North America Medical Products Market Size, Share, Trends & Growth Forecast Report By Type (Diagnostic Imaging, Minimally Invasive Surgical (MIS)e), End-user and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

North America Medical Products Market Size

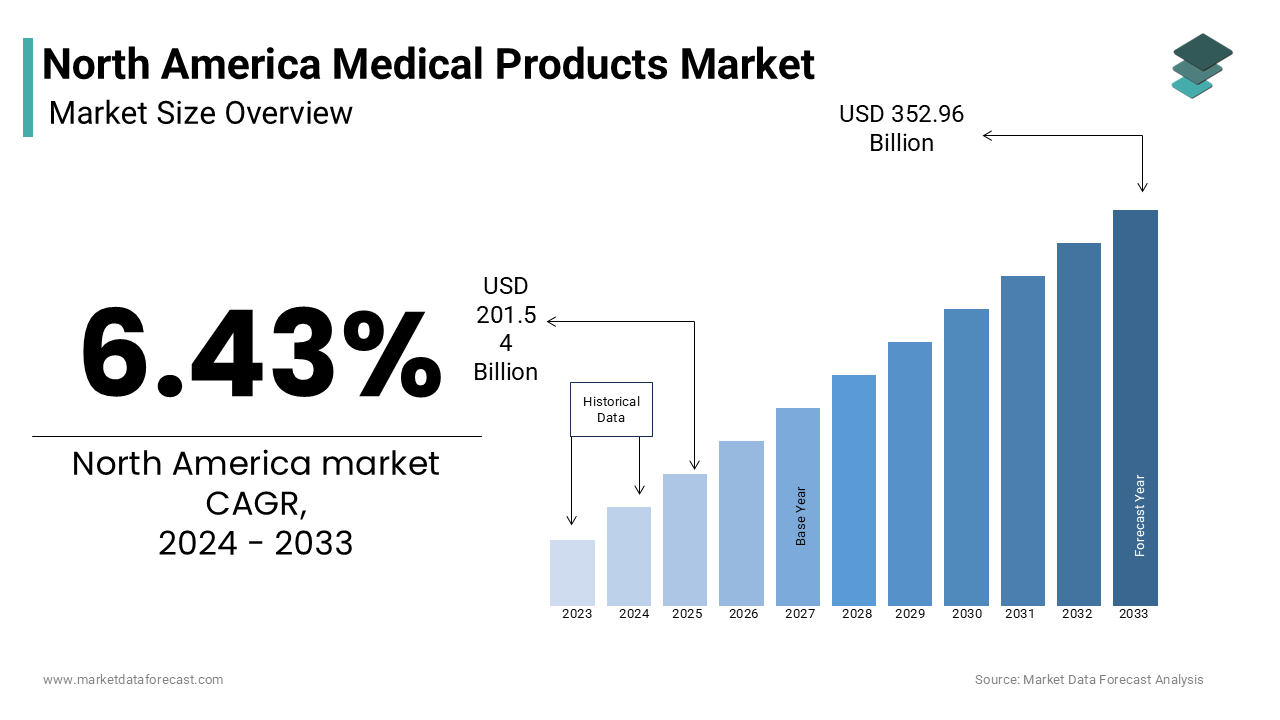

The North America medical products market size was valued at USD 214.50 billion in 2025 and is anticipated to reach USD 228.29 billion in 2026 from USD 375.84 billion by 2034, growing at a CAGR of 6.43% during the forecast period from 2026 to 2034.

Medical products are devices, equipment, consumables, and technologies designed for the diagnosis, treatment, monitoring, and prevention of diseases across diverse healthcare settings. This multifaceted sector includes everything from basic surgical instruments and diagnostic reagents to sophisticated imaging systems, implantable devices, and advanced therapeutic equipment utilized in hospitals, clinics, ambulatory surgery centers, and home healthcare environments. According to the U.S. Bureau of Labor Statistics, the healthcare sector employed over 17 million workers in 2023, creating a substantial demand for a wide array of medical products to support daily clinical operations and patient care delivery.

The market's evolution is significantly influenced by technological innovation, regulatory frameworks, demographic shifts, and evolving healthcare delivery models that prioritize efficiency, safety, and patient outcomes. The healthcare industry's increasing focus on value-based care and evidence-based medicine has elevated the importance of high-quality, cost-effective medical products that demonstrate clear clinical benefits and contribute to improved patient safety metrics. Furthermore, the integration of digital health technologies and the Internet of Medical Things (IoMT) is transforming traditional medical products into connected solutions, driving demand for smart devices and data management systems.

