- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

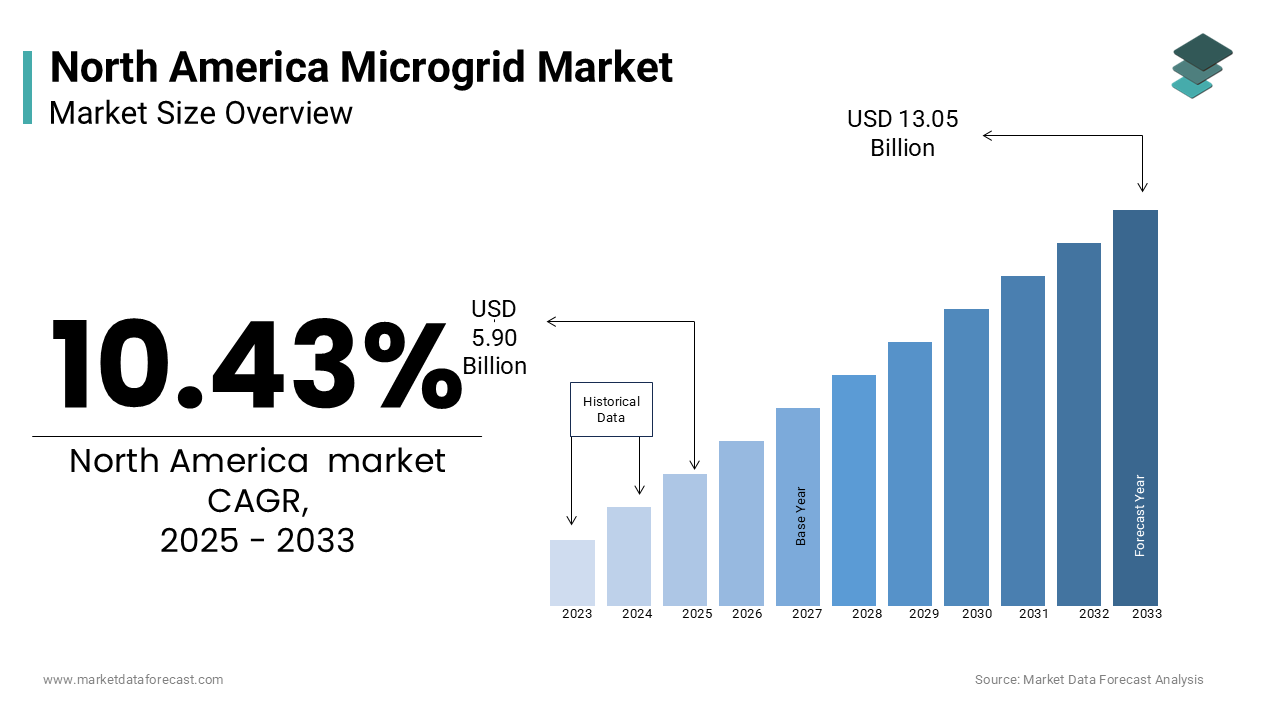

Market Size, 2025

$5.90 BnMarket Estimate, 2026

$6.52 BnMarket Forecast, 2034

$14.42 BnCAGR, 2026–2034

10.43%North America Microgrid Market Report Summary

The North America microgrid market was valued at USD 5.90 billion in 2025, is estimated to reach USD 6.52 billion in 2026, and is projected to reach USD 14.42 billion by 2034, growing at a CAGR of 10.43% during the forecast period from 2026 to 2034. The growth of the North America microgrid market is driven by increasing demand for energy resilience, rising frequency of climate-related power outages, and growing adoption of decentralized energy systems. Integration of renewable energy sources, expansion of battery storage technologies, and strong government support for grid modernization are further fueling market growth. Moreover, rising investments in campus, military, healthcare, and remote community microgrids are strengthening the adoption of localized energy solutions across the region.

Key Market Trends

- Rising adoption of microgrids for energy resilience and uninterrupted power supply in critical infrastructure.

- Growing integration of renewable energy sources such as solar and wind with battery storage systems.

- Increasing deployment of microgrids in military bases, healthcare facilities, and university campuses.

- Strong focus on decarbonization and net-zero targets supported by federal and state-level incentives.

- Expanding use of microgrids in remote and off-grid communities to reduce diesel dependency.

