Global Whole Slide Imaging Market Size, Share, Trends & Growth Forecast Report By Product, Application, End-User & Region (North America, Europe, APAC, Latin America, Middle East and Africa), Industry Analysis (2026 to 2034)

Global Whole Slide Imaging Market Report Summary

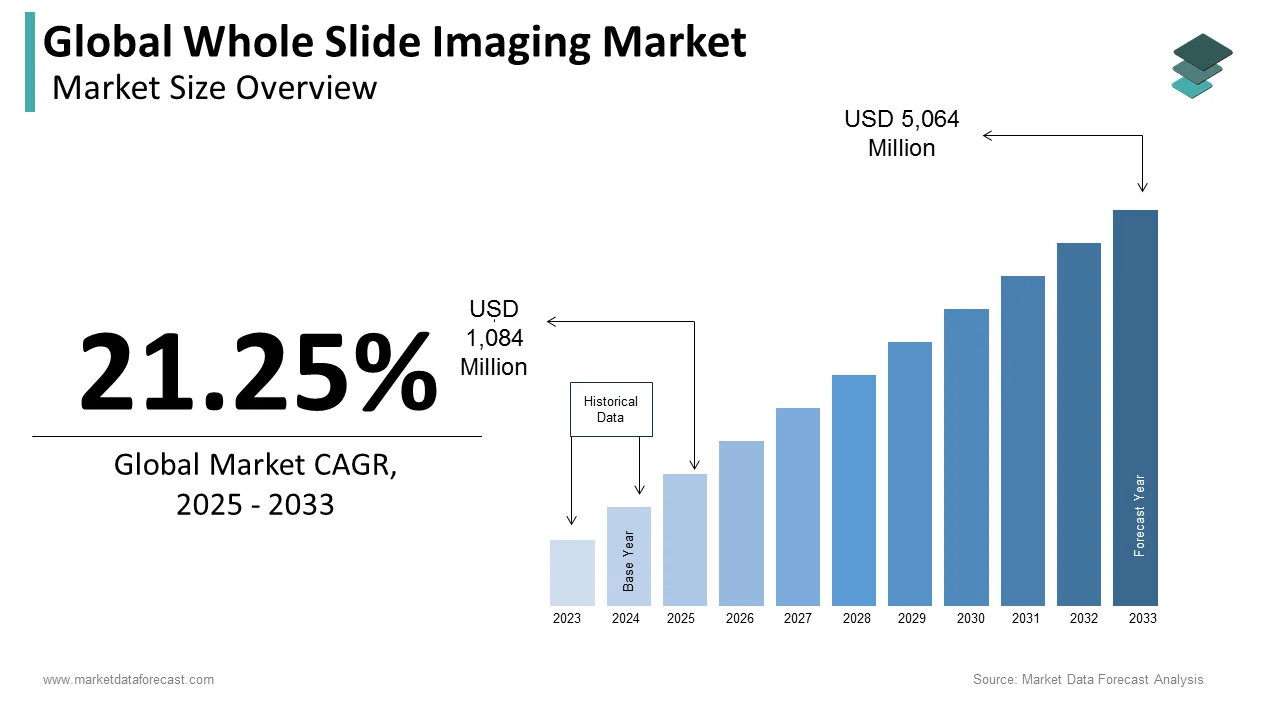

The global whole slide imaging market was valued at USD 1,084 million in 2025 and is projected to grow from USD 1,314.35 million in 2026 to USD 6,140 million by 2034, registering a CAGR of 21.25% from 2026 to 2034. Market growth is driven by increasing adoption of digital pathology solutions, rising demand for telepathology services, and expanding integration of artificial intelligence in diagnostic imaging workflows. Whole slide imaging enables the digitization of glass pathology slides into high-resolution digital images, supporting remote diagnosis, collaborative consultations, and advanced image analysis. Growing investments in healthcare digitalization, increasing cancer diagnostic procedures, and rising demand for laboratory automation are further accelerating global market expansion.

Key Market Trends

- Rising adoption of digital pathology and virtual slide technologies.

- Increasing demand for telepathology and remote diagnostic services.

- Growing integration of AI-powered image analysis and pathology workflow automation.

- Expansion of cloud-based pathology data management platforms.

- Increasing focus on laboratory digitization and precision diagnostics.

