North America Tuna Market Size, Share, Trends & Growth Forecast Report By Species (Skipjack Tuna, Albacore Tuna), Product Type, And Country (US, Canada, And Rest Of North America), Industry Analysis From 2025 To 2033

North America Tuna Market Size

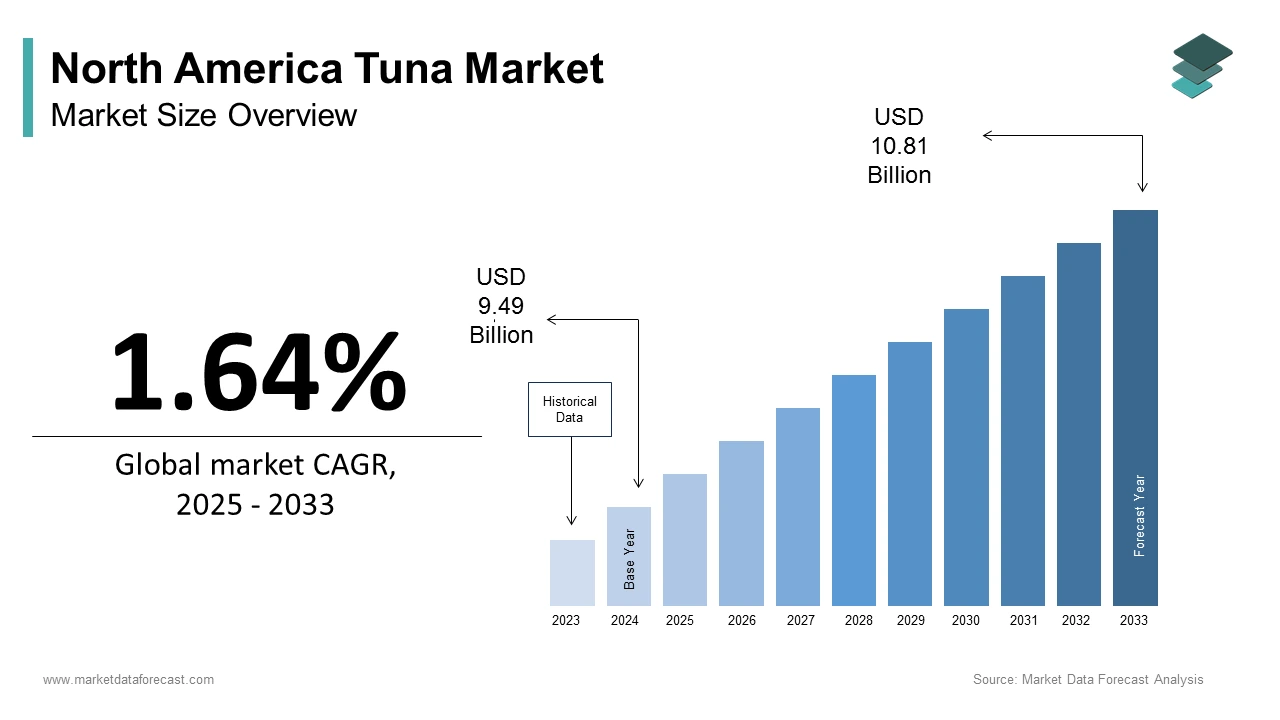

The North America Tuna Market Size was calculated to be USD 9.34 billion in 2024 and is anticipated to be worth USD 10.81 billion by 2033, from USD 9.49 billion in 2025, growing at a CAGR of 1.64% during the forecast period.

Tuna, a staple in both fresh and canned seafood products, plays a crucial role in regional diets due to its high protein content, omega-3 fatty acids, and versatility in culinary applications. In the U.S., canned light tuna remains the most widely consumed form, largely used in sandwiches, salads, and school meal programs. Also, domestic pole-and-line and purse-seine fleets contribute significantly to fresh and frozen tuna supply, especially along the West Coast. Meanwhile, Canada imports a substantial volume of canned and fresh tuna from Southeast Asia and Latin America to meet retail and foodservice demand. Mexico’s tuna industry is centered on coastal fisheries and small-scale canning operations, primarily utilizing skipjack and yellowfin species.

