North America Surgical Staplers Market Research Report By Type (Linear staplers, circular staplers) Technology , Usability, Application & Country (the United States, Canada & Rest of North America) - Industry Analysis on Size, Share, Trends & Growth Forecast (2026 to 2034)

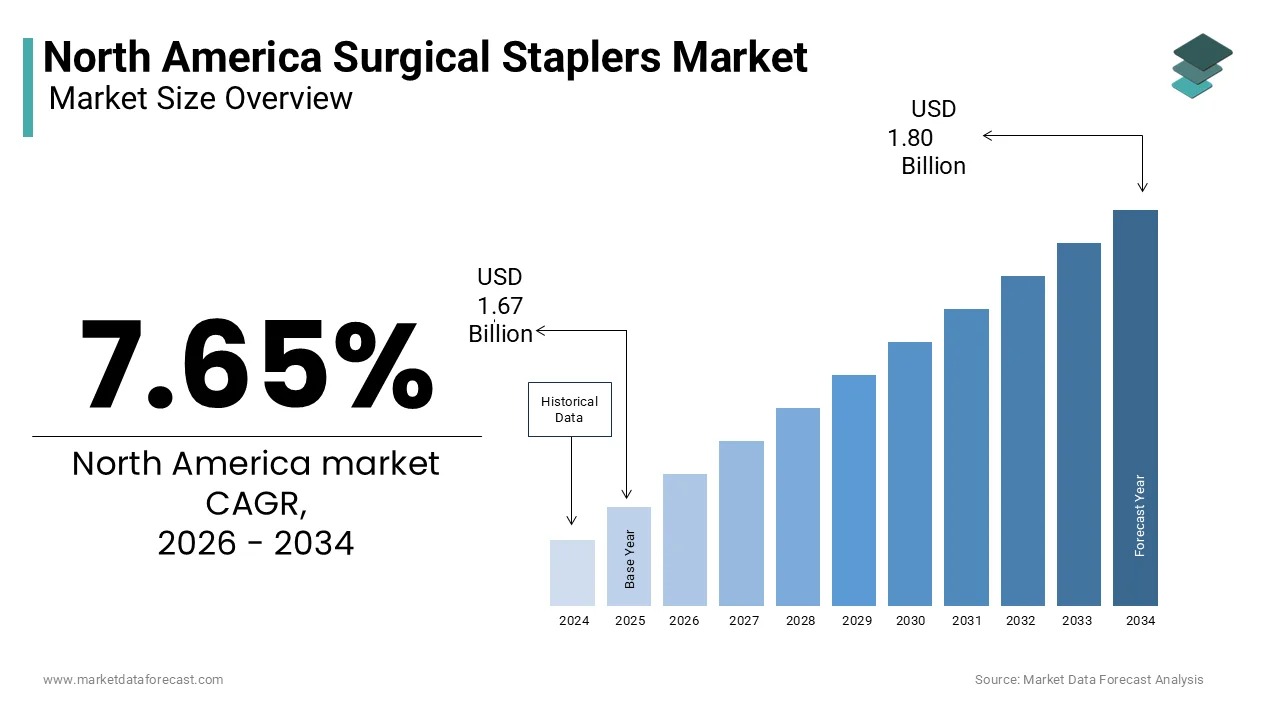

Market Size, 2025

$1.67 BnMarket Estimate, 2026

$1.80 BnMarket Forecast, 2034

$3.24 BnCAGR, 2026–2034

7.65%North America Surgical Staplers Market Size

The North America Surgical Staplers Market was valued at USD 1.67 billion in 2025, is expected to have 7.65 % CAGR from 2026 to 2034 and be worth USD 3.24 billion by 2034 from USD 1.80 billion in 2026.

The North American surgical staplers market is a robust segment within the broader healthcare industry, driven by advancements in minimally invasive surgeries and increasing demand for efficient wound closure techniques. For instance, the region accounted for over 40% of the global surgical staplers market in 2022, reflecting its prominence. The United States dominates this regional market, primarily due to the presence of advanced healthcare infrastructure, high adoption rates of cutting-edge medical technologies, and a growing prevalence of chronic diseases requiring surgical interventions. A key factor shaping the market's growth trajectory is the rising incidence of obesity-related conditions such as gastrointestinal disorders, which necessitate bariatric surgeries. According to the Centers for Disease Control and Prevention (CDC), approximately 42% of adults in the U.S. were obese in 2021, creating substantial demand for abdominal surgeries where surgical staplers are indispensable. Additionally, the aging population further fuels demand, with projections indicating that by 2030, nearly one-fifth of Americans will be aged 65 or older, as stated by the U.S. Census Bureau. This demographic shift is expected to escalate the need for orthopedic and general surgeries, propelling the market forward. Despite favorable conditions, regulatory scrutiny and pricing pressures remain challenges. However, ongoing innovations in product design and functionality continue to bolster the market’s resilience and expansion potential.

