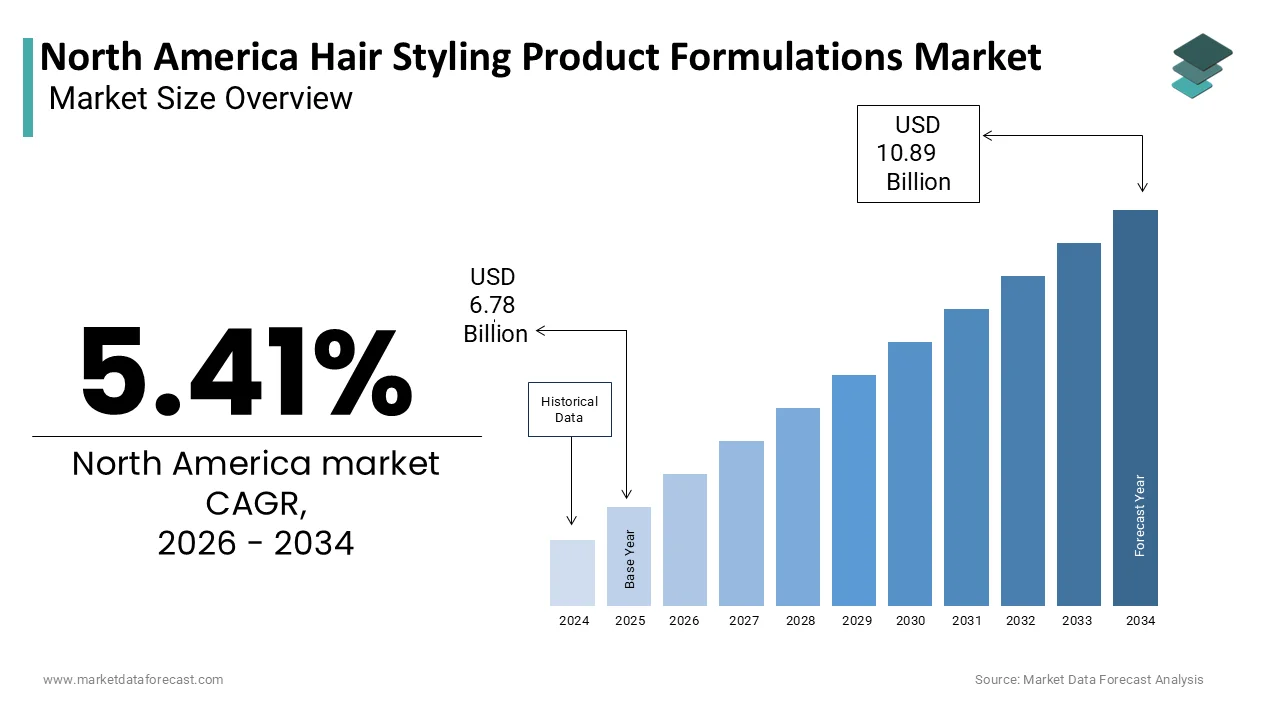

$6.78 BnMarket Estimate, 2026

$7.14 BnMarket Forecast, 2034

$10.89 BnCAGR, 2026–2034

5.41%North America Hair Styling Product Formulations Market Size

The North America Hair styling product formulations market size in North America was valued at USD 6.78 billion in 2025 and is predicted to be worth USD 10.89 billion by 2034, from USD 7.14 billion in 202,6 and grow at a CAGR of 5.41% from 2026 to 2034.

The hair styling product formulations are designed to shape, hold, texture, and protect hair, including gels, mousses, sprays, pomades, and creams. Unlike finished goods, this domain focuses specifically on the ingredient architecture, rheological properties, and functional chemistry that define performance, safety, and sensory experience. These formulations are increasingly driven by advances in polymer science, emulsification technology, and biomimetic actives that balance hold strength with scalp compatibility. The region’s consumer base exhibits highly diverse hair types and styling needs, ranging from fine, straight hair to tightly coiled, curly textures, necessitating tailored formulation strategies. This diversity has prompted formulators to prioritize inclusivity in product design, particularly in humidity resistance, frizz control, and curl definition. Additionally, regulatory oversight by the U.S. Food and Drug Administration and Health Canada mandates transparency in ingredient labeling and safety assessments, influencing the adoption of non-irritant preservatives and biodegradable polymers.

