North America Whole Slide Imaging Market Research Report By Product, Application, End-User & Country (The United States, Canada and Rest of North America) – Industry Analysis( 2026 to 2034)

North America Whole Slide Imaging Market Size

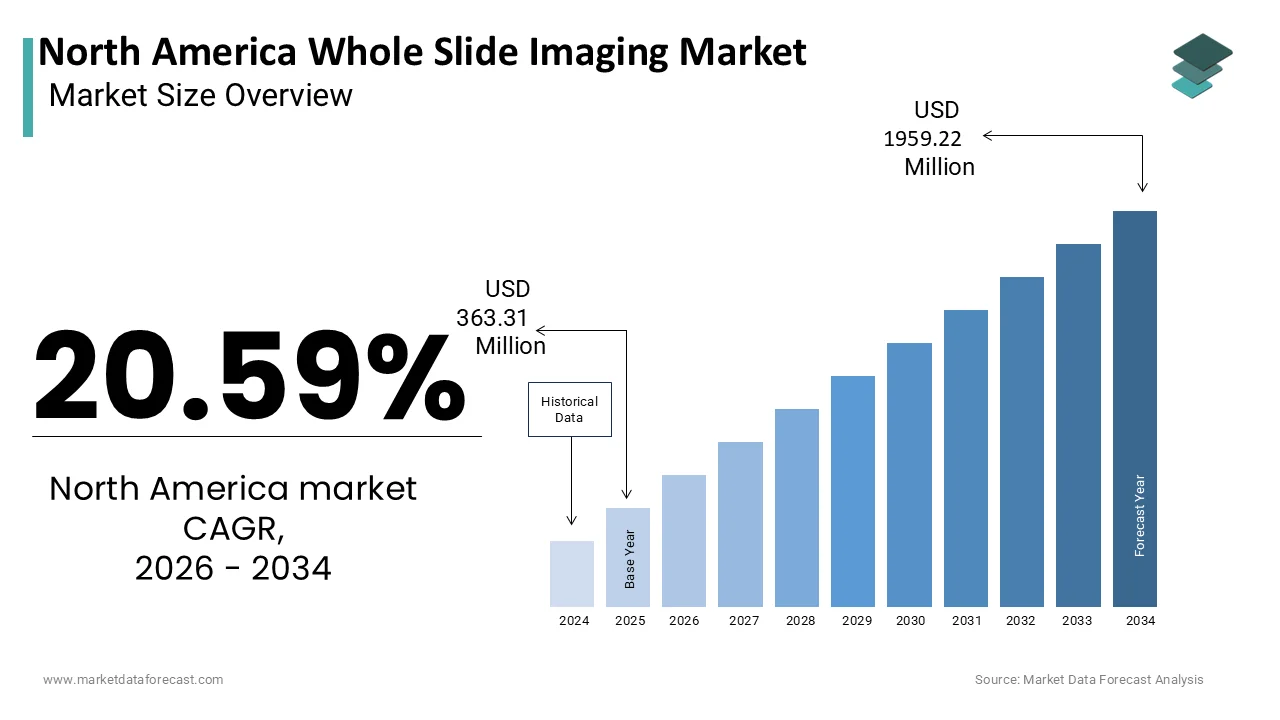

The North America Whole Slide Imaging Market Size was valued at USD 363.31 million in 2025, is expected to have 20.59% CAGR from 2026 to 2034 and be worth USD 1959.22 million by 2034 from USD 438.12 million in 2026.

Whole Slide Imaging (WSI) is referred to as digital pathology, is a modern technology that converts glass histology or cytology slides into high-resolution digital images using specialized scanners. These digital images can be viewed, analyzed, shared, and archived using software platforms, enabling pathologists to make more accurate and faster diagnoses. This innovation has significantly transformed traditional pathology by integrating advanced image analysis algorithms, cloud-based data storage, and telepathology capabilities. According to the U.S. National Library of Medicine, digital pathology systems have demonstrated improved diagnostic accuracy by up to 30% in certain oncology applications. Moreover, the American Society for Clinical Pathology reported that over 60% of pathology labs in the U.S. are either piloting or implementing digital workflows in their operations by 2025. The region benefits from a robust healthcare infrastructure, favorable reimbursement policies, and strong regulatory support from agencies such as the U.S. Food and Drug Administration (FDA), which approved multiple WSI systems for primary diagnostic use in recent years.