MARKET DRIVERS

Increasing Demand for Canned Tuna in Everyday Diets

The widespread incorporation of canned tuna into daily meals, especially among budget-conscious consumers and families, is one of the primary drivers of the North America tuna market. Canned tuna offers an affordable, shelf-stable source of high-quality protein and essential nutrients like omega-3 fatty acids, making it a pantry staple in many households.

This consistent demand is further supported by its use in institutional settings such as schools, military bases, and food assistance programs. The U.S. Department of Agriculture (USDA) includes canned tuna in its National School Lunch Program due to its nutritional profile and cost-effectiveness. Additionally, rising interest in plant-based alternatives has not diminished tuna’s relevance; instead, it has prompted innovation in premium and sustainably sourced canned products.

Retailers like Bumble Bee Foods and Chicken of the Sea have capitalized on this trend by introducing low-sodium, dolphin-safe, and MSC-certified options. These efforts resonate with environmentally aware consumers while maintaining accessibility for price-sensitive demographics, ensuring sustained growth in the canned tuna segment.

Expansion of Sustainable Fishing Practices and Eco-Certifications

The growing emphasis on sustainable fishing practices and eco-certifications, which are reshaping consumer purchasing behavior and regulatory frameworks, is a critical factor driving the North America tuna market. Over the past decade, organizations such as the Marine Stewardship Council (MSC) and the International Seafood Sustainability Foundation (ISSF) have played pivotal roles in certifying responsible tuna fisheries.

North American consumers are increasingly seeking transparency in seafood sourcing, prompting major retailers and brands to adopt these certifications. This shift is also evident in procurement policies adopted by large foodservice chains, including Subway and Panera Bread, which now highlight sustainable tuna sourcing in marketing campaigns.

Moreover, advancements in electronic monitoring systems aboard fishing vessels have improved traceability, reducing illegal, unreported, and unregulated (IUU) fishing. These developments not only enhance brand credibility but also align with international trade regulations, ensuring long-term market stability and consumer trust in North America’s tuna supply chain.

MARKET RESTRAINTS

Depletion of Wild Tuna Stocks and Regulatory Restrictions

The depletion of certain wild tuna stocks due to overfishing and inadequate stock management in international waters is a major restraint affecting the North America tuna market. Species such as bluefin tuna, once abundant in the Atlantic and Pacific Oceans, have seen significant population declines.

Regulatory bodies have responded with stricter catch limits and seasonal closures. In 2023, NOAA implemented new restrictions on bluefin tuna landings in the U.S. Atlantic and Pacific coasts, limiting commercial and recreational catches to protect spawning populations. These measures, while ecologically necessary, reduce short-term supply availability and drive up prices for high-value tuna cuts used in sushi and gourmet dining.

Additionally, enforcement challenges persist in offshore fisheries, where illegal, unreported, and unregulated (IUU) fishing undermines conservation efforts. These constraints complicate supply chain stability and raise concerns about long-term resource availability.

Rising Production and Import Costs

The increasing cost of production and importation, which affects both domestic fisheries and overseas suppliers, is another significant constraint on the North America tuna market. Fuel prices, vessel maintenance, labor expenses, and compliance with new environmental regulations have all contributed to higher operational costs for fishing companies.

Imported tuna, which constitutes a large portion of the U.S. and Canadian markets, has also become more expensive due to inflationary pressures and currency fluctuations. With rising freight costs and port congestion issues post-pandemic, landed costs have increased, leading to higher retail prices.

These financial pressures affect consumer affordability, particularly among lower-income households who rely on tuna as a budget-friendly protein. Retailers and manufacturers must balance cost management with maintaining product quality and sustainability standards, adding complexity to market expansion strategies.

MARKET OPPORTUNITIES

Growth of Premium and Value-Added Tuna Products

The development and expansion of premium and value-added tuna products tailored to evolving consumer preferences is an emerging opportunity within the North America tuna market. As demand for convenience, nutrition, and gourmet experiences rises, manufacturers are introducing pre-seasoned fillets, vacuum-packed sashimi-grade cuts, and ready-to-eat tuna bowls that cater to urban professionals and health-conscious shoppers.

Brands like Safe Catch and Wild Planet have gained traction by offering mercury-tested, sustainably sourced, and minimally processed tuna varieties that appeal to premium grocery segments and specialty stores.

Furthermore, upscale restaurants and fast-casual eateries are incorporating high-quality tuna into signature dishes, boosting demand for premium frozen and fresh cuts. Companies are leveraging blockchain-based traceability and digital labeling to provide consumers with detailed information about sourcing, handling, and sustainability credentials.