MARKET DRIVERS

Rising Consumer Demand for Multi-Functional and Hybrid Formulations

The growing consumer preference for multi-functional products that combine styling efficacy with hair health benefits is escalating the growth of the North America hair styling product formulations market. Modern users increasingly seek formulations that not only provide hold and texture but also deliver conditioning, heat protection, UV defense, and damage repair in a single application. According to the NPD Group, over 68% of consumers in the U.S. now prioritize products labeled as “2-in-1” or “3-in-1,” reflecting a shift toward minimalist, efficient routines. This demand has prompted formulators to integrate active ingredients such as hydrolyzed keratin, panthenol, and ceramides into styling bases, traditionally dominated by synthetic polymers.

Expansion of Inclusive Hair Care for Curly, Coily, and Textured Hair Types

The increasing emphasis on inclusive hair care for curly, coily, and textured hair types is a major driving factor for the growth of the North American hair styling formulations market. Historically, many styling products were designed for straight or wavy hair, leaving consumers with Type 3 and Type 4 curls underserved. According to the Pew Research Center, African Americans constitute 13.6% of the U.S. population, with over 85% reporting regular use of styling products to define curls and reduce frizz, as documented by the Journal of the National Medical Association. Formulators are incorporating humectants like shea butter and agave nectar, alongside cationic polymers such as Polyquaternium-7, to enhance moisture retention and reduce electrostatic repulsion in tightly coiled strands. The Curl Collective, a consumer research initiative, found that 79% of curly-haired users avoid alcohol-containing products due to dryness, compelling brands to replace ethanol with milder solvents. Additionally, the rise of the “natural hair movement” has spurred demand for sulfate-free, silicone-free, and fragrance-conscious formulations.

MARKET RESTRAINTS

Regulatory Scrutiny on Potentially Harmful Ingredients in Styling Products

The intensifying regulatory and consumer scrutiny surrounding certain chemical ingredients traditionally used for hold, texture, and preservation is restricting the growth of the North American hair styling product formulations market. Ingredients such as formaldehyde-releasing preservatives, phthalates, and high concentrations of volatile organic compounds (VOCs) have come under investigation for potential health risks. The U.S. Food and Drug Administration has issued multiple warnings about formaldehyde in Brazilian blowout treatments, with testing by the National Institute for Occupational Safety and Health revealing formaldehyde levels exceeding 10 ppm in several keratin-based styling products, posing inhalation risks to salon workers. Additionally, California’s Proposition 65 mandates labeling for products containing dibutyl phthalate, a plasticizer historically used in flexible hold gels, due to endocrine disruption concerns. The Environmental Working Group has flagged over 40 styling products for high hazard scores based on ingredient toxicity. In response, formulators face the challenge of replacing these functional but controversial components with safer alternatives without compromising performance. For instance, replacing alcohol-based hold systems with plant-derived polymers often results in reduced stiffness or increased tackiness, requiring extensive R&D to balance aesthetics and safety. Health Canada has also tightened restrictions on nano-sized particles in aerosol sprays, affecting delivery mechanisms.

High Cost and Technical Complexity of Sustainable Ingredient Sourcing

The financial and technical challenges associated with sourcing sustainable, bio-based, and biodegradable ingredients are also hindering the growth of the North American hair styling product formulations market. While demand for eco-conscious products is rising, the transition from petroleum-derived polymers like PVP and acrylates to renewable alternatives such as fermented polylactic acid or sugar-based resins remains hindered by scalability and performance limitations. According to the Biotechnology Innovation Organization, fewer than 15 bio-derived styling polymers are commercially viable at scale, and their production costs are 30–50% higher than synthetic counterparts. Additionally, natural ingredients like plant-based waxes and oils often exhibit batch-to-batch variability in viscosity and stability, complicating formulation consistency. The Sustainable Beauty Coalition reports that 62% of formulators face delays in obtaining certified sustainable raw materials, particularly in emollients and film-formers.