MARKET DRIVERS

Rising Demand for Telepathology Services

One of the most significant drivers of the North America Whole Slide Imaging (WSI) market is the growing reliance on telepathology services in rural and underserved areas. Telepathology enables remote diagnosis through digital image transmission, eliminating geographical barriers and improving access to expert pathologists. According to the Association of American Medical Colleges, nearly 20% of the U.S. population resides in rural regions where access to specialized pathology services is limited. WSI facilitates real-time collaboration between pathologists and clinicians, enhancing diagnostic efficiency and turnaround time. The surge in demand for second opinions and multi-disciplinary tumor board consultations has further fueled the adoption of WSI-enabled telepathology. For instance, the University of Pittsburgh Medical Center (UPMC) reported a 40% reduction in case turnaround time after integrating digital pathology into its teleconsultation framework. Additionally, the U.S. Department of Veterans Affairs launched a nationwide digital pathology initiative in 2022, aiming to streamline cancer diagnostics across its 1,298 healthcare facilities. This expansion reflects institutional confidence in WSI’s ability to enhance diagnostic consistency and reduce inter-observer variability.

Integration of Artificial Intelligence in Diagnostic Workflows

The incorporation of artificial intelligence (AI) into Whole Slide Imaging (WSI) systems has emerged as a critical growth driver for the North America market. AI-powered image analysis tools enable automated detection, classification, and quantification of cellular structures, significantly improving diagnostic accuracy and reducing manual workload for pathologists. Major players such as Paige.AI, PathAI, and ProFound AI have introduced FDA-cleared AI modules designed to assist in identifying malignancies with high sensitivity. For example, Paige.AI's AI system achieved a 96% accuracy rate in detecting metastatic breast cancer in lymph node samples during clinical trials conducted in partnership with Memorial Sloan Kettering Cancer Center. Furthermore, the U.S. National Institutes of Health (NIH) allocated $75 million in funding in 2025 to accelerate the development of AI-driven pathology tools under its broader cancer moonshot initiative. Additionally, the American Journal of Surgical Pathology published findings indicating that AI-integrated WSI reduced diagnostic errors by 18% across participating labs in a multi-center study involving 12,000 cases.

MARKET RESTRAINTS

High Initial Capital Investment and Operational Costs

A major restraint impeding the widespread adoption of Whole Slide Imaging (WSI) in North America is the substantial initial capital investment required for digital pathology infrastructure. In addition to acquisition costs, laboratories must invest in IT infrastructure upgrades, cybersecurity measures, and ongoing maintenance, which collectively increase total cost of ownership. Operational expenses also pose a challenge. Annual maintenance contracts for WSI systems can exceed $20,000 per scanner, while cloud-based storage solutions incur recurring subscription fees. For smaller hospital labs and independent pathology practices, these financial burdens limit scalability and delay digital transformation efforts. A survey conducted by the Association for Pathology Informatics in 2023 revealed that 42% of small-to-mid-sized pathology labs cited cost constraints as the primary barrier to adopting WSI.

Moreover, training pathologists and lab technicians to operate digital pathology systems requires additional time and resources. According to the Archives of Pathology & Laboratory Medicine, training programs for digital pathology implementation average $15,000 per user, further compounding economic pressures. Although larger academic medical centers and reference labs have managed to absorb these costs, many community hospitals remain hesitant to transition from conventional microscopy.