Segmental Insights

- Based on type, the scanners segment dominated the global whole slide imaging market in 2025 by accounting for 40.4% market share, driven by increasing deployment of high-resolution digital slide scanners across pathology laboratories and hospitals.

- Based on application, the tele-pathology segment led the market by capturing 40.9% share in 2025, supported by rising demand for remote pathology consultations, digital collaboration, and faster diagnostic workflows.

- Based on end user, the hospitals and clinics segment held the majority share of 45.7% in 2025, driven by growing adoption of digital diagnostic infrastructure and increasing demand for efficient pathology workflow management.

Regional Insights

The global whole slide imaging market is witnessing rapid growth across major regions, supported by increasing healthcare digitalization, rising pathology automation, and expanding demand for advanced diagnostic imaging solutions.

- North America maintained the leading position in the global whole slide imaging market in 2025, supported by advanced healthcare infrastructure, widespread adoption of digital pathology technologies, and strong investments in laboratory automation.

- Europe represents a highly progressive market for digital pathology solutions, driven by increasing adoption of virtual slide architectures, healthcare modernization initiatives, and growing integration of AI-assisted diagnostics.

- Asia-Pacific is projected to register the fastest growth during the forecast period, supported by rapid expansion of healthcare infrastructure, increasing adoption of digital pathology workflows, and rising demand for advanced diagnostic imaging systems.

Competitive Landscape

The global whole slide imaging market is characterized by strong competition among medical imaging companies, digital pathology solution providers, and healthcare technology firms focusing on high-resolution imaging systems, AI-powered pathology analysis, and laboratory workflow automation. Market participants are emphasizing innovation in scanner technologies, cloud-based pathology platforms, and integrated digital diagnostic ecosystems to strengthen market positioning. Strategic collaborations, acquisitions, and investments in precision diagnostics and telepathology solutions are shaping competitive dynamics across the market.

Prominent companies operating in the global whole slide imaging market include Philips, Siemens, Roche Diagnostics, Positron Corporation, Agfa-Gevaert N.V., CardiArc Ltd., Digirad Corporation, Gamma Medica Inc., GE Healthcare, Leica Biosystems, Hologic Inc., Leica Microsystems GmbH, Nikon Corporation, Visiopharm, 3DHISTECH, Hamamatsu Photonics KK, and Indica Labs.

Global Whole Slide Imaging Market Size

The global whole slide imaging market size was valued at USD 1,084 million in 2025, and this value is expected to be worth USD 6,140 million by 2034, from USD 1,314.35 million in 2026, growing at a CAGR of 21.25% from 2026 to 2034.

The whole slide imaging market is expanding through the high-resolution digitization of conventional glass specimens into dynamic, multi-gigapixel virtual slides. This technological paradigm shift has diagnostic pathology from manual optical microscopes to automated scanning systems integrated with advanced image management software. The clinical relevance of this transition is underscored by the escalating oncological burden forcing laboratories to optimize throughput. As per data published by the American Cancer Society, an estimated 2.1 million new cancer cases are projected in the United States, driving an urgent demand for high-capacity brightfield and fluorescence scanners to manage intensive biopsy workloads. Concurrently, regional pathology shortfalls accelerate the integration of virtual workflows. According to a workforce analysis by the Royal College of Pathologists, merely 3% of histopathology departments in the United Kingdom operate with sufficient staff, propelling the adoption of digital slide platforms to enable remote consultations and mitigate diagnostic backlogs through cross-border telepathology.

MARKET DRIVERS

Escalating Global Oncological Burden and Complex Biopsy Volume Demands

The exponential rise in complex cancer cases is one of the major factors driving the growth of the global whole slide imaging market, which is forcing laboratories to transition from manual glass slides to automated high-throughput scanning. According to a long-term epidemiological forecast by the World Health Organization, global cancer cases are projected to rise by around 77% by the middle of the century, climbing from an estimated 20 million new cases to more than 35 million annual diagnoses. This massive influx of tissue samples creates an operational bottleneck in traditional pathology departments, which must process multiple specialized stains and deep biopsies per patient. Whole slide imaging platforms resolve this capacity crisis by scanning an entire glass specimen into a digital format in fewer than 90 seconds. This speed enables continuous, high-volume slide digitization without manual manipulation, allowing laboratories to optimize their workflows. Furthermore, complex oncological evaluations often require subspecialist consultations, which are severely hindered by the logistics of physical slide shipping. Digitized slides eliminate these delays by facilitating immediate remote access, ensuring that complex caseloads are reviewed quickly. This capability mitigates diagnostic bottlenecks, directly driving the integration of whole slide scanners into routine clinical workflows.

