North America Optical Sensor Market Size, Share, Trends & Growth Forecast Report By Sensor Type (Fiber Optic Sensors, Image Sensors, Position Sensors, Ambient Light & Proximity Sensors, Infrared Sensors), Application, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2024 to 2033

North America Optical Sensor Market Size

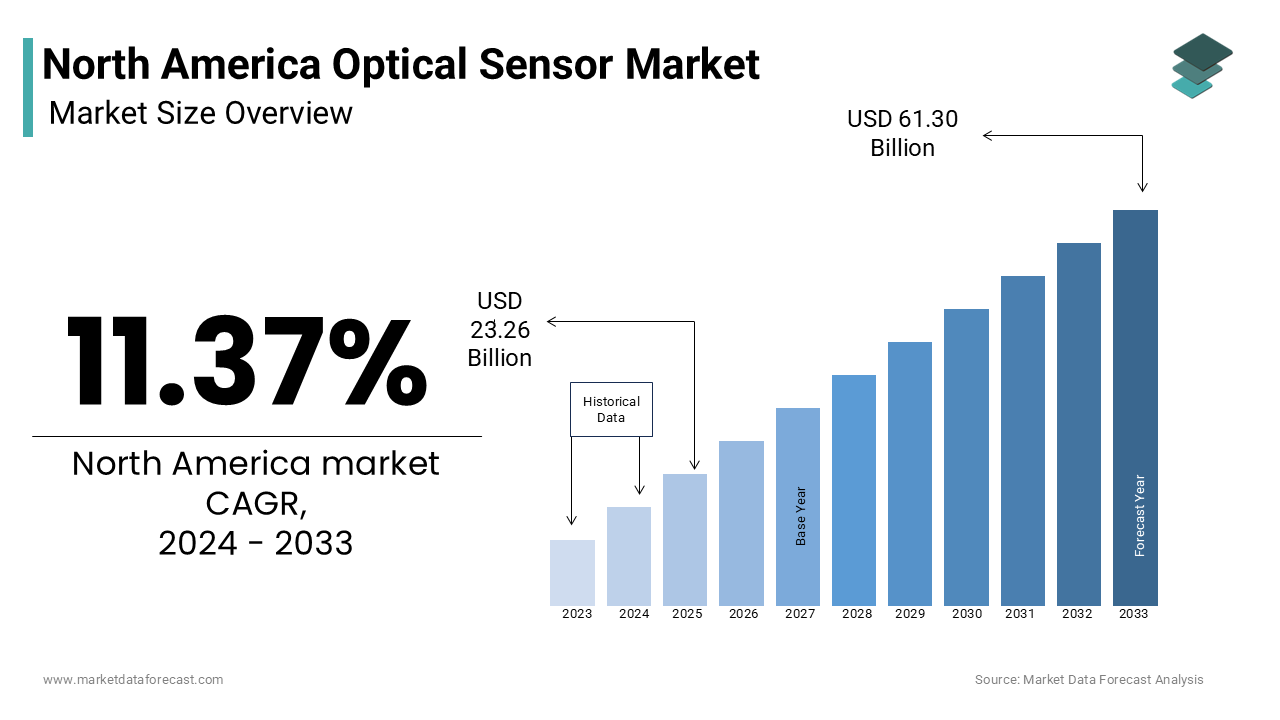

In 2024, the North America Optical Sensor Market was valued at USD 23.26 billion and is forecasted to grow to USD 61.30 billion by 2033, at a CAGR of 11.37%.

The optical sensor is range of devices that detect and measure light or other electromagnetic radiation to provide data for industrial, commercial, and consumer applications. These sensors are widely used in manufacturing automation, healthcare diagnostics, automotive systems, aerospace navigation, environmental monitoring, and smart building technologies. Optical sensors operate using principles such as absorption, reflection, fluorescence, and interferometry to enable precision sensing in diverse environments. According to the U.S. Department of Commerce, the United States leads global investments in photonics and optoelectronics, with over 3,000 companies actively engaged in sensor development and integration across multiple sectors.

MARKET DRIVERS

Growth of Industrial Automation and Smart Manufacturing

The rapid expansion of industrial automation and smart manufacturing systems is fuelling the growth of the North America optical sensor market. Optical sensors are integral to automated production lines, where they enable real-time object detection, dimensional measurement, and product sorting. In sectors like food and beverage, pharmaceuticals, and automotive manufacturing, these sensors ensure high levels of precision and compliance with safety standards. Additionally, the rise of predictive maintenance strategies has boosted demand for optical sensors capable of detecting anomalies through vibration analysis, thermal imaging, and spectral monitoring. As manufacturers seek to reduce downtime and improve operational efficiency, optical sensors have become essential components in smart factories leveraging IoT and AI-based analytics for performance optimization.