MARKET DRIVERS

Aging Population and Rising Chronic Disease Prevalence

The demographic transition toward an aging population and the concomitant rise in chronic disease prevalence across North America serve as primary catalysts for the expanding medical products market, generating sustained demand for diagnostic tools, therapeutic devices, and long-term care supplies. The Centers for Disease Control and Prevention underscores the magnitude of this challenge, reporting that 60% of adults in the United States live with at least one chronic condition, while 40% manage two or more concurrent chronic diseases, necessitating a continuous supply of medications, monitoring equipment, and medical devices. Cardiovascular diseases, affecting millions of adults, represent a significant driver for medical product demand, particularly for diagnostic equipment like ECG machines, therapeutic devices such as pacemakers and defibrillators, and pharmaceutical interventions. Millions of individuals are living with Alzheimer's disease, driving demand for assistive technologies, safety monitoring devices, and specialized care supplies tailored to cognitive decline and related behavioral challenges. Respiratory conditions, including asthma and chronic obstructive pulmonary disease (COPD), fueling the market for inhalation therapies, portable oxygen concentrators, and pulmonary function testing equipment. The complexity of managing multiple chronic conditions has led to increased hospitalization rates and emergency department visits, further amplifying the need for diverse medical products.

Technological Innovation and Digital Health Integration

The relentless pace of technological innovation and the seamless integration of digital health solutions within the North American healthcare landscape are potent drivers propelling the medical products market forward, creating demand for intelligent, connected, and data-driven medical devices and systems. Also, the adoption of connected medical devices has surged in the past five years, as healthcare providers seek to leverage real-time patient data, enhance care coordination, and improve clinical decision-making through integrated technology platforms. The convergence of artificial intelligence, machine learning, and the Internet of Medical Things (IoMT) has revolutionized traditional medical products, transforming them into smart, predictive tools capable of remote monitoring, early intervention, and personalized treatment protocols. Telemedicine integration has become a cornerstone of modern healthcare delivery, particularly accelerated by recent global health events, creating substantial demand for home-based diagnostic equipment, remote patient monitoring systems, and secure communication platforms that require specialized medical-grade hardware and software solutions. The development of precision medicine and personalized therapies has increased demand for advanced diagnostic products, including companion diagnostics, genetic testing kits, and biomarker analysis tools that enable targeted treatment strategies tailored to individual patient profiles. The emphasis on interoperability and health information exchange has accelerated the adoption of standardized medical products that can seamlessly integrate with electronic health records and hospital information systems, driving demand for compatible interfaces, data management solutions, and cybersecurity measures.

MARKET RESTRAINTS

Stringent Regulatory Environment and Compliance Costs

The highly stringent regulatory environment governing medical products in North America, while essential for ensuring safety and efficacy, presents a significant restraint to market growth by imposing substantial compliance costs, lengthy approval processes, and complex quality assurance requirements that can delay product launches and increase development expenses. The complexity of regulatory pathways has intensified with the implementation of risk-based classification systems and enhanced post-market surveillance requirements, necessitating continuous investment in quality management systems, adverse event reporting, and periodic safety updates. The regulatory approval timeline for innovative medical products can extend from 18 months for 510(k) clearances to 3-5 years for PMAs, creating significant cash flow pressures and opportunity costs for manufacturers operating in rapidly evolving market segments. Cross-border trade requirements necessitate compliance with multiple regulatory frameworks, including FDA, Health Canada, and provincial health authority standards, adding layers of complexity and cost for companies seeking to serve diverse North American markets. The shortage of qualified regulatory affairs professionals and quality assurance specialists has created bottlenecks in product development and market entry processes, limiting innovation velocity and responsiveness to emerging clinical needs.

Healthcare Cost Containment and Reimbursement Pressures

The persistent pressure for healthcare cost containment and the complex landscape of reimbursement policies across North American healthcare systems significantly constrain the medical products market by limiting adoption of premium-priced innovations and creating financial barriers for both manufacturers and healthcare providers. The shift toward bundled payments and capitated reimbursement models has forced healthcare providers to prioritize cost-effectiveness over technological advancement, often delaying the adoption of innovative medical products that may offer superior clinical outcomes but come at a higher initial cost. A notable share of hospitals operate with thin margins or deficits, compelling administrators to focus on reducing supply chain costs and standardizing product portfolios to achieve economies of scale. The complexity of navigating diverse reimbursement pathways, including Medicare, Medicaid, private insurance, and out-of-pocket payments, creates uncertainty for medical product manufacturers regarding market access and revenue potential. Payers increasingly require health technology assessments and real-world evidence to justify coverage decisions, extending the time between product launch and widespread market adoption. The emphasis on generic substitution and group purchasing agreements has intensified price competition and compressed profit margins for medical product manufacturers, particularly for commodity items and established technologies. The implementation of international reference pricing and value-based procurement initiatives has further pressured manufacturers to reduce prices while maintaining quality standards, limiting investment in research and development for next-generation products.

