- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

North America Nerve Repair and Regeneration Market Summary

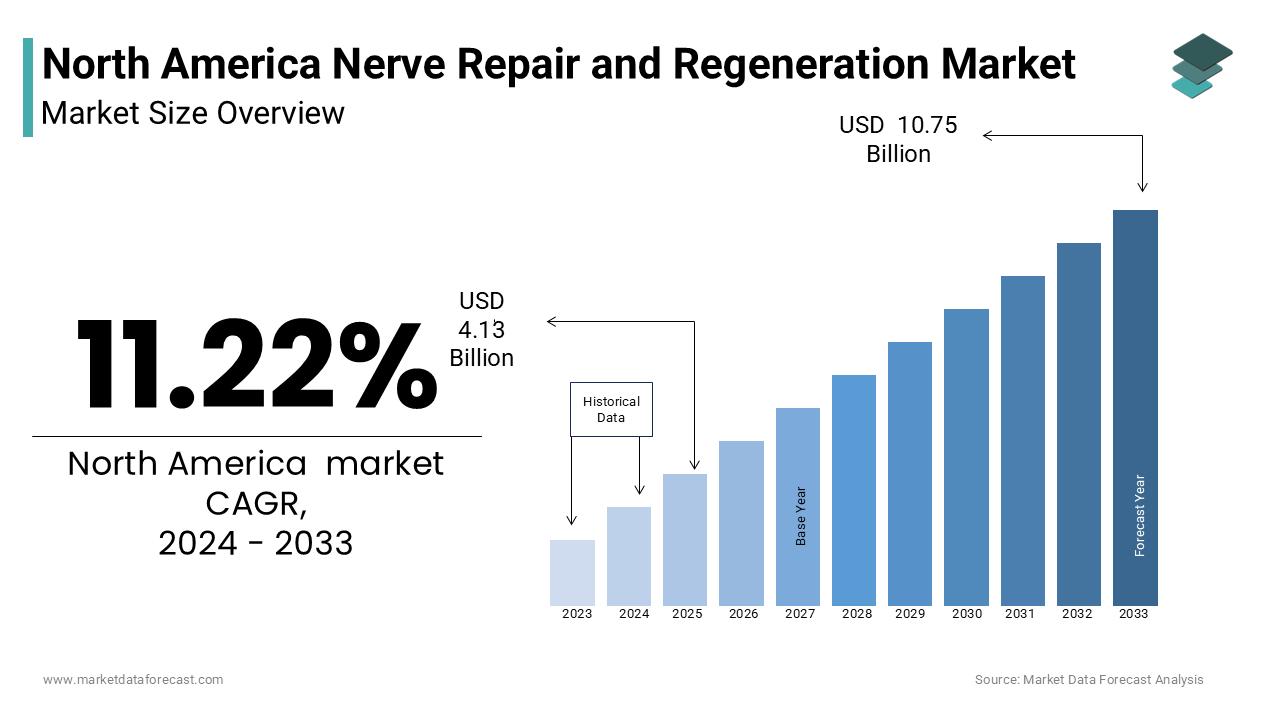

The North America nerve repair and regeneration market was valued at USD 4.59 billion in 2025 and is projected to reach USD 11.96 billion by 2034, growing at a CAGR of 11.22% from 2026 to 2034. Market growth is driven by the rising incidence of nerve injuries, diabetic neuropathy, aging population, and technological advancements in stem cell therapy, neurostimulation devices, and regenerative medicine. The U.S. remains the dominant contributor, with strong R&D support and early adoption of innovative therapies.

Key Market Trends & Insights

- United States dominated the regional market with an 84.6% share in 2025.

- Nerve grafting held the largest surgery share at 32.2% in 2025.

- Biomaterials led the product category with a 38.6% share in 2025.

- Stem cell therapy is the fastest-growing segment, projected at a CAGR of 18.7%.

- Neuromodulation devices are expected to grow at a CAGR of 16.2% through 2034.

Market Size & Forecast

- 2025 Market Size: USD 4.59 Billion

- 2034 Projected Market Size: USD 11.96 Billion

- CAGR (2026–2034): 11.22%

- United States: Largest market in 2025

- Canada: Rapidly expanding with biomedical innovation and an aging population

North America Nerve Repair and Regeneration Market Size

The North America nerve repair and regeneration market size was valued at USD 4.59 billion in 2025 and is anticipated to reach USD 5.11 billion in 2026 from USD 11.96 billion by 2034, growing at a CAGR of 11.22% during the forecast period from 2026 to 2034.

