North America Refrigerants Market Size, Share, Trends & Growth Forecast Report By Type, By Application, By End User, and By Country (United States, Canada, Mexico & Rest of North America) – Industry Analysis and Forecast, 2026 to 2034

North America Refrigerants Market Size

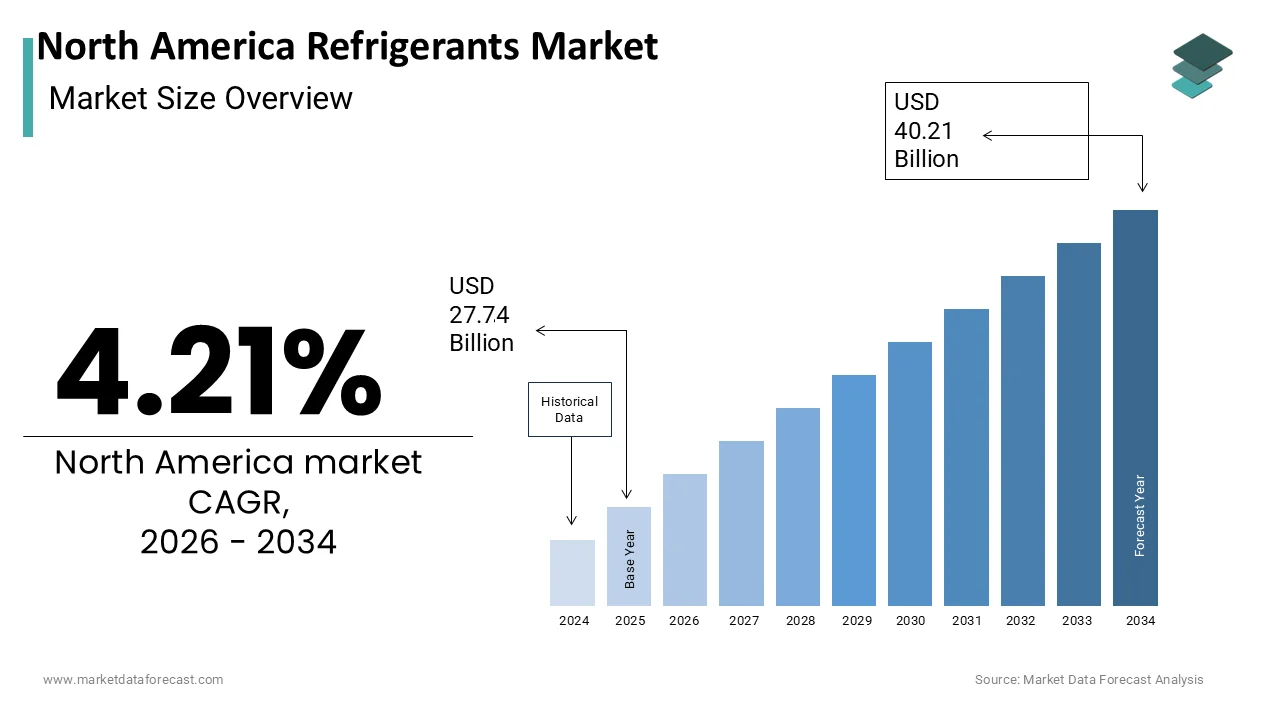

The North America Refrigerator Market was valued at USD 27.74 billion in 2025, is estimated to reach USD 28.91 billion in 2026, and is projected to reach USD 40.21 billion by 2034, growing at a CAGR of 4.21% from 2026 to 2034.

A refrigerator, often called a fridge, is a vital kitchen appliance that uses a thermally insulated compartment and a heat pump to cool and preserve food. These substances operate as the fundamental working fluids within vapor compression cycles, enabling precise temperature regulation for climate control,l food preservation, and manufacturing processes. The operational landscape has shifted dramatically due to evolving environmental mandates and infrastructure modernization initiatives. According to the United States Census Bureau, new residential construction permits reached 1450000 units during the preceding fiscal year,r reflecting sustained demand for integrated climate control infrastructure. The Environmental Protection Agency established a phased reduction schedule targeting high global warming potential compounds with a 40 percent consumption decrease mandated by 2024 and an 85 percent reduction by 2036. As per the National Oceanic and Atmospheric Administration, the United States experienced 23 separate billion-dollar weather and climate disasters that collectively generated approximately 115 billion dollars in direct losses, intensifying the structural reliance on reliable thermal management networks. The industrial sector accounts for approximately 37% to 38% of total final global energy consumption, making it the single largest energy end-use sector and driving an aggressive push for efficiency updates by organizations like ASHRAE. These operational parameters demonstrate how infrastructure development and environmental compliance intersect to shape the functional ecosystem for refrigerant utilization across the region.

