North America Laboratory Freezers Market Research Report - Segmented By Product (Ultra-Low Freezer, Blood Bank Refrigerator, Pharmacy Refrigerator, Cryopreservation Plasma Freezer, Explosion-Proof Freezer, Enzyme Freezer, Chromatography Refrigerator), By End User & By Country (U.S., Canada & Rest of North America) - Industry Analysis From 2026 to 2034

North America Laboratory Freezers Market Summary

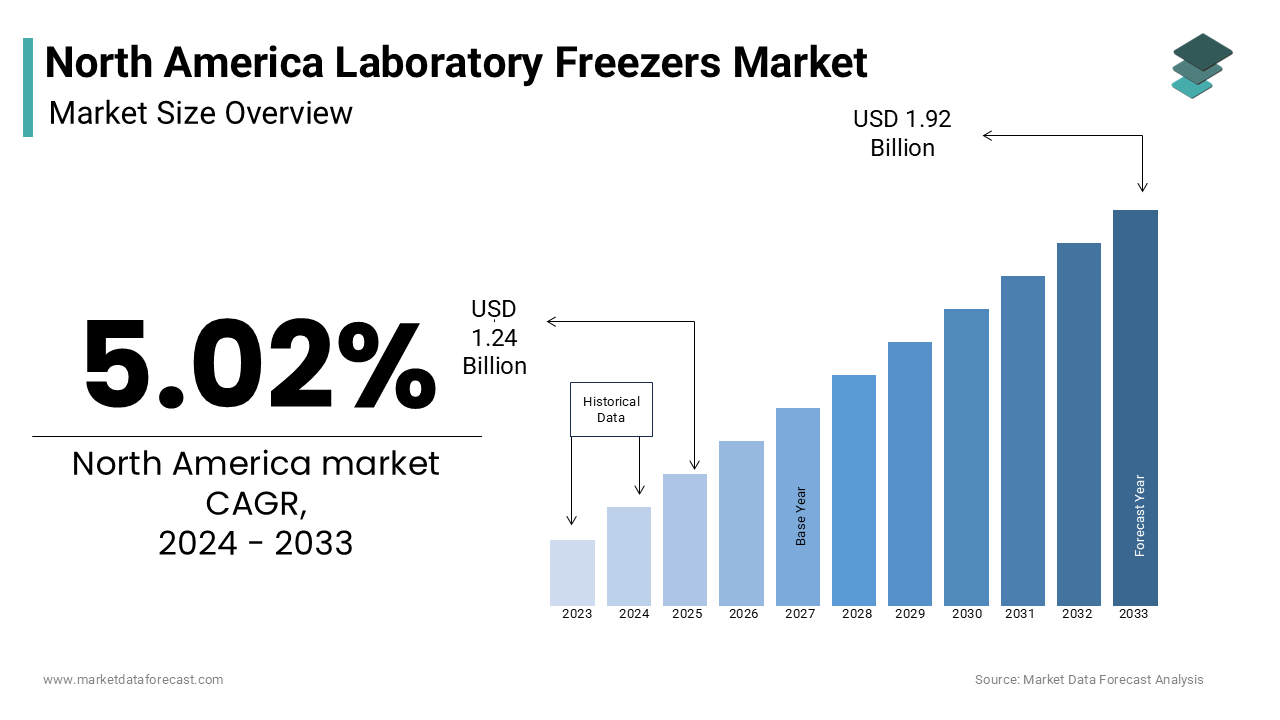

The North America laboratory freezers market was valued at USD 1.30 billion in 2025 and is projected to reach USD 2.03 billion by 2034, growing at a CAGR of 5.02% from 2026 to 2034.

Growth is driven by expanding biobanking infrastructure, rising life sciences R&D, and increased cold storage needs for personalized medicine, vaccine development, and decentralized diagnostics. Smart, IoT-enabled, and energy-efficient freezer systems are shaping the market’s future.

Key Market Trends & Insights

- United States led the regional market with a 75.3% share in 2025.