The nerve repair and regeneration includes surgical sutures, nerve conduits, growth factor therapies, stem cell applications, and implantable neurostimulation devices. The market has gained significant traction due to rising incidences of traumatic nerve injuries, increasing prevalence of chronic diseases such as diabetes that lead to peripheral neuropathy, and growing advancements in regenerative medicine. In recent years, the United States has emerged as a global leader in innovation within this sector, driven by robust R&D investments from pharmaceutical and biotech firms. As per the American Association of Neurological Surgeons, over 1.5 million new cases of peripheral nerve injuries are reported annually in the U.S., contributing significantly to the demand for advanced nerve repair solutions. Additionally, the aging population across North America is amplifying the need for effective treatment options, as older adults are more susceptible to nerve damage due to degenerative conditions. Technological breakthroughs, such as bioengineered nerve grafts and 3D-printed scaffolds, have also catalyzed market expansion. These developments align with the broader healthcare focus on minimizing recovery times and improving patient outcomes. Government funding and regulatory support from agencies like the FDA further encourage innovation in this space, which is reinforcing North America's position as a dominant region in the global nerve repair and regeneration landscape.

MARKET DRIVERS

Rising Incidence of Peripheral Nerve Injuries

One of the primary drivers of the North America nerve repair and regeneration market is the escalating incidence of peripheral nerve injuries (PNIs). According to the National Institutes of Health, approximately 2% of all trauma cases involve some form of nerve damage, with over 200,000 surgical procedures performed annually in the U.S. alone to treat these injuries. PNIs can result from accidents, sports-related trauma, or surgical complications, and often require complex interventions ranging from autografts to bioengineered nerve conduits. The rise in vehicular accidents and workplace injuries further exacerbates this trend. As per data from the National Highway Traffic Safety Administration, motor vehicle crashes accounted for over 38,000 fatalities and millions of non-fatal injuries in 2021, many of which involved nerve trauma. Additionally, the Bureau of Labor Statistics recorded over 2.7 million non-fatal workplace injuries in the same year, a significant portion involving musculoskeletal and nerve damage.

Increasing Prevalence of Chronic Diseases Leading to Neuropathy

A major contributing factor to the growth of the North America nerve repair and regeneration market is the rising prevalence of chronic diseases that cause nerve damage, particularly diabetes. As per the Centers for Disease Control and Prevention, over 37 million Americans suffer from diabetes, with nearly half experiencing some degree of diabetic neuropathy. This condition leads to progressive nerve deterioration, which is primarily affecting the extremities and increasing the risk of ulcers, infections, and even amputation. Additionally, autoimmune disorders such as Guillain-Barré syndrome and multiple sclerosis contribute to the burden of nerve damage. According to the National Multiple Sclerosis Society, approximately 1 million people in the U.S. live with MS, a disease known to impact the central nervous system through demyelination and nerve degradation. This growing patient pool necessitates advanced treatment modalities beyond traditional pain management. Regenerative therapies, including stem cell therapy, neurotrophic factors, and neuromodulation devices, are gaining traction as viable long-term solutions. The launch of novel products, such as electroconductive nerve guidance conduits and implantable stimulators, reflects the industry’s response to this unmet clinical need. As awareness and healthcare spending increase, so does the potential for market expansion in this critical segment.

MARKET RESTRAINTS

High Cost of Advanced Nerve Repair Therapies

One of the key restraints impeding the growth of the North America nerve repair and regeneration market is the high cost associated with advanced therapeutic interventions. Cutting-edge treatments such as bioengineered nerve grafts, stem cell therapies, and implantable neurostimulation devices often come with steep price tags that limit widespread adoption. For instance, according to a 2022 report by Becker’s Spine Review, the average cost of a single-use nerve allograft can exceed $10,000, while implantable neurostimulation systems may cost upwards of $30,000 per unit before surgery and hospital fees. These costs pose a significant barrier, especially for patients without comprehensive insurance coverage. While private insurers increasingly cover nerve repair procedures, out-of-pocket expenses remain substantial. Medicaid beneficiaries face even greater limitations, as state-level reimbursement policies vary widely. A 2021 study published in JAMA Surgery found that nearly 22% of patients undergoing nerve repair surgeries faced financial hardship due to uncovered costs. Moreover, hospitals and ambulatory surgical centers must weigh the economic viability of investing in expensive regenerative technologies, which may not always be justified by procedural volume.