This shift toward premiumization allows producers to command higher price points while differentiating themselves in a competitive market.

Expansion of E-commerce and Direct-to-Consumer Sales Channels

The digital transformation of seafood retail presents a significant opportunity for the North America tuna market through the expansion of e-commerce and direct-to-consumer (DTC) platforms. Online seafood delivery services have gained momentum, particularly post-pandemic, as consumers seek fresher, traceable, and ethically sourced food options delivered directly to their homes.

Companies like Seattle Fish Co., Vital Choice, and Local Catch have capitalized on this trend by offering subscription-based models, same-day delivery, and blockchain-enabled traceability features that provide detailed information on catch location, processing date, and sustainability credentials.

Canada has also seen similar growth, with platforms like Hooked Inc. expanding their tuna offerings through nationwide shipping and smart packaging solutions that maintain product integrity during transit.

These developments enable producers and distributors to bypass traditional intermediaries, thereby improving profit margins while delivering fresher products.

MARKET CHALLENGES

Climate Change and Its Impact on Tuna Migration Patterns

The impact of climate change on tuna migration patterns and fishery yields is one of the foremost challenges confronting the North America tuna market. Rising ocean temperatures are altering the distribution of key tuna species, disrupting traditional fishing zones, and affecting breeding cycles. According to the National Marine Fisheries Service, warmer sea surface temperatures have led to shifts in skipjack and yellowfin tuna populations, pushing them farther north than historically recorded ranges.

These changes pose logistical and economic challenges for domestic fisheries, particularly those off the coasts of California and Oregon, where fleet operators must travel greater distances to reach viable catch areas. Increased fuel consumption and longer voyages raise operational costs, reducing profitability for smaller fishing enterprises.

Moreover, unpredictable El Niño events exacerbate volatility in tuna abundance. Such climatic disruptions threaten long-term supply consistency and require adaptive management strategies to mitigate risks.

Intensifying Competition from Alternative Protein Sources

The North America tuna market faces intensifying competition from alternative protein sources, including plant-based seafood substitutes, lab-grown fish, and insect-based protein products. As consumers become more conscious of sustainability, ethical sourcing, and dietary flexibility, these alternatives are capturing a growing share of the protein market.

Brands such as Good Catch and Sophie’s Kitchen are positioning themselves as sustainable, cruelty-free alternatives to conventional tuna, appealing to flexitarian and vegan demographics.

Simultaneously, cellular agriculture is advancing rapidly. Companies like BlueNalu and Wildtype have successfully developed lab-grown tuna prototypes and are working toward commercial approval. While still in early stages, cell-cultured seafood could disrupt traditional markets once production scales and costs decrease.

This diversification of protein choices poses a strategic challenge for the tuna industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 1.64% |

| Segments Covered | By Species, Product Type And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Us, Canada, and the Rest of North America |

| Market Leaders Profiled | Bumble Bee Foods, StarKist Co., Chicken of the Sea, Crown Prince Inc., Wild Planet Foods, American Tuna, Genova Seafood, Safe Catch, Ocean Naturals, Trader Joe’s, Whole Foods Market, Costco Wholesale Corporation, Walmart Inc. |