Expansion of Automotive and Autonomous Vehicle Development

The accelerated development of advanced driver-assistance systems (ADAS) and autonomous vehicles is ascribed to bolster the growth of the North America optical sensor market. According to the Center for Automotive Research, over 80% of new vehicle models introduced in North America in 2023 featured some form of optical sensing technology, including LiDAR, CMOS image sensors, and infrared proximity detectors. These sensors are crucial for functions such as lane departure warnings, adaptive cruise control, obstacle detection, and 360-degree surround view systems. Moreover, the rise of electric vehicles (EVs) has further amplified the need for optical sensors in battery management, cabin monitoring, and gesture-controlled infotainment systems. Companies like Tesla, General Motors, and Ford are integrating multi-sensor fusion architectures that rely heavily on optical inputs for situational awareness and safe operation.

MARKET RESTRAINTS

High Cost of Advanced Optical Sensor Systems

The high cost associated with advanced optical sensor systems, which can limit widespread adoption, particularly among small and medium-sized enterprises (SMEs) is restricting the growth of the North America optical sensor market. According to the National Association of Manufacturers, nearly 60% of surveyed SMEs cited capital expenditure constraints as a major barrier to deploying optical sensing technologies in production environments. High-performance optical sensors, especially those incorporating LiDAR, hyperspectral imaging, or fiber optics, often require specialized materials, precision optics, and complex signal processing hardware. Furthermore, integration costs including software compatibility, calibration, and system redesign add to the financial burden.

Complexity of Integration with Existing Infrastructure

The complexity involved in integrating advanced optical sensors with legacy industrial and transportation systems is also to degrade the growth of the North America optical sensor market. According to the Industrial Internet Consortium, many manufacturing facilities in the U.S. still rely on outdated control systems that lack compatibility with modern optical sensing interfaces, which is necessitating costly upgrades to support seamless connectivity. In the automotive sector, the Society of Automotive Engineers notes that integrating optical sensors with vehicle electronic architectures requires extensive validation to ensure functional safety, cybersecurity, and interoperability with radar and ultrasonic systems. Moreover, in healthcare and aerospace applications, regulatory compliance adds another layer of complexity. The U.S. Food and Drug Administration mandates rigorous testing for optical sensors used in diagnostic equipment, while the Federal Aviation Administration enforces strict certification protocols for optical sensing units in aircraft navigation and flight control systems.

MARKET OPPORTUNITIES

Integration with Artificial Intelligence and Machine Vision

The integration of optical sensing technologies with artificial intelligence (AI) and machine vision systems is creating new opportunities for the growth of the North America optical sensor market. According to the Computer Vision Foundation, AI-driven vision systems are being adopted at an unprecedented rate across manufacturing, logistics, and healthcare, creating a surge in demand for high-resolution optical sensors capable of delivering real-time visual data. AI-powered optical sensors are now being used in quality assurance processes to detect defects at microscopic levels, improving yield rates and reducing waste in semiconductor, pharmaceutical, and food packaging industries. Additionally, in retail and security applications, facial recognition systems powered by optical sensors and deep learning algorithms are gaining traction.

Expansion of Medical Diagnostics and Remote Monitoring Devices

The growing adoption of optical sensing in medical diagnostics and remote patient monitoring systems is levelling up the growth of the North America optical sensor market. According to the American Telemedicine Association, telehealth usage increased by 63% in 2023 compared to pre-pandemic levels, which is driving demand for wearable and portable diagnostic devices equipped with optical sensors. Wearable fitness trackers, pulse oximeters, and continuous glucose monitors all rely on optical sensors to measure vital signs such as heart rate, blood oxygen saturation, and skin temperature. The Centers for Disease Control and Prevention emphasize that non-invasive monitoring tools powered by optical sensing have improved early disease detection and reduced hospital readmission rates, particularly among chronic disease patients. Furthermore, hospitals and clinics are increasingly adopting optical coherence tomography (OCT), endoscopic imaging, and spectroscopy-based diagnostics that rely on advanced optical sensors for high-resolution internal imaging.

MARKET CHALLENGES

Environmental Sensitivity and Performance Variability

The environmental sensitivity of optical components, which can affect performance and reliability under varying conditions is likely to slow down the growth of the North America optical sensor market in the coming years. According to the National Institute of Standards and Technology, optical sensors operating in outdoor or uncontrolled environments face significant performance variability, particularly in industrial and agricultural applications. Additionally, exposure to moisture and particulate matter can degrade optical surfaces, reducing lifespan and increasing maintenance needs.