MARKET DRIVERS

Rising Adoption of Minimally Invasive Surgeries

Minimally invasive surgeries (MIS) have become a cornerstone of modern healthcare, significantly influencing the demand for surgical staplers. These devices play a pivotal role in MIS procedures by enabling precise tissue approximation and reducing recovery times. According to the American Hospital Association (AHA), over 90% of hospitals in the U.S. now offer minimally invasive options, underscoring their widespread adoption. Data from the Agency for Healthcare Research and Quality reveals that laparoscopic procedures alone accounted for more than 5 million surgeries annually in the U.S., driving significant demand for surgical staplers. The precision and reliability of surgical staplers make them indispensable tools in complex surgeries like colorectal and thoracic operations. For instance, during bariatric surgeries, circular staplers are extensively used to create anastomoses, ensuring secure and leak-proof connections. The growing preference for MIS can also be attributed to patient-centric benefits such as reduced postoperative pain and shorter hospital stays. A report published by the National Institutes of Health estimates that MIS reduces recovery time by up to 60%, making it a preferred choice among both surgeons and patients.

Increasing Prevalence of Chronic Diseases

Chronic diseases, including cardiovascular disorders and cancer, are escalating the demand for surgical interventions, thereby fueling the growth of the surgical staplers market. The American Heart Association states that cardiovascular diseases affect over 120 million Americans, often requiring surgical treatments. Similarly, the American Cancer Society reported that there were approximately 1.9 million new cancer cases diagnosed in 2022, many of which necessitate tumor resection surgeries. The surgical staplers are critical in oncological procedures, providing rapid and consistent hemostasis while minimizing damage to surrounding tissues. For example, linear staplers are frequently employed in lung cancer surgeries to achieve optimal sealing of airways. Furthermore, the prevalence of diabetes, estimated at 11.3% of the U.S. population by the CDC, correlates with complications like diabetic foot ulcers, which may require amputations using skin staplers. These statistics highlight how chronic disease prevalence acts as a catalyst for the burgeoning use of surgical staplers, reinforcing their status as essential medical devices in contemporary healthcare settings.

MARKET RESTRAINTS

High Costs and Budget Constraints

One of the most significant barriers to the growth of the North American surgical staplers market is the high cost associated with these devices. Advanced surgical staplers often come with steep price tags due to their sophisticated engineering and specialized functionalities. According to a report by the Healthcare Supply Chain Association, hospitals spend billions annually on medical devices, with surgical staplers being one of the costliest categories. Such expenditures strain hospital budgets, particularly in smaller facilities or rural areas where financial resources are limited. Additionally, reimbursement policies for surgeries involving staplers vary widely, and in some cases, they fail to cover the full cost of the procedure. A study referenced by the American Medical Association highlights that inconsistent insurance coverage discourages healthcare providers from adopting premium-priced staplers. For instance, Medicare reimbursement rates for certain surgeries using disposable staplers are often insufficient to offset procurement costs, leading to reluctance among providers to invest in newer models. These economic factors hinder the widespread adoption of advanced staplers despite their clinical advantages, creating a restraint on market growth.

Stringent Regulatory Standards

Stringent regulatory requirements imposed by agencies like the U.S. Food and Drug Administration (FDA) pose another challenge to the surgical staplers market. Manufacturers must comply with rigorous testing protocols and obtain premarket approvals before launching new products. The FDA reports that approval timelines for Class II medical devices, including surgical staplers, can extend up to two years, delaying market entry and increasing development costs. Furthermore, recent recalls of defective staplers have heightened scrutiny. For example, in 2021, the FDA issued warnings about malfunctions in certain powered staplers, citing instances of misfires and tissue damage. Such incidents not only tarnish brand reputations but also intensify regulatory oversight, compelling manufacturers to allocate additional resources toward compliance. These stringent measures act as a deterrent to innovation and slow down the introduction of next-generation staplers, impeding overall market progress.