Technical Validation and Strict Regulatory Compliance Frameworks

The establishment of standardized validation protocols by international pathology bodies is further fuelling the whole slide imaging market expansion. As per clinical practice guidelines published by the College of American Pathologists, laboratories implementing whole slide imaging for primary diagnosis must execute a rigorous self-validation study involving at least 60 individual cases. This protocol mandates a formal 2-week washout period between viewing the digital images and the physical glass slides to ensure objectivity, requiring a diagnostic concordance rate greater than 95% to achieve clinical certification. These explicit regulatory benchmarks give healthcare institutions the clinical assurance required to shift entirely away from conventional optical microscopes. Regulatory agencies have also established clear data integrity, image resolution, and metadata synchronization criteria, which reduce the risk of diagnostic discrepancies. By formalizing these legal and clinical pathways, the industry provides laboratories with clear implementation templates. This reduces compliance anxiety and drives hospital networks to invest in digital pathology systems to future-proof their operations.

MARKET RESTRAINTS

Substantial Initial Capital Expenditures and Ongoing Operational Maintenances

The prohibitive upfront acquisition cost of high-throughput scanning systems, coupled with software licensing fees, restricts the adoption of digital pathology workflows in small to mid-sized laboratories. According to financial assessment data compiled by the Digital Pathology Association, the baseline purchase price for a clinical-grade high-capacity whole slide scanner often ranges between 150000 and 350000 American dollars per unit. This capital outlay represents only the physical hardware component of the transition, as laboratories must also finance specialized image management systems, laboratory information system integrations, and multi-year technical support contracts. Furthermore, regular optical calibrations, mechanical servicing, and automated component replacements contribute to steep annual maintenance expenditures that generally average 10% to 15% of the original equipment purchase price. For community hospitals and independent diagnostic facilities operating on narrow profit margins, these multi-hundred-thousand-dollar investments yield a prolonged return on investment period that is difficult to justify. Consequently, smaller medical institutions frequently delay clinical digitization, relying instead on traditional light microscopes and restricting the market to large academic medical centers.

Overwhelming Long-Term Data Storage Infrastructures and Local Network Bandwidth Capacities

The colossal file size generated during high-resolution tissue digitization creates a severe data management and financial burden that strains existing laboratory information technology networks, which is hindering the whole slide imaging market expansion. As per technical infrastructure documentation published by the College of American Pathologists, a single standard tissue specimen scanned at 40 times magnification produces an uncompressed data file ranging between 1 and 10 gigabytes. When a large diagnostic facility processes an average volume of 250000 slides annually, the laboratory generates upwards of 250 terabytes of non-redundant data each year, which escalates rapidly when factoring in mandatory backup protocols and data redundancies. Compounding this challenge, medical regulatory frameworks demand that primary diagnostic images be archived securely for at least 10 years, creating an unsustainable storage accumulation curve. Managing this multi-petabyte data footprint requires substantial investments in enterprise-tier cloud storage or costly on-premises servers, alongside high-speed network upgrades to prevent severe latency during slide retrieval. This immense data architecture bottleneck severely deters healthcare providers from pursuing complete digital transformation.

MARKET OPPORTUNITIES

Seamless Integration of Advanced Computational Pathology and Artificial Intelligence Diagnostic Algorithms

The convergence of whole slide imaging with deep learning foundation models presents a promising opportunity for global market growth. According to an extensive clinical review published in the Journal of Pathology Informatics, deploying artificial intelligence algorithms as an automated second read on whole slide images yields a disease detection sensitivity rate of 96.3% and a specificity rate of 93.3% across diverse malignancies. These advanced computational tools analyze multi-gigapixel images in real time, executing complex tasks such as micro metastasis screening, mitotic figure counting, and structural tumor grading that are traditionally prone to interobserver variability. For instance, recent regulatory milestones confirm this momentum, as exemplified by the United States Food and Drug Administration granting clearance to specialized algorithmic tools like Paige PanCancer Detect to assist in flagging suspicious tumor foci across multiple tissue types. By embedding these machine learning pipelines directly into image management software, laboratories can automate routine screening workflows and reduce slide review times from 180 seconds to fewer than 120 seconds per case. This synergistic integration dramatically optimizes diagnostic accuracy, positioning digital slide systems as an indispensable prerequisite for modern computational oncology.