Supply Chain Disruptions and Component Shortages

The ongoing supply chain disruptions and shortages of critical components such as photodiodes, optical filters, and laser diodes is additionally to limit the growth of the North America optical sensor market. According to Deloitte’s 2023 Global Semiconductor Risk Outlook, the optical sensor industry faces extended lead times due to bottlenecks in wafer fabrication, packaging, and testing capacities. The U.S. International Trade Commission reports that geopolitical tensions and export restrictions have disrupted the availability of high-precision optical components those sourced from Asia-Pacific suppliers. Many manufacturers have had to delay product launches or scale back production targets due to limited access to raw materials and subassemblies. Moreover, labor shortages in advanced manufacturing hubs and logistical bottlenecks at major ports have compounded delivery delays. The U.S. Chamber of Commerce notes that in 2023, nearly 45% of optical sensor producers experienced shipment delays exceeding six weeks, impacting project timelines and client commitments.

SEGMENTAL ANALYSIS

By Technology Insights

The optical coherence tomography (OCT) segment was the largest and held 34.2% of the North America optical sensor market share in 2024 with the growing prevalence of chronic diseases requiring advanced diagnostic tools. According to the Centers for Disease Control and Prevention, over 60% of American adults suffer from at least one chronic condition, driving demand for non-invasive imaging technologies like OCT.Additionally, technological advancements have significantly improved OCT resolution and speed, which is making it indispensable in both clinical and research settings. Moreover, strong government and private sector investment in healthcare innovation supports OCT expansion. The U.S. Department of Health and Human Services has funded several OCT-based research initiatives aimed at improving early cancer detection and neurodegenerative disease monitoring.

The hyperspectral imaging segment is emerging with a CAGR of 12.8% from 2025 to 2033 with the expansion of precision agriculture and crop monitoring systems. In California, which produces nearly half of all U.S. fruits and vegetables, agricultural tech firms are deploying these sensors to optimize irrigation and pesticide use. Additionally, the rise of industrial process monitoring and counterfeit detection applications is fueling demand. The Food and Drug Administration reports that hyperspectral imaging is increasingly used in pharmaceutical manufacturing to ensure drug purity and uniformity without damaging samples. Moreover, advancements in compact, cost-effective hyperspectral modules are expanding deployment beyond traditional sectors. Companies like Headwall Photonics and Applied Spectral Imaging are developing handheld and embedded solutions for field use in environmental monitoring and forensic investigations.

By Sensor Type Insights

The image sensors segment was accounted in holding 39.2% of the North America optical sensor market share in 2024 with the widespread integration of CMOS and CCD image sensors into smartphones, tablets, and laptops. According to the Consumer Technology Association, over 140 million smartphones were sold in the U.S. in 2023, each incorporating multiple image sensors for facial recognition, biometric authentication, and camera functionality. The rapid expansion of machine vision and autonomous vehicle development is additionally to fuel the growth of the North America optical sensor market. The Society of Automotive Engineers reports that nearly 80% of new car models launched in North America in 2023 featured front-facing cameras using advanced image sensors for lane-keeping assistance and pedestrian detection. Furthermore, industrial automation and robotics rely heavily on image sensors for real-time object recognition and quality control.

The fiber optic sensors segment is projected to expand with a CAGR of 11.6% throughout the forecast period. The increasing use of fiber optic sensors in structural health monitoring of bridges, pipelines, and buildings is ascribed to fuel the growth of the segment. According to the Federal Highway Administration, over 45,000 bridges in the U.S. were classified as structurally deficient in 2023, prompting investments in continuous monitoring systems using distributed fiber optic sensing. Additionally, the oil & gas industry is adopting fiber optic sensors for downhole monitoring and leak detection. Natural Resources Canada reports that several Canadian pipeline operators have implemented fiber-based strain and temperature sensing systems to enhance operational safety and reduce maintenance costs. Moreover, military and aerospace applications are accelerating adoption, with the U.S. Department of Defense investing in fiber optic gyroscopes and vibration monitoring systems for aircraft and submarines.