SEGMENTAL ANALYSIS

By Species Insights

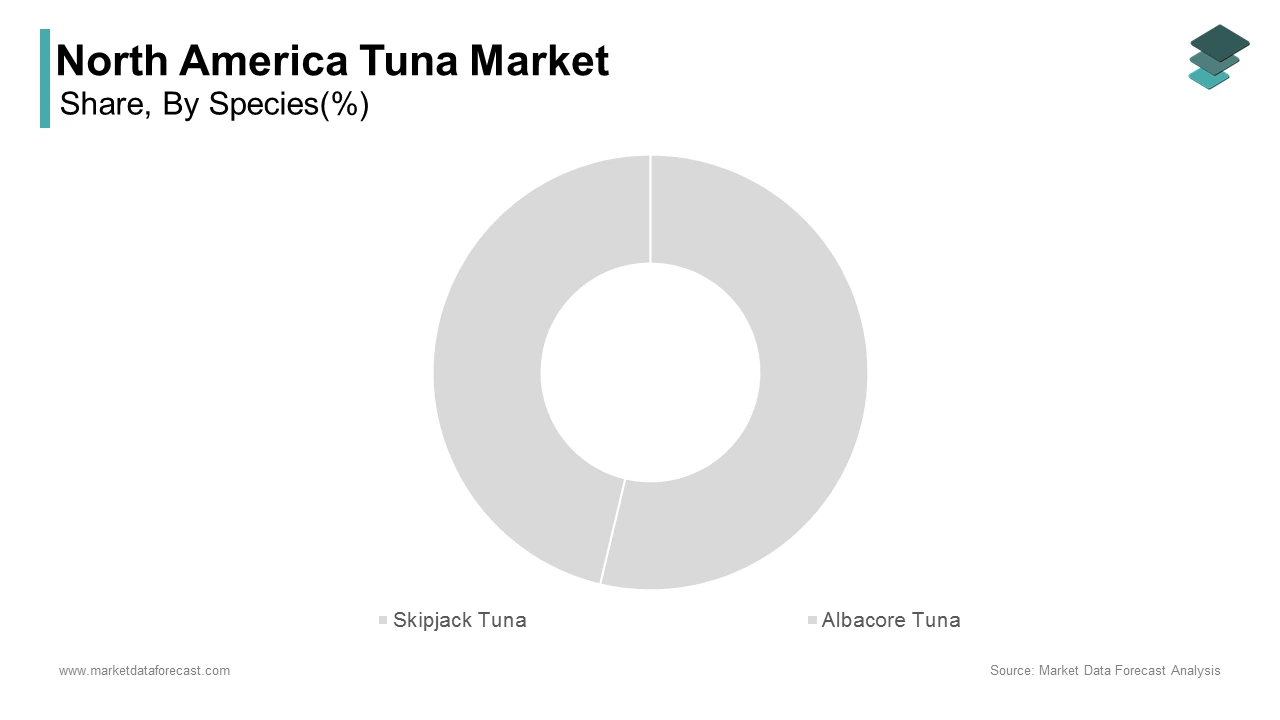

The skipjack tuna segment was the dominant species in the North America tuna market by accounting for a 40.5% of total consumption volume in 2024. The dominance of this segment is primarily attributed to its widespread use in canned tuna products, which form the backbone of retail and institutional seafood consumption across the region. The affordability and mild flavor profile of skipjack make it ideal for mass-market applications, particularly in school meal programs, military rations, and everyday household cooking. Moreover, skipjack populations remain relatively stable compared to other tuna species, allowing for sustained fishing efforts without severe regulatory restrictions. Retail giants like Bumble Bee Foods and Chicken of the Sea have leveraged this availability to maintain consistent product lines while promoting dolphin-safe certifications. These factors reinforce skipjack tuna’s stronghold on the North America tuna market.

The albacore tuna segment is emerging as the fastest-growing species in the North America tuna market and is projected to grow at a CAGR of 6.5% during the forecast period. Known for its white meat and higher omega-3 content, albacore is increasingly favored by health-conscious consumers and premium food brands. The United States leads in albacore consumption, with the majority sourced from troll- or pole-caught fisheries off the West Coast, particularly in Oregon and Washington. Retail demand has surged accordingly. Its association with heart health and clean labeling appeals to organic and gourmet food shoppers. Additionally, growing export interest from Europe and Asia is encouraging higher value-added processing in North America, further boosting the segment’s momentum.

By Product Type Insights

The canned tuna segment accounted for the largest share of the North America tuna market 65.2% of total volume in 2024. The superiority of this segment is primarily driven by its affordability, long shelf life, and versatility in everyday meals ranging from sandwiches to casseroles. Like, canned tuna remains one of the top three seafood choices among U.S. consumers , with over 90% of households purchasing it annually. The product is widely used in institutional settings such as schools, hospitals, and military bases due to its cost-effectiveness and nutritional benefits. Technological advancements in canning and retorting processes have also improved texture retention and flavor consistency. Major retailers like Walmart, Kroger, and Costco continue to expand their private-label canned tuna offerings, often highlighting sustainability credentials through eco-certifications. These factors collectively cement canned tuna’s position as the leading product type in the North America market.