Segmental Insights

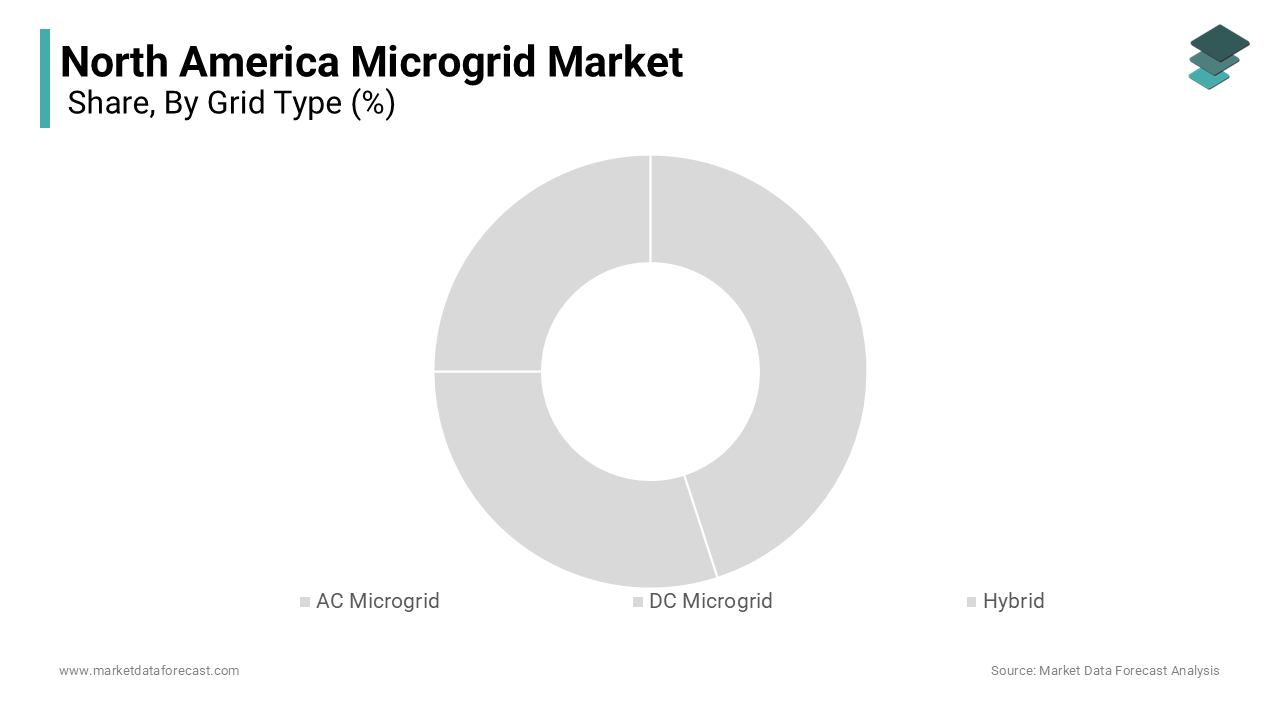

- Based on grid type, the AC microgrid segment was the largest and held a significant share of the North America microgrid market in 2024. The segment’s dominance is attributed to its compatibility with existing power infrastructure, mature technology base, and widespread adoption across commercial and institutional facilities.

- Based on connectivity, the grid-connected microgrid segment accounted for the largest share of the North America microgrid market in 2024. The dominance of this segment stems from its ability to operate in coordination with the main grid while providing islanding capability during outages.