By Application Insights

The medical application segment was the largest and held 28.3% of the North America optical sensor market share in 2024 due to the increased deployment of optical sensors in non-invasive diagnostic devices, including pulse oximeters, glucose monitors, and endoscopic imaging systems. According to the Centers for Disease Control and Prevention, chronic diseases such as diabetes and cardiovascular disorders affect over 150 million Americans with continuous monitoring solutions powered by optical sensing technologies. Additionally, hospitals and research institutions are adopting optical coherence tomography (OCT), spectroscopy, and photoplethysmography (PPG) for enhanced diagnostic accuracy. Moreover, telemedicine expansion is reinforcing the need for wearable optical sensors. The American Telemedicine Association reports that remote patient monitoring device shipments grew by 55% in 2023, with many relying on optical sensing for vital sign measurement.

The automotive application segment is likely to have a significant CAGR of 13.2% from 2025 to 2033 with the accelerated adoption of LiDAR and CMOS image sensors in autonomous and semi-autonomous vehicles. According to the Center for Automotive Research, over 85% of new luxury vehicles introduced in 2023 included optical sensing systems for adaptive cruise control, lane departure warning, and blind-spot detection. Additionally, electric vehicle manufacturers are incorporating optical sensors for cabin monitoring, battery thermal management, and gesture-controlled interfaces. The U.S. Department of Energy notes that EVs require more sophisticated sensing capabilities compared to internal combustion engine vehicles, further boosting optical sensor demand. The National Highway Traffic Safety Administration requires automakers to implement occupant detection systems using optical sensors to prevent child entrapment incidents.

REGIONAL ANALYSIS

United States Optical Sensor Market Insights

The United States was the top performer in the North America optical sensor market by accounting for 78.3% of share in 2024 due to the integrated development of optical sensors in defense, aerospace, and healthcare industries. Additionally, the U.S. leads in commercialization of optical sensors within autonomous vehicles and smart manufacturing.

Canada Optical Sensor Market Insights

Canada optical sensor market growth is driving with the rising adoption of optical sensors in healthcare and life sciences. The Canadian Institutes of Health Research emphasizes that hospitals and research centers are increasingly utilizing optical coherence tomography (OCT) and fluorescence-based sensors for early disease diagnosis and minimally invasive surgery. Additionally, Canadian aerospace and defense sectors are integrating optical sensors for structural health monitoring and aircraft navigation. Moreover, smart infrastructure initiatives are gaining traction, with cities like Toronto and Vancouver piloting fiber-based sensors for bridge and tunnel monitoring. The Canadian Standards Association is actively developing guidelines to facilitate broader adoption of optical sensing in civil engineering and energy networks.

KEY MARKET PLAYERS AND COMPETETIVE LANDSCAPE

Honeywell International Inc., Texas Instruments Incorporated, Rockwell Automation, Inc., STMicroelectronics, TE Connectivity Ltd., OSI Optoelectronics, Hamamatsu Photonics K.K., Onsemi (ON Semiconductor Corporation), Analog Devices, Inc., and Broadcom Inc.

The competition in the North America optical sensor market is characterized by a dynamic mix of global technology leaders, mid-sized specialists, and emerging startups striving to capture market share through differentiation, innovation, and strategic positioning. As industries increasingly adopt optical sensing for automation, diagnostics, and environmental monitoring, companies are under pressure to deliver high-performance, reliable, and cost-effective solutions. Product differentiation remains a central battleground, with firms investing in next-generation sensor architectures, including multi-spectral imaging, edge AI integration, and ultra-compact designs suitable for wearable and mobile applications.

Customer engagement strategies have evolved beyond product sales to include software licensing, cloud connectivity, and system integration services, ensuring long-term value creation. Additionally, participation in federal and state-funded R&D programs has become essential for expanding market access and aligning with national innovation priorities in defense, healthcare, and autonomous mobility. While multinational corporations dominate due to their R&D scale and brand strength, mid-tier players are gaining traction by focusing on niche segments, localized service offerings, and cost-effective sensor platforms. This evolving competitive environment fosters continuous innovation and drives the industry toward greater efficiency, resilience, and alignment with global sustainability trends.

Top Players in the North America Optical Sensor Market

Teledyne Technologies

Teledyne is a leading manufacturer of advanced optical sensors, particularly known for its expertise in scientific imaging, LiDAR, and industrial vision systems. The company supplies high-performance CMOS and CCD sensors to aerospace, defense, and life science sectors, playing a crucial role in space exploration and medical diagnostics. Its acquisition strategy and deep R&D focus have fueled its position as a key innovator in the North American optical sensor landscape.