Acceleration of Precision Medicine Pathways and Companion Diagnostic Development in Clinical Trials

The virtualization of glass slides unlocks unprecedented utility in translational research and targeted therapeutic development by facilitating deep spatial tissue phenotyping within the tumor microenvironment. As per clinical validation data presented at the American Society of Clinical Oncology annual meeting, utilizing artificial intelligence foundation models trained on more than 58000 whole slide images allows researchers to infer molecular alterations and predict treatment responses directly from standard hematoxylin and eosin-stained slides. This capability bridges the gap between traditional histology and next-generation sequencing, enabling biopharmaceutical developers to utilize digital slide libraries for rapid patient stratification in global clinical trials. The strategic value of this technology is further highlighted by the United States Food and Drug Administration granting Breakthrough Device Designation to computational pathology applications, such as the Ventana TROP2 RxDx digital assay, marking the first time an image analysis algorithm received such status as a cancer companion diagnostic. By integrating high-resolution scanning infrastructure into the drug development pipeline, the market transitions from a basic laboratory digitization tool to a core component of personalized medicine, driving sustained long-term enterprise investments from pharmaceutical consortia and contract research organizations.

MARKET CHALLENGES

Universal System Interoperability Obstacles and Proprietary Image Format Incompatibilities

The fragmentation of digital architectures due to specialized vendor-specific data formats is challenging the expansion of the whole slide imaging market. According to a technical evaluation published by the Digital Imaging and Communications in Medicine Standards Committee, many prominent hardware manufacturers archive scanned tissue specimens using individual proprietary file structures instead of universally accessible open source layers. This technological isolation forces medical institutions into vendor lock-in, since a multi-gigapixel image captured on one scanner platform cannot be easily rendered or processed within a competing image management software or laboratory information system. To resolve this structural gap, international groups actively advocate for the widespread implementation of the DICOM Supplement 145 standard for whole slide imaging to establish uniform metadata structures and tiling geometries. However, legacy systems lack native compliance, necessitating secondary software converters that introduce transmission latency and increase implementation costs. Because large medical networks frequently utilize hardware from multiple scanner generations, these pervasive format discrepancies complicate clinical workflows, prevent cross-institutional telepathology collaborations, and slow down the broader adoption of uniform digital pathology networks.

High Preanalytical Tissue Preparation Variabilities and Automated Scanning Artifact Vulnerabilities

The strict dependency of automated high-throughput optical scanners on near-flawless tissue geometry is further challenging the global market expansion. As per a comprehensive quality control study published in the Journal of Pathology Informatics, physical slide preparation irregularities such as tissue folds, air bubbles under the coverslip, varying section thicknesses, and stain intensity fluctuations directly induce scanning failures. While a human pathologist using a traditional manual microscope can easily compensate for a slight blur by adjusting the fine focus knob on a thick tissue sample, automated scanning arrays frequently fail to calculate the correct focal plane over uneven surfaces. This limitation results in out-of-focus zones that render the final virtual slide clinically unusable, creating an average rescanning and remounting rate of 5% to 12% in high-volume clinical laboratories. This high rate of technical repetition disrupts laboratory workflows, delays diagnostic turnaround times, and increases material costs. Additionally, these subtle physical artifacts transfer directly into digital pixels, introducing misleading data that can degrade the accuracy of downstream artificial intelligence diagnostic algorithms.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, End-user, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Philips, Siemens, Positron Corporation, Agfa-Gevaert N.V., CardiArc Ltd., Digirad Corporation, Gamma Medica Inc., GE Healthcare, Hologic Inc., Leica Microsystems GmbH, Nikon Corporation, Visiopharm, 3Dhistech, Hamamatsu Photonics KK, Indica Labs., and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The scanners segment dominated the market by holding 40.4% of the global market share in 2025. The rapid technological shift toward ultra-high throughput automation within clinical laboratories is one of the major factors propelling the dominance of the scanners segment in the global market. Large diagnostic networks are investing heavily in multi-rack, continuous load scanners that can digitize up to 400 glass slides per hour without human intervention. This intense automation is critical to handle escalating tissue workloads, making physical scanner installation the top budgetary priority for medical centers. The widespread clinical adoption of brightfield imaging configurations for standard diagnostic workflows is further boosting the segmental expansion in the global market. For instance, brightfield scanning units command 51.62% of the component market share because they match the exact visual parameters of traditional light microscopy used for gold standard hematoxylin and eosin staining. This immediate familiarity allows laboratories to transition smoothly to digital workflows without altering their established staining protocols. Because brightfield units provide reliable high-resolution digitization for the vast majority of routine biopsies, hospital networks prioritize purchasing these scanning systems, securing the segment's dominant revenue share.