MARKET OPPORTUNITIES

Technological Innovations Enhancing Efficiency

Technological advancements are opening new avenues for growth in the North American surgical staplers market. Manufacturers are increasingly focusing on integrating smart features into staplers, such as real-time feedback systems and automated adjustments, to improve surgical outcomes. According to a publication by the Journal of Medical Devices, next-generation powered staplers equipped with sensors can monitor tissue thickness and adjust staple height accordingly,s reducing complications like leaks or tears. The adoption of IoT-enabled staplers is also gaining traction, allowing surgeons to track device performance during procedures. A report by McKinsey & Company suggests that connected medical devices could enhance operational efficiency by up to 30%, driving demand for technologically advanced staplers. Additionally, innovations in biocompatible materials are expanding usability, with bioabsorbable staples offering improved healing properties. These advancements align with the growing emphasis on precision medicine, which is presenting lucrative opportunities for companies willing to invest in R&D.

Expanding Applications in Emerging Therapies

The expanding scope of surgical staplers beyond traditional applications presents another promising opportunity. With the rise of organ transplantation and reconstructive surgeries, staplers are being adapted for novel uses. The United Network for Organ Sharing (UNOS) reports that over 40,000 organ transplants were performed in the U.S. in 2022, with the need for reliable tools like circular staplers to ensure vascular anastomosis. Moreover, the growing field of robotic-assisted surgery offers untapped potential. As per data from the International Federation of Robotics, the number of robotic surgical systems installed in North America grew by 25% between 2020 and 2022. Surgical staplers compatible with robotic platforms enable greater precision and control, fostering collaboration between device manufacturers and robotics firms. These emerging therapies and technological synergies expand the vast untapped potential within the market.

MARKET CHALLENGES

Intense Market Competition and Price Wars

The North American surgical staplers market faces stiff competition among key players, leading to aggressive pricing strategies that impact profitability. Major companies like Medtronic, Johnson & Johnson, and Ethicon dominate the landscape, but smaller firms are increasingly entering the fray, intensifying rivalry. According to a competitive analysis by Deloitte, price wars have become commonplace, with discounts ranging from 10% to 20% offered to secure contracts with large hospital networks. This environment creates challenges for manufacturers striving to balance affordability with innovation. Smaller players often struggle to compete with established brands, limiting their ability to scale operations. Furthermore, consolidation among healthcare providers has resulted in bulk purchasing agreements that favor low-cost suppliers, which are squeezing profit margins. These dynamics hinder long-term investments in research and development by posing a challenge to sustained market growth.

Resistance to Change Among Practitioners

Another obstacle is the resistance to adopting new technologies among some healthcare practitioners. Despite the availability of advanced staplers, many surgeons prefer traditional suturing methods due to familiarity and perceived reliability. A survey conducted by the American College of Surgeons found that nearly 30% of respondents expressed hesitation in switching to newer stapler models without extensive training. Training programs for innovative devices are often inadequate or underfunded, exacerbating this issue. Moreover, concerns about device malfunctions persist, as highlighted by the FDA's recall database, which documents user-reported errors. Overcoming practitioner skepticism requires targeted educational initiatives and robust post-market support, which remains a persistent challenge for market players aiming to drive adoption of cutting-edge solutions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Technology, Usability, Application, and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | The U.S., Can,ada the restRest of North America |

| Market Leader Profiled | Ethicon Inc., Medtronic plc, CONMED Corporation, Smith & Nephew, Purple Surgical Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The disposable stapler segment held the majority share of the North American surgical staplers market in 2025. This dominance of the segment is mainly driven by the stringent infection control protocols mandated across the United States and Canada, where preventing surgical site infections is a top priority for hospital accreditation and reimbursement. Apart from these, the leading factor is the unequivocal shift toward single-use devices to eliminate the risk of cross-contamination and the high costs associated with reprocessing complex instruments. According to the Centers for Disease Control and Prevention, surgical site infections remain a costly challenge for the US healthcare system. However, rather than mandating disposable devices, guidelines emphasize comprehensive sterile protocols, which have led facilities to weigh the convenience of pre-sterilized single-use items against the environmental benefits of reusables. Furthermore, the intricate design of modern articulating and powered staplers makes effective cleaning and sterilization technically challenging and economically unviable compared to the cost of a new unit. Updates to standards by the Association for the Advancement of Medical Instrumentation (AAMI) have introduced more rigorous validation requirements for cleaning and sterilization processes, contributing to an increase in the operational overhead required to maintain complex reusable medical devices. The operational efficiency gained by eliminating reprocessing time also reduces operating room turnover, a crucial metric for high-volume centers. This combination of patient safety imperatives, regulatory compliance, and logistical convenience solidifies the disposable segment as the undisputed market leader.