Hamamatsu Photonics (North American Operations)

Hamamatsu Photonics delivers ultra-sensitive optical sensing solutions tailored for medical imaging, nuclear physics, and industrial automation. In North America, the company plays a pivotal role in advancing photomultiplier tubes, single-photon detectors, and custom sensor arrays for research and diagnostics. Its collaboration with academic and clinical institutions has made Hamamatsu a trusted partner in cutting-edge optical sensor applications.

Excelitas Technologies Corp.

Excelitas specializes in photonic and optical sensor solutions for healthcare, defense, and industrial markets. Known for its high-performance infrared and laser-based sensing products, Excelitas serves critical applications such as night vision, fire detection, and spectroscopy. Its commitment to customized sensor design and broad product portfolio make it a key contributor to North America’s optical sensing ecosystem.

FLIR Systems (a part of Teledyne Technologies)

FLIR is a major player in infrared and thermal imaging sensors, widely used in defense, security, and industrial monitoring. Following its acquisition by Teledyne, FLIR has expanded its reach in optical sensing for autonomous vehicles, drone navigation, and predictive maintenance. Its emphasis on ruggedized and portable sensor systems has reinforced its presence across diverse commercial and military applications.

Osram Opto Semiconductors (North American Division)

Osram is a global leader in LED-based optical sensing technologies, with a strong footprint in automotive and consumer electronics applications. In North America, Osram supplies proximity, ambient light, and driver monitoring sensors for next-generation vehicles and smart devices. Its focus on energy-efficient and human-centric lighting applications has positioned it as a key supplier in the automotive and IoT-enabled sensor markets.

Top Strategies Used by Key Market Participants

One major strategy employed by leading optical sensor manufacturers is deep integration with artificial intelligence and machine learning algorithms by enabling real-time data interpretation and decision-making in industrial and medical applications. Companies like Sony and Lumentum are embedding AI-enhanced image processing directly into sensor hardware to improve performance in autonomous vehicles and robotic vision.

The strategic acquisitions and partnerships to expand technological portfolios and geographic reach are allowing companies to access specialized capabilities in LiDAR, spectroscopy, and fiber optics. For instance, Teledyne’s acquisition of FLIR Systems was driven by the need to consolidate optical sensing expertise across defense and industrial domains. Firms are focusing on customized sensor development for niche applications in biophotonics, aerospace, and homeland security by ensuring differentiation in a competitive landscape.

RECENT MARKET DEVELOPMENTS

- In January 2024, Teledyne Technologies announced the launch of a new line of high-speed CMOS image sensors designed for autonomous vehicle perception systems, aiming to enhance real-time object detection and depth sensing capabilities in next-generation self-driving cars.

- In March 2024, Hamamatsu Photonics expanded its manufacturing facility in Bridgewater, New Jersey, to increase production capacity for ultra-low-light optical sensors used in life sciences, security, and quantum sensing applications.

- In June 2024, Excelitas Technologies introduced a new family of infrared sensors for smart building automation, targeting HVAC and lighting control systems with improved occupancy detection and energy efficiency features.

- In September 2024, Lumentum Holdings entered a joint venture with a leading automotive Tier 1 supplier to develop integrated LiDAR modules for advanced driver-assistance systems, strengthening its position in the rapidly growing ADAS market in North America.

- In December 2024, Osram Opto Semiconductors unveiled a suite of eye-safe infrared sensors for facial authentication in consumer electronics, aiming to meet rising demand for secure and contactless biometric identification in smartphones and wearables.

MARKET SEGMENTATION

This research report on the North America Optical Sensor Market is segmented and sub-segmented based on categories.

By Sensor Type

- Fiber Optic Sensors

- Image Sensors

- Position Sensors

- Ambient Light & Proximity Sensors

- Infrared Sensors

By Application

- Commercial

- Consumer Electronics

- Medical

- Automotive

- Industrial

- Aerospace and Defense

- Optocouplers

By Country

- U.S.

- Canada

- Rest of North America

Frequently Asked Questions

What are the key drivers of the North America Optical Sensor Market?

The market is driven by rising demand in consumer electronics, industrial automation, automotive applications (especially ADAS systems), healthcare diagnostics, and increasing adoption in IoT and smart devices.

What types of optical sensors are commonly used in North America?

The most common types are fiber optic sensors, image sensors, photoelectric sensors, and ambient light sensors.

What challenges does the North America Optical Sensor Market face?

Challenges include high cost of advanced sensors, complexity in integration, and competition from other sensing technologies like ultrasonic and LiDAR.

What is the future outlook of the North America Optical Sensor Market?

The market is expected to witness significant growth due to advancements in sensor technology, increased penetration in emerging applications, and the expansion of smart infrastructure and Industry 4.0.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com