North America Scar Treatment Market Research Report – Segmented By Treatment Type (Topical treatment, Laser Treatment, Injectable Treatment, Invasive Surgical Treatment), Scar Type and Country (the United States, Canada and Rest of North America) - Industry Analysis From 2026 to 2034

North America Scar Treatment Market Size

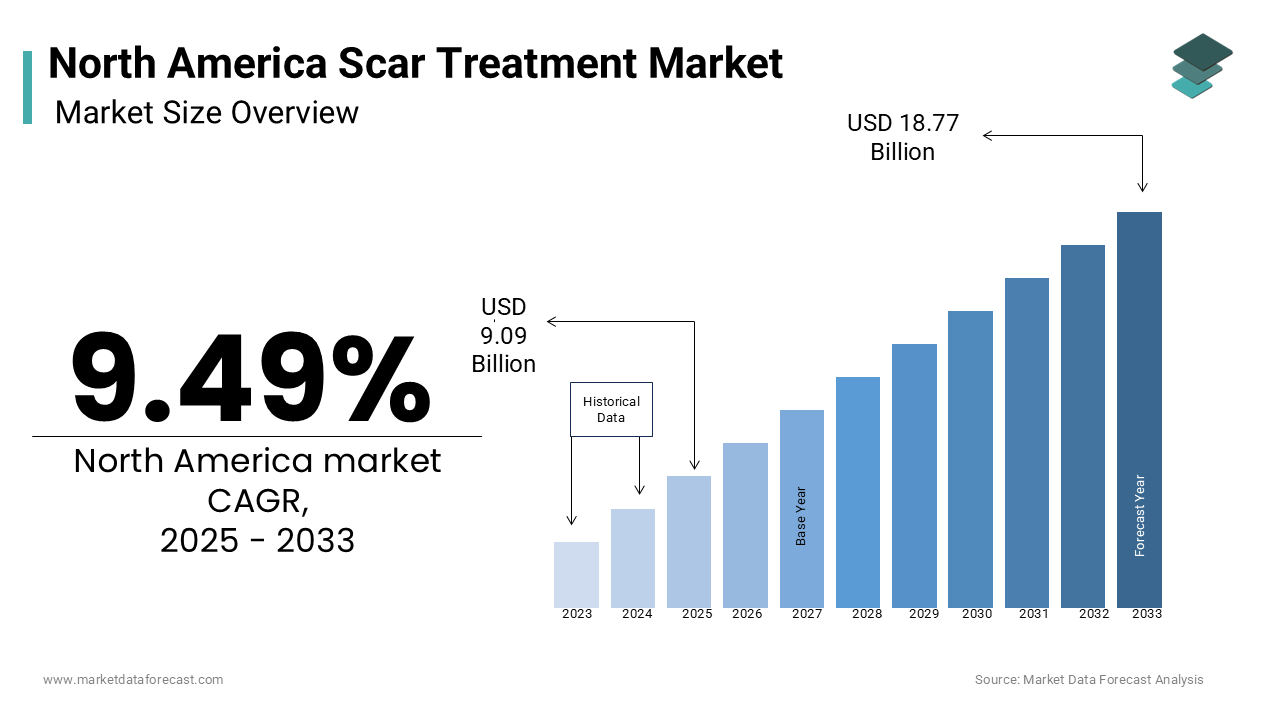

The North America scar treatment market size was valued at USD 8.30 billion in 2024 and is estimated to reach USD 18.77 billion by 2033 from USD 9.09 billion in 2025, registering a CAGR of 9.49% from 2025 to 2033.

The North America scar treatment market is driven by advancements in dermatological solutions and increasing consumer awareness about aesthetic procedures. Canada follows with a smaller but steadily growing contribution, while the Rest of North America remains an emerging segment. This growth is fueled by rising incidences of surgeries and trauma cases, which directly increase the demand for post-surgical scar management. According to the American Society of Plastic Surgeons, over 1.8 million reconstructive procedures were performed in 2021 with the need for effective scar treatments. Additionally, the prevalence of acne scars among millennials and Gen Z, as reported by the Journal of Clinical and Aesthetic Dermatology, has significantly contributed to market expansion. Rising disposable incomes and the availability of advanced treatments like laser therapy further bolster the market’s upward trajectory.