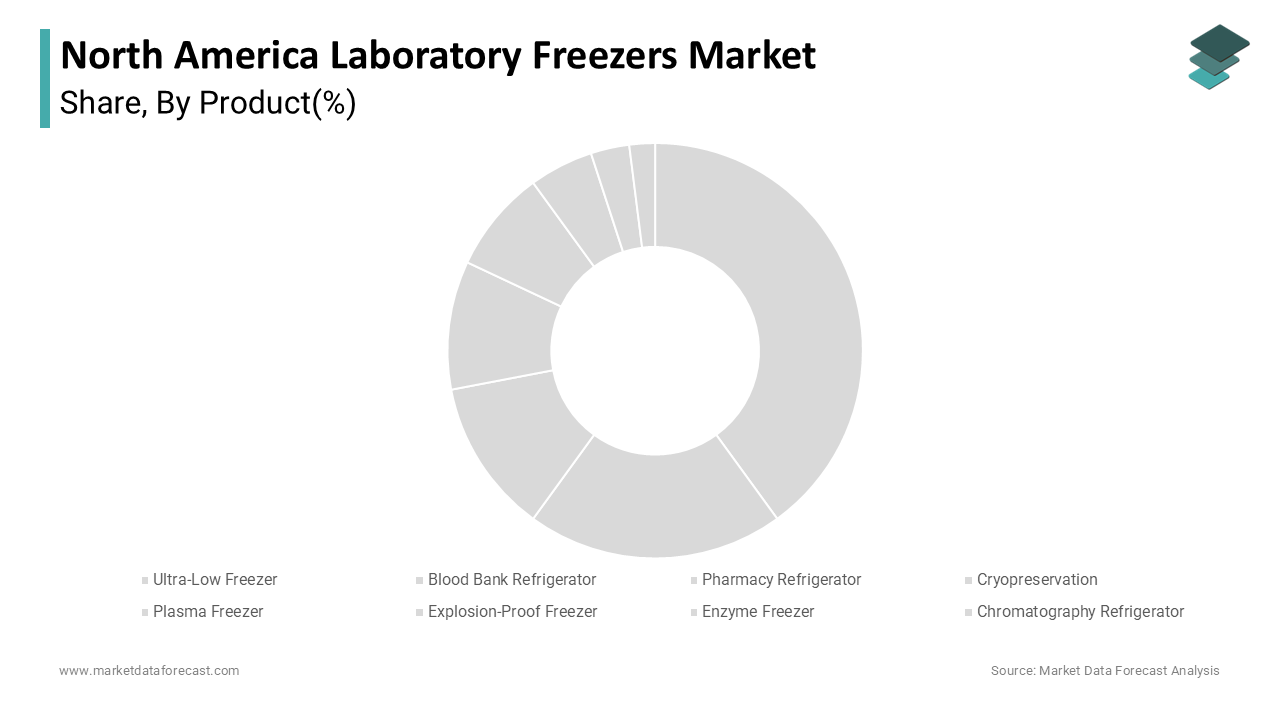

- Ultra-low temperature freezers held the largest product share at 35.4% in 2025.

- Pharmaceutical & biotechnology companies were the largest end users at 30.2% in 2025.

- The cryopreservation segment is the fastest-growing with a CAGR of 12.3%.

- Academic and research institutes are expected to grow at 11.8% CAGR through 2034.

Market Size & Forecast

- 2025 Market Size: USD 1.30 Billion

- 2034 Projected Market Size: USD 2.03 Billion

- CAGR (2026–2034): 5.02%

- United States: Largest market in 2025

- Canada: Gaining momentum through biomanufacturing and academic investments

North America Laboratory Freezers Market Size

The North America laboratory freezers market size was valued at USD 1.30 billion in 2025 and is anticipated to reach USD 1.37 billion in 2026 from USD 2.03 billion by 2034, growing at a CAGR of 5.02% during the forecast period from 2026 to 2034.