Regulatory Hurdles and Lengthy Approval Processes

Another significant restraint impacting the North America nerve repair and regeneration market is the complex and time-consuming regulatory approval process for novel therapies and devices. The U.S. Food and Drug Administration (FDA) maintains stringent evaluation protocols to ensure the safety and efficacy of emerging treatments, particularly those involving biologics, stem cells, or implantable devices. As per the FDA’s Center for Biologics Evaluation and Research, the average time required for approval of regenerative medicine therapies exceeds five years, with preclinical and clinical trial phases accounting for the majority of this duration. As per a 2022 white paper issued by the Advanced Regenerative Manufacturing Institute (ARMI), this ambiguity hampers innovation and slows the introduction of transformative nerve repair solutions into the market, which is ultimately limiting patient access and market growth.

MARKET OPPORTUNITIES

Advancements in Stem Cell and Gene Therapy Technologies

A significant opportunity driving the North America nerve repair and regeneration market lies in the rapid advancements in stem cell and gene therapy technologies. These cutting-edge modalities offer the potential to regenerate damaged nerves at the molecular level, rather than merely managing symptoms. According to the National Institutes of Health, over 400 active clinical trials were registered in 2023 focusing on stem cell-based interventions for neurological disorders, including spinal cord injury, peripheral neuropathy, and stroke-induced nerve damage. Institutions such as the Mayo Clinic and the University of California, San Diego, have been conducting pioneering research in this domain. Notably, a 2023 trial demonstrated that mesenchymal stem cell injections improved sensory and motor function in patients with chronic sciatic nerve injuries. Moreover, CRISPR-based gene editing techniques are being explored to enhance nerve regeneration by modifying genetic pathways responsible for scar formation and axonal growth inhibition. Companies like Editas Medicine and BlueRock Therapeutics are actively developing next-generation gene-editing tools tailored for neural repair.

Integration of AI and Robotics in Nerve Reconstruction Surgery

The integration of artificial intelligence (AI) and robotics into nerve reconstruction surgery presents a compelling opportunity for growth in the North America nerve repair and regeneration market. Robotic-assisted surgical platforms are increasingly being adopted for precision-driven procedures, particularly in microsurgery where nerve suturing demands extreme accuracy. AI-powered imaging and intraoperative navigation systems are enhancing surgical decision-making by providing real-time visualization of nerve structures. For instance, the use of machine learning algorithms to analyze intraoperative nerve conduction data has improved post-surgical outcomes by enabling surgeons to assess nerve viability instantly. Additionally, robotic platforms such as Medtronic’s Hugo Surgical System and Intuitive Surgical’s Da Vinci are being adapted for nerve graft placement and tissue dissection with sub-millimeter precision. These innovations not only reduce human error but also accelerate patient recovery, making them attractive for both clinicians and healthcare providers.

MARKET CHALLENGES

Limited Long-Term Clinical Efficacy Data for Emerging Therapies

A major challenge confronting the North America nerve repair and regeneration market is the limited availability of long-term clinical efficacy data for many emerging therapies. While numerous regenerative treatments show promise in early-phase trials, sustained functional recovery outcomes remain uncertain. This gap in longitudinal evidence poses difficulties for both clinicians and payers in assessing the true value of novel interventions. For example, despite promising short-term results from adipose-derived stem cell therapy in treating facial nerve injuries, multi-year studies tracking sensory and motor function restoration remain sparse. Regulatory bodies like the FDA increasingly emphasize real-world evidence and extended follow-up periods before granting full market authorization. This requirement extends product development timelines and increases costs for manufacturers. Furthermore, variability in patient response due to differences in age, comorbidities, and injury severity complicates the standardization of outcomes.

Lack of Standardized Protocols for Nerve Repair Procedures

A persistent challenge in the North America nerve repair and regeneration market is the absence of universally accepted clinical protocols for nerve repair procedures. Variability in surgical approaches, graft selection, and rehabilitation strategies contributes to inconsistent patient outcomes. According to the American Society for Surgery of the Hand, there is no consensus on optimal timing for intervention, choice of nerve conduit versus autograft, or post-operative physical therapy regimens. This lack of standardization stems from diverse clinical experiences and limited comparative effectiveness studies. For instance, a 2023 multicenter review published in Plastic and Reconstructive Surgery revealed that treatment decisions were largely surgeon-dependent, with over 60% of respondents admitting to using different graft types based on personal preference rather than evidence-based guidelines. Efforts by organizations such as the Peripheral Nerve Society and the American Association of Neuromuscular & Electrodiagnostic Medicine to develop standardized care pathways are still in early stages.