Regulatory and Reimbursement Complexities

Another critical constraint affecting the growth of the North America Whole Slide Imaging (WSI) market is the complexity of regulatory approvals and inconsistent reimbursement frameworks. While the U.S. Food and Drug Administration (FDA) has cleared several WSI platforms for primary diagnostic use, the approval process remains rigorous and time-consuming. Manufacturers must undergo extensive clinical validation, including multi-site studies demonstrating non-inferiority to traditional microscopy. For example, the FDA’s clearance of Philips’ IntelliSite Pathology Solution in 2017 followed a three-year evaluation period involving over 2,000 cases across eight institutions.

Beyond regulatory hurdles, reimbursement challenges persist due to the absence of standardized billing codes for digital pathology services. The Centers for Medicare & Medicaid Services (CMS) currently lacks a specific Current Procedural Terminology (CPT) code for WSI interpretation, leading to inconsistent coverage among private and public payers. This disparity discourages smaller healthcare providers from investing in WSI, fearing insufficient return on investment. Additionally, some states impose restrictive regulations on cross-border telepathology, complicating interstate diagnostic collaborations.

MARKET OPPORTUNITIES

Expansion of Precision Oncology and Biomarker Research

A significant opportunity driving the North America Whole Slide Imaging (WSI) market is the rapid expansion of precision oncology and biomarker research. With the growing emphasis on personalized treatment strategies, there is an increased need for highly detailed histopathological analysis to identify molecular markers and assess tumor heterogeneity. Whole Slide Imaging plays a crucial role in this context by enabling high-resolution, quantitative analysis of tissue samples, facilitating the discovery and validation of novel biomarkers.

According to the National Cancer Institute, over 1.9 million new cancer cases were diagnosed in the United States in 2023 with the urgent need for more effective diagnostic tools. WSI, when integrated with machine learning and deep learning algorithms, allows for multiplexed image analysis, supporting the identification of predictive biomarkers such as PD-L1, HER2, and BRCA mutations. For instance, a 2025 study published in Nature Medicine demonstrated that AI-enhanced WSI could detect microsatellite instability (MSI) in colorectal cancer tissues with 94% accuracy, offering a non-invasive alternative to genetic testing. Pharmaceutical companies are also leveraging WSI for companion diagnostic development. Roche and PathAI collaborated in 2023 to develop AI-driven image analysis tools for immuno-oncology drug trials, accelerating patient stratification and response prediction.

Increasing Adoption of Digital Pathology in Academic and Research Institutions

The growing adoption of digital pathology in academic and research institutions presents a compelling growth avenue for the North America Whole Slide Imaging (WSI) market. Universities, teaching hospitals, and biomedical research centers are increasingly incorporating WSI into their educational curricula and translational research initiatives. This shift is driven by the advantages of digital slide repositories, which facilitate collaborative learning, remote access, and standardized training protocols. For example, Harvard Medical School and the University of Toronto have implemented fully digital pathology training programs, allowing students and residents to access vast libraries of annotated digital slides. Beyond education, WSI is instrumental in large-scale biomedical research projects. The Human Protein Atlas initiative, led by researchers in collaboration with U.S.-based institutions, utilizes WSI to map protein expression across thousands of tissue samples.

MARKET CHALLENGES

Data Storage and Management Complexity

One of the foremost challenges confronting the North America Whole Slide Imaging (WSI) market is the immense volume of data generated by high-resolution digital pathology scans. A single WSI file can range from 1 GB to over 5 GB in size, depending on the magnification level and tissue area scanned. Many hospitals and diagnostic centers struggle with existing infrastructure limitations. Traditional Picture Archiving and Communication Systems (PACS) used in radiology are not optimized for the sheer size and complexity of WSI files. According to a 2025 white paper by the Healthcare Information and Management Systems Society (HIMSS), nearly 50% of surveyed pathology labs reported delays in image retrieval due to inadequate server capacity and bandwidth constraints. Furthermore, interoperability issues between different vendors' WSI platforms complicate data exchange and archival processes. The lack of standardized formats and APIs hampers seamless integration with electronic health records (EHRs) and laboratory information systems (LIS).