The reusable stapler segment is likely to experience the fastest CAGR of 3.2% from 2026 to 2034 due to sustainability initiatives and budget constraints within certain public health systems and rural clinics that seek to reduce medical waste and lower procurement costs. In addition, the main driver is the increasing environmental awareness among healthcare administrators who are under pressure to minimize the carbon footprint of surgical operations. The Practice Greenhealth organization reports that North American hospitals are increasingly implementing "Green Surgery" initiatives to reduce regulated medical waste, driving a renewed interest in durable, reusable stainless steel instruments, such as skin staplers, for routine and low-risk applications. Economic assessments by major health networks indicate that adopting high-quality reusable stapling systems can yield substantial lifecycle savings compared to the cumulative expense of single-use models, providing a financially viable alternative for budget-conscious facilities. Additionally, advancements in automated cleaning and inspection technologies have improved the reliability and safety profile of reprocessed instruments, addressing previous concerns about device integrity. This economic and environmental pragmatism ensures that the reusable segment maintains a steady, albeit smaller, growth trajectory in specific niches where cost containment and sustainability are paramount.

By Product Insights

The manual surgical stapler segment led the North American surgical staplers market and accounted for a 65.8% share in 2025. This leading position of the segment is attributed to the extensive installed base of surgeons proficient in manual techniques and the significantly lower acquisition cost compared to powered alternatives. A key driving factor is the versatility and reliability of manual devices, which do not require batteries, charging infrastructure, or complex maintenance, making them ideal for a wide range of procedures from emergency trauma to routine general surgery. According to the American College of Surgeons, manual staplers remain the standard of care for many open surgical procedures and are widely used in community hospitals where capital expenditure for powered systems is limited. The simplicity of manual devices allows for rapid deployment in critical situations where time is of the essence, and their mechanical nature ensures functionality even in environments with power instability. As per data from hospital procurement records, the unit price of a manual stapler is often less than half that of a powered counterpart, making them the preferred choice for high-volume, cost-sensitive applications. Furthermore, the clinical efficacy of manual staplers for standard resections and anastomoses is well documented, reducing the perceived necessity for upgrading to powered systems for every case. This blend of affordability, reliability, and established clinical practice ensures that manual staplers remain the workhorse of the North American surgical landscape.

The powered surgical stapler segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 9.8% over the forecast period due to the widespread adoption of robotic-assisted surgery and the increasing demand for ergonomic solutions that reduce surgeon fatigue during lengthy minimally invasive procedures. The primary driver is the superior performance of powered devices, which offer consistent firing speeds, adaptive tissue compression, and the ability to fire through thick tissue loads with greater precision than manual models. According to clinical studies published in the Annals of Surgery, the use of powered staplers in complex colorectal and bariatric surgeries has been associated with a reduction in staple line failures and operative time compared to manual counterparts. As per sources, the integration of powered staplers with robotic platforms like the da Vinci system is becoming standard practice, creating a dedicated and expanding demand stream. The growing number of ambulatory surgical centers performing advanced laparoscopic procedures also favors powered technology due to its ease of use and consistency. Additionally, manufacturers are introducing next-generation battery-free motorized systems that reduce long-term operational costs, making them more accessible to a broader range of facilities. This convergence of technological superiority, procedural complexity, and the rise of robotics positions powered staplers as the most dynamic growth engine in the product segmentation.

By End User Insights

The hospitals segment was the largest segment in the North America surgical staplers market and occupied a substantial share in 2025. This prominence of the segment is credited to the fact that the vast majority of complex surgical procedures requiring stapling, such as oncological resections, major trauma repairs, and complex bariatric surgeries, are performed in inpatient settings equipped with full operating theaters and intensive care units. The concentration of surgical volume in large academic and community hospitals, which function as the region's main hubs for secondary and tertiary care, is the primary driver. According to the American Hospital Association, US hospitals perform millions of inpatient surgeries annually, with a significant portion involving the use of multiple stapler loads per procedure. Hospitals also possess the financial capacity and established procurement frameworks to purchase bulk quantities of staplers and manage the diverse inventory required for various surgical specialties. As per sources, the trend toward centralizing complex surgical services in large hospital systems further consolidates demand within this segment. The presence of specialized surgical departments and multidisciplinary teams ensures a consistent and high-volume utilization of stapling devices. Furthermore, government reimbursement policies and insurance coverage for inpatient procedures provide a stable revenue stream that supports the continuous acquisition of advanced stapling technologies. This centralization of care and resources ensures that hospitals will remain the primary revenue generator for the surgical staplers market.