MARKET OPPORTUNITIES

Advancements in Biomimetic and Peptide-Enhanced Styling Technologies

The integration of biomimetic science and peptide-based actives that enhance hair strength and resilience during styling is expected to promote new opportunities for the growth of the North American hair styling product formulations market. According to the Society of Cosmetic Chemists, over 30 peptide variants are now being evaluated for their ability to mimic natural hair proteins, offering reparative benefits within styling matrices. Brands like Olaplex and K18 have pioneered this approach, incorporating bond-building technology into leave-in treatments and heat protectants, effectively merging styling with restoration. These formulations require advanced encapsulation techniques to ensure peptide stability in aqueous and alcohol-based systems, driving innovation in delivery mechanisms. The growing acceptance of “cosmeceutical” claims, though not regulated as drugs, has opened a premium segment where performance and science converge. Academic collaborations, such as those between MIT’s Media Lab and beauty biotech firms, are accelerating the development of self-repairing polymers inspired by biological structures.

Growth of Customizable and On-Demand Formulation Platforms

The emergence of customizable and on-demand hair styling formulation platforms is also expected to enhance the growth of the North America hair styling product formulations market. Enabled by digital diagnostics and AI-driven analysis, these systems allow consumers to receive tailored products based on hair type, climate, lifestyle, and styling goals. Prose is a New York-based brand that uses an algorithm that analyzes over 80 data points from scalp condition to local humidity levels to create bespoke shampoos and styling creams. According to the company’s internal data, users of personalized formulations report a 41% improvement in hold longevity and reduced frizz compared to off-the-shelf products. This model relies on modular formulation architecture, where base polymers, humectants, and conditioning agents are blended in real time, requiring advanced rheological control and sterile filling systems. Additionally, in-salon customization is gaining traction, with devices like the L’Oréal Hair Coach smart brush collecting real-time data to recommend ingredient adjustments.

MARKET CHALLENGES

Balancing Performance with Clean-Label and Hypoallergenic Claims

The reconciling high-performance styling outcomes with the growing demand for clean-label, hypoallergenic, and dermatologically tested products is likely to degrade the growth of the North America hair styling product formulations market. Consumers increasingly avoid parabens, sulfates, synthetic fragrances, and silicones, yet these ingredients have historically delivered functionality, such as long-lasting hold, smooth application, and shine. According to the American Contact Dermatitis Society, allergic reactions to cocamidopropyl betaine and methylisothiazolinone, common in “natural” gels and mousses, increased by 34% between 2018 and 2022, with the safety perception of alternative chemistries. Formulators must now design systems that maintain stiffness and humidity resistance using plant-based polymers like guar hydroxypropyltrimonium chloride, which often require co-formulants to prevent flaking.

Intellectual Property Constraints and Ingredient Patent Landscapes

The dense intellectual property (IP) landscape surrounding proprietary polymers, delivery systems, and functional actives is additionally expected to hinder the growth of the North America hair styling product formulations market. Many high-performance ingredients, such as PVP/VA copolymers, styling resins, and silicone emulsions, are protected by long-standing patents held by chemical suppliers like BASF, Dow, and Ashland. According to the United States Patent and Trademark Office, over 1,200 active patents relate to hair styling polymers, with key formulations guarded for up to 20 years, limiting generic substitution. This restricts independent formulators and smaller brands from replicating proven technologies without licensing agreements, which can be cost-prohibitive. For example, the patent for Polyquaternium-11, a cationic polymer widely used in anti-frizz sprays, was only recently expired, opening limited avenues for reformulation. Additionally, trade secrets around emulsification techniques and viscosity modifiers prevent full transparency, forcing companies to reverse-engineer or develop novel alternatives. The Society of Cosmetic Chemists notes that over 60% of new product launches require freedom-to-operate assessments to avoid infringement. This legal complexity slows innovation, particularly for startups aiming to enter the premium segment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, End-Use, Distribution Channel, and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, and the rest of North America |

| Market Leaders Profiled | L’Oréal, Tresemmé, John Paul Mitchell Systems, Brylcreem, Unilever, Kao Corporation, Henkel AG & Co., KGaA, Shiseido Company, Procter & Gamble Company, and others |

SEGMENTAL ANALYSIS

By Product Insights

The hair spray segment accounted in holding 54.3% of the North American hair styling product formulations market share in 2024, with its universal applicability, versatility across hair types, and integration into both daily routines and professional salon treatments. Their aerosol or pump-based delivery systems allow for even distribution and reworkability, which is particularly valued in dynamic styling environments. According to the U.S. Environmental Protection Agency, over 78 million aerosol hair care products were sold in the United States in 202, with sustained consumer reliance on spray formats. Additionally, the National Cosmetology Association reports that 92% of licensed stylists use hair sprays during client services for setting styles by reducing flyaways, and providing humidity resistance.