SEGMENTAL ANALYSIS

By Surgery Type Insights

The nerve grafting segment was the largest and held 32.2% of the North America nerve repair and regeneration market share in 2024. One of the key drivers behind the continued leadership of autografts is their proven clinical efficacy and biocompatibility, which significantly reduce immune rejection risks compared to allografts or xenografts. According to a 2023 study published in The Journal of Hand Surgery , autografts demonstrated a 90% functional recovery rate in patients with peripheral nerve defects exceeding 3 cm, which is reinforcing their preference among surgeons despite donor site morbidity concerns. Additionally, the high volume of trauma-related nerve injuries fuels demand for autograft procedures. As per the Centers for Disease Control and Prevention (CDC), over 1.6 million emergency department visits in the U.S. in 2022 were due to nerve-damaging injuries , many of which required reconstructive surgery involving nerve grafting. Coupled with growing awareness and improved diagnostic capabilities, this trend sustains the segment's market-leading position.

The stem cell therapy segment is projected to register a CAGR of 18.7% in the next coming years. A major factor fueling this growth is the expansion of stem cell-based research and clinical trials targeting nerve restoration. As per data from the National Institutes of Health (NIH), over 150 active clinical trials in North America in 2023 focused on stem cell applications for neurological conditions , including spinal cord injury, diabetic neuropathy, and post-surgical nerve damage. Another contributing factor is the supportive regulatory environment and increased funding from federal agencies . The U.S. Department of Health and Human Services allocated over $120 million in grants in FY2023 for regenerative medicine projects , including those involving induced pluripotent stem cells (iPSCs) and mesenchymal stem cell (MSC) therapies.

By Product Type Insights

The biomaterials segment held 38.6% of the North America nerve repair and regeneration market share in 2024. The dominance of biomaterials is primarily driven by technological advancements in tissue engineering and the rising preference for off-the-shelf solutions that eliminate the need for donor harvesting. For example, companies like Axogen and Polyganics have commercialized synthetic nerve conduits that offer comparable outcomes to autografts without the complications of secondary surgery. Furthermore, increased incidence of diabetes-induced neuropathy and trauma-related nerve injuries has boosted demand for advanced biomaterials. According to the American Diabetes Association, more than 30 million Americans suffer from some form of neuropathy, which is necessitating long-term regenerative interventions.

The neuromodulation surgery devices segment is expected to grow with an anticipated CAGR of 16.2% from 2026 to 2034. This rapid growth is largely fueled by rising adoption of implantable spinal cord stimulators (SCS) and peripheral nerve stimulators (PNS) for chronic neuropathic pain. According to the International Neuromodulation Society, over 60,000 SCS implants were performed in the U.S. in 2023, a 12% increase from the previous year. Additionally, advancements in wireless and minimally invasive neuromodulation technologies are enhancing patient compliance and physician acceptance. Abbott and Boston Scientific launched next-generation micro-implantable systems in 2023, offering longer battery life and better spatial targeting.

REGIONAL ANALYSIS

United States Nerve Repair and Regeneration Market Insights

The United States was the largest contributor in the North America nerve repair and regeneration market with 84.6% of share in 2024. One of the primary drivers of the U.S. market is the high prevalence of nerve-damaging diseases and traumatic injuries. Moreover, the presence of leading biotechnology and medical device companies fosters rapid commercialization of nerve repair technologies. Major players such as Medtronic, Axogen, and Stryker have headquarters or major R&D facilities in the U.S., ensuring early access to novel therapies. Additionally, FDA expedited pathways for regenerative products and neuromodulation devices further accelerate market entry, reinforcing the U.S. as the nerve repair industry’s epicenter.

Canada Nerve Repair and Regeneration Market Insights

Canada held 11.2% of the North America nerve repair and regeneration market share in 2024. A key driver of market growth in Canada is the rising geriatric population, which increases the incidence of degenerative nerve conditions. Consequently, demand for nerve grafting, neurostimulation, and regenerative therapies is on the rise. In addition, government initiatives promoting biomedical innovation are supporting local development of nerve repair solutions. Innovation, Science and Economic Development Canada (ISED) provided over CAD 85 million in funding during FY2023 for regenerative medicine projects, including nerve tissue engineering.

COMPETITIVE LANDSCAPE

The competition in the North America nerve repair and regeneration market is characterized by a mix of established medical device giants and emerging biotech firms striving to capture a significant market share. The market features a diverse array of products ranging from nerve grafts and conduits to neuromodulation devices and stem cell therapies, each backed by varying levels of clinical evidence and commercialization strategies. Competitive pressures are further intensified by the need for regulatory approvals, reimbursement support, and physician adoption. Firms are investing heavily in research, forging strategic alliances, and expanding their product pipelines to maintain relevance in a rapidly evolving landscape. Additionally, as regenerative medicine gains momentum, companies are exploring next-generation therapies such as bioengineered scaffolds and gene-editing applications to stay ahead of the curve and meet the growing expectations of clinicians and patients alike.