The fresh tuna segment is the fastest-growing segment in the North America tuna market and is projected to grow at a CAGR of 7.2% between 2025 and 2033. This surge reflects shifting consumer preferences toward minimally processed, high-quality proteins, especially among urban and affluent demographics. The proliferation of premium seafood counters in upscale grocery stores and specialty fish markets has been instrumental in driving fresh tuna consumption. Furthermore, the rise of direct-to-consumer seafood delivery platforms, such as Hooked Inc. and Seattle Fish Co., has made fresh tuna more accessible nationwide. These services offer same-day or next-day delivery with temperature-controlled packaging, ensuring freshness even in inland regions. Restaurants, particularly those specializing in sushi, fine dining, and farm-to-table concepts, also contribute significantly to this trend. With consumers prioritizing transparency and quality, fresh tuna continues to gain momentum as a premium protein option.

REGIONAL ANALYSIS

United States Tuna Market Insights

The United States led the North America tuna industry by accounting for a 76.4% of regional consumption. It serves as the primary importer and consumer of both canned and fresh tuna, driven by strong domestic demand and an expansive foodservice sector. Tuna consumption in the U.S. has steadily risen due to growing awareness of its health benefits, particularly omega-3 fatty acids. The country also leads in innovation and retail expansion, with major supermarket chains investing heavily in premium and sustainable seafood lines. Despite significant West Coast albacore production, the U.S. relies heavily on imports, primarily from Ecuador, Thailand, and Indonesia.

Canada Tuna Market Insights

Canada plays a crucial role as a key importer and retailer of both canned and fresh tuna products. Canadian consumers rely heavily on imported tuna. Canned tuna dominates retail shelves, particularly in large supermarket chains such as Loblaws and Sobeys, where it is marketed under private label and branded formats. Urban centers like Toronto, Vancouver, and Montreal are driving growth in premium tuna consumption, particularly among Asian-inspired cuisine enthusiasts and health-focused consumers. With increasing e-commerce adoption and cold-chain logistics improvements, Canada’s tuna market is expanding beyond traditional retail into online seafood delivery and niche gourmet offerings.

Mexico Tuna Market Insights

Mexico constitutes a smaller but rapidly evolving segment of the North America tuna market. Though traditionally less prominent than the U.S. and Canada, Mexico’s tuna market is witnessing steady growth due to changing dietary habits and increased urbanization. Imports play a crucial role in meeting local demand. The expansion of modern retail formats, such as Walmart de México and Soriana, has introduced pre-packaged and frozen tuna options to a broader consumer base. Urban centers like Mexico City, Monterrey, and Guadalajara are leading this shift, with rising middle-class incomes and exposure to global food trends. Although still in its early stages, Mexico’s tuna market presents promising potential for future expansion, supported by ongoing trade agreements and increasing awareness of seafood nutrition.

LEADING PLAYERS IN THE NORTH AMERICA TUNA MARKET

Bumble Bee Foods is one of the leading seafood brands in North America and a key player in the canned and value-added tuna market. Known for its long-standing presence in U.S. households, the company offers a wide range of tuna products, emphasizing sustainability, convenience, and nutrition. Bumble Bee has played a significant role in promoting dolphin-safe fishing practices and has been instrumental in shaping consumer awareness around responsible seafood sourcing.

Chicken of the Sea , a subsidiary of Thai Union Group, is another dominant force in the North America tuna market. The brand is recognized for its extensive product portfolio, including traditional canned tuna, gourmet selections, and ready-to-eat meals. Chicken of the Sea has consistently focused on innovation and brand differentiation, contributing to its strong retail presence and consumer loyalty across the U.S. and Canada.

Tri Marine Group is a major global supplier of tuna and plays a crucial role in the supply chain for North America. The company operates across multiple fishing zones and provides raw materials to processors and private-label brands. Tri Marine is known for its commitment to sustainable fisheries and traceability, supporting both domestic and international markets with responsibly sourced tuna products.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by key players in the North America tuna market is sustainability-driven sourcing and certification , where companies align with global standards such as the Marine Stewardship Council (MSC) and the International Seafood Sustainability Foundation (ISSF). This not only enhances brand credibility but also meets the growing consumer demand for ethically sourced seafood.

Another critical approach is product innovation and diversification , particularly in the development of value-added, ready-to-eat, and premium tuna products. Companies are investing in packaging, flavor profiles, and functional ingredients to cater to evolving dietary preferences and urban lifestyles.