The Ambulatory Surgical Centers (ASCs) segment is expected to exhibit a noteworthy CAGR of 11.5% between 2026 and 2034. This swift expansion of the segment is attributed to a strategic shift toward outpatient care models in North America, aimed at reducing healthcare costs and improving patient convenience for elective procedures. This expansion is primarily fueled by the migration of minimally invasive surgeries, including select bariatric and laparoscopic procedures, from inpatient settings to ASCs. According to the Medicare Payment Advisory Commission, the number of procedures performed in ASCs has grown by over 30 percent in the last decade, with projections indicating continued acceleration as reimbursement policies increasingly favor outpatient care. These centers prioritize efficiency, speed, and rapid patient turnover, creating a strong demand for single-use, ready-to-load staplers that minimize setup time and eliminate the need for complex sterilization processes. As per the Ambulatory Surgery Center Association, hundreds of new ASC facilities are opening annually, each requiring a steady supply of high-quality stapling devices. The focus on same-day discharge necessitates devices that ensure reliable hemostasis and minimal complications, driving the adoption of premium powered staplers that reduce operative time. This structural transformation in healthcare delivery creates a vibrant new channel for stapler manufacturers, offering high growth potential as the volume of outpatient surgeries continues to climb.

COUNTRY LEVEL ANALYSIS

United States Surgical Staplers Market Analysis

The United States dominated the North American surgical staplers market and accounted for a 85.1% share in 2025. This growth of the US market is driven by its massive healthcare infrastructure, high prevalence of chronic diseases, and early adoption of advanced surgical technologies. The market is also propelled by high demand for manual and powered staplers, fueled by a robust network of academic medical centers, private hospitals, and thriving ambulatory surgical centers. The main driving factor is the high incidence of obesity and cancer, which fuels a significant volume of bariatric and oncological surgeries requiring precise stapling devices. According to the Centers for Disease Control and Prevention, between 40 million and 50 million inpatient surgical procedures are performed annually in the US, creating a foundational demand for closure technologies. The country also leads globally in the adoption of robotic-assisted surgery, with thousands of da Vinci systems installed, directly boosting the consumption of compatible powered staplers. As per data from the Food and Drug Administration, the US regulatory environment fosters innovation while ensuring safety, encouraging manufacturers to launch their latest products here first. The presence of major global medtech headquarters and a sophisticated supply chain further solidifies its position. This combination of demographic scale, technological leadership, and clinical volume ensures the United States remains the most lucrative and influential market for surgical staplers in the region.

Canada Surgical Staplers Market Analysis

Canada holds a notable position in the North American surgical staplers market and occupied a share of 12.8% in 2025. This position of the Canadian market is attributed to its universally funded healthcare system, rigorous safety standards, and steady adoption of minimally invasive techniques. The market status here is defined by a centralized procurement model where provincial health authorities negotiate contracts, often prioritizing cost-effectiveness alongside clinical efficacy. One of the driving factors is the aging population, which correlates with a higher incidence of gastrointestinal cancers and degenerative conditions requiring surgical intervention. According to Statistics Canada, the proportion of seniors in the population is projected to reach a significant level by 2030, driving sustained demand for surgical services. The Canadian healthcare system places a strong emphasis on reducing wait times and improving patient outcomes, leading to increased investment in advanced surgical equipment, including powered staplers. As per reports from Health Canada, the regulatory framework is stringent, ensuring that only high-quality devices enter the market, which fosters trust in premium brands. The growing network of ambulatory surgical centers in provinces like Ontario and Quebec is also contributing to market expansion by shifting elective procedures to outpatient settings. The Canadian market for surgical staplers is smaller than its southern neighbor. However, its stable funding and commitment to high standards of care make it a critical, reliable part of North America.

Top Players in the Market

Medtronic

Medtronic stands as a global pioneer in the surgical staplers market, renowned for its innovative product portfolio tailored to meet diverse clinical needs. The company’s powered staplers, integrated with advanced sensors and feedback mechanisms, set industry benchmarks for precision and reliability. Medtronic’s strong distribution network ensures widespread accessibility across North America, catering to both urban hospitals and rural clinics.

Ethicon (Johnson & Johnson)

Ethicon, a subsidiary of Johnson & Johnson, commands a formidable presence in the surgical staplers market through its focus on quality and usability. The company specializes in circular and linear staplers designed for complex procedures like colorectal surgeries. Ethicon’s commitment to sustainability is evident in its biocompatible materials, which enhance patient outcomes. Collaborations with academic institutions for training programs have strengthened surgeons' confidence in adopting their products.