The pomade segment is deemed to grow at a CAGR of 8.9% during the forecast period, owing to the resurgence of textured, defined hairstyles among men and the increasing adoption of pomades by women seeking natural, touchable finishes. The NPD Group reports that pomade sales in the U.S. grew by 14% year-over-year in 2023, outpacing other styling formats. This growth is further fueled by social media influence, where platforms like TikTok and Instagram showcase pomade-driven styles such as the “textured quiff” and “slick back.” Additionally, the expansion of men’s grooming into premium and specialty retail channels has elevated pomade’s positioning from a niche product to a core styling essential. With formulators now incorporating natural waxes, shea butter, and CBD extracts, the segment is attracting both clean-beauty advocates and performance-driven users, accelerating its market penetration.

By End-Use Insights

The women’s segment accounted for a prominent share of the North America hair styling product formulations market in 2024, with the complexity and diversity of women’s hair routines, which often involve multiple styling steps, product layering, and frequent use of heat tools. Women’s hairstyles tend to be longer, more voluminous, and subject to greater environmental stress, necessitating advanced formulations for hold, volume, and damage mitigation. According to the U.S. Census Bureau, women spend an average of 42 minutes daily on personal care, with hair styling constituting a significant portion. According to the Journal of the American Academy of Dermatology, 74% of women use heat styling tools at least twice a week, increasing demand for heat-protectant sprays, volumizing mousse, and frizz-control serums.

The men’s segment is solely growing with an expected CAGR of 9.3% from 2025 to 2033, with the evolving perception of male grooming as an essential aspect of self-presentation, rather than a luxury. Men are increasingly investing in personal care, with a focus on achieving defined, polished hairstyles that reflect individuality and confidence. The NPD Group reports that men’s styling product sales grew by 16% in 2023, outpacing women’s categories for the first time in a decade. Social media, celebrity influence, and the normalization of salon visits have dismantled traditional stigmas around male grooming. Additionally, the rise of hybrid work environments has increased demand for “polished yet natural” looks, driving adoption of lightweight gels, texturizing sprays, and pomades. The Professional Beauty Association notes that men now account for 38% of all salon visits in the U.S., up from 22% in 2015, indicating a structural shift in behavior.

By Distribution Channel Insights

The Hypermarkets & Supermarkets segment accounted in holding 52.3% of the North America hair styling product formulations market share in 2024, with the accessibility, affordability, and impulse-purchase dynamics of mass retail environments. Major chains such as Walmart, Target, and Kroger offer extensive hair care aisles featuring both drugstore and mid-tier brands, enabling consumers to purchase styling products alongside daily essentials. According to the Food Marketing Institute, the average American visits a supermarket 1.6 times per week, creating frequent touchpoints for product discovery. The U.S. Census Bureau reports that over 70% of personal care products are purchased in physical retail stores, with shampoo and styling items among the top categories. Additionally, promotional strategies such as multi-buy discounts, end-cap displays, and brand sampling significantly influence consumer decisions.

The online distribution channel segment in the North America hair styling product formulations market is projected to expand at a CAGR of 12.4% from 2025 to 2033 wit,,h the increasing preference for convenience, personalized shopping experiences, and access to niche and premium brands unavailable in physical stores. Consumers are increasingly turning to e-commerce platforms such as Amazon, Ulta.com, and brand-owned websites to research ingredients, read reviews, and purchase products with home delivery. The U.S. Department of Commerce reports that online sales of personal care products grew by 18% in 2023, with hair styling categories outperforming others. Subscription models, such as those offered by Prose and Function of Beauty, allow for customized formulations delivered regularly by enhancing customer retention. Additionally, social commerce, where users purchase directly through Instagram or TikTok links, has accelerated adoption among younger demographics.