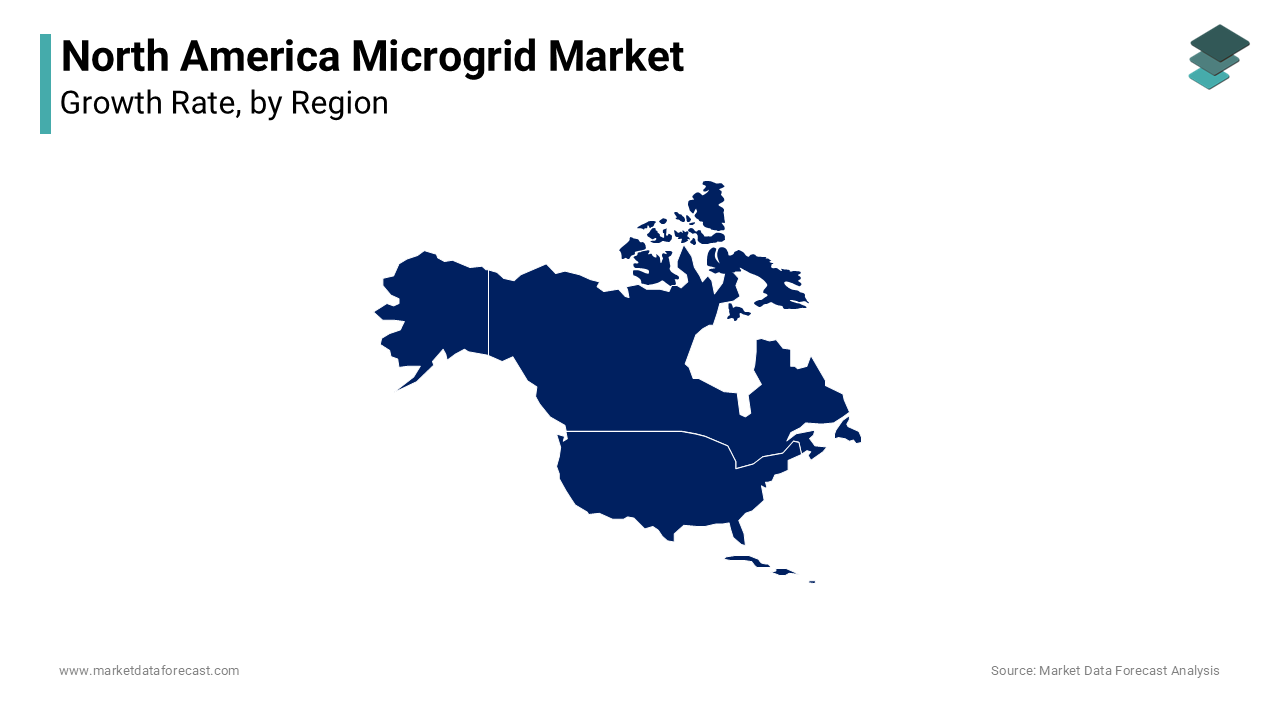

Regional Insights

The North America microgrid market is witnessing strong growth across major economies, supported by grid modernization initiatives, renewable energy integration, and rising resilience requirements.

- The United States was the largest contributor to the North America microgrid market in 2024, driven by extensive deployment across military installations, hospitals, data centers, and university campuses, along with strong federal funding under infrastructure and clean energy programs.

- Canada continues to perform well, supported by increasing deployment of renewable-powered microgrids in remote and Indigenous communities to reduce reliance on diesel generation.

Competitive Landscape

The North America microgrid market is characterized by the presence of global energy and automation companies with strong technological capabilities and integrated solution offerings. Leading players are focusing on advanced energy management software, renewable integration, storage technologies, and turnkey microgrid solutions. Strategic partnerships with utilities, governments, and commercial customers are strengthening market positioning. Prominent players in the North America microgrid market include Schneider Electric, Siemens AG, General Electric, Eaton Corporation, Hitachi Energy, Honeywell International, NRG Energy, Exelon Corporation, S&C Electric Company, and ENGIE.

North America Microgrid Market Size

The North America microgrid market was worth USD 5.90 billion in 2025. The North American market is estimated to grow at a CAGR of 10.43% from 2026 to 2034 and be valued at USD 14.42 billion by the end of 2034 from USD 6.52 billion in 2026.

The North America microgrid market refers to the deployment and operation of localized, decentralized energy systems that can function independently or in conjunction with the main power grid. These microgrids integrate distributed energy resources such as solar, wind, battery storage, and diesel generators to provide reliable, resilient, and often cleaner electricity for communities, campuses, industrial facilities, and remote locations. The increasing need for energy security, resilience against climate-related outages, and decarbonization efforts has driven widespread interest in microgrid solutions across the region. These systems are increasingly being adopted by military bases, universities, healthcare facilities, and data centers seeking an uninterrupted power supply and reduced reliance on centralized grids vulnerable to extreme weather events. In Canada, Natural Resources Canada reports growing investment in off-grid and islanded microgrids particularly in northern and Indigenous communities—that rely on renewable integration to reduce dependence on imported diesel fuel. In addition, the rise of corporate sustainability commitments and the push for net-zero buildings have further reinforced the relevance of microgrids in both urban and rural settings.