On the other hand, the software and image management systems segment is expanding at the fastest rate and is estimated to progress at a CAGR of 14.4% during the forecast period in the global market, owing to a shift from simple pixel capture to sophisticated algorithmic image analysis and cloud database storage. For instance, software platforms are outpacing traditional hardware expansions with a sustained 6.63% compound annual growth rate as laboratories transition toward automated diagnostic assistance. Modern image management software no longer just displays digital slides; it actively runs parallel machine learning models to highlight micro metastases and automate cell counting. This structural shift from static image viewing to active computer-aided diagnostics compels medical networks to invest heavily in recurring software subscriptions and cloud enterprise licenses, driving the rapid growth of the segment. The critical demand for cloud-based tele-pathology networks and remote diagnostic capabilities is further boosting the expansion of the software and image management systems segment in the global market. According to infrastructure studies published by the Digital Pathology Association, the requirement to safely share multi-gigapixel slides across different geographic hospital sites forces laboratories to update legacy local servers to web-based image management platforms. These advanced platforms facilitate zero-latency image streaming, allowing remote specialists to review a virtual slide simultaneously from anywhere in the world. As hospital networks combine their operations into unified digital systems, the need for complex, compliant image management software grows exponentially, securing its position as the fastest-growing market segment.

By Application Insights

The telepathology segment commanded for 40.9% of the global market share in 2025. The growth of the telepathology segment in the global market can be credited to the systemic operational inefficiencies and geographical barriers inherent in traditional microscopic slide consultations. As per a comprehensive workforce study published by the Royal College of Pathologists, less than 3% of surveyed healthcare departments possess adequate full-time personnel to manage their routine pathology workloads. Telepathology resolves this labor bottleneck by allowing physical glass slides to be scanned locally and instantly reviewed by off-site experts, eliminating physical slide shipping delays. This digital accessibility maximizes the utility of existing medical staff and prevents diagnostic backlogs, making telepathology the primary application for whole slide imaging. The rapid development of regional and national digital consultation networks is further boosting the expansion of the telepathology segment in the global market. For instance, telepathology accounted for 40% of market revenues due to its role in driving cross-border medical collaborations and secondary opinions for complex cases. These integrated software networks allow rural community hospitals to connect directly with major academic medical centers for real-time diagnostic verification. Because establishing telepathology pathways yields an immediate return on investment by reducing patient turnaround times from days to minutes, healthcare systems heavily prioritize this application during digital transitions.

However, the immunohistochemistry segment is anticipated to register a CAGR of 8.2% during the forecast period in the global market, owing to the growing reliance on quantitative biomarker evaluations to guide targeted cancer therapies. The shift from subjective visual grading to automated, highly precise digital quantification of tumor antigens is further boosting the expansion of the immunohistochemistry segment in the global market. As per clinical data published in the Journal of Pathology Informatics, artificial intelligence algorithms applied to whole slide images achieve a 95% diagnostic concordance rate with expert human readers when scoring critical cancer biomarkers such as HER2, PD L1, and Ki-67. Traditional manual microscopic evaluations of these complex stains are often prone to interobserver variability, which can affect patient treatment eligibility. By utilizing whole slide scanning to run advanced image analysis software, laboratories eliminate human subjectivity and deliver reproducible, pixel-level quantitative scoring that improves diagnostic accuracy. The growing use of multiplexed immunohistochemistry staining techniques within precision oncology is further boosting the growth of this segment in the global market. For instance, the rising incidence of complex malignancies and the development of personalized companion diagnostics are accelerating the adoption of specialized digital assays. Advanced whole slide systems can capture multiple fluorescent or brightfield layers on a single tissue section, allowing researchers to map the precise spatial relationships of various immune cells within the tumor microenvironment. As biopharmaceutical companies increasingly require these sophisticated spatial profiles for clinical trials, the demand for whole slide imaging in immunohistochemistry applications expands rapidly.