MARKET DRIVERS

Rising Prevalence of Surgical Procedures

The surge in surgical interventions across North America serves as a pivotal driver for the scar treatment market. According to the Centers for Disease Control and Prevention (CDC), approximately 51.4 million inpatient surgeries were performed annually in the U.S. alone is leading to a significant demand for post-operative scar management solutions. Elective procedures, such as cosmetic surgeries, have also gained traction, with the American Society for Aesthetic Plastic Surgery reporting over 2.3 million procedures in 2021. Moreover, advancements in minimally invasive techniques have increased patient willingness to undergo procedures is indirectly boosting the need for scar treatments. Topical treatments and gel sheets are often recommended post-surgery is contributing to their widespread adoption. The hospitals and private clinics are increasingly integrating scar management protocols into post-operative care plans to ensure better recovery outcomes.

Growing Awareness About Aesthetic Treatments

Consumer awareness regarding aesthetic enhancements has surged among younger demographics is driving demand for scar treatments. Data from the International Journal of Dermatology reveals that nearly 50 million Americans suffer from acne annually, with a substantial portion seeking treatments for resultant scars. Social media platforms and influencer marketing have played a crucial role in normalizing discussions around skin health by encouraging individuals to invest in scar reduction therapies. Non-invasive options like laser treatments and injectables are gaining popularity due to their efficacy and minimal downtime. Furthermore, the proliferation of e-commerce platforms has made scar treatment products more accessible, enabling consumers to explore a wide range of solutions.

MARKET RESTRAINTS

High Cost of Advanced Treatments

The cost barrier associated with advanced scar treatments poses a significant challenge to market accessibility. Laser treatments and invasive surgical procedures, though highly effective, often come with hefty price tags is making them unaffordable for a large segment of the population. According to a study published in the Journal of Cosmetic Dermatology, the average cost of a single laser treatment session ranges from USD 200 to USD 3,000, depending on the severity of scarring and the technology used. Additionally, injectable treatments and surgical options require multiple sessions those are further escalating costs. This financial burden limits the adoption of premium scar management solutions among lower-income groups. The disparity in affordability creates a fragmented market, where only a subset of consumers can access cutting-edge treatments. Consequently, this restricts overall market penetration and slows down growth, despite the availability of innovative technologies.

Stringent Regulatory Frameworks

Stringent regulatory requirements for scar treatment products and procedures present another major obstacle to market expansion. In North America, the Food and Drug Administration (FDA) mandates rigorous testing and approval processes for medical devices and topical formulations used in scar management. According to the Food and Drug Administration, obtaining clearance for a new scar treatment product can take anywhere from 12 to 36 months, involving extensive clinical trials and safety assessments. These prolonged timelines delay product launches and increase development costs is discouraging smaller companies from entering the market. Furthermore, compliance with evolving regulations requires continuous investment in research and development, which can strain resources for mid-sized firms. The complexity of navigating regulatory landscapes also leads to inconsistencies in product availability across regions.

MARKET OPPORTUNITIES

Expansion of Telemedicine Platforms

The integration of telemedicine into dermatology practices presents a transformative opportunity for the scar treatment market. According to McKinsey & Company, telehealth adoption in the U.S. surged by 38 times pre-pandemic levels, with dermatology being one of the most frequently accessed specialties. This shift enables practitioners to recommend tailored scar treatment regimens, including topical solutions and non-invasive therapies, directly to patients' doorsteps. E-commerce platforms further complement this trend by offering a wide array of scar management products, from gel sheets to silicone-based treatments. The companies can expand their customer base and enhance user engagement through personalized care plans. Additionally, partnerships between telehealth providers and pharmaceutical firms are likely to drive innovation is creating synergies that benefit both industries. This convergence of technology and healthcare not only broadens market reach but also improves treatment adherence and outcomes.

Development of Biologics and Regenerative Therapies

Advancements in biologics and regenerative medicine offer promising avenues for innovation in scar treatment. These therapies utilize stem cells, growth factors, and tissue engineering to promote natural healing and reduce scar formation. For instance, platelet-rich plasma (PRP) injections have gained traction for their ability to accelerate tissue repair and minimize hypertrophic scarring. According to the National Institutes of Health, ongoing clinical trials exploring the efficacy of bioengineered skin substitutes, which could revolutionize post-surgical and burn scar management. Such innovations cater to the growing demand for non-invasive, long-lasting solutions is appealing to both healthcare providers and patients. This focus on cutting-edge science not only enhances treatment efficacy but also strengthens competitive positioning within the marketplace.