MARKET DRIVERS

Increasing Demand for Energy Resilience and Grid Independence

One of the primary drivers fueling the North America microgrid market is the rising demand for energy resilience and independence from the central power grid, particularly in the face of increasing climate-induced disruptions. Severe weather events, including hurricanes, wildfires, and winter storms, have exposed vulnerabilities in traditional utility networks, prompting critical institutions such as hospitals, military bases, and data centers to seek self-sufficient energy solutions. According to the National Oceanic and Atmospheric Administration (NOAA), the U.S. experienced 28 climate-related disasters exceeding $1 billion each in economic damages in 2023 alone, underscoring the urgency for more robust energy infrastructure. Microgrids offer a compelling solution by enabling continuous power supply during grid outages through localized generation and energy storage. For example, the U.S. Department of Defense has deployed microgrids at several military installations, including Fort Bragg and Naval Base San Diego, ensuring operational continuity during emergencies. As per a report by the Rocky Mountain Institute, over 60% of surveyed commercial and institutional energy managers indicated plans to invest in microgrids within the next five years to mitigate outage risks and ensure mission-critical operations. Moreover, the growing emphasis on cybersecurity threats to national power infrastructure has further intensified interest in microgrid adoption. With the ability to disconnect from the main grid during cyberattacks or physical disruptions, microgrids enhance not only reliability but also energy sovereignty.

Integration of Renewable Energy and Decarbonization Goals

Another key driver behind the growth of the North America microgrid market is the increasing integration of renewable energy sources and alignment with regional and national decarbonization targets. Governments and private enterprises alike are prioritizing clean energy transitions, and microgrids serve as an essential enabler by allowing localized control over energy generation, consumption, and storage. According to the U.S. Environmental Protection Agency (EPA), the electricity sector accounts for nearly 25% of total greenhouse gas emissions in the United States, making it a focal point for emissions reduction strategies. Microgrids facilitate the seamless incorporation of intermittent renewables like solar and wind by pairing them with battery storage and advanced energy management systems. States like California and New York have mandated aggressive reductions in carbon emissions, pushing municipalities and utilities to adopt microgrids as part of broader climate action plans. Also, corporations committed to achieving net-zero emissions, such as Microsoft and Google, are investing in microgrid-enabled campuses and data centers to meet their environmental goals.

MARKET RESTRAINTS

High Initial Investment and Complex Financing Structures

A significant restraint affecting the North America microgrid market is the high initial capital expenditure required for system design, installation, and integration with existing energy infrastructure. Microgrids involve complex engineering, advanced control systems, and multiple distributed energy resources, which collectively increase upfront costs compared to conventional power sourcing models. Financing these projects poses an additional challenge, as traditional utility models and regulatory frameworks do not always accommodate decentralized energy investments. Many potential adopters especially small municipalities, tribal communities, and rural hospitals lack access to flexible funding mechanisms or creditworthy backing needed to secure financing. While federal programs such as the Bipartisan Infrastructure Law (BIL) and state-level incentives aim to offset some of these costs, navigating eligibility criteria and grant application processes can be time-consuming and resource-intensive.

Regulatory and Policy Uncertainty Across Jurisdictions

Another key challenge restraining the North America microgrid market is the inconsistency in regulatory frameworks and interconnection standards across different states and provinces. Unlike centralized utilities, microgrids operate at the intersection of energy generation, distribution, and retail services, leading to jurisdictional ambiguity that complicates permitting, pricing, and revenue models. Like, over half of U.S. states lack clear regulatory guidelines for microgrid ownership and operation, creating legal uncertainty for developers and investors. In many jurisdictions, outdated utility regulations treat microgrids as independent power producers rather than integrated energy assets, limiting their ability to sell excess power back to the grid or participate in wholesale markets. As reported by the Regulatory Assistance Project (RAP), only 15 U.S. states had established formal microgrid tariff structures by early 2024, impeding the scalability of commercial and community-based microgrid projects. In Canada, similar challenges exist, particularly regarding interprovincial differences in energy governance and compensation mechanisms for distributed generation. Natural Resources Canada highlights that interoperability standards for microgrids vary significantly across provinces, making it difficult to replicate successful models in different regions.

MARKET OPPORTUNITIES

Expansion of Microgrids in Remote and Off-Grid Communities

One of the most promising opportunities for the North America microgrid market lies in the growing deployment of microgrids in remote and off-grid communities that traditionally rely on expensive and polluting diesel generators. In both the United States and Canada, isolated settlements, Indigenous communities, and mining operations often face unreliable power supply and high fuel transportation costs, making microgrids an attractive alternative for achieving energy independence while reducing environmental impact. According to Natural Resources Canada, over 200 remote communities in Canada depend almost entirely on diesel for electricity generation, resulting in high operating costs and significant carbon emissions. To address this, provincial governments and Indigenous councils have launched initiatives to transition toward renewable-powered microgrids using solar, wind, and battery storage. For instance, Ontario’s Independent Electricity System Operator (IESO) has funded pilot microgrid projects in several First Nations communities to improve energy affordability and sustainability. Similarly, in the U.S., the Department of Energy's Office of Indian Energy has supported the implementation of solar-diesel hybrid microgrids in Native American reservations across Alaska and the Southwest.