MARKET OPPORTUNITIES

Personalized Medicine and Companion Diagnostics

The emergence of personalized medicine and the parallel development of companion diagnostics present a transformative opportunity within the North American medical products market, creating demand for highly specialized diagnostic tools, targeted therapeutic agents, and precision delivery systems that cater to individual patient genetic profiles and disease characteristics. The integration of pharmacogenomics into clinical practice has increased demand for genetic testing platforms, sample collection devices, and data interpretation software that enable healthcare providers to tailor medication selection and dosing based on individual patient genetic variations. The development of liquid biopsy technologies and circulating tumor DNA analysis has created new market segments for minimally invasive diagnostic products that can monitor disease progression and treatment response in real-time. The emphasis on value-based care and outcomes measurement has increased payer acceptance of companion diagnostics that demonstrate clear clinical utility and cost-effectiveness, supporting broader market adoption and reimbursement coverage.

Home Healthcare and Remote Patient Monitoring

The rapid expansion of home healthcare services and the widespread adoption of remote patient monitoring technologies represent a significant growth opportunity within the North American medical products market, driven by demographic trends, healthcare delivery model evolution, and patient preference for convenient, accessible care options. The aging population demographic, with individuals aged 65 and older comprising of the North American population, prefers receiving care in familiar home environments, creating sustained demand for durable medical equipment, home diagnostic devices, and telehealth platforms that enable remote clinical management. Also, the adoption of remote patient monitoring solutions has surged over the past three years, driven by the need for chronic disease management, post-acute care coordination, and reduced hospital readmissions. The implementation of value-based care models and accountable care organizations has incentivized healthcare providers to invest in home healthcare infrastructure and remote monitoring technologies that improve patient outcomes while reducing overall care costs. The development of user-friendly, consumer-grade medical devices and mobile health applications has expanded the addressable market beyond traditional clinical settings, enabling patients to actively participate in their care through self-monitoring and data sharing. The integration of artificial intelligence and predictive analytics in remote monitoring systems has enhanced their clinical utility, enabling early intervention and proactive care management that prevents costly emergency department visits and hospitalizations.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Component Shortages

The North American medical products market faces persistent and evolving supply chain vulnerabilities and component shortages that have created critical operational challenges, increased costs, and threatened the continuity of essential healthcare services throughout 2023 and into 2024. Critical components such as specialized electronic chips, rare earth magnets, sterile packaging materials, and pharmaceutical ingredients have experienced extended lead times, price volatility, and intermittent unavailability due to global manufacturing disruptions, geopolitical tensions, and natural disasters. The reliance on international suppliers, particularly for active pharmaceutical ingredients, electronic components, and specialized raw materials sourced from Asia and Europe, has created significant vulnerabilities in the supply chain that impact inventory management and emergency preparedness efforts. The semiconductor shortage has particularly impacted smart medical devices and connected health technologies that incorporate digital monitoring and communication capabilities, with lead times for certain microprocessor components extending several weeks. Freight and logistics challenges, including port congestion, driver shortages, and fuel price fluctuations, have added to transportation costs, further pressuring procurement budgets and affecting medical product affordability. The concentration of key component manufacturing in specific geographic regions, such as semiconductor fabrication in Taiwan and rare earth processing in China, has amplified supply chain risks, making inventory diversification and supplier redundancy critical strategic imperatives for healthcare systems and medical product manufacturers.

Cybersecurity Threats and Data Privacy Concerns

The increasing connectivity and digital integration of medical products within the North American healthcare ecosystem have created significant cybersecurity vulnerabilities and data privacy concerns that pose substantial challenges to patient safety, regulatory compliance, and market confidence. The complexity of medical device ecosystems, which often include legacy systems, third-party software, and interconnected networks, creates numerous potential entry points for cybercriminals seeking to exploit vulnerabilities and gain unauthorized access to sensitive patient data or disrupt critical healthcare operations. The implementation of the FDA's Cybersecurity Guidance for Medical Devices has introduced new regulatory requirements for manufacturers to implement robust cybersecurity measures throughout the product lifecycle, including risk management, vulnerability assessment, and coordinated disclosure programs that add complexity and cost to device development and maintenance. The shortage of qualified cybersecurity professionals with healthcare expertise has created capacity constraints for healthcare organizations seeking to protect their expanding digital infrastructure and connected medical device fleets. Cross-border data transfer requirements and varying international privacy regulations, including GDPR for Canadian operations involving European data, add layers of compliance complexity for medical product manufacturers and healthcare providers operating in interconnected North American markets.

SEGMENTAL ANALYSIS

By Type Insights

The diagnostic imaging segment the dominant force in the North American medical products market by commanding the largest share due to its fundamental role in disease diagnosis, treatment planning, and patient monitoring across diverse medical specialties. The segment's dominance stems from the universal requirement for accurate diagnostic information across all medical specialties, from cardiology and oncology to orthopedics and neurology. The versatility of diagnostic imaging allows for application across diverse healthcare settings including hospitals, outpatient imaging centers, and specialized clinics, making it indispensable to healthcare delivery systems. Market participants have extensively adopted diagnostic imaging solutions due to their proven impact on patient outcomes, established reimbursement frameworks, and continuous technological advancements that enhance image quality and reduce radiation exposure. The segment's strength is further supported by regulatory frameworks that mandate specific imaging procedures for disease screening and treatment monitoring, as well as the growing emphasis on precision medicine that relies heavily on advanced imaging biomarkers.