Becton, Dickinson and Company (BD)

Becton, Dickinson, and Company excels in offering cost-effective yet high-performing surgical staplers, making it a preferred choice for budget-conscious facilities. BD’s emphasis on ergonomic design and modular reloadable cartridges enhances operational efficiency during surgeries. The company’s strategic acquisitions have expanded its product line, enabling it to cater to niche applications such as thoracic surgeries. BD continues to reinforce its competitive edge in the market with a robust pipeline of innovations.

Top strategies used by the key market participants

Key players in the North America surgical staples market employ a mix of organic and inorganic strategies to maintain their dominant positions. These include product innovation, strategic partnerships, and mergers and acquisitions. For instance, Medtronic focuses heavily on R&D, launching technologically advanced staplers equipped with IoT capabilities to enhance precision. Ethicon leverages collaborations with training institutions to promote awareness about its products among surgeons. Meanwhile, BD prioritizes cost optimization by streamlining manufacturing processes while maintaining high-quality standards. Penetration pricing strategies are another common tactic, particularly in emerging markets within North America, ensuring affordability without compromising performance. Joint ventures with robotics firms also enable companies to integrate staplers into automated surgical systems, fostering synergies across technologies.

COMPETITIVE LANDSCAPE

The North American surgical staplers market is characterized by intense competition among established players striving to innovate and capture greater market share. Leading firms like Medtronic, Ethicon, and BD continuously invest in R&D to introduce cutting-edge products that address unmet clinical needs. This competitive landscape is further shaped by collaborations between manufacturers and healthcare providers to develop customized solutions. Technological advancements, such as AI-enabled staplers and compatibility with robotic platforms, serve as key differentiators. Smaller players also contribute to market dynamism by targeting underserved segments with affordable alternatives. Regulatory compliance and stringent quality controls add layers of complexity, compelling companies to prioritize safety alongside innovation. Overall, the market reflects a balance of consolidation and fragmentation, with ample opportunities for growth amid evolving healthcare demands.

KEY MARKET PLAYERS

A few of the noteworthy companies operating in the North America surgical staplers market profiled in the report are

- Ethicon Inc.

- Medtronic plc

- CONMED Corporation

- Smith & Nephew

- Purple Surgical Inc.

- Intuitive Surgical Inc.

- Welfare Medical Ltd.

- Reach Surgical Inc.

- Merril Life Science Pvt. Ltd.

- Grena Ltd.

- B. Braun Melsungen AG

- Dextera Surgical Inc.

- Frankenman International

- Becton Dickinson

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Medtronic launched Signia™ Powered Stapling System, featuring adaptive firing technology to improve tissue compression accuracy,and ity is strengthening its dominance in powered staplers.

- In June 2023, Ethicon introduced Echelon™ Circular Stapler with Gripping Surface Technology, enhancing hemostasis during colorectal surgeries by reinforcing its expertise in complex procedures.

- In September 2023, BD acquired Staple Innovations Inc., expanding its portfolio of reusable staplers and addressing sustainability trends in healthcare.

- In November 2023, Medtronic partnered with Intuitive Surgical to integrate its staplers with da Vinci robotic systems, boosting compatibility and market reach.

- In February 2024, Ethicon collaborated with Mayo Clinic to conduct training workshops on advanced stapling techniques, whichares increasing surgeon confidence and adoption rates.

MARKET SEGMENTATION

This research report on the North America surgical staplers market has been segmented and sub-segmented into the following.

By Type

- Linear staplers

- circular staplers

By Technology

- manual staplers

- powered staplers

By Usability

- Disposable staplers

- reusable staplers

By Application

- abdominal and pelvic surgeries

- orthopedic surgeries segment

By Country

- The U.S.

- Canada

- Rest of North America.

Frequently Asked Questions

What are the major types of surgical staplers available in north america surgical staplers market?

The market primarily includes manual and powered surgical staplers. They can further be classified into disposable and reusable staplers.

What are the latest technological advancements in surgical staplers market in north america ?

Recent innovations include robotic-assisted staplers, smart staplers with real-time feedback, bioabsorbable staplers, and advanced ergonomic designs for better precision.

What is the market outlook for the North America Surgical Staplers Market?

The market is expected to grow steadily, driven by technological advancements, increasing surgical volumes, and the adoption of minimally invasive procedures.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com