MARKET DRIVERS

Escalating Extreme Weather Events Accelerate Cooling Infrastructure Deployment

The increasing frequency of prolonged heat waves directly amplifies consumer and commercial demand for active thermal management systems across residential and industrial facilities, which drives the growth of the North America refrigerator market. Rising ambient temperatures compel property owners to upgrade or install new air conditioning units to maintain habitable indoor environments and protect temperature-sensitive inventory. According to statistics from the Centers for Disease Control and Prevention, expanding seasonal baseline temperatures have driven increasing heat-related mortality rates across the United States, prompting municipal governments to closely review local climate control capabilities. The National Weather Service issues extensive regional Extreme Heat Warnings during anomalous summer heatwave cycles, establishing mechanical cooling systems as essential public health infrastructure rather than a luxury appliance. Commercial real estate operators have scaled up the routine replacement and upgrading of legacy rooftop chillers to comply with updated indoor air quality and building efficiency codes. Industrial manufacturing facilities heavily expand refrigeration networks to protect operational continuity during peak ambient heat periods, with thermal management and freezing steps consuming the primary share of processing facility energy grids. This persistent thermal stress generates continuous procurement cycles that sustain robust demand for refrigerant compounds required to charge newly installed and retrofitted equipment across multiple economic sectors.

Regulatory Phaseout Schedules Compel System Replacement Cycles

Legislative mandates targeting high global warming potential substances force widespread equipment turnover and generate sustained procurement demand for compliant alternatives, and thereby propel the expansion of the North American refrigerator market. Facility operators must replace legacy cooling infrastructure that relies on restricted compounds to maintain operational legality and avoid substantial financial penalties. According to the Environmental Protection Agency, the historical American consumption baseline for regulated high-GWP fluids was formally established at 303.9 million metric tons of CO2 equivalent before enforcing the AIM Act phase-down limits. The Environmental Protection Agency mandates that new commercial HVAC and chiller installations transition away from high-GWP compounds, driving contractors to heavily source compliant alternative blends well in advance of final system installation deadlines. Industry installation trends show that mechanical technicians are performing a high volume of proactive system updates as property managers scramble to avoid high maintenance overhead on legacy equipment before strict manufacturing bans take hold. Industrial cold storage operators have scaled up facility modernization programs, utilizing massive volumes of next-generation low-impact alternatives to completely replace legacy phased-out fluorinated gas inventory. Manufacturing enterprises in the automotive and pharmaceutical sectors aligned their procurement strategies with the established phaseout timeline, securing long-term supply agreements to prevent operational disruptions. This regulatory-driven equipment turnover establishes a predictable and continuous demand stream that sustains market activity across residential, commercial,l and industrial cooling networks.

MARKET RESTRAINTS

Stringent Certification Requirements Elevate Compliance Expenditures

Complex regulatory frameworks impose substantial financial and administrative burdens on manufacturers and service providers attempting to distribute compliant thermal management compounds, which hampers the growth of the North American refrigerator market. The certification process demands rigorous testing, documentation,n and facility audits that delay product commercialization and increase operational overhead. Industry compliance data shows that transitioning to next-generation HVAC systems and enforcing stricter safety protocols for mildly flammable alternatives have increased specialized overhead for equipment owners. The Environmental Protection Agency mandates comprehensive, inspectable recordkeeping for all covered refrigeration systems, requiring equipment owners to document leak rates, verification tests, and quantities added for every service intervention. Training programs designed to prepare technicians for advanced low-GWP certifications emphasize rigorous field training and safety testing, creating a localized demand for highly skilled workforce personnel. Small and medium-sized mechanical contractors face significant compliance management overhead to implement specialized software, calibrate tracking tools, and keep up with rapidly evolving environmental mandates. Chemical manufacturers highlight that navigating complex federal approval channels for next-generation, low-impact chemical formulations requires significant administrative planning and long regulatory review timelines. These compliance expenditures suppress market expansion by restricting entry for innovative suppliers and inflating baseline operational costs across the distribution network.