REGIONAL ANALYSIS

United States Hair Styling Product Formulations Market Insights

The United States was the dominant force in the North American hair styling product formulations market, holding an estimated 80% of regional revenue in 2023, as per Kline & Company. As the largest consumer market for personal care products, the U.S. combines demographic diversity, high disposable income, and a deeply ingrained beauty culture to drive innovation and demand. The U.S. Census Bureau reports a population of over 334 million, with significant representation from African American, Hispanic, and Asian communities, each with distinct hair care traditions and styling needs. This diversity has prompted formulators to develop inclusive product architectures that address curl pattern, porosity, and environmental exposure. The American Academy of Dermatology notes that over 60% of African American women use leave-in conditioners and styling creams weekly, fueling demand for high-moisture, low-alcohol formulations. Regulatory oversight by the FDA and growing consumer reliance on ingredient transparency platforms like EWG further shape formulation strategies.

Canada Hair Styling Product Formulations Market Insights

Canada accounted for holding 15.4% of the North American hair styling product formulations market share in 202,4 owing to the high product penetration, strong regulatory alignment with the U.S., and a growing emphasis on clean, sustainable beauty. Health Canada enforces strict ingredient labeling and safety standards, influencing the adoption of non-toxic preservatives and biodegradable polymers. The Canadian Cosmetic, Toiletry and Fragrance Association reports that 68% of consumers prefer products labeled as “paraben-free” or “sulfate-free,” driving reformulation efforts. Urban centers like Toronto, Vancouver, and Montreal exhibit high demand for premium and salon-exclusive brands, supported by a dense network of beauty retailers and barbershops. The rise of homegrown brands like Habit Cosmetics and Humbyrd reflects growing consumer sophistication.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

L’Oréal, Tresemmé, John Paul Mitchell Systems, Brylcreem, Unilever, Kao Corporation, Henkel AG & Co., KGaA, Shiseido Company, and Procter & Gamble Company

The competitive landscape of the North American hair styling product formulations market is characterized by a dynamic interplay between legacy conglomerates, agile indie brands, and science-driven startups, each vying for influence through innovation, inclusivity, and sustainability. Dominant players leverage extensive R&D infrastructure and global supply chains to maintain formulation superiority, while emerging brands disrupt with niche positioning, clean ingredients, and digital-first engagement. Competition is no longer confined to hold strength or scent but extends to molecular compatibility, scalp safety, and environmental impact. The rise of personalized beauty has intensified the race to develop adaptive, data-informed formulations that respond to individual hair biology and lifestyle factors. Ingredient transparency, ethical sourcing, and carbon footprint are now differentiators, which is compelling companies to reengineer legacy systems. Barriers to entry remain high due to regulatory scrutiny and the complexity of polymer chemistry, yet open innovation models and biotech partnerships are democratizing access to advanced actives. Regional diversity drives demand for culturally relevant solutions, particularly for textured and curly hair, reshaping formulation priorities. With social media amplifying consumer voice, brands must balance scientific rigor with authenticity and inclusivity. The market is evolving into a sophisticated ecosystem where technological advancement, ethical responsibility, and emotional resonance collectively define competitive advantage.

TOP PLAYERS IN THE MARKET

L’Oréal

L’Oréal stands as a dominant force in theNorth Americana hair styling product formulations market, leveraging its unparalleled R&D capabilities and deep understanding of diverse hair types. Through its professional division, L’Oréal Professionnel, and consumer brands like Garnier and Redken, the company pioneers advanced polymer systems, heat-protectant technologies, and curl-defining architectures tailored to the region’s multicultural consumer base. Its formulation expertise spans from mass-market aerosols to high-performance salon-grade gels and creams, integrating dermatological insights with sensory refinement. L’Oréal’s global influence is evident in its patent portfolios, ingredient partnerships, and sustainability initiatives, which set industry benchmarks.

Procter & Gamble (P&G)

Procter & Gamble plays a pivotal role in shaping the hair styling formulations landscape through its portfolio of trusted brands, including Pantene, Herbal Essences, and Aussie. The company combines decades of polymer science expertise with consumer behavior research to develop accessible, high-efficacy formulations that balance hold, shine, and hair health. P&G’s formulation strategies emphasize scalp compatibility, residue reduction, and multi-benefit integration, particularly in heat protection and damage repair. Its global R&D network enables rapid translation of scientific advances into scalable product architectures, ensuring consistency across markets.