Shortage of Skilled Professionals and Training Gaps

A persistent challenge in the North America Whole Slide Imaging (WSI) market is the shortage of trained professionals capable of effectively operating and interpreting digital pathology systems. Transitioning from traditional microscopy to digital workflows requires pathologists, lab technicians, and IT staff to acquire new competencies in image analysis software, data management, and quality assurance protocols. According to a 2023 workforce analysis by the Association of American Medical Colleges, the U.S. faces a projected shortfall of over 5,000 pathologists by 2030, exacerbating the strain on existing personnel. Many practicing pathologists received minimal exposure to digital pathology during their training, resulting in a learning curve that slows adoption. To bridge this gap, institutions such as the American Society for Clinical Pathology (ASCP) and the Association for Pathology Informatics (API) have launched continuing education programs and certification courses. However, enrollment remains low, and formalized training pathways are still emerging.

REPORT COVERAGE

| METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, End-User and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | The U.S., Canada and Rest of North America |

| Market Leader Profiled | Digirad Corporation, Gamma Medica Inc., GE Healthcare, Hologic Inc., Leica Microsystems GmbH |

SEGMENTAL ANALYSIS

By Product Insights

The software segment was the largest and held 32.1% of the North America Whole Slide Imaging (WSI) market share in 2025. AI-based software solutions can detect subtle morphological variations in tissue samples, enabling early cancer diagnosis with greater accuracy. For instance, PathAI's AI-assisted software demonstrated a 95% sensitivity rate in identifying breast cancer cells in lymph node biopsies during clinical trials conducted in collaboration with Johns Hopkins University in 2023. Additionally, the growing demand for cloud-based image management systems has further fueled software adoption. Cloud platforms offer scalable storage, seamless data sharing, and real-time collaboration among pathologists. According to a 2025 HIMSS survey, over 60% of U.S. hospitals have adopted cloud-based digital pathology solutions to improve workflow efficiency and reduce local server costs.

The services segment is projected to grow with a CAGR of 18.7% from 2025 to 2033. One of the primary factors driving service expansion is the increasing adoption of WSI in decentralized healthcare settings, particularly in rural and community hospitals that lack in-house pathology expertise. The U.S. Department of Health and Human Services noted that nearly 20% of Americans reside in areas with limited access to specialized pathology services, prompting hospitals to contract third-party diagnostic firms. Companies like ProFound AI and Paige.AI offer subscription-based diagnostic services that allow smaller labs to access high-quality WSI interpretation without investing heavily in internal infrastructure. Moreover, the growing need for maintenance, training, and system integration services is accelerating market expansion. A 2023 survey by the Association for Pathology Informatics revealed that 55% of laboratories required external technical support within the first year of deploying WSI systems.

By Application Insights

The telepathology segment held 36.3% of the North America Whole Slide Imaging (WSI) market share in 2025. A major driver of this segment’s growth is the increasing implementation of teleconsultation networks across hospital systems. According to the Association of American Medical Colleges, nearly 20% of the U.S. population resides in rural areas, where fewer than 10% of practicing pathologists are based. To bridge this gap, healthcare providers are leveraging WSI-based telepathology to enable real-time case reviews and second opinions. Another critical factor fueling telepathology adoption is the rise in multi-disciplinary tumor boards requiring rapid case assessments.

The cancer diagnostics segment is likely to grow with a CAGR of 19.3% from 2025 to 2033. According to the National Cancer Institute, over 1.9 million new cancer cases were diagnosed in the United States in 2023, reinforcing the demand for efficient and precise diagnostic methodologies. Whole Slide Imaging plays a crucial role in oncology by enabling detailed histopathological evaluations, including tumor grading, biomarker detection, and microenvironment analysis. Additionally, pharmaceutical companies are increasingly utilizing WSI in companion diagnostic development for targeted therapies. Roche and PathAI collaborated in 2023 to develop AI-driven image analysis tools for immuno-oncology drug trials, enhancing patient stratification and response prediction.