Laboratory freezers are specialized refrigeration systems designed to maintain ultra-low temperatures for preserving biological samples, reagents, vaccines, and other temperature-sensitive materials used in research, clinical diagnostics, and pharmaceutical development. These units typically operate at temperatures ranging from -40°C to -86°C and are essential for ensuring sample integrity in laboratories across academic institutions, biobanks, hospitals, and life sciences companies. The North America laboratory freezers market is experiencing steady growth, driven by the increasing demand for reliable cold storage solutions in biomedical research and healthcare infrastructure. The growing emphasis on precision medicine, genomic research, and vaccine development has significantly increased the need for advanced cryogenic storage capabilities. Additionally, regulatory agencies such as the FDA have mandated stringent storage conditions for biological products, which further reinforces the adoption of high-performance laboratory freezers. Technological advancements, including energy-efficient models with smart monitoring systems, are also shaping market dynamics.

MARKET DRIVERS

Expansion of Biobanking Infrastructure

One of the key drivers fueling the growth of the North America laboratory freezers market is the rapid expansion of biobanking infrastructure. Biobanks are centralized repositories that collect, process, store, and distribute biospecimens for use in research and clinical applications. According to the International Society for Biological and Environmental Repositories (ISBER), North America hosts more than 40% of the world's biobanks, with the U.S. alone accounting for over 300 operational biorepositories. This proliferation is largely supported by federal funding initiatives, such as those provided by the National Institutes of Health (NIH), which has allocated over USD 500 million since 2020 toward biobank-related research and infrastructure development. These investments directly correlate with increased procurement of laboratory freezers equipped with precise temperature controls and data-logging capabilities. Moreover, the integration of biobanks into large-scale genomics and personalized medicine programs is intensifying storage requirements.

Rising R&D Expenditure in Life Sciences

Another pivotal driver of the North America laboratory freezers market is the surge in research and development (R&D) expenditure within the life sciences sector. Governments and private entities in the U.S. and Canada have consistently increased their investments in biomedical research, pharmaceutical innovation, and diagnostic development sectors that heavily rely on cold storage infrastructure. As per the Battelle Memorial Institute, total U.S. R&D spending reached USD 660 billion in 2022, with life sciences accounting for nearly 30% of this investment. In addition, academic and government-funded research institutions are expanding their laboratory capacities. Moreover, the rise in contract research organizations (CROs) and contract manufacturing organizations (CMOs) supporting pharmaceutical development has amplified the demand for modular and scalable freezer systems.

MARKET RESTRAINTS

High Capital and Operational Costs

A major restraint impeding the growth of the North America laboratory freezers market is the substantial capital and ongoing operational costs associated with acquiring and maintaining these systems. Beyond acquisition, the energy consumption of ULT freezers poses a considerable financial burden. According to My Green Lab, a non-profit organization focused on sustainable laboratory practices, a single ULT freezer consumes approximately 18 kWh per day equivalent to the annual electricity usage of two average American households. Furthermore, maintenance and repair expenses add to the overall cost of ownership. Annual servicing, parts replacement, and potential downtime due to system failures can escalate operational expenditures.

Regulatory Compliance and Stringent Standards

Stringent regulatory compliance and quality assurance standards represent another significant challenge for the North America laboratory freezers market. Manufacturers must adhere to a complex array of regulations set forth by agencies such as the U.S. Food and Drug Administration (FDA), the Centers for Disease Control and Prevention (CDC), and the Occupational Safety and Health Administration (OSHA). These regulations govern aspects such as temperature accuracy, alarm systems, validation protocols, and environmental safety. For example, the FDA mandates that laboratories storing regulated biological materials follow Good Manufacturing Practices (GMP) and maintain documented evidence of temperature stability. Compliance with these requirements often necessitates the installation of validated freezers with calibrated sensors, remote monitoring systems, and backup power sources all of which elevate procurement and implementation costs. Additionally, international standards such as ISO 9001 and ISO 14644-1 further complicate the design and certification process for laboratory freezer manufacturers. As reported by the Association for the Advancement of Medical Instrumentation (AAMI), the time required to validate a new freezer model for clinical use can extend beyond six months, delaying market entry and increasing development expenditures.

MARKET OPPORTUNITIES

Integration of Smart Technologies and IoT-enabled Systems

A prominent opportunity emerging in the North America laboratory freezers market is the integration of smart technologies and Internet of Things (IoT)-enabled systems into freezer designs. These innovations allow for real-time monitoring, predictive maintenance, and enhanced energy management, aligning with the broader digital transformation occurring in laboratory environments.