The continuous wave of technological advancements and significant improvements in image quality have solidified diagnostic imaging as the largest segment in the North American medical products market, as healthcare providers invest in next-generation systems that offer superior diagnostic capabilities and enhanced patient experience. The development of hybrid imaging systems, such as PET-MRI and SPECT-CT, has revolutionized diagnostic capabilities by combining functional and anatomical imaging in single examinations, reducing patient examination time and improving diagnostic confidence. Also, advances in detector technology and image reconstruction algorithms have reduced radiation exposure in CT scans while maintaining or improving diagnostic image quality, addressing growing concerns about radiation safety in medical imaging. The implementation of cloud-based image storage and sharing platforms has enhanced workflow efficiency and enabled remote consultation capabilities. The miniaturization of imaging equipment and development of portable systems have expanded access to diagnostic imaging in point-of-care settings and mobile healthcare delivery models. The integration of augmented reality and virtual reality technologies in diagnostic imaging workflows has enhanced surgical planning and interventional procedures, creating new applications for advanced imaging systems in precision medicine and personalized treatment approaches.

The demographic shift toward an aging population and the increasing prevalence of chronic diseases across North America have created substantial demand for diagnostic imaging services and equipment that support disease screening, monitoring, and treatment evaluation in elderly patients with complex medical conditions. Cardiovascular diseases, which affect over 122 million adults according to the American Heart Association, represent a significant driver for diagnostic imaging demand, particularly for cardiac MRI, CT angiography, and echocardiography services that enable precise assessment of heart structure and function. As per the American Cancer Society, over 2 million new cancer cases are diagnosed annually in the United States, creating demand for advanced imaging systems including PET scanners, MRI systems, and molecular imaging equipment that support cancer staging, treatment planning, and response assessment. The complexity of managing multiple chronic conditions has increased hospitalization rates and specialist referrals.

The minimally invasive surgical devices segment is the fastest-growing segment in the North American medical products market. This growth of segment is due to the transformative impact of advanced surgical technologies including robotic-assisted systems, laparoscopic instruments, endoscopic devices, and image-guided navigation systems that enable complex procedures through small incisions while maintaining surgical precision and clinical outcomes. The segment's expansion encompasses diverse applications across multiple surgical specialties including general surgery, urology, gynecology, orthopedics, and cardiothoracic surgery, with market participants investing heavily in next-generation MIS platforms that enhance surgeon dexterity and patient safety. The segment's growth is particularly pronounced in applications requiring precision instrumentation, real-time visualization, and advanced tissue manipulation capabilities that support complex therapeutic interventions with minimal patient trauma. Government initiatives supporting value-based care and healthcare cost containment have created substantial market opportunities for MIS device manufacturers and healthcare providers seeking to optimize resource utilization and improve patient satisfaction.

The overwhelming patient preference for minimally invasive surgical procedures and the demonstrated benefits of enhanced recovery outcomes have accelerated the growth of MIS devices as the fastest-growing segment in the North American medical products market, as healthcare consumers increasingly demand treatment options that minimize pain, scarring, and recovery time. The implementation of enhanced recovery after surgery (ERAS) protocols has increased demand for MIS devices that support rapid patient mobilization, reduced opioid utilization, and shortened hospital stays. The cosmetic benefits of smaller incisions and reduced scarring have particularly influenced patient decision-making in elective procedures. The integration of patient-reported outcome measures in healthcare quality assessment has elevated the importance of patient satisfaction and functional recovery metrics, supporting adoption of MIS technologies that demonstrate superior performance in these domains. The expansion of outpatient surgery centers and ambulatory surgical facilities has increased access to minimally invasive procedures.

The rapid advancement of surgical technology and the widespread adoption of robotic surgical systems have significantly accelerated the growth of minimally invasive surgical devices in the North American medical products market, as healthcare providers invest in sophisticated platforms that enhance surgical precision, reduce human error, and expand the capabilities of complex therapeutic interventions. The development of next-generation robotic systems featuring enhanced dexterity, tremor reduction, and three-dimensional visualization has enabled surgeons to perform increasingly complex procedures through minimally invasive approaches. The implementation of artificial intelligence and machine learning algorithms in surgical navigation and tissue analysis has enhanced decision-making capabilities during minimally invasive procedures. The miniaturization of surgical instruments and development of single-incision laparoscopic surgery platforms have expanded the applicability of minimally invasive techniques to previously challenging anatomical regions, creating new market opportunities for specialized MIS devices. The emphasis on surgeon training and credentialing programs for advanced MIS techniques has accelerated adoption of robotic surgical systems and specialized instrumentation.