By End-User Insights

The hospitals and clinics segment was accounted in holding 48% of the North America whole slide imaging market share in 2025. According to the American Hospital Association, over 6,000 hospitals operate in the United States, many of which are investing in digital transformation initiatives to enhance diagnostic accuracy and streamline operations. Furthermore, regulatory approvals from the U.S. Food and Drug Administration (FDA) for WSI systems in primary diagnostics have encouraged broader hospital adoption. In 2025, the FDA cleared additional scanner models for intraoperative frozen section analysis, expanding the use of WSI in surgical pathology departments.

The academic and research institutes segment is lucratively growing with a CAGR of 20.1% from 2025 to 2033. One of the primary factors driving this segment is the integration of WSI into pathology education programs. According to the Association of Pathology Chairs, over 70% of U.S. pathology residency programs had adopted digital pathology for teaching purposes by 2023, allowing students to access high-resolution virtual slides remotely. Institutions such as Harvard Medical School and the University of Toronto have replaced traditional microscopy with digital slide repositories by enhancing student engagement and diagnostic training efficiency.

Additionally, academic research centers are leveraging WSI for translational studies in precision medicine and biomarker discovery. The National Institutes of Health (NIH) funded multiple WSI-based projects under its All of Us Research Program, aiming to digitize over one million biospecimens for personalized treatment development. Furthermore, collaborations between universities and tech firms such as the partnership between Stanford University and Paige.AI are advancing AI-driven pathology research.

COUNTRY LEVEL ANALYSIS

United States led the North America Whole Slide Imaging (WSI) market with 82.1% of the share in 2025. Moreover, leading academic institutions such as MD Anderson Cancer Center and Memorial Sloan Kettering have integrated digital pathology into their clinical and research workflows. The American Society for Clinical Pathology reported that over 60% of pathology labs in the U.S. are actively using or piloting WSI technologies by 2025.

Canada was in leading the North America WSI market with 13.3% of share in 2025. A major factor supporting Canada’s WSI market expansion is the country’s focus on centralized healthcare digitization. The Canadian Institute for Health Information (CIHI) reported that healthcare spending reached $331 billion in 2023, with a significant portion allocated to digital health infrastructure upgrades. Hospitals in Ontario and British Columbia have been early adopters of digital pathology, with institutions like the University Health Network (UHN) in Toronto implementing enterprise-wide WSI systems for oncology diagnostics. Additionally, the Canadian government has prioritized innovation in pathology through initiatives such as the Digital Technology Supercluster, which funds AI-driven healthcare solutions. In 2023, a partnership between PathAI and the University of Calgary was launched to develop AI-based tools for prostate cancer detection using WSI. According to the Canadian Association of Pathologists, over 40% of academic pathology departments have transitioned to digital workflows, signaling a promising trajectory for WSI adoption across the country.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a key role in the North American whole slide imaging market profiled in this report are Philips, Siemens, Positron Corporation, Agfa-Gevaert N.V., CardiArc Ltd., Digirad Corporation, Gamma Medica Inc., GE Healthcare, Hologic Inc., Leica Microsystems GmbH, Nikon Corporation, Visiopharm, 3Dhistech, Hamamatsu Photonics KK, and Indica Labs.

The competition in the North America Whole Slide Imaging (WSI) market is marked by rapid technological evolution, increasing vendor diversification, and strategic positioning by established players. While a few dominant firms continue to lead in innovation and market penetration, emerging companies are gaining traction by introducing niche solutions tailored for specialized applications. The landscape is shaped by continuous advancements in artificial intelligence, machine learning, and cloud-based diagnostics, which are redefining how pathology is practiced. Mergers and acquisitions are also becoming common as larger companies seek to consolidate their offerings and expand their service portfolios. At the same time, academic and clinical end-users are playing a pivotal role in shaping vendor strategies through collaborative research and pilot implementations. This dynamic environment fosters innovation but also intensifies pressure on companies to differentiate themselves through superior technology, robust support systems, and tailored deployment models that align with evolving healthcare delivery paradigms.