MARKET CHALLENGES

Limited Insurance Coverage for Aesthetic Procedures

A significant hurdle for the scar treatment market is the lack of comprehensive insurance coverage for aesthetic and elective procedures. According to the American Medical Association, most insurance plans categorize scar treatments as cosmetic enhancements, excluding them from reimbursement policies. This classification places the financial burden entirely on patients, limiting accessibility for individuals seeking treatments for conditions like keloid or hypertrophic scars. Even post-surgical scar management, which may improve functional outcomes, often falls outside covered benefits unless deemed medically necessary. According to a report by the Kaiser Family Foundation, nearly 27 million Americans remain uninsured, further exacerbating disparities in treatment access. The absence of financial support discourages patients from pursuing advanced therapies, hindering market growth. Additionally, inconsistent guidelines across insurance providers create confusion, complicating efforts to advocate for broader coverage. Addressing this challenge requires collaboration between stakeholders to redefine policy frameworks and emphasize the therapeutic value of scar treatments.

Consumer Skepticism Toward New Products

Consumer skepticism toward novel scar treatment products represents another pressing challenge. Despite technological advancements, many individuals remain wary of adopting unfamiliar solutions due to concerns about efficacy and safety. According to a survey conducted by the Pew Research Center, approximately 60% of consumers prioritize recommendations from dermatologists or personal experiences over marketing claims when choosing scar treatments. This cautious approach slows the adoption of innovative formulations, such as bioactive gels or nanotechnology-based creams, which often lack long-term clinical data. Misinformation propagated through online forums and social media further fuels doubts, undermining trust in emerging brands. Additionally, counterfeit products flooding e-commerce platforms erode confidence in legitimate offerings. To overcome this barrier, companies must invest in robust clinical trials and transparent communication strategies. Building credibility through peer-reviewed studies and endorsements from trusted healthcare professionals can help dispel misconceptions and foster greater acceptance of cutting-edge solutions.

SEGMENTAL ANALYSIS

By Treatment Type Insights

The topical treatment segment was the largest by accounting for 40.3% of the North America scar treatment market share in 2025 due to their affordability, ease of use, and widespread availability across pharmacies and e-commerce platforms. According to the American Academy of Dermatology, over-the-counter topical creams and ointments are the first line of defense for mild to moderate scarring by making them a preferred choice for consumers. Silicone-based products, in particular, have gained traction due to their proven efficacy in reducing hypertrophic and keloid scars. The accessibility of these treatments, coupled with strong brand recognition, drives their dominance. Additionally, advancements in formulation technologies, such as the incorporation of antioxidants and peptides, enhance product appeal. Retailers and manufacturers capitalize on this demand by expanding product portfolios and leveraging digital marketing strategies to reach broader audiences. This combination of convenience, affordability, and innovation ensures that topical treatments remain the cornerstone of the scar management landscape.

Laser treatments segment is projected to gain huge traction over the growth with a CAGR of 8.5% from 2026 to 2034. The growth of the segment is fueled by increasing consumer preference for non-invasive procedures that deliver visible results with minimal downtime. The American Society for Laser Medicine and Surgery reports that laser therapies are particularly effective for acne scars and pigmentation issues, addressing a growing concern among younger demographics. Technological advancements, such as fractional CO2 lasers and pulsed dye lasers, have enhanced precision and reduced recovery periods is attracting a wider patient base. Furthermore, the proliferation of specialized dermatology clinics offering laser services has improved accessibility in urban areas. Rising disposable incomes and a growing emphasis on aesthetics also to expel the growth of the segment.

By Scar Type Insights

The post-surgical scars segment was the largest and held 35.4% of the North America scar treatment market share in 2025. According to the American College of Surgeons, millions of surgical procedures are performed annually is creating a substantial demand for scar management solutions. Patients undergoing orthopedic, cardiovascular, and cosmetic surgeries often seek treatments to minimize visible scarring and improve aesthetic outcomes. Silicone gel sheets and pressure garments are commonly prescribed for post-operative care, supported by clinical evidence demonstrating their effectiveness. The standardization of scar management protocols in hospitals and clinics further bolsters adoption. Additionally, the aging population, which is more prone to surgeries that amplifies the need for scar treatments. Rising awareness about post-surgical care and the availability of advanced products tailored to specific scar types ensure this segment's continued dominance.