Growth of Campus and Institutional Microgrids

Another significant opportunity for the North America microgrid market is the increasing adoption of microgrids by educational institutions, healthcare campuses, and research facilities seeking energy autonomy, cost efficiency, and sustainability. Universities, hospitals, and large corporate campuses represent ideal candidates for microgrid deployment due to their dense energy demands, commitment to climate goals, and the need for an uninterrupted power supply. A key factor driving this trend is the ability of microgrids to provide continuous power during grid failures, ensuring critical operations in medical facilities and university research labs. Also, campus microgrids enable institutions to optimize energy use through combined heat and power (CHP) systems, solar arrays, and battery storage, thereby reducing operational expenses and carbon footprints.

MARKET CHALLENGES

Technical Complexity and Interoperability Issues

A major challenge confronting the North America microgrid market is the technical complexity involved in designing, integrating, and managing microgrid systems that incorporate diverse energy sources, control platforms, and grid interaction protocols. Unlike conventional power systems, microgrids require sophisticated energy management software, real-time monitoring, and adaptive control mechanisms to maintain stability, optimize dispatch, and ensure safe islanding from the main grid. According to the National Renewable Energy Laboratory (NREL), nearly 40% of microgrid deployment delays in 2023 were attributed to interoperability issues among hardware and software components from different vendors. This complexity extends to system sizing, redundancy planning, and frequency regulation, all of which must be carefully engineered to match site-specific load profiles and generation capabilities. As reported by the Electric Power Research Institute (EPRI), many microgrid operators face difficulties in synchronizing battery storage, solar inverters, and backup generators without causing instability or inefficiencies, particularly during dynamic grid transitions. Furthermore, the absence of standardized communication protocols and equipment compatibility benchmarks creates barriers for scalable deployment. Utilities, regulators, and system integrators are still working to establish uniform technical standards that simplify microgrid implementation and maintenance.

Utility Opposition and Grid Integration Barriers

Another critical challenge facing the North America microgrid market is resistance from traditional utility providers and the complexities of integrating microgrids into the existing electrical grid. Many investor-owned and municipal utilities perceive microgrids as disruptive to their business models, particularly when customers generate and manage their own power, potentially reducing utility revenue streams. According to the Edison Electric Institute, several utility companies have lobbied against net metering reforms and third-party microgrid ownership models, citing concerns over grid stability and cost recovery. From a technical standpoint, integrating microgrids with the main grid involves intricate synchronization and bidirectional power flow management, which requires updated infrastructure and advanced protection systems. Moreover, disputes over rate structures, standby charges, and grid service fees create financial disincentives for microgrid development. A 2023 report by the Regulatory Assistance Project (RAP) noted that unpredictable utility tariffs and unclear compensation mechanisms deterred over one-third of planned microgrid projects in North America from moving forward.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.43% |

| Segments Covered | By Grid Type, Connectivity, Power Source, Storage Device, Application and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | The United States, Canada and Rest of North America |

| Market Leaders Profiled | Schneider Electric, Siemens AG, General Electric (GE), Eaton Corporation, Hitachi Energy, Honeywell International, NRG Energy, Exelon Corporation, S&C Electric Company, and ENGIE |

SEGMENTAL ANALYSIS

By Grid Type Insights

The AC microgrid segment dominated the North America microgrid market by accounting for a 64.3% of total installed capacity in 2025. This leading position is attributed to the compatibility of AC microgrids with existing power infrastructure, which is predominantly designed for alternating current transmission and distribution. One of the key factors behind this dominance is the widespread integration of AC microgrids into utility-scale and institutional energy systems, including hospitals, military bases, and university campuses. These facilities often operate within the conventional grid framework and require seamless synchronization with the main grid during normal operations or islanded mode during outages. Another major contributor to the segment's growth is the availability of mature technology and established supply chains for AC-based generation and control equipment, making it easier for developers to deploy reliable and scalable microgrid solutions.

The hybrid microgrid segment is emerging as the fastest-growing category within the North America microgrid market, projected to expand at a CAGR of 13.2%. Unlike traditional AC or DC-only microgrids, hybrid systems combine both technologies to maximize efficiency, flexibility, and compatibility with diverse distributed energy resources. A primary driver behind this rapid growth is the increasing deployment of hybrid microgrids in remote communities and off-grid industrial sites, where they enable optimal utilization of solar, wind, battery storage, and diesel generators. These systems allow for direct coupling of DC sources like solar panels and batteries without conversion losses, while still supporting AC-powered appliances and motors. As per Natural Resources Canada, over 40% of new microgrid projects in northern Indigenous communities adopted hybrid architectures between 2022 and 2024, enhancing reliability and reducing fuel dependency. Additionally, the rising interest in high-efficiency data centers, mining operations, and campus energy systems has further fueled demand for hybrid microgrids that can dynamically manage multiple load types and energy inputs.