By End-user Insights

The hospitals and ambulatory surgery centers segment was the prominent end-user segment in the North American medical products market. This dominance of segment is because of hospitals serving as the primary destination for complex medical procedures, emergency care, and specialized treatments that require access to advanced medical technologies, specialized staff, and comprehensive inventory management systems. The segment's strength is reinforced by the sophisticated nature of healthcare delivery in hospital settings, which requires access to advanced diagnostic equipment, therapeutic devices, and comprehensive inventory systems that can support diverse clinical scenarios from routine procedures to complex surgical interventions. The segment's dominance is further supported by established reimbursement frameworks, regulatory requirements for healthcare delivery capabilities, and continuous technological advancements that enhance clinical effectiveness and operational efficiency. Market participants have extensively targeted hospital and ASC end users due to their purchasing power, standardized procurement processes, and the critical nature of medical product requirements that demand reliable supplier relationships and comprehensive product portfolios.

The overwhelming volume of complex medical procedures and the sophisticated specialized equipment requirements within hospital and ambulatory surgery center settings have established these facilities as the dominant end-user segment in the North American medical products market, creating sustained demand for diverse and advanced medical products that support immediate patient care and life-saving interventions. The complexity of modern medical care requires hospitals and ASCs to maintain comprehensive inventories of specialized products including advanced surgical instruments, implantable devices, diagnostic reagents, and monitoring equipment that enable immediate intervention for life-threatening conditions and complex therapeutic interventions. The implementation of hospital quality metrics and patient outcome measures has increased demand for advanced monitoring products, evidence-based therapeutic devices, and standardized clinical protocols that support clinical decision-making and treatment effectiveness. Trauma center designations and specialized care capabilities require hospitals to maintain extensive inventories of specialized products including massive transfusion protocols, surgical airway equipment, and advanced resuscitation medications that represent significant components of medical product expenditures.

The extensive technology adoption and substantial capital equipment investment requirements within hospital and ambulatory surgery center environments have significantly propelled their position as the dominant end-user segment in the North American medical products market, as healthcare facilities invest extensively in advanced medical technologies that enhance clinical capabilities and patient outcomes. The complexity of modern healthcare delivery requires continuous investment in advanced diagnostic imaging systems, surgical robots, minimally invasive instrumentation, and patient monitoring technologies that enable healthcare providers to deliver state-of-the-art care while maintaining competitive advantage in their respective markets. The implementation of value-based care models and quality metrics has increased demand for evidence-based medical products that demonstrate clear clinical utility and cost-effectiveness, supporting broader market adoption and reimbursement coverage. The emphasis on infection control and patient safety has accelerated adoption of single-use medical products, advanced sterilization equipment, and antimicrobial technologies that reduce healthcare-associated infections and improve patient outcomes. Healthcare reform initiatives and insurance coverage expansions have increased patient access to advanced medical procedures and technologies, creating sustained demand for innovative medical products that support improved clinical outcomes and patient satisfaction.

The clinics segment is the fastest-growing end-user in the North American medical products market and is experiencing rapid expansion. This growth of segment is due to the healthcare industry's shift toward outpatient care delivery and the expansion of specialized clinic services that provide immediate medical interventions, preventive care, and chronic disease management requiring access to diagnostic equipment, therapeutic devices, and monitoring supplies. The segment's expansion encompasses diverse practice settings including primary care clinics, specialty practices, urgent care centers, occupational health facilities, and community health centers that provide immediate medical services for acute conditions, preventive care interventions, and ongoing disease management. Market participants are experiencing increased demand for compact, cost-effective medical products that can support immediate care delivery in smaller practice environments with limited storage space and inventory management capabilities. The segment's growth is particularly pronounced in regions experiencing healthcare access challenges and rural communities where clinics serve as primary sources of medical care for local populations. Government initiatives supporting expanded scope of practice for nurse practitioners and physician assistants have created additional market opportunities for medical product manufacturers and distributors serving clinic environments.

The extensive expansion of primary care services and the increasing emphasis on chronic disease management within clinic settings have accelerated the growth of clinics as the fastest-growing end-user segment in the North American medical products market, as these facilities seek to provide comprehensive medical services for ongoing patient care and preventive interventions. The complexity of chronic disease management in clinic settings requires access to monitoring equipment, diagnostic testing supplies, and therapeutic devices that enable ongoing patient assessment and treatment optimization for conditions including diabetes, hypertension, and cardiovascular disease. The implementation of patient-centered medical home models and accountable care organizations has increased demand for point-of-care diagnostic equipment, remote monitoring devices, and evidence-based therapeutic supplies that support comprehensive care delivery and improved patient outcomes. The expansion of telemedicine and remote consultation capabilities has enhanced the safety and effectiveness of medical care delivery in clinic settings, allowing specialists to provide real-time guidance and support to primary care providers managing complex medical conditions. Healthcare reform initiatives and insurance coverage expansions have increased patient access to primary care services, creating sustained demand for medical products that support immediate care delivery and preventive interventions in outpatient environments.