IoT-enabled freezers can transmit continuous temperature readings, send alerts during deviations, and integrate with laboratory information management systems (LIMS), thereby enhancing workflow efficiency. Manufacturers like Eppendorf AG and Panasonic Healthcare have introduced cloud-connected freezer models equipped with AI-driven analytics that assess performance trends and flag potential malfunctions before they occur. Moreover, the push for sustainability in laboratories has spurred interest in intelligent energy optimization features. Energy Star-certified freezers with adaptive cooling algorithms can reduce electricity consumption by up to 40%, according to the U.S. Department of Energy. Growth of Point-of-Care Diagnostics and Decentralized Research Models

The emergence of point-of-care diagnostics and decentralized research models presents a compelling growth avenue for the North America laboratory freezers market. Unlike traditional centralized labs, decentralized models involve conducting research and diagnostic procedures closer to patients or field locations, necessitating compact and portable freezing solutions.

The rise of mobile testing units, pop-up labs, and community-based research initiatives especially post-pandemic has increased the demand for smaller, transportable ultra-low freezers. Pharmaceutical companies engaged in decentralized clinical trials are increasingly relying on field-deployed freezers to store investigational drugs and biomaterials. For example, Pfizer and Moderna have incorporated mobile freezer units in their trial logistics to support rural and remote participant enrollment. Additionally, universities and public health departments are deploying mini-freezers in educational outreach and surveillance programs. The CDC’s recent initiative to equip regional clinics with sub-zero freezers for flu vaccine distribution exemplifies this trend.

MARKET CHALLENGES

Environmental Impact and Refrigerant Regulations

A critical challenge confronting the North America laboratory freezers market is the environmental impact associated with refrigerants and the tightening of related regulations. Traditional ultra-low temperature freezers often utilize hydrofluorocarbons (HFCs), potent greenhouse gases that contribute significantly to climate change when released into the atmosphere. The U.S. Environmental Protection Agency (EPA) has implemented phasedown measures under the American Innovation and Manufacturing (AIM) Act, which is aiming to reduce HFC production and consumption by 85% over the next 15 years. Moreover, end-users face additional complexities in handling and disposing of legacy units. The Cold Chain Sustainability Initiative, backed by several North American universities, estimates that replacing outdated freezers with environmentally compliant models could cost institutions millions of dollars collectively.

Supply Chain Disruptions and Component Shortages

Supply chain disruptions and component shortages have emerged as a formidable challenge for the North America laboratory freezers market, affecting production timelines and pricing structures. The ongoing global semiconductor shortage, exacerbated by geopolitical tensions and logistical bottlenecks, has impacted the availability of critical components such as microcontrollers, compressors, and electronic control boards used in modern freezer systems. Additionally, raw material price volatility has compounded the issue. The U.S. Bureau of Labor Statistics recorded a 17% increase in industrial metal prices between 2021 and 2023, driven by surges in copper, aluminum, and steel costs. These fluctuations have led to double-digit price hikes for laboratory freezers, straining budgets for smaller research institutions and hospital networks.

SEGMENTAL ANALYSIS

By Product Insights

The ultra-low temperature freezers segment was the largest by capturing 35.4% of in the North America laboratory freezers market share in 2024. One key driver behind the dominance of ULT freezers is the expansion of genomic and proteomic research, which necessitates long-term storage of biological samples at temperatures below -70°C. According to the National Institutes of Health (NIH), over 800 biorepositories operate in the U.S., each requiring an average of 30 to 60 ULT freezers for sample preservation.

The cryopreservation freezers segment is lucratively growing with a CAGR of 12.3% in the next coming years. A primary driver is the rising adoption of cell and gene therapies, which require ultra-stable freezing conditions for preserving live cells and tissues. Additionally, advancements in automated freezing systems have enhanced process efficiency and sample viability, encouraging their integration into commercial labs and biotech firms.

By End User Insights

The pharmaceutical and biotechnology companies segment held 30.2% of the North America laboratory freezers market share in 2025. One key growth driver is the accelerated pace of drug discovery and development, particularly in oncology, neurology, and infectious diseases. The FDA approved a record 61 novel therapeutics in 2023, many of which required stable cold storage during preclinical and clinical testing phases. Another contributing factor is the outsourcing trend in drug development, with rising reliance on contract research organizations (CROs) and contract manufacturing organizations (CMOs).