KEY MARKET PLAYERS

Promising Companies dominating the North America Nerve Repair and Regeneration Market include

- Cyberonics

- Medtronic

- Polyganics B.V.

- Stryker Corporation

- AxoGen, Inc.

- Boston Scientific Corporation

- Integra LifeSciences Corporation

- Baxter International Inc.

- St. Jude Medical

- Orthomed S.A.S.

Top Players in the North America Nerve Repair and Regeneration Market

Axogen Inc

Axogen Inc. is a leading innovator in surgical solutions for nerve repair, specializing in biologically active products designed to regenerate damaged nerves. The company’s portfolio includes nerve grafts and tissue processing technologies that are widely used in peripheral nerve reconstruction. Axogen has significantly contributed to advancing non-metallic, off-the-shelf nerve repair solutions, promoting minimally invasive treatment approaches. Its focus on education, clinical research, and physician training has enhanced adoption across surgical specialties in both hospital and ambulatory settings.

Medtronic plc

Medtronic plc is a global leader in medical technology and plays a crucial role in the neuromodulation segment of the nerve repair market. Through its advanced spinal cord stimulators and peripheral nerve stimulation systems, Medtronic offers long-term pain management and functional restoration therapies. The company's extensive R&D infrastructure, coupled with strategic partnerships and product innovations, continues to shape therapeutic standards in chronic nerve conditions across North America.

Integra LifeSciences Holdings Corporation

Integra LifeSciences Holdings Corporation specializes in regenerative medicine and neurosurgical devices, offering a wide range of nerve repair products including collagen-based conduits and allografts. Integra’s contributions have expanded access to alternatives to traditional autografts, improving patient outcomes and reducing donor site complications.

Top Strategies Used by Key Market Participants

One major strategy employed by key players in the North America nerve repair and regeneration market is product innovation and development, where companies continuously invest in research to introduce advanced biomaterials, nerve conduits, and regenerative therapies that offer superior efficacy and safety. These innovations help differentiate offerings in a competitive landscape.

Another critical approach is strategic collaborations and partnerships, which allow firms to pool resources, share expertise, and accelerate time-to-market for new solutions. Collaborations with academic institutions, research organizations, and healthcare providers enable deeper clinical insights and broader market penetration.

The market expansion through mergers and acquisitions is frequently leveraged to enhance product portfolios and geographic reach. Larger firms strengthen their competitive edge and consolidate their position in the evolving nerve repair and regeneration space with niche players with promising technologies.

RECENT MARKET DEVELOPMENTS

- In January 2023, Axogen announced the launch of its new nerve preservation solution aimed at extending the viability of autologous nerve grafts by enhancing surgical flexibility and outcomes.

- In June 2023, Medtronic introduced a next-generation spinal cord stimulator system designed specifically for treating chronic neuropathic pain with improved targeting and reduced side effects.

- In October 2023, Integra LifeSciences acquired a biotech startup specializing in bioengineered nerve matrices, which is strengthening its regenerative medicine portfolio and expanding its pipeline.

- In February 2024, Stryker partnered with a leading university to conduct clinical trials on a novel nerve guidance conduit aimed at improving recovery times post-surgery.

- In May 2024, Boston Scientific launched an AI-integrated platform for optimizing neuromodulation therapy delivery by aiming to improve patient response rates and physician decision-making.

MARKET SEGMENTATION

This research report on the North American nerve repair and regeneration market has been segmented and sub-segmented into the following categories.

By Surgery

- Direct Neuropathy

- Epineural Repair

- Perineural Repair

- Group Fascicular Repair

- Nerve Grafting

- Autografts

- Allografts

- Xenografts

- Stem Cell Therapy

- Neuromodulation Surgery

- External Neuromodulation Surgery

- Internal Neuromodulation Surgery

By Product

- Biomaterials

- Nerve Conduits

- Nerve Protectors

- Nerve Wraps

- Nerve Connectors

- Neuromodulation Surgery Devices

- External Neuromodulation Surgery

- Transcutaneous Electrical Nerve Stimulation

- Transcranial Magnetic Stimulation

- Internal Neuromodulation Surgery

- Spinal Cord Stimulation

- Deep Brain Stimulation

- Sacral Nerve Stimulation

- Vagus Nerve Stimulation

- Others

- External Neuromodulation Surgery

By Country

- United States

- Canada

- Rest of North America