The extensive adoption of point-of-care testing and the development of advanced diagnostic capabilities within clinic environments have significantly accelerated the growth of clinics as the fastest-growing end-user segment in the North American medical products market, as healthcare providers seek to reduce diagnostic turnaround times and improve care effectiveness through immediate test results and rapid clinical decision-making. The complexity of modern primary care medicine requires rapid identification of conditions such as diabetes, cardiovascular disease, infectious diseases, and metabolic disorders, with medical products enabling healthcare providers to initiate appropriate treatments within minutes rather than hours or days. The implementation of telemedicine and remote care services has increased demand for portable diagnostic products that can provide accurate results in field conditions and mobile healthcare settings, supporting expanded access to medical services in underserved communities. Emergency response organizations maintain extensive inventories of rapid diagnostic medical products for disaster response and pandemic preparedness operations. The emphasis on preventive care and wellness screening has accelerated adoption of point-of-care diagnostic products that enable immediate health assessment and patient education during routine clinic visits.

REGIONAL ANALYSIS

United States Medical Products Market Analysis

The United States was the dominant force in the North American medical products market by commanding a 92.5% of the total regional market share. This overwhelming market position is due to the country's extensive healthcare infrastructure, diverse medical device ecosystem, and sophisticated supply chain networks that support immediate access to innovative medical products across diverse geographic and demographic populations. The United States' medical products market is characterized by high technological adoption rates, stringent regulatory compliance requirements, and significant investment in research and development that reflects broader healthcare innovation priorities. The market's maturity is evident in its comprehensive distribution networks, established manufacturing facilities, and robust service infrastructure that supports both large-scale hospital systems and smaller outpatient care facilities. The country's lead position in medical technology innovation and its role as a global hub for medical device development have solidified its position as the largest consumer of advanced medical products in North America.

The United States' position as the largest market participant is fundamentally supported by its extensive healthcare infrastructure and comprehensive medical technology innovation ecosystem that requires vast quantities of diverse medical products to support daily operations and cutting-edge healthcare delivery. The complexity of healthcare delivery in U.S. hospitals requires access to advanced diagnostic equipment, therapeutic devices, and comprehensive inventory systems that can support diverse clinical scenarios from routine procedures to complex surgical interventions requiring specialized instrumentation and monitoring capabilities. The implementation of hospital quality metrics and patient outcome measures has increased demand for advanced monitoring products, evidence-based therapeutic devices, and standardized clinical protocols that support clinical decision-making and treatment effectiveness. The emphasis on value-based care and population health management has accelerated adoption of remote monitoring devices, connected health technologies, and data analytics platforms that enable comprehensive patient management and care coordination across diverse healthcare settings.

The comprehensive regulatory framework and stringent quality assurance requirements governing medical products in the United States have established the country as the dominant market participant, as manufacturers and healthcare facilities invest extensively in compliance activities and quality management systems that ensure product safety and effectiveness. The complexity of validation protocols has increased substantially with the implementation of risk-based classification systems and enhanced post-market surveillance requirements that necessitate extensive documentation and quality assurance procedures for medical products used in critical care environments. The need for third-party certification and regulatory approval can extend product development timelines by several months, creating project delays and cash flow pressures for manufacturers operating in competitive markets. Cross-border trade requirements necessitate compliance with multiple regulatory frameworks, including FDA, state health departments, and local emergency management standards, creating additional complexity for manufacturers serving diverse U.S. markets.

Canada Medical Products Market Analysis

Canada holds a significant position in the North American medical products market. The Canadian market's distinctive characteristics include rigorous healthcare quality standards, universal healthcare coverage requirements, and unique geographic challenges that shape medical product specifications and distribution strategies. Canada's medical products sector demonstrates strong growth potential driven by expanding healthcare infrastructure, aging population demographics, and increasing emphasis on rural healthcare access and technology adoption. The market benefits from proximity to major U.S. manufacturers while maintaining distinct regulatory requirements and healthcare delivery models that influence product development and distribution approaches. Canadian market participants emphasize sustainability, quality assurance, and regulatory compliance in their medical product procurement decisions, reflecting the country's commitment to healthcare equity and responsible resource management.

Canada's significant position in the North American medical products market is largely attributed to its universal healthcare coverage system and comprehensive medical technology access requirements that mandate immediate availability of innovative medical products across diverse geographic regions and population demographics. The geographic diversity of Canadian healthcare delivery, with vast rural and remote regions requiring medical services, has increased demand for portable medical products, telemedicine capabilities, and strategic supply positioning that ensures immediate access to life-saving interventions and routine care delivery. The implementation of wait time benchmarks and quality metrics for healthcare delivery has increased demand for rapid diagnostic products, evidence-based therapeutic agents, and monitoring equipment that support timely and effective patient management. Provincial healthcare systems maintain strategic medical product reserves and mutual aid agreements that require standardized medical supplies capable of supporting mass casualty events and prolonged emergency operations in diverse geographic and climatic conditions.