Raw Material Volatility Disrupts Production Continuity

Fluctuations in feedstock availability and pricing directly constrain manufacturing output and limit the consistent supply of thermal management compounds required by end users within the North American refrigerator market. Petrochemical derivatives, fluorinated chemicals, and specialty catalysts represent critical inputs that experience unpredictable market behavior due to geopolitical shifts and extraction limitations. According to energy economic tracking, global supply disruptions and shifting energy baselines have driven severe cost volatility for essential petrochemical building blocks, destabilizing expense planning for chemical processors. The International Trade Administration monitors trade enforcement actions on chemical imports, forcing domestic manufacturers to carefully diversify their raw input supply networks. Industrial production facilities report that temporary supply blockages for critical chemical intermediates can disrupt localized blending schedules and output lines. Logistics and safety restrictions regarding the handling and interstate shipping of pressurized hazardous gases have driven up specialized freight costs for commercial and industrial buyers. Tightening allocation caps under environmental phase-down schedules forces regional distribution centers to carefully manage inventory reserves to handle seasonal demand spikes. This persistent supply instability restricts market fluidity and forces end users to delay equipment servicing or pursue suboptimal thermal management alternatives.

MARKET OPPORTUNITIES

Transition to Low Global Warming Potential Alternatives Expands Commercial Applications

The accelerated adoption of environmentally optimized thermal management compounds opens extensive commercial deployment avenues across retail hospitality and data center operations, which is anticipated to accelerate the growth of the North American refrigerator market. Facility managers actively seek compliant alternatives that deliver equivalent cooling performance while satisfying stringent sustainability mandates and corporate environmental targets. According to the International Institute of Refrigeration, transitioning from legacy high-GWP fluids to next-generation alternatives can slash direct chemical warming impacts by over 99%, driving widespread global commercial adoption. Industrial computing indices show that hyperscale data facilities are aggressively installing advanced liquid cooling and low-GWP chiller loops to maintain server temperature stability amid massive computational loads. Retail grocery chains are steadily updating their refrigeration footprints, utilizing corporate sustainability programs to expand low-GWP and natural refrigerant architectures across regional logistics facilities. Hospitality operators integrate low-impact cooling architectures into newly constructed properties to earn critical LEED credits under the U.S. Green Building Council's energy and atmosphere criteria. Chemical manufacturers have aggressively expanded domestic and global manufacturing plants to satisfy the accelerating procurement pipeline for low-GWP industrial fluids. This sector-wide transition generates substantial volume expansion while positioning suppliers to capture long-term contractual relationships with sustainability-focused enterprise clients.

Infrastructure Modernization Initiatives Drive Retrofit Market Expansion

Aging thermal management systems across commercial and municipal properties create a substantial retrofit pipeline within the North American refrigerator market. This demand requires specialized, compatible compounds and technical conversion services. Building owners prioritize equipment upgrades that extend operational lifespans while reducing energy consumption and environmental impact through targeted refrigerant replacements. According to the American Council for an Energy-Efficient Economy, widespread building efficiency retrofits and HVAC modernizations represent a massive commercial opportunity to curb urban greenhouse gas emissions. The Department of Energy provides federal grant frameworks that enable municipal authorities to accelerate whole-building energy retrofits across public facilities. Public agencies and municipal school districts are executing modernization campaigns to phase out aging HVAC infrastructure, utilizing federal infrastructure funds to deploy high-efficiency climate technology. Mechanical trade networks are scaling up specialized technical training programs to ensure the workforce can safely execute complex system conversions utilizing mildly flammable alternative fluids. Equipment manufacturers provide specialized modification components that streamline the mechanical installation process, easing field installation demands for commercial contractors. This retrofit ecosystem transforms aging infrastructure into a sustained demand channel that supports long-term refrigerant procurement and technical service expansion.