By End-user Insights

The hospitals and clinics segment had 45.7% share of the global market in 2025. The primary driver of this hospital segment dominance is the integration of digital pathology systems into broader electronic health records to streamline clinical workflows. For instance, the clinical center segment is expanding at a robust 12.01% annual rate because hospitals utilize whole slide imaging to connect pathology data directly with patient medical histories, radiology reports, and oncology treatment plans. This complete digitization removes the historical isolation of the pathology lab, allowing multidisciplinary tumor boards to access high-resolution digital slides during treatment planning sessions. The resulting efficiency gains and reductions in diagnostic errors drive large hospital groups to invest heavily in central whole slide imaging systems. The urgent operational requirement to handle large numbers of chronic disease samples is further contributing to the expansion of the hospitals and clinics segment in the global market. Managing hundreds of thousands of physical glass slides each year creates immense archival and retrieval challenges for hospital staff. Implementing whole slide imaging allows these institutions to automate slide archiving, optimize space, and reduce the time required to retrieve historical patient slides from hours to seconds, reinforcing the clinical segment's market dominance.

On the other hand, the pharmaceutical and biotechnology companies segment is estimated to grow at a CAGR of 7.2% during the forecast period, owing to the integration of digital tissue analysis into modern drug discovery and development and the widespread use of whole slide imaging to automate preclinical toxicology screenings and safety evaluation protocols. As per operational documentation published by the Digital Pathology Association, biopharmaceutical companies process millions of tissue sections annually during animal safety studies to identify adverse drug reactions. Manually reviewing these massive tissue volumes under light microscopes creates an expensive bottleneck in the drug development pipeline. Whole slide imaging platforms resolve this delay by enabling high-throughput automated scanning and artificial intelligence screening, allowing research teams to quickly filter out toxic drug candidates and shorten preclinical timelines. The growing reliance on digital slide repositories to support international, multicenter clinical trial collaborations is further contributing to the segmental growth in the global market. For instance, whole slide imaging is central to modern biomarker discovery and large-scale digital tissue analysis in multi-center trials, where patient biopsies are collected from diverse geographic regions. Instead of shipping fragile glass slides to a central core laboratory, research sites digitize specimens locally and upload them to secure cloud systems for immediate evaluation by distributed trial pathologists. This virtual centralization reduces data loss risks, ensures uniform scoring criteria, and accelerates regulatory approval timelines, prompting global pharmaceutical companies to rapidly adopt whole slide imaging systems.

REGIONAL ANALYSIS

North America Whole Slide Imaging Market Analysis

North America occupies the premier position within the global digital slide landscape, acting as the primary hub for technological integration and large-scale laboratory automation. The North American regional sector is heavily anchored by the United States market, which reached an independent valuation of 0.41 billion American dollars. This dominant market footprint is primarily driven by the systematic regulatory clearance of advanced digital pathology systems for primary clinical diagnostics. For instance, the United States Food and Drug Administration has granted clearances to major digital pathology platforms, allowing healthcare networks to replace traditional manual microscopes completely. Furthermore, the regional market status is bolstered by an extensive network of national cancer centers and biopharmaceutical hubs that utilize whole slide scanners to accelerate high-throughput oncology research and companion diagnostic development, cementing its leading position.

Europe Whole Slide Imaging Market Analysis

Europe functions as a highly progressive territory within the global digital diagnostic landscape, guiding the adoption of virtual slide architectures across the continent. The European market represents the second largest share globally, driven by widespread institutional funding and national healthcare digitization. The core driving force behind this market strength is the systematic implementation of structured laboratory efficiency protocols designed to counter rising operating costs and specialist shortages. European pathology networks are increasingly investing in multi-rack brightfield scanners to handle immense daily biopsy volumes seamlessly. Additionally, the region features highly robust data infrastructure networks and clear legal guidelines regarding digital patient records, which allow large hospital groups to establish secure, centralized digital image repositories without facing significant compliance obstacles.

Asia Pacific Whole Slide Imaging Market Analysis

Asia Pacific holds the position of the fastest-expanding geographic market within the global digital pathology sector, functioning as the primary driver of rapid digital workflow adoption and scanner sales. The Asia Pacific regional market is expanding at the highest rate worldwide, posting a promising CAGR for the forecast period. This rapid acceleration is primarily fueled by a critical demographic deficit, particularly in major nations like China and India, where there is an acute shortage of certified histopathologists relative to vast population bases. This deficit forces major tier 3 hospitals to deploy high-capacity whole slide scanners to capture digital representations of tissue specimens instantly. These digitized files are then transmitted through expansive telepathology networks, allowing a small number of urban specialists to serve remote rural clinics.