Canada's robust market position in the medical products sector is significantly strengthened by the unique geographic challenges and remote healthcare delivery requirements that necessitate specialized medical products and distribution strategies to ensure comprehensive healthcare access across vast geographic distances. The Arctic and northern regions of Canada require specialized medical products that can function effectively in extreme cold temperatures and support extended storage periods without refrigeration, necessitating investment in cold-weather compatible equipment and stabilized pharmaceutical formulations. The implementation of telemedicine and remote consultation capabilities has increased demand for portable diagnostic products, wireless communication equipment, and specialized monitoring devices that enable real-time consultation and intervention guidance for remote healthcare providers. Provincial healthcare systems have established air ambulance services and mobile medical response units that require specialized medical products capable of supporting prolonged patient care during transport and field operations in challenging environmental conditions.

COMPETITIVE LANDSCAPE

The North American medical products market exhibits highly competitive dynamics characterized by the presence of established global corporations alongside specialized regional manufacturers and emerging technology-focused companies. Market leaders leverage their extensive distribution networks, brand recognition, and financial resources to maintain dominant positions while continuously innovating to address evolving healthcare requirements. The competitive landscape is marked by strategic acquisitions, partnerships, and product development initiatives that enable companies to expand their product portfolios and geographic reach. Pricing pressures persist as healthcare facilities increasingly demand value-added features and services while maintaining cost-effectiveness. Differentiation strategies focus on technological innovation, quality assurance, and customized solutions that address specific clinical applications and healthcare delivery models. The market's maturity has led to consolidation trends where larger players acquire smaller competitors to strengthen their market positions and eliminate competition. Innovation cycles are accelerating as participants invest in research and development to incorporate advanced materials, digital technologies, and sustainable practices. Customer relationships are becoming increasingly important as switching costs rise and product complexity increases. Service capabilities, technical support, and supply chain reliability have emerged as critical competitive factors alongside product performance and regulatory compliance.

KEY MARKET PLAYERS

The key players in the North America Medical Products Market include

- Medtronic plc

- Johnson & Johnson

- Abbott Laboratories

- GE Healthcare

- Stryker Corporation

- Becton, Dickinson and Company (BD)

- Boston Scientific Corporation

- Siemens Healthineers AG

- Cardinal Health, Inc.

- Baxter International Inc.

- 3M Company

- B. Braun Melsungen AG

- Medline Industries, LP

- McKesson Corporation

- CONMED Corporation

Top Players in the Market

Johnson & Johnson

Johnson & Johnson stands as a global healthcare giant with a dominant presence in the North American medical products market, significantly contributing to the global landscape through its diversified portfolio spanning pharmaceuticals, medical devices, and consumer health products. The company's medical device division offers a comprehensive range of products including surgical instruments, orthopedic implants, cardiovascular devices, and advanced wound care solutions utilized in healthcare facilities worldwide. Their commitment to research and development has resulted in numerous breakthrough innovations that have transformed patient care and clinical outcomes across multiple therapeutic areas. Johnson & Johnson's extensive global manufacturing capabilities and robust supply chain infrastructure enable rapid response to healthcare needs and public health emergencies. The company's focus on quality assurance and regulatory compliance ensures their medical products meet the highest safety and efficacy standards internationally. Their strategic acquisitions and partnerships have expanded their product offerings and strengthened their market presence across diverse geographical regions. Johnson & Johnson's dedication to global health initiatives and healthcare accessibility demonstrates their commitment to advancing medical care and improving patient lives worldwide through innovative medical products and solutions.

Medtronic plc

Medtronic plc maintains a prominent position in the global medical products market through its extensive portfolio of medical technologies and therapeutic solutions designed to alleviate pain, restore health, and extend life for millions of patients worldwide. The company's offerings include advanced medical devices such as pacemakers, insulin pumps, spinal implants, and minimally invasive surgical technologies that are utilized in healthcare settings across the globe. Their commitment to innovation is evident through substantial investments in research and development, focusing on creating intelligent, connected medical devices that enhance clinical outcomes and patient experience. Medtronic's global reach and established distribution networks ensure rapid deployment of critical medical products during healthcare emergencies and routine clinical practice. The company's emphasis on training and education programs supports healthcare providers worldwide in effectively utilizing advanced medical technologies. Their focus on evidence-based medicine and clinical research has established Medtronic as a trusted partner for healthcare systems seeking to improve patient outcomes through innovative medical solutions. Medtronic's integration of digital health solutions with medical devices positions them at the forefront of transforming healthcare delivery through technology.

Stryker Corporation

Stryker Corporation plays a crucial role in the global medical products market, particularly in orthopedics, medical and surgical equipment, and neurotechnology through its specialized medical device offerings. The company's comprehensive product portfolio includes advanced orthopedic implants, surgical navigation systems, endoscopy equipment, and neurovascular devices that are critical in hospitals and surgical centers worldwide. Their innovation in minimally invasive surgical technologies and robotic-assisted surgery platforms enhances surgical precision and patient outcomes globally. Stryker's commitment to developing smart, connected medical devices aligns with the growing need for integrated healthcare solutions that improve clinical decision-making and operational efficiency. The company's global service network and technical support capabilities ensure reliable performance of their medical equipment in diverse healthcare settings internationally. Their focus on education and training programs helps healthcare professionals worldwide effectively utilize advanced medical technologies. Stryker's strategic investments in digital health and artificial intelligence integration position them to lead future advancements in medical device innovation and patient care delivery on a global scale.