The academic and research institutes segment is likely to grow with an estimated CAGR of 11.8% in the next coming years. A key growth enabler is the increase in federal research grants, particularly from the National Institutes of Health (NIH). Moreover, universities are investing heavily in modernizing their laboratory facilities. The Association of American Universities (AAU) reported that member institutions collectively allocated over USD 15 billion toward lab upgrades and equipment purchases between 2022 and 2023. These upgrades include replacing aging freezer units with energy-efficient models featuring IoT-enabled monitoring capabilities. In addition, the rise of interdisciplinary research hubs and biobanking collaborations between academic institutions and hospitals is further amplifying demand for scalable and secure freezer solutions tailored to academic settings.

REGIONAL ANALYSIS

United States Laboratory Freezers Market Insights

The United States was the top performer in the North America laboratory freezers market by capturing 75.3% of the share in 2024. One of the core drivers is the high concentration of biopharmaceutical companies and research institutions. According to the Biotechnology Innovation Organization (BIO), the U.S. hosts over 9,000 life sciences firms, including leading players such as Pfizer, Merck, and Amgen. These companies invest heavily in lab infrastructure, including freezer systems for storing drug candidates, vaccines, and biomaterials. Additionally, the country’s strong government support for scientific research plays a pivotal role. Furthermore, the U.S. leads in biobank development, with over 350 operational repositories nationwide. These facilities store millions of specimens annually, necessitating large-scale freezer deployments.

Canada Laboratory Freezers Market Insights

Canada was positioned next by holding 15.3% of the North American laboratory freezers market share in 2024. A key growth catalyst is the expansion of Canada’s biomanufacturing sector, driven by federal initiatives such as the Strategic Innovation Fund (SIF) and the Canadian Biomedical Research Fund (CBRF). In 2022, the Canadian government committed CAD 4 billion toward strengthening domestic vaccine and therapeutic manufacturing capabilities, directly influencing freezer procurement in both private and public sectors. Additionally, the presence of world-class research universities contributes to sustained demand. Institutions like the University of Toronto and McGill University have significantly upgraded their lab infrastructure in recent years. Moreover, the growth of regional biobanks and tissue banks supports freezer adoption. The Canadian Tissue Repository Network (CTRNet) oversees over 60 biobanks, many of which require ultra-low temperature units for specimen preservation.

COMPETITIVE LANDSCAPE

The competition in the North America laboratory freezers market is characterized by a mix of established global players and emerging regional manufacturers striving to capture a larger share of the expanding market. As demand for reliable cold storage solutions grows across research institutions, pharmaceutical companies, and healthcare facilities, vendors are increasingly focusing on differentiation through product innovation, enhanced energy efficiency, and integration of smart technologies. The market landscape is marked by continuous advancements aimed at improving freezer performance, reducing environmental impact, and ensuring compliance with stringent regulatory requirements. While large multinational corporations dominate due to their extensive product portfolios and strong brand recognition, smaller firms are leveraging niche expertise and localized service networks to carve out a competitive advantage. Strategic collaborations, technology licensing agreements, and targeted marketing initiatives further intensify the rivalry among market participants. Additionally, the push toward sustainability and the development of next-generation refrigerants are shaping competitive strategies, prompting companies to reengineer existing models and introduce more eco-friendly alternatives.

KEY MARKET PLAYERS

Companies playing a dominant role in the North America Laboratory Freezers Market include

- VWR Corporation

- ARCTIKO A/S

- Biomedical Solutions Inc.

- EVERmed S.R.L.

- Philipp Kirsch GmbH

- Thermo Fisher Scientific Inc.

- Haier Biomedical

- Eppendorf AG

- Helmer Scientific

- Panasonic Healthcare Co., Ltd.

Top Players in the North America Laboratory Freezers Market

Thermo Fisher Scientific Inc.

Thermo Fisher Scientific is a global leader in laboratory equipment and solutions, with a strong presence in the North American laboratory freezers market. The company offers a comprehensive portfolio of ultra-low temperature freezers, cryogenic storage systems, and refrigeration units tailored for pharmaceutical, clinical, and research applications.