Acne scars segment is likely to register a CAGR of 9.2% during the forecast period. This growth is driven by the rising prevalence of acne among adolescents and young adults, compounded by lifestyle factors such as stress and diet. The Journal of the American Academy of Dermatology estimates that over 85% of individuals aged 12-24 experience acne, with a significant proportion developing scars. Non-invasive treatments like chemical peels, microdermabrasion, and laser therapies are gaining popularity due to their ability to address various types of acne scars effectively. Social media platforms and influencer marketing play a pivotal role in shaping consumer perceptions, encouraging individuals to seek professional treatments. Moreover, the emergence of personalized skincare solutions tailored to individual scar profiles enhances treatment efficacy. Investments in research and development by key players further accelerate innovation by ensuring sustained growth in this dynamic segment.

By End-User Insights

The hospitals segment was the largest by occupying 45.3% of the North America scar treatment market share in 2025. This dominance is attributed to the high volume of surgical procedures performed in hospital settings by necessitating comprehensive scar management protocols. According to the Healthcare Cost and Utilization Project, over 15 million inpatient surgeries occur annually in the U.S. is creating a steady demand for post-operative scar treatments. Hospitals also serve as hubs for advanced treatments like laser therapy and reconstructive surgeries by attracting patients seeking specialized care. The presence of skilled dermatologists and plastic surgeons further enhances their appeal. Additionally, hospitals benefit from established supply chains and partnerships with leading manufacturers by ensuring access to cutting-edge products. Government initiatives promoting affordable healthcare and insurance coverage for medically necessary scar treatments also bolster hospital-based adoption. This combination of infrastructure, expertise, and patient trust cements hospitals as the primary end-user segment in the market.

The e-commerce segment is likely to grow with a CAGR of 10.3% from 2025 to 2033. The convenience of online shopping, coupled with an extensive product range, drives this rapid expansion. Platforms like Amazon and specialized e-pharmacies offer a variety of scar management solutions, from topical creams to silicone sheets, catering to diverse consumer needs. Millennials and Gen Z, who prioritize convenience and digital engagement, are the primary drivers of this trend. Aggressive marketing strategies, including discounts and subscription models, further enhance customer acquisition. Additionally, the COVID-19 pandemic accelerated the shift toward online shopping is establishing e-commerce as a permanent fixture in the scar treatment landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Analyzed | By Treatment Type, Scar Type, End-User & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | The U.S., Canada, Mexico, Rest of North America. |

| Key Market Players | Oculus Innovative Sciences Inc., Smith & Nephew PLC, Nutramarks Inc, Merz Inc, Enaltus LLC, CCA Industries Inc., Cynosure Inc., Syneron Medical Ltd, Mölnlycke Health Care, Avita Medical Limited, Pacific World Corporation, Shanghai Fosun Pharmaceuticals Ltd, AC. Alma Lasers, Valeant Pharmaceuticals International Inc., and Beijing Toplaser Technology Company Limited. |

REGIONAL ANALYSIS

The United States was the top performer in the North America scar treatment market with 76.5% of share in 2024 owing to a robust infrastructure, high disposable incomes, and a culture that prioritizes aesthetics. According to the American Society of Plastic Surgeons, over 18 million cosmetic procedures were performed in 2021 by reflecting the nation's enthusiasm for aesthetic enhancements. The prevalence of chronic conditions like diabetes and obesity, which often lead to surgical interventions, further amplifies demand for scar treatments. Key players leverage advanced R&D facilities and partnerships with academic institutions to introduce innovative products, maintaining the U.S.'s dominance in the global market. Additionally, favorable reimbursement policies for certain scar treatments enhance accessibility, ensuring sustained growth. The convergence of technological innovation, consumer awareness, and supportive regulatory frameworks positions the U.S. as a powerhouse in the scar treatment industry.

Canada is estimated to register a CAGR of 13.5% during the forecast period with the increasing awareness about skin health and advancements in dermatological care. According to Health Canada, the country's healthcare system emphasizes preventive measures, including scar management, to improve patient outcomes. The Canadian Dermatology Association reports a rising incidence of acne and post-surgical scars, fueling demand for effective treatments. Urban centers like Toronto and Vancouver host specialized clinics offering laser therapies and injectables, catering to a growing affluent population. Additionally, the influx of immigrants, who often bring diverse skincare practices, enhances the market growth.