Latin America Whole Slide Imaging Market Analysis

Latin America represents an emerging and rapidly consolidating territory within the global digital slide landscape, with regional performance tied closely to private medical investments. The Latin American whole slide imaging industry is primarily driven by healthcare developments in Brazil and Mexico, which constitute the largest slice of South American revenue. The dominant factor for the technology in this region is the rapid consolidation of independent diagnostic laboratories into massive corporate diagnostic networks. These multi-site healthcare corporations utilize high-throughput digital scanning systems to centralize their pathology expertise in major metropolitan offices, reducing the overhead costs of maintaining physical laboratories in every branch. This corporate centralization helps mitigate the logistical challenges of shipping fragile glass slides across vast geographic distances.

Middle East and Africa Whole Slide Imaging Market Analysis

The Middle East and Africa occupy a developing position within the global digital pathology ecosystem, focusing on modernizing laboratory infrastructure to bridge substantial access gaps. The regional market status is characterized by targeted investments in public-private hospital partnerships, particularly within the Gulf Cooperation Council nations and South Africa. The primary driver of adoption is the urgent clinical requirement to manage complex infectious diseases and rising oncological cases with limited specialized personnel. By installing automated slide scanners in major regional reference laboratories, these countries can leverage telepathology pathways to connect local technicians with international subspecialists. This digital outreach significantly shortens patient diagnostic turnaround times and improves primary diagnostic accuracy across underserved provinces.

COMPETITIVE LANDSCAPE

The competition within the whole slide imaging market is characterized by intense technological rivalries among global medical device conglomerates, established diagnostics firms, and agile software start-ups. As laboratories shift from traditional light microscopes to fully virtualized workflows, the competitive pressure has transitioned from simple physical scanning speed to the depth of the software ecosystem. Companies compete aggressively to deliver integrated solutions that encompass automated tissue handling, high-resolution optics, cloud archival infrastructure, and machine learning analytics.

This dynamic creates a highly consolidated top-tier market structure where a few prominent players control the core clinical installation footprints due to their robust regulatory approvals. However, the software layer remains highly fragmented, with numerous specialized artificial intelligence firms introducing novel algorithms for specific cancer tracking. This balance forces major hardware manufacturers to continuously update their platforms into open environments that can host third-party diagnostic tools, shaping a competitive landscape centered on system flexibility, data security, and clinical validation.

KEY MARKET PLAYERS

Companies playing a dominating role in the global whole slide imaging market profiled in this report are

- Philips

- Siemens

- Roche Diagnostics

- Positron Corporation

- Agfa-Gevaert N.V.

- CardiArc Ltd.

- Digirad Corporation

- Gamma Medica Inc.

- GE Healthcare

- Leica Biosystems

- Hologic Inc.

- Leica Microsystems GmbH

- Nikon Corporation

- Visiopharm

- 3Dhistech

- Hamamatsu Photonics KK

- Indica Labs

TOP PLAYERS IN THE MARKET

- Leica Biosystems operates as a vital contributor to the development of automated glass slide digitization by providing high-speed scanning hardware and companion image management platforms. The company focuses heavily on streamlining anatomic pathology workflows to eliminate diagnostic delays in clinical laboratories. To strengthen its position in the market, the enterprise recently rolled out its next-generation scanning hardware alongside an artificial intelligence-powered quality control software platform. This system automatically identifies common scanning artifacts and focus discrepancies in real time, reducing the need for costly manual repeat scans and establishing a highly integrated computational environment for oncology research.

- Philips contributes extensively to the market through the engineering of enterprise-tier digital pathology infrastructure designed to support large hospital networks during complete digital transformations. The company focuses on bridging the gap between hardware scanning and secure cloud networks to optimize cross-institutional laboratory collaboration. To expand its market footprint, the organization recently introduced a fully cloud-enabled version of its core digital pathology solution integrated with global public cloud web services. This architectural advancement allows pathologists to securely stream, archive, and manage multi-gigapixel virtual slides from anywhere without relying on complex on-premises server infrastructure.