By Connectivity Insights

The grid-connected microgrid segment had the largest share of the North America microgrid market in 2025. This is driven by the growing need for resilient, flexible power solutions that can operate seamlessly with the central grid while maintaining the ability to disconnect and function autonomously during outages. One of the primary drivers of this segment’s dominance is the integration of microgrids into urban and suburban infrastructure, particularly in densely populated areas where grid reliability is increasingly challenged by climate events and aging infrastructure. Cities such as New York, Boston, and San Francisco have launched microgrid initiatives aimed at improving grid stability, enabling participation in demand response programs, and supporting local renewable energy integration. Another major factor supporting market growth is the ability of grid-connected microgrids to generate revenue through utility markets, including peak shaving, load shifting, and ancillary services.

The off-grid microgrid segment is experiencing the fastest growth rate in the North America microgrid market, projected to grow at a CAGR of 14.1%. While historically smaller in scale, this segment is gaining traction due to rising investments in remote electrification, rural development, and decarbonization efforts in isolated locations. A key driver behind this expansion is the increasing deployment of off-grid microgrids in remote and underserved regions, particularly in Alaska, northern Canada, and tribal lands where access to the centralized grid is either impractical or prohibitively expensive. Another contributing factor is the growing adoption of off-grid microgrids in the mining, oil & gas, and agricultural sectors, where energy independence and cost predictability are essential

By Power Source Insights

The natural gas segment commanded the North America microgrid market by accounting for 32.5% of total power source installations in 2024. This is primarily attributed to the widespread use of natural gas-fueled combined heat and power (CHP) systems in institutional, industrial, and commercial microgrids, where continuous operation and thermal integration are crucial. One of the key factors behind this dominance is the high efficiency and reliability of natural gas-fired generators, which provide stable baseload power while also delivering waste heat recovery for heating, ventilation, and air conditioning (HVAC) applications. According to the U.S. Environmental Protection Agency (EPA), CHP systems powered by natural gas achieve overall efficiencies exceeding 80% significantly higher than conventional grid-supplied electricity. Many hospitals, data centers, and manufacturing plants leverage these benefits to ensure uninterrupted power and reduce operational costs. Another major contributor to the segment's growth is the availability of extensive natural gas pipeline infrastructure in the U.S. and Canada, ensuring secure and relatively low-cost fuel supply compared to diesel.

The solar PV segment is experiencing the highest development rate in the North America microgrid market, projected to expand at a CAGR of 15.4%. This rapid expansion is largely driven by falling photovoltaic module prices, favorable policy incentives, and increasing corporate and governmental commitments to clean energy targets. A primary driver behind this surge is the declining cost of solar panels and balance-of-system components, making solar PV an accessible and economically viable option for microgrid developers. Additionally, state-level incentives such as net metering, tax credits, and feed-in tariffs have accelerated solar adoption across educational institutions and public facilities. Another key factor fueling this segment’s momentum is the growing emphasis on sustainability and zero-emission energy generation, particularly among corporations aiming to meet environmental, social, and governance (ESG) goals.

By Storage Device Insights

The lithium-ion (Li-ion) batteries segment dominated the market by having for 65.1% portion of the North America microgrid market's energy storage segment. Their dominance is due to high energy density, longer lifespan, and declining costs. According to the U.S. Department of Energy (DOE), Li-ion battery costs have dropped by over 85% since 2010, making them the preferred choice for microgrid storage. Apart from this, the National Renewable Energy Laboratory (NREL) reported that more than 70% of new microgrid projects in the U.S. included Li-ion storage due to its superior efficiency, rapid charge cycles, and scalability.

Flow batteries segment is forecasted to grow at a CAGR of 16.9% from 2025 to 2033. These batteries are gaining traction because of longer cycle life, deep discharge capability, and scalability, which are essential for large-scale microgrids. The U.S. Department of Energy found that flow batteries offer over 10,000 charge cycles is significantly outperforming Li-ion in longevity. The National Renewable Energy Laboratory (NREL) emphasized that flow battery projects in microgrids increased by 30% in 2024, particularly in remote and utility-scale applications. Besides these, the California Energy Commission is funding flow battery storage projects to enhance grid stability and energy resilience, further accelerating adoption.