COMPETITVE LANDSCAPE

The North America scar treatment market is characterized by intense competition, with key players vying for dominance through innovation and strategic initiatives. Established firms leverage their extensive resources and brand recognition to maintain its prominence, while emerging companies focus on niche segments and disruptive technologies. The market's fragmented nature encourages collaborations and partnerships, fostering a collaborative yet competitive environment. Regulatory compliance and consumer trust serve as critical differentiators, driving companies to prioritize quality and safety.

KEY MARKET PLAYERS

A few of the promising companies operating in the North America scar treatment market include

- Oculus Innovative Sciences Inc.

- Smith & Nephew PLC

- Nutramarks Inc.

- Merz Inc.

- Enaltus LLC

- CCA Industries Inc.

- Cynosure Inc.

- Syneron Medical Ltd.

- Mölnlycke Health Care

- Avita Medical Limited

- Pacific World Corporation

- Shanghai Fosun Pharmaceuticals Ltd.

- Alma Lasers

- Valeant Pharmaceuticals International Inc.

- Beijing Toplaser Technology Company Limited

Top Players in the North America Scar Treatment Market

Johnson & Johnson

Johnson & Johnson occupies a prominent position in the North America scar treatment market by leveraging its extensive portfolio of dermatological products. The company's strengths lie in its global reach, robust R&D capabilities, and strong brand equity. Its flagship scar management solutions, including silicone-based products, are widely recognized for their efficacy and safety. Johnson & Johnson's commitment to innovation is evident in its collaborations with academic institutions and healthcare providers to develop next-generation treatments. Additionally, its distribution networks ensure widespread availability across hospitals, clinics, and retail outlets.

Allergan (AbbVie)

Allergan, now part of AbbVie, is a key player in the scar treatment market, which is renowned for its expertise in aesthetic and reconstructive therapies. The company's strengths include its cutting-edge technologies, such as injectable treatments and laser devices, which cater to diverse patient needs. Allergan's focus on personalized care and patient outcomes sets it apart from competitors. Its partnerships with dermatologists and plastic surgeons enhance credibility and foster trust among consumers. Furthermore, its strategic acquisitions and investments in R&D ensure a steady pipeline of innovative solutions.

Smith & Nephew

Smith & Nephew is a leading innovator in the scar treatment space in advanced wound care and regenerative therapies. Smith & Nephew's collaborations with healthcare providers and research organizations enable it to address unmet needs in scar management effectively. Its focus on sustainability and ethical practices enhances brand loyalty and differentiates it from competitors.

Top Strategies Used by Key Market Participants

Key players in the North America scar treatment market employ a variety of strategies to maintain their competitive edge. Product innovation remains a cornerstone, with companies investing heavily in R&D to introduce advanced formulations and devices. Strategic partnerships and collaborations with healthcare providers and academic institutions enhance credibility and foster innovation. Expanding distribution networks through e-commerce platforms and retail channels ensures broader accessibility. Marketing campaigns emphasizing clinical efficacy and consumer testimonials build trust and drive adoption. Additionally, mergers and acquisitions enable companies to consolidate their market position and diversify their product portfolios. These multifaceted approaches ensure sustained growth and resilience in a dynamic market landscape.

RECENT MARKET DEVELOPMENTS

- In April 2024, Johnson & Johnson launched a new line of silicone-based scar gels is enhancing its dermatological portfolio

- In June 2023, Allergan introduced an advanced laser device for scar reduction is targeting premium clinics

- In February 2023, Smith & Nephew partnered with a biotech firm to develop regenerative scar treatments.

- In September 2022, Biodermis expanded its e-commerce platform by offering direct-to-consumer scar management solutions

- In January 2022, Medline Industries acquired a startup specializing in bioactive wound care products by strengthening its market presence.

MARKET SEGMENTATION

This research report on the North American scar treatment market has been segmented and sub-segmented into the following categories

By Treatment Type

- Topical treatment

- Creams

- Oils

- Gels

- Gel Sheets

- Surface Treatment

- Dermabrasion

- Chemical Peeling

- Cryosurgery

- Laser Treatment

- Injectable Treatment

- Tissue Fillers

- Steroid Injections

- Invasive Surgical Treatment

By Scar type

- Keloid and Hypertrophic Scars

- Contracture Scars

- Acne Scars

- Stretch Scars

- Post-Surgical Scars

By End-user

- Hospitals

- private clinics

- pharmacies & drug stores

- E-Commerce

By Country

- The United States

- Canada

- Rest of North America

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com