Lastly, strategic partnerships and vertical integration play a significant role in strengthening market position. By securing supply chain control from catch to retail and collaborating with eco-conscious organizations, tuna companies ensure quality, traceability, and resilience against supply fluctuations.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the North America Tuna Market include Bumble Bee Foods, StarKist Co., Chicken of the Sea, Crown Prince Inc., Wild Planet Foods, American Tuna, Genova Seafood, Safe Catch, Ocean Naturals, Trader Joe’s, Whole Foods Market, Costco Wholesale Corporation, Walmart Inc.

The North America tuna market is characterized by a competitive landscape driven by a mix of established seafood brands, international suppliers, and emerging private-label retailers. Competition is not only based on pricing and product availability but also increasingly on sustainability, traceability, and brand positioning. Consumers are more informed and selective, demanding transparency in sourcing and environmental impact, which has pushed companies to adopt responsible fishing practices and obtain third-party certifications. The dominance of canned tuna in the market has led to intense rivalry among major brands like Bumble Bee and Chicken of the Sea, both of which are continuously innovating to capture new consumer segments. At the same time, fresh and frozen tuna segments are gaining traction, particularly in premium retail and foodservice channels, creating new opportunities for differentiation. The presence of global tuna suppliers in the North American supply chain further intensifies competition, requiring domestic players to enhance logistics, invest in eco-friendly sourcing, and improve consumer engagement through digital platforms and direct-to-consumer strategies.

RECENT HAPPENINGS IN THE MARKET

- In May 2023, Bumble Bee Foods launched a new line of sustainably sourced, ready-to-eat tuna snacks packaged in eco-friendly materials, aiming to capture the growing health-conscious and environmentally aware consumer base.

- In September 2023, Chicken of the Sea announced a strategic partnership with a major U.S. grocery chain to expand its private-label tuna offerings, reinforcing its presence in mainstream retail and enhancing brand accessibility.

- In January 2024, Tri Marine Group introduced an advanced blockchain-based traceability system across its supply chain to provide real-time tracking of tuna from catch to consumer, strengthening transparency and compliance with sustainability standards.

- In November 2023, Thai Union North America invested in upgrading its U.S. processing facility to increase production capacity and improve cold-chain logistics, ensuring higher product quality and faster delivery to market.

- In March 2024, a consortium of North American tuna importers, including key industry players, collaborated with the International Seafood Sustainability Foundation to support conservation initiatives in the Eastern Pacific, aligning with global sustainability goals and strengthening their sourcing credentials.

MARKET SEGMENTATION

This research report on the North America tuna market has been segmented and sub-segmented based on species, product type and region.

By Species

- Skipjack Tuna

- Albacore Tuna

By Product Type

- Canned Tuna

- Fresh Tuna

By Region

- US

- Canada

- Rest of North America

Frequently Asked Questions

1. What are the main types of tuna products available in the market?

The market includes canned tuna, frozen tuna, fresh tuna, tuna steaks, and ready-to-eat tuna meals.

2. Who are the key players in the North America tuna market?

Major players include Bumble Bee Foods, StarKist Co., Chicken of the Sea, Genova, and Wild Planet Foods.

3. What are the major factors driving growth in the North America tuna market?

Factors include increased demand for protein-rich diets, convenience foods, sustainability awareness, and innovations in packaging.

4. What are the popular distribution channels for tuna products in North America?

Supermarkets/hypermarkets, online retailers, convenience stores, and specialty seafood stores.

5. What consumer trends are influencing the tuna market in North America?

Rising demand for sustainably sourced tuna, organic/clean-label products, and flavored/ready-to-eat tuna snacks.

6. How is sustainability impacting the tuna industry in North America?

Certifications like MSC and initiatives like pole-and-line fishing are increasingly influencing consumer preferences and brand strategies.

7. What challenges are faced by the North America tuna market?

Overfishing concerns, supply chain disruptions, fluctuating raw material prices, and regulatory compliance.

8. What role does technology play in the tuna market?

Innovations in processing, packaging, and traceability (e.g., blockchain, smart labeling) are enhancing product quality and consumer trust.

9. What regulations affect the tuna market in North America?

FDA food safety standards, NOAA guidelines, and import/export regulations play key roles.

10. What is the forecast for the North America tuna market in the coming years?

The market is expected to grow at a steady CAGR, driven by health trends, convenience, and sustainable practices.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com