Top Players in the Market

Philips Healthcare is a global leader in medical imaging and digital pathology solutions. The company's IntelliSite Pathology Solution was among the first whole slide imaging systems to receive FDA clearance for primary diagnostic use in the U.S. Philips continues to drive innovation by integrating AI and cloud-based platforms into its digital pathology offerings by enabling seamless data sharing and advanced image analysis. Its strong presence in academic institutions and large hospital networks has significantly influenced the adoption of WSI across North America.

Leica Biosystems, which is a subsidiary of Danaher Corporation, plays a crucial role in advancing digital pathology through its high-resolution scanners and comprehensive workflow solutions. The company’s Aperio portfolio is widely used in research, diagnostics, and pharmaceutical applications. Leica’s focus on interoperability, ease of integration with existing lab systems, and continuous enhancement of software analytics has made it a preferred partner for pathology labs transitioning to digital workflows. Its commitment to education and training further supports broader WSI adoption.

Hamamatsu Photonics is a key player known for its high-performance digital pathology scanners, particularly the NanoZoomer series. The company emphasizes precision imaging and long-term system reliability, making its products popular in research and clinical trial settings. Hamamatsu collaborates extensively with academic and pharmaceutical organizations to develop advanced imaging tools tailored for biomarker discovery and cancer research.

Top Strategies Used by Key Market Participants

One of the most prominent strategies employed by leading players in the North America Whole Slide Imaging market is strategic partnerships and collaborations. Companies are increasingly teaming up with academic institutions, healthcare providers, and AI developers to enhance their product capabilities and expand clinical applications. These alliances help integrate cutting-edge technologies into existing WSI platforms and accelerate adoption in real-world settings.

Another major approach is product innovation and development. Market leaders continuously invest in R&D to introduce advanced imaging systems, AI-powered analysis tools, and cloud-based storage solutions that improve diagnostic accuracy and workflow efficiency.

The expanding service offerings and support ecosystems has become essential for maintaining competitive advantage. Vendors are enhancing their post-sales services, offering training programs, maintenance packages, and telepathology consulting to ensure smooth implementation and sustained usage of WSI systems across diverse healthcare environments.

RECENT HAPPENINGS IN THE MARKET

In January 2025, Philips Healthcare launched an updated version of its IntelliSite Digital Pathology Solution, featuring enhanced AI-driven image analysis tools designed to improve cancer detection rates and streamline diagnostic workflows across hospitals and research centers in North America.

In March 2025, Leica Biosystems expanded its collaboration with a leading U.S.-based cancer research institute to integrate its Aperio digital pathology platform into ongoing clinical trials by aiming to support precision oncology and accelerate drug development processes.

In May 2025, Hamamatsu Photonics introduced a new remote consultation module for its NanoZoomer series, which is allowing pathologists to securely share and analyze digital slides in real-time, reinforcing its presence in the telepathology segment of the North American market.

In July 2025, PathAI partnered with a major U.S. health system to deploy its AI-assisted diagnostic software within hospital pathology departments by enhancing accuracy in cancer diagnosis and supporting large-scale screening initiatives.

In September 2025, DynaPath Solutions , a digital pathology startup, received strategic funding from a leading venture capital firm to scale its cloud-based WSI platform by targeting smaller laboratories seeking cost-effective and scalable digital transformation solutions.

MARKET SEGMENTATION

This research report on the north america whole slide imaging market has been segmented and sub-segmented into the following categories

By Product

- Software

- Service

By Application

- Telepathology

- Cancer

By End-User

- Biotechnology and Pharmaceutical Companies

- Academic and Research Institutes

- Hospitals and Clinics

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What is North America Whole Slide Imaging (WSI)?

Whole Slide Imaging involves digitizing glass microscope slides into high-resolution digital images. These images can be analyzed, stored, and shared electronically, facilitating remote consultations and enhancing diagnostic workflows in pathology.

What challenges does the North America WSI market face?

The market encounters several challenges are High initial and maintenance costs Data storage and management issues Regulatory and standardization hurdles Integration complexities with existing systems

What are the cost implications of implementing WSI?

Implementing WSI involves significant costs, including: Initial capital investment (e.g., scanners, software) Ongoing maintenance and storage fees Training and support expenses

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com