By Application Insights

The natural gas segment commanded the North America microgrid market by accounting for 32.5% of total power source installations in 2025. This is primarily attributed to the widespread use of natural gas-fueled combined heat and power (CHP) systems in institutional, industrial, and commercial microgrids, where continuous operation and thermal integration are crucial. One of the key factors behind this dominance is the high efficiency and reliability of natural gas-fired generators, which provide stable baseload power while also delivering waste heat recovery for heating, ventilation, and air conditioning (HVAC) applications. According to the U.S. Environmental Protection Agency (EPA), CHP systems powered by natural gas achieve overall efficiencies exceeding 80% significantly higher than conventional grid-supplied electricity. Many hospitals, data centers, and manufacturing plants leverage these benefits to ensure uninterrupted power and reduce operational costs. Another major contributor to the segment's growth is the availability of extensive natural gas pipeline infrastructure in the U.S. and Canada, ensuring secure and relatively low-cost fuel supply compared to diesel.

The solar PV segment is experiencing the highest development rate in the North America microgrid market, projected to expand at a CAGR of 15.4%. This rapid expansion is largely driven by falling photovoltaic module prices, favorable policy incentives, and increasing corporate and governmental commitments to clean energy targets. A primary driver behind this surge is the declining cost of solar panels and balance-of-system components, making solar PV an accessible and economically viable option for microgrid developers. Additionally, state-level incentives such as net metering, tax credits, and feed-in tariffs have accelerated solar adoption across educational institutions and public facilities. Another key factor fueling this segment’s momentum is the growing emphasis on sustainability and zero-emission energy generation, particularly among corporations aiming to meet environmental, social, and governance (ESG) goals.

REGIONAL ANALYSIS

United States spearheaded the North America microgrid market by capturing a 74.4% of the regional market share in 2024. As a global leader in energy innovation and digital grid technologies, the U.S. has been at the forefront of microgrid deployment across military installations, academic campuses, healthcare facilities, and urban resilience initiatives. One of the primary drivers of the U.S. market is the strong federal and state-level policy support for decentralized energy systems, particularly under the Bipartisan Infrastructure Law (BIL) and Inflation Reduction Act (IRA). These policies have allocated billions of dollars toward grid modernization, clean energy transitions, and community resiliency projects. Another key factor supporting market growth is the rapid adoption of microgrids by critical infrastructure sectors, including defense, healthcare, and research institutions. The U.S. military alone operates a major number of microgrid systems across various bases, ensuring energy security and mission continuity. As per the National Rural Electric Cooperative Association (NRECA), rural utilities and electric cooperatives have also embraced microgrids to improve service reliability in vulnerable regions .

Canada plays a vital role in advancing microgrid adoption, particularly in remote and Indigenous communities that face significant energy access challenges. A major driver behind Canada’s market position is the government-backed push toward replacing diesel-based power generation in off-grid settlements with renewable-integrated microgrids. Programs such as the Smart Renewables and Efficient Energy Use (SREEU) initiative have supported numerous microgrid projects aimed at reducing emissions and lowering long-term energy costs. Another contributing factor is the expansion of microgrids in the mining and resource extraction sectors, particularly in provinces like Ontario, Quebec, and British Columbia.

Mexico is reflecting a nascent but gradually developing presence in the regional decentralized energy ecosystem. While still in the early stages of adoption compared to the U.S. and Canada, Mexico is beginning to explore opportunities in microgrid deployment, particularly in industrial zones and rural electrification projects. One of the primary drivers influencing Mexico’s market trajectory is the increased focus on energy sovereignty and diversification away from centralized fossil fuel reliance, especially following recent reforms in the national electricity sector. Another contributing factor is the emerging trend of microgrid adoption in the mining and manufacturing sectors, particularly in states like Coahuila, Sonora, and Chihuahua, where energy-intensive operations seek cost-effective and resilient power solutions.

COMPETITIVE LANDSCAPE

The North America microgrid market is highly competitive, characterized by a mix of global energy conglomerates, specialized microgrid developers, and emerging clean-tech startups. Established players like Siemens Energy, General Electric, and Schneider Electric dominate due to their extensive R&D capabilities, mature supply chains, and deep relationships with utilities and institutional clients. However, niche firms such as Enchanted Rock, Scale Microgrids, and PowerSecure are gaining traction by offering agile, customer-centric solutions tailored for specific use cases.

Competition is intensifying as companies differentiate not only through technological innovation but also through business models, financing structures, and deployment speed. While large corporations leverage scale and global experience, smaller firms capitalize on local knowledge and rapid implementation cycles. Additionally, the convergence of IT and energy infrastructure has brought in new entrants from the software and data analytics domains, further diversifying the competitive landscape.