MARKET CHALLENGES

Legacy System Incompatibility Complicates Transition Protocols

Older cooling infrastructure exhibits fundamental engineering limitations that prevent seamless integration with modern, low-impact refrigerant formulations, which is challenging the growth of the North American refrigerator market. Consequently, these hardware constraints create significant technical barriers during routine replacement cycles. Material compatibility,y pressure tolerance, es, and lubricant specifications often conflict with newer compound properties, requiring extensive system modifications before successful operation can occur. According to ASHRAE technical briefs, the transition to next-generation low-GWP refrigerants imposes physical constraints on existing vapor-compression equipment, requiring property managers to weigh cost, efficiency, and component safety limits. Thermodynamic research published by the National Institute of Standards and Technology emphasizes that alternative refrigerant formulations must be carefully paired with compatible compressor maps to preserve design capacity and prevent mechanical degradation. Chemical developers and compressor manufacturers execute extensive laboratory testing to validate that newly introduced synthetic lubricants achieve safe chemical compatibility with alternative refrigerants. Facility operators face variable system-retrofit expenses to address physical seal compatibility and mechanical oil-flushing steps when converting older equipment to handle next-generation compounds. The Environmental Protection Agency mandates strict leak verification testing following system interventions on regulated equipment, forcing technicians to document compliance within clear statutory timelines. These technical mismatches extend deployment schedules and increase capital requirements for end users attempting to transition toward compliant thermal management solutions.

Specialized Workforce Deficiency Constrains Service Deployment Capacity

The expanding demand for advanced thermal management compounds coincides with a critical shortage of technicians trained in safe handling and precise charging procedures for next-generation formulations, which in turn inhibits the expansion of the North American refrigerator market. Complex safety protocols and specialized equipment requirements limit the number of qualified professionals available to execute system conversions and routine maintenance across residential and commercial networks. According to the U.S. Bureau of Labor Statistics, employment for refrigeration and HVAC technicians is projected to grow 8% over the coming decade, driven by sustained demand for sophisticated climate infrastructure. Technical testing bodies like NATE have introduced specialized certifications for low-GWP and A2L flammable alternatives to ensure field technicians are trained in updated safety protocols. Trade experts note that as the average age of a core mechanical professional sits near 54, the rate of legacy retirements is outpacing new technical school entrants, driving intense demand for skilled labor. Commercial insurers evaluate risk metrics for mechanical contractors based on documented workforce safety credentials and adherence to updated regional building codes. This workforce gap extends service wait times and forces facility operators to delay critical equipment maintenance,e creating operational vulnerabilities across temperature-dependent commercial environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Honeywell International Inc., The Chemours Company, Arkema S.A., Linde plc, Daikin Industries, Ltd., Orbia Advance Corporation, S.A.B. de C.V., AGC Inc., A-Gas International Limited, Air Liquide S.A., Airgas, Inc., Hudson Technologies, Inc., National Refrigerants, Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The hydrofluorocarbons segment dominated the North American refrigerant market and accounted for a 54.2% share in 2025. This dominance of the segment was driven by entrenched infrastructure compatibility and established supply chains across residential and commercial cooling networks. Industry operational reviews show that despite aggressive regulatory phasedowns, the vast majority of legacy residential and commercial cooling units in the United States continue to rely on HFC-based formulations due to the long lifespan of existing mechanical assets. The American Society of Heating, Refrigeration,g and Air Conditioning Engineers documented that retrofitting legacy systems requires significant capital investment, which delays widespread transition to alternatives. Manufacturers prioritize HFC production to service the substantial installed base of equipment that cannot immediately accommodate next-generation fluids. Industry shipment summaries show that residential HVAC installations have historically relied heavily on HFCs due to established component supply lines and widespread technician familiarity, though active environmental rules are forcing a pivot to alternative solutions. This operational inertia sustains robust procurement cycles that reinforce segment leadership even amid accelerating environmental mandates.