Eppendorf AG

Eppendorf is a prominent player recognized for its high-performance laboratory freezers designed for precision and sample integrity. The company serves diverse sectors including academic research, biobanking, and life sciences. Eppendorf’s commitment to developing energy-efficient and space-saving freezer models has made it a preferred choice among laboratories seeking optimized cold storage solutions.

Panasonic Healthcare Co., Ltd.

Panasonic Healthcare has established itself as a key contributor to the laboratory freezer market by delivering durable and technologically advanced freezing systems. The company focuses on enhancing energy efficiency and operational stability, particularly in ultra-low and plasma freezer categories. Its strategic collaborations with research institutions and healthcare providers support widespread adoption across North America. Panasonic's reputation for long-term reliability and continuous product refinement strengthens its competitive edge in the market.

Top Strategies Used by Key Market Participants

One major strategy employed by leading players is product innovation and technological advancement. Companies are investing heavily in R&D to develop energy-efficient, smart-connected, and sustainable freezer models that meet evolving regulatory and environmental standards. These innovations enhance performance, reduce operational costs, and improve user experience.

Another key approach is strategic partnerships and collaborations. Market leaders frequently engage with academic institutions, biobanks, and healthcare organizations to co-develop customized freezer solutions. These alliances help companies align their offerings with end-user needs while expanding their market reach and credibility.

The expansion through acquisitions and mergers is a prevalent growth tactic. Companies can strengthen their distribution networks, enhance service capabilities, and accelerate market penetration in North America by acquiring complementary firms or merging with regional players.

RECENT MARKET DEVELOPMENTS

- In January 2023, Thermo Fisher Scientific launched a new line of energy-efficient ultra-low temperature freezers featuring IoT-enabled monitoring systems. This initiative was aimed at enhancing user control and data accuracy while reducing overall power consumption, which reinforces the company’s dominance in sustainable lab equipment.

- In August 2023, Eppendorf AG expanded its North American service network by opening a dedicated technical support and repair center in Boston. The move was intended to provide faster maintenance response times and improved after-sales service to academic and research clients across the Northeastern U.S.

- In February 2024, Panasonic Healthcare introduced a collaboration with a major U.S. biobank to supply customized plasma freezers designed for long-term sample preservation. This partnership supported the growing need for specialized cold storage in personalized medicine and genomic research.

- In June 2024, Stirling Ultracold announced the release of a new line of compressor-free laboratory freezers designed for a reduced carbon footprint and lower operating costs. This innovation positioned the company as a sustainable alternative in the ultra-low freezer segment.

- In November 2024, Helmer Scientific acquired a software firm specializing in cold chain management solutions. This acquisition enabled Helmer to integrate real-time monitoring and predictive analytics into its freezer systems, which is strengthening its value proposition for healthcare and clinical labs.

MARKET SEGMENTATION

This research report on the North American laboratory freezers market is segmented and sub-segmented into the following categories:

By Product

- Ultra-Low Freezer

- Blood Bank Refrigerator

- Pharmacy Refrigerator

- Cryopreservation

- Plasma Freezer

- Explosion-Proof Freezer

- Enzyme Freezer

- Chromatography Refrigerator

By End User

- Blood Banks

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Medical Laboratories

- Hospitals

- Pharmacies

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What factors are driving the growth of the laboratory freezers market in North America?

Growth is driven by the rising demand for biopharmaceuticals, expanding research in genomics and cell biology, the need for safe storage of vaccines and biological samples, and increasing investments in healthcare infrastructure.

What challenges does this market face?

Key challenges include high energy consumption of ultra-low temperature freezers, stringent regulatory requirements for laboratory equipment, and the high cost of advanced freezers.

What is the future outlook for the North America laboratory freezers market?

The market is expected to experience steady growth due to rising biobanking activities, increased demand for personalized medicine, and expansion of clinical trials across the region.

What are the key trends shaping the laboratory freezers market in North America?

Major trends include the adoption of energy-efficient and environmentally friendly freezers, integration of IoT and remote monitoring systems, and a shift toward modular and compact freezer designs.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com