Regulatory dynamics, funding availability, and regional policy incentives also shape competitive positioning, creating opportunities for both national expansion and cross-border collaboration. As demand for resilient, clean, and decentralized power grows, competition is shifting toward total value delivery ranging from system performance and lifecycle cost to sustainability impact and cybersecurity readiness making differentiation increasingly nuanced yet essential.

KEY MARKET PLAYERS

Some of the key market players in the North America microgrid market include

- Schneider Electric

- Siemens AG

- General Electric (GE)

- Eaton Corporation

- Hitachi Energy

- Honeywell International

- NRG Energy

- Exelon Corporation

- S&C Electric Company

- ENGIE

Top Players in the North America Microgrid Market

Siemens Energy plays a pivotal role in the North America microgrid market by offering end-to-end solutions that integrate advanced digitalization, automation, and energy management technologies. The company specializes in scalable microgrid systems tailored for industrial complexes, campuses, and utility-scale applications. Siemens’ expertise lies in combining grid resilience with renewable integration, making it a preferred partner for large-scale decentralized energy projects across the U.S. and Canada.

General Electric (GE) contributes significantly to the North America microgrid landscape through its robust portfolio of power generation, grid control, and digital grid analytics tools. GE’s microgrid offerings are built on decades of experience in power system engineering, enabling seamless integration of distributed energy resources. Its focus on hybrid systems—combining renewables, storage, and gas turbines—has positioned it as a key player in both urban and remote microgrid deployments.

Schneider Electric is a global leader in energy management and automation, with a strong presence in North America's microgrid sector. The company delivers intelligent microgrid platforms that emphasize sustainability, efficiency, and cybersecurity. Schneider supports a wide range of clients from military bases to commercial buildings—with integrated software and hardware solutions that enable real-time monitoring, optimization, and islanding capabilities, reinforcing its leadership in smart decentralized energy systems.

Top strategies used by the key market participants

One of the primary strategies employed by leading microgrid companies is strategic partnerships and joint ventures, where firms collaborate with utilities, government agencies, and technology providers to co-develop customized microgrid solutions. These alliances help accelerate project execution, enhance technical capabilities, and expand market reach across diverse sectors including defense, healthcare, and rural electrification.

Another crucial approach is technology innovation and digital integration, focusing on advanced control systems, AI-driven energy management, and predictive maintenance platforms. By embedding smart grid technologies into microgrid operations, key players improve system reliability, optimize energy dispatch, and enhance user engagement, making microgrids more adaptive and economically viable for end-users.

The third major strategy involves expanding service portfolios and localized deployment models, allowing companies to offer turnkey microgrid solutions from design to operation. This includes financing support, long-term maintenance contracts, and performance-based agreements that reduce customer risk and encourage broader adoption. Through these initiatives, top players strengthen their foothold and drive deeper penetration of microgrid technologies across North America.

RECENT MARKET DEVELOPMENTS

- In January 2024, Siemens Energy announced a strategic partnership with a U.S.-based battery storage provider to co-develop integrated microgrid systems optimized for commercial campuses and municipal applications, enhancing scalability and operational efficiency.

- In March 2024, General Electric launched an expanded suite of digital microgrid controllers designed to improve real-time load balancing, frequency regulation, and remote monitoring, particularly for off-grid and hybrid installations in remote regions.

- In June 2024, Schneider Electric inaugurated a dedicated microgrid innovation hub in Toronto, aimed at accelerating pilot deployments and testing next-generation microgrid configurations for Indigenous communities and northern industries.

- In September 2024, a leading U.S. microgrid developer secured exclusive rights to deploy a proprietary hydrogen-fueled generator within North American microgrid projects, signaling a strategic shift toward low-carbon baseload solutions.

- In November 2024, a Canadian cleantech firm acquired a U.S.-based microgrid software platform specializing in AI-enabled energy forecasting and dispatch optimization, strengthening its position in the intelligent microgrid space.

MARKET SEGMENTATION

This research report on the North America microgrid market is segmented and sub-segmented based on categories.

By Grid Type

- AC Microgrid

- DC Microgrid

- Hybrid

By Connectivity

- Grid Connected

- Off Grid

By Power Source

- Diesel Generators

- Natural Gas

- Solar PV

- CHP

- Others

By Storage Device

- Lithium-ion

- Lead Acid

- Flow Battery

- Flywheels

- Others

By Application

- Healthcare

- Educational Institutes

- Military

- Utility

- Industrial/ Commercial

- Remote

- Others

By Country

- The United States

- Canada

- Rest of North America