On the other hand, the hydrofluoro olefins segment is predicted to witness the highest CAGR of 14.9% from 2026 to 2034. This acceleration of the segment is propelled by regulatory tailwinds and technological validation that position HFOs as compliant drop-in solutions for multiple applications. According to the United States Environmental Protection Agency, the AIM Act mandates an 85 percent reduction in high global warming potential refrigerant consumption by 2036, creating urgent procurement demand for low-impact alternatives. The International Institute of Refrigeration confirmed that HFO formulations demonstrate equivalent thermodynamic performance to legacy compounds while reducing atmospheric impact by over 99 percent. Automotive original equipment manufacturers accelerated adoption with over 95 percent of new light-duty vehicles in North America specifying R 1234yf for cabin climate control as documented by the Society of Automotive Engineers. To meet the accelerating commercial and industrial procurement pipeline, major chemical producers have scaled up multi-million dollar capital investments to expand the output capacity of low-impact alternatives at global manufacturing facilities. This convergence of regulatory compliance performance parity and supply chain readiness establishes HFOs as the highest velocity growth segment across the regional refrigerant landscape.

By Application Insights

The air conditioning systems segment held the majority share of 52.8% of the North America refrigerant market in 2025. This supremacy of the segment was credited to sustained residential construction activity and commercial building modernization initiatives that drive continuous equipment deployment. According to the United States Census Bureau, new residential construction permits reached 1.45 million units during the preceding fiscal year,r with over 90 percent incorporating central air conditioning infrastructure. As per tracking by the National Oceanic and Atmospheric Administration, expanding baseline summer temperatures have driven record-breaking heatwaves across the United States, intensifying consumer reliance on high-capacity thermal management systems. Commercial real estate operators have scaled up capital outlays into high-efficiency HVAC networks to meet updated ASHRAE ventilation rules and lower commercial carbon tax footprints. Equipment manufacturers responded by scaling production of compliant air conditioning units that utilize next-generation refrigerants while maintaining backward compatibility with existing service networks. This persistent infrastructure expansion generates continuous refrigerant procurement cycles that sustain segment leadership across residential, commercial, and institutional cooling applications.

But the mobile air conditioning segment is estimated to register the fastest CAGR of 6.8% during the forecast period. This expansion of the segment is fuelled by accelerating electric vehicle adoption and stringent cabin climate control requirements that elevate per-vehicle refrigerant consumption. According to the Alliance for Automotive Innovation, electric vehicle sales in North America surpassed 1.2 million units during the most recent fiscal year, with over 98 percent incorporating advanced thermal management systems. The Society of Automotive Engineers documented that electric vehicle battery packs require precise temperature regulation between 15 and 35 degrees Celsius to maintain optimal performance and longevity. Automotive original equipment manufacturers standardized ultra-low GWP R-1234yf formulations for cabin and battery loops to satisfy European MAC Directive rules capping vehicle fluids below a GWP of 150 and to leverage valuable U.S. EPA environmental vehicle manufacturing credits. Logistical data highlights that refrigerated transport networks are scaling up vehicle acquisitions to accommodate rising demand for temperature-sensitive e-commerce grocery home delivery and cold-chain pharmaceutical distribution. This convergence of electrification, on regulatory compliance, and cold chain expansion establishes mobile air conditioning as the highest velocity growth application across the regional refrigerant ecosystem.

By End User Insights

The commercial end-user segment led the North American refrigerant market and captured a 48.5% share in 2025. This leading position of the segment was attributed to extensive deployment across retail, hospitality, and food service, and office infrastructure that requires continuous climate control and food preservation capabilities. Macroeconomic tracking indicators show that private non-residential and commercial structural spending continues to drive multi-billion dollar capital outlays, with high-efficiency commercial environmental loops representing a significant portion of core building utility investments. The Food and Drug Administration enforces strict temperature profiles for storage and transit to ensure product integrity, forcing commercial facility operators to leverage engineering safety margins and advanced sensors to guarantee compliance. The National Restaurant Association highlights that thousands of active food service providers rely heavily on uninterrupted refrigeration systems, making the maintenance and timely replacement of legacy cooling systems vital for restaurant economics. Facility managers prioritize procurement of compliant refrigerants that satisfy both operational reliability and environmental mandates to avoid regulatory penalties and service disruptions. Equipment manufacturers responded by introducing conversion kits that streamline the transition to low global warming potential alternatives while preserving system performance. This sustained infrastructure investment and regulatory alignment reinforce commercial segment leadership across the regional refrigerant landscape.