Top Strategies Used by Key Market Participants

Technology Integration and Digital Health Solutions Leading manufacturers in the North American medical products market are aggressively pursuing technology integration strategies that transform traditional medical devices into intelligent, connected systems. This approach involves incorporating IoT sensors, cloud connectivity, and advanced analytics capabilities that enable real-time monitoring, predictive maintenance, and enhanced clinical decision-making. Companies are developing proprietary software platforms that provide comprehensive device management solutions, allowing healthcare providers to optimize equipment performance and reduce downtime. The integration of artificial intelligence and machine learning algorithms enhances diagnostic accuracy and treatment effectiveness while adapting to evolving clinical requirements. This strategic focus on digital health transformation not only improves patient care outcomes but also creates new value-added service opportunities through data analytics and remote support offerings. Smart connectivity features enable remote diagnostics and troubleshooting, reducing service response times and improving healthcare facility operational efficiency.

Strategic Partnerships and Collaborative Innovation Market participants are implementing comprehensive partnership strategies that involve collaboration with healthcare systems, research institutions, and technology companies to accelerate innovation and expand market reach. This involves forming strategic alliances that leverage complementary capabilities, share development costs, and access new customer segments through established distribution networks. Companies are investing in joint development initiatives that combine clinical expertise with advanced engineering capabilities to create next-generation medical solutions. The focus extends to partnerships with telemedicine providers, digital health platforms, and healthcare IT companies to develop integrated healthcare ecosystems. Strategic collaborations with academic medical centers facilitate clinical validation and real-world evidence generation that supports regulatory approvals and market adoption. These partnership strategies enable participants to address complex healthcare challenges through multidisciplinary approaches while reducing individual investment risks and accelerating time-to-market for innovative solutions.

Product Portfolio Diversification and Specialization Key players are pursuing comprehensive product portfolio diversification strategies that emphasize specialization in high-growth therapeutic areas and emerging medical technologies to strengthen their market positions and reduce dependency on single product categories. This involves developing comprehensive product lines that address specific clinical needs across multiple medical specialties, from cardiology and orthopedics to neurology and oncology. Companies are investing in research and development to create specialized medical devices that address unmet clinical needs and support personalized medicine approaches. The focus extends to developing companion diagnostic products, combination therapies, and integrated treatment platforms that enhance clinical outcomes and support value-based care models. Strategic acquisitions and licensing agreements enable participants to expand their product portfolios and enter new therapeutic areas without extensive internal development timelines. These diversification strategies not only enhance revenue stability but also support broader healthcare delivery objectives while improving patient access to innovative medical technologies.

RECENT MARKET DEVELOPMENTS

- In March 2024, Johnson & Johnson announced the launch of their new Digital Health Platform featuring integrated patient monitoring systems and AI-powered clinical decision support tools for hospital and home care environments.

- In January 2024, Medtronic completed the acquisition of Cardialen, a medical device company specializing in heart failure treatment technologies, expanding their cardiovascular product portfolio and therapeutic capabilities.

- In February 2024, Stryker Corporation partnered with Microsoft Azure to develop cloud-based data analytics capabilities for their surgical navigation and robotic-assisted surgery systems, enhancing real-time clinical decision-making support.

- In May 2024, Johnson & Johnson established a new manufacturing facility in Texas to serve North American markets while enhancing supply chain resilience and reducing production lead times for critical medical devices.

- In April 2024, Medtronic launched their Connected Care Initiative, offering comprehensive remote monitoring services and predictive maintenance programs to healthcare facilities utilizing their medical devices with integrated IoT capabilities.

MARKET SEGMENTATION

This research report on the North America Medical Products Market is segmented and sub-segmented based on categories.

By Type

- Diagnostic Imaging

- Minimally Invasive Surgical (MIS)

By End-user

- Hospitals & Ambulatory Surgery Centers (ASCs)

- Clinics

By Country

- U.S.

- Canada

- Rest of North America

Frequently Asked Questions

What factors are driving the growth of this market?

Growth is driven by an aging population, rising prevalence of chronic diseases, technological advancements, increased healthcare spending, and demand for minimally invasive procedures.

What are the main challenges faced by North America Medical Products Market?

Regulatory complexities, high costs of advanced devices, cybersecurity threats, and supply chain disruptions are key challenges.

How is the adoption of AI and IoT impacting the market?

AI and IoT are revolutionizing the market by enabling smart diagnostics, remote monitoring, predictive analytics, and improved patient outcomes.

What is the growth outlook for the North America medical products market?

The market is expected to grow steadily at a CAGR of around 5–7% over the next several years, driven by innovation and expanding healthcare infrastructure.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com