Unilever

Unilever is a key architect of modern hair styling formulations, which is driving innovation through brands such as TRESemmé, Dove, and Living Proof. The company distinguishes itself by merging clinical dermatology with consumer-centric design, creating products that deliver strong hold without compromising hair integrity. Unilever’s formulation philosophy emphasizes clean-label transitions, sulfate-free systems, and humidity-resistant polymers that cater to textured and chemically treated hair. Its investment in digital diagnostics and AI-driven personalization has positioned it at the forefront of adaptive styling science. Through strategic collaborations with ingredient suppliers and academic institutions, Unilever advances sustainable chemistry and scalable green formulations. The company’s global reach and commitment to inclusive beauty have made it a trendsetter in developing solutions for diverse curl patterns and scalp conditions, setting standards that resonate across international markets and reinforcing its status as a formulation leader.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

One major strategy employed by leading players is the integration of dermatological and trichological science into styling formulations to enhance scalp and hair health, transforming styling products from aesthetic tools into wellness-focused solutions. This approach strengthens brand credibility and aligns with growing consumer demand for safe, long-term hair care.

Another key strategy is the development of personalized and direct-to-consumer (DTC) platforms that use AI and consumer data to create bespoke formulations, enabling brands to differentiate through precision, exclusivity, and deeper customer engagement beyond traditional mass-market offerings.

Another important strategy is the advancement of sustainable formulation architectures, including bio-based polymers, water-efficient systems, and recyclable delivery mechanisms, by allowing companies to meet evolving regulatory expectations and consumer preferences for environmentally responsible beauty without sacrificing performance.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, L’Oréal launched a new biomimetic polymer platform under its Redken brand, designed to repair disulfide bonds during styling by enhancing hair strength while providing flexible hold. This innovation is anticipated to redefine the performance standards for professional-grade styling products.

- In August 2023, Procter & Gamble introduced a water-efficient formulation architecture across its Pantene line, reducing water content in gels and mousses by reformulating with concentrated actives, aiming to lower environmental impact without compromising product efficacy.

- In November 2023, Unilever partnered with a biotech startup to integrate fermented plant-based resins into TRESemmé’s spray formulations, whichares replacing petroleum-derived polymers and advancing the brand’s sustainable chemistry roadmap.

- In January 2024, L’Oréal expanded its personalized hair care platform, Prose, with a new AI-powered diagnostic tool that analyzes user-submitted hair images to optimize styling product formulations for texture, porosity, and climate exposure.

- In June 2024, Procter & Gamble acquired a specialty ingredient firm focused on scalp-compatible film formers, enabling the development of next-generation hold systems that minimize irritation and buildup, particularly for sensitive and textured hair consumers.

MARKET SEGMENTATION

This research report on the North AmAmericanair styling product formulations market has been segmented and sub-segmented based on the following categories.

By Product

- Hair Gel

- Hair Wax

- Hair Mousse

- Hair Spray

- Pomade

- Others

By End-Use

- Male

- Female

By Distribution Channel

- Hypermarkets and Supermarkets

- Convenience Stores

- Specialty Stores

- Online

- Others

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

1. What is the North America Hair Styling Product Formulations Market?

It covers gels, sprays, mousses, and creams designed to style and maintain diverse hair types.

2. What drives growth in the North America Hair Styling Product Formulations Market?

Rising beauty awareness, demand for natural products, and fashion trends fuel strong growth.

3. Which country leads the North America Hair Styling Product Formulations Market?

The U.S. leads with high consumer spending, followed by Canada and Mexico.

4. What are popular formulations in the North America Hair Styling Product Formulations Market?

Top types include gels, waxes, mousses, sprays, pomades, creams, and serums.

5. Which distribution channels are key in the North America Hair Styling Product Formulations Market?

Supermarkets, salons, specialty stores, and online platforms drive sales.

6. Who are leading players in the North America Hair Styling Product Formulations Market?

L’Oréal, P&G, Unilever, Henkel, Johnson & Johnson, and organic brands dominate.

7. What trends shape the North America Hair Styling Product Formulations Market?

Eco-friendly packaging, vegan products, and tailored solutions for curly hair.

8. How is technology impacting the North America Hair Styling Product Formulations Market?

Innovations add heat protection, humidity resistance, and long-lasting hold.

9. Which consumer groups drive the North America Hair Styling Product Formulations Market?

Women lead demand, while men’s grooming and youth styling are growing fast.

10. What challenges face the North America Hair Styling Product Formulations Market?

Key issues include high competition, counterfeit products, and raw material costs.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com