However, the industrial end user segment is anticipated to witness the fastest CAGR of 7.2% between 2026 and 2034 o, owing to expanding pharmaceutical manufacturing, cold storage logistics,s and specialized processing applications that demand precise thermal management. Research from organizations like the Air-Conditioning, Heating, and Refrigeration Institute (AHRI) tracks massive shifts in equipment manufacturing, driven by expanding cooling demands from high-precision biologics facilities and clinical supply chains. The expanding production of sophisticated biopharmaceuticals and mRNA-based products has driven an aggressive expansion of high-tech manufacturing cleanrooms, heavily scaling up demand for low-temperature process cooling networks. The U.S. Department of Agriculture tracks a vast domestic footprint of over 3.7 billion cubic feet of gross refrigerated storage capacity, which continues to scale to support shifting international agricultural export logistics. Industrial operators increasingly specify low global warming potential refrigerants to align with corporate sustainability targets and avoid future regulatory constraints. To meet tight environmental compliance schedules, leading global chemical companies are expanding specialized production facilities to scale up the availability of low-impact industrial heat transfer fluids. This convergence of manufacturing expansion, logistics modernization,n and environmental compliance establishes industrial applications as the highest velocity growth segment across the regional refrigerant market.

COUNTRY LEVEL ANALYSIS

United States Refrigerant Market Analysis

The United States outperformed other countries in the North American refrigerant market and occupied a 78.3% share in 2025. This dominance of the US market was driven by extensive residential, commercial, and industrial cooling infrastructure, coupled with aggressive environmental regulatory frameworks that drive continuous equipment modernization. According to the Environmental Protection Agency, the American baseline for regulated hydrofluorocarbon consumption was formally established at 303.9 million metric tons of CO2 equivalent prior to initiating the phasedown protocols under the AIM Act. The Department of Energy manages multi-billion-dollar building technology initiatives that broadly incentivize consumer adoption of electric heat pumps and HVAC equipment utilizing next-generation, low-GWP blended refrigerants. The United States Census Bureau documented that residential construction permits reached 1.45 million units during the most recent fiscal year, with over 90 percent incorporating central air conditioning infrastructure. Commercial real estate operators have scaled up capital investments into advanced HVAC systems to meet updated ASHRAE building codes and federal energy guidelines, driving a widespread transition toward low-impact climate systems. Automotive original equipment manufacturers standardized R 1234yf formulations for cabin climate control to comply with California Air Resources Board regulations. This convergence of infrastructure scale,e regulatory momentum, and technological adoption establishes the United States as the undisputed market leader across the regional refrigerant landscape.

Canada Refrigerant Market Analysis

Canada plays a major role in the North American refrigerant market. This growth of the Canadian market is supported by robust residential construction activity and stringent federal environmental policies that accelerate the adoption of low-impact thermal management solutions. According to Statistics Canada, the total value of national building permits has exhibited monthly volatility, showing an 8.4% contraction in early 2026, led primarily by cooling construction intentions within the non-residential segment. Environment and Climate Change Canada implemented a phased reduction schedule targeting high global warming potential compounds,s with a 30 percent consumption decrease mandated by 2025. The Canadian Standards Association updates national mechanical refrigeration codes to establish strict safety and handling parameters for commercial operators converting legacy systems to compliant alternatives. Industrial cold storage operators initiated facility modernization programs that required 45000 metric tons of transition compounds to replace phased-out inventory. Chemical manufacturers expanded distribution networks to ensure a reliable supply of compliant alternatives across remote and urban markets. This alignment of construction growth, regulatory compliance,e and supply chain development sustains Canada's significant regional market position.