- Roche Diagnostics significantly impacts the market by merging advanced digital slide hardware with highly specialized companion diagnostic assays and open computational pathology environments. The company works to transform standard tissue specimens into highly predictive data assets that support modern targeted clinical oncology workflows. The enterprise has recently expanded its digital ecosystem by integrating a wide range of specialized biomarker analysis algorithms into its cloud software platform. These machine learning pipelines assist clinical teams in evaluating complex tissue structures, making the firm a central coordinator for precision medicine applications and automated oncology screening.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key market participants in the whole slide imaging market employ distinct strategic blueprints to accelerate widespread institutional adoption and secure long-term growth. The primary strategy centers on expanding artificial intelligence software integrations to transition raw digital slides into active diagnostic tools. Leading firms actively collaborate with software developers to embed deep learning models into their native image management platforms, enabling automated micro metastasis screening and cell counting.

Another prominent strategy involves transitioning legacy local server networks to secure cloud-based subscription models, allowing laboratories to scale their data architectures without high upfront IT costs. Furthermore, companies focus heavily on obtaining regulatory clearances across different countries to validate their systems for primary clinical diagnostics rather than research use only. Finally, manufacturers emphasize open standard hardware interoperability, engineering scanners that can output files in universally accessible formats like DICOM to prevent customer lock-in and capture multi-site hospital contracts.

GLOBAL WHOLE SLIDE IMAGING MARKET NEWS

- In June 2025, Leica Biosystems unveiled its advanced digital pathology suite at the European Congress on Digital Pathology, introducing high-performance brightfield and multimodal scanning hardware to support translational medicine workflows.

- In January 2026, Leica Biosystems launched the compact Aperio CS5 scanner, a low to medium-volume whole slide imaging system designed to support affordable digital transformation in space-constrained research laboratories.

- In January 2026, Philips received the Global Enabling Technology Leadership Award in Digital Pathology from Frost and Sullivan, validating its long-term technical contributions and cloud scaling initiatives within the industry.

- In March 2026, Philips expanded its digital pathology portfolio by launching the cloud-enabled Philips IntelliSite Pathology Solution on HealthSuite powered by Amazon Web Services to simplify enterprise data management.

- In March 2026, Leica Biosystems introduced the next-generation Aperio GT Elite scanner, paired with artificial intelligence-powered quality control software in the United States to automate artifact detection during active slide processing.

MARKET SEGMENTATION

This research report on the global whole slide imaging market has been segmented and sub-segmented based on product, application, end-user, and region.

By Product

- Hardware

- Scanners

- Viewers

- Image Management System

- Software

- Service

By Application

- Telepathology

- Cytopathology

- Immunohistochemistry

- Hematopathology

- Cancer

- Cardiology

By End-User

- Biotechnology and Pharmaceutical Companies

- Academic and Research Institutes

- Hospitals and Clinics

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the global whole slide imaging market?

The global whole slide imaging market involves digitizing glass slides for remote viewing, analysis, and sharing in pathology, diagnostics, and research

2. What drives growth in the global whole slide imaging market?

Growth stems from rising cancer incidence, digital pathology adoption, AI integration, telepathology, and increasing healthcare infrastructure investments worldwide

3. Which regions lead the global whole slide imaging market?

North America dominates, especially the U.S., due to early adoption and infrastructure, followed by Europe, with Asia-Pacific exhibiting rapid growth prospects

4. What are major applications of whole slide imaging?

Applications include digital pathology for cancer diagnostics, telepathology, research, and drug development processes

5. How does AI influence the whole slide imaging market?

AI enhances image analysis, diagnostic accuracy, quantification, and workflow automation, boosting overall market growth

6. What are the key benefits of whole slide imaging?

Enhanced diagnostic accuracy, remote access, improved workflow, digital archiving, and collaboration are vital benefits

7. What challenges does the market face?

High equipment costs, need for specialized training, regulatory approval barriers, and data security concerns

8. How is telepathology impacting the market?

It enables remote diagnosis and consultation, expanding access and speeds up disease detection and treatment decisions

9. What is the future outlook for the market?

The market is forecast to grow significantly, driven by technological innovations, increasing healthcare needs, and digital transformation in pathology

10. How does the Asia-Pacific market compare?

Asia-Pacific is the fastest-growing region, with expanding healthcare infrastructure and rising awareness of digital pathology

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com