- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

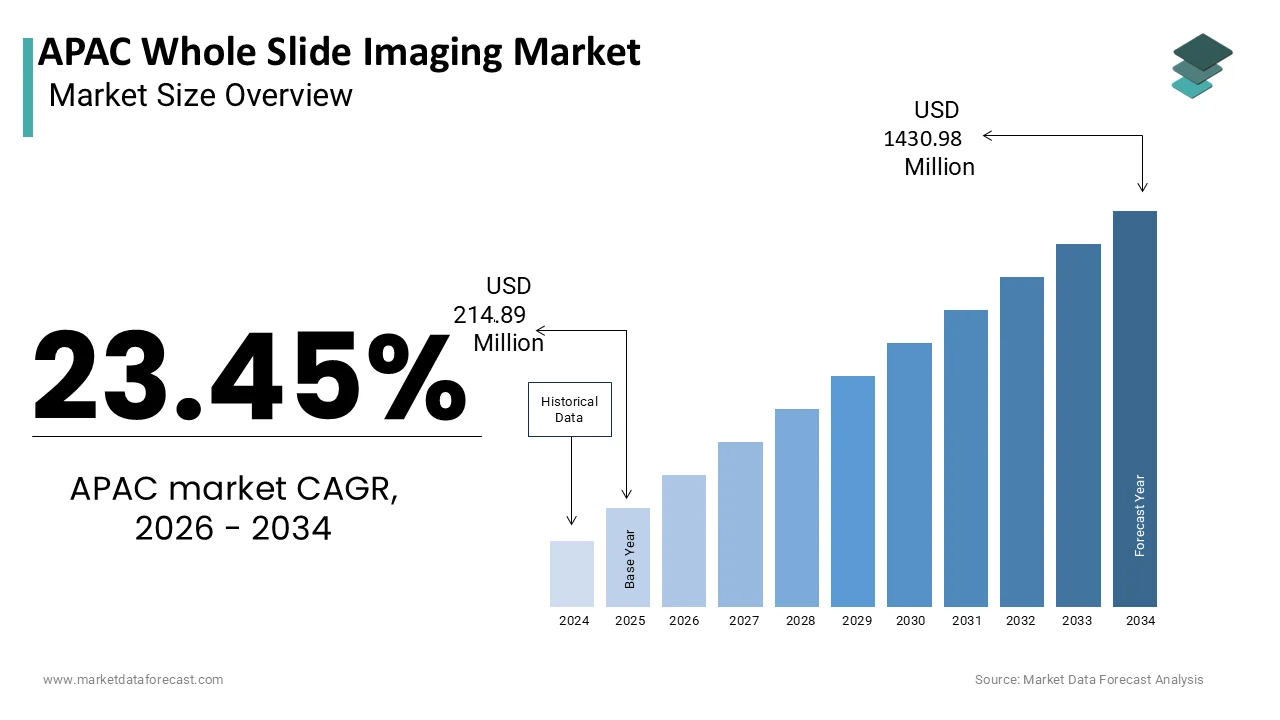

Market Size, 2025

$214.89 MnMarket Estimate, 2026

$265.28 MnMarket Forecast, 2034

$1,430.98 MnCAGR, 2026–2034

23.45%APAC Whole Slide Imaging Market Size

The APAC Whole Slide Imaging Market Size was valued at USD 214.89 Million in 2025, is expected to have 23.45% CAGR from 2026 to 2034 and be worth USD 1430.98 Million by 2034 from USD 265.28 Million in 2026.

Whole Slide Imaging (WSI), known as digital pathology, refers to the process of converting glass slides into digital images using high-resolution scanners. These images are then used for diagnostic, educational, and research purposes in pathology labs, hospitals, and academic institutions. In the Asia-Pacific (APAC) region, the adoption of WSI is gaining momentum due to the increasing burden of chronic diseases, rising demand for precision diagnostics, and growing investments in healthcare