COMPETITIVE LANDSCAPE

The North American refrigerant market exhibits moderate concentration with established chemical manufacturers leveraging scale, regulatory expertise,e and distribution reach to maintain a competitive advantage. Leading participants differentiate through proprietary formulations, technical support services, and compliance guidance that facilitate customer transition to low global warming potential alternatives. Emerging players focus on niche applications and natural refrigerant segments where agility and specialized knowledge create entry opportunities. Competitive dynamics intensify as regulatory deadlines accelerate procurement cycles and compress product development timelines. Organizations invest substantially in intellectual property protection, application engineering,g and customer education to defend market position and capture growth in evolving segments. Price competition remains secondary to performance reliability and regulatory compliance as primary selection criteria for commercial and industrial buyers. Supply chain resilience and technical service capabilities increasingly influence procurement decisions amid complex transition requirements.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the North America Refrigerants Market include

- Honeywell International Inc.

- The Chemours Company

- Arkema S.A.

- Linde plc

- Daikin Industries, Ltd.

- Orbia Advance Corporation, S.A.B. de C.V.

- AGC Inc.

- A-Gas International Limited

- Air Liquide S.A.

- Airgas, Inc.

- Hudson Technologies, Inc.

- National Refrigerants, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Honeywell International Inc maintains a prominent global position through continuous innovation in low global warming potential refrigerant formulations and strategic partnerships with original equipment manufacturers. The company's Solstice product portfolio delivers compliant alternatives for automotive, commercial,l and residential applications while supporting regulatory transition timelines across multiple jurisdictions. Recent initiatives include collaboration with BOSCH to integrate energy-efficient refrigerants into next-generation heat pump systems and expansion of production capacity to satisfy accelerating North American procurement demand. The organization invests substantially in research and development to advance thermodynamic performance and safety characteristics of next-generation fluids.

- The Chemours Company contributes significantly to global refrigerant markets through its Opteon brand of low-impact formulations that satisfy stringent environmental mandates while preserving system efficiency. The organization recently expanded manufacturing capacity at its Corpus Christi facility to increase the supply of hydrofluoro olefin compounds for North American customers. Strategic agreements with international chemical producers enhance raw material security and distribution reach across diverse application segments. The company prioritizes technical support and certification programs to accelerate technician adoption of next-generation refrigerants across service networks.

- Arkema sustains global market relevance through its Forane refrigerant portfolio that balances performance, compliance, and cost effectiveness across residential, commercial,l and industrial applications. The organization recently established commercial arrangements with technology leaders to broaden the availability of low global warming potential blends for the North American HVACR market. Investment in application engineering and customer training programs facilitates a smooth transition from legacy compounds to next-generation alternatives. The company emphasizes supply chain resilience and regulatory expertise to support customers navigating complex environmental compliance requirements across multiple jurisdictions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Leading participants prioritize research and development investments to advance low global warming potential formulations that satisfy regulatory mandates while preserving thermodynamic performance. Organizations establish strategic partnerships with original equipment manufacturers to integrate compliant refrigerants into next-generation cooling systems and accelerate market adoption. Companies expand production capacity and distribution networks to ensure a reliable supply of specialized compounds across diverse geographic and application segments. Market participants invest in technician training and certification programs to facilitate safe handling and proper installation of next-generation refrigerants. Organizations pursue vertical integration strategies to secure raw material access and optimize cost structures amid volatile feedstock markets.

NORTH AMERICA REFRIGERATOR MARKET NEWS

- In April 2024, Honeywell International Inc announced a collaboration with BOSCH to integrate Solstice 454B refrigerant into a new heat pump product line,s strengthening the North America Refrigerant Market presence through expanded OEM partnerships and compliant technology deployment.

- In May 2023, The Chemours Company signed a manufacturing agreement with Zhejiang Juhua Co Ltd to expand production capacity for Opteon low global warming potential fluid, strengthening the North America Refrigerant Market presence through enhanced supply security and regional distribution capabilities. ies

MARKET SEGMENTATION

This research report on the North America Refrigerants Market is segmented and sub-segmented into the following categories.

By Type

- Hydrofluorocarbons (HFCs)

- Hydrofluoro Olefins (HFOs)

- Hydrochlorofluorocarbons (HCFCs)

- Ammonia

- Carbon Dioxide

- Hydrocarbons

- Others

By Application

- Air Conditioning Systems

- Refrigeration Systems

- Mobile Air Conditioning

- Chillers

- Heat Pumps

- Others

By End User

- Residential

- Commercial

- Industrial

By Country

- United States

- Canada

- Mexico

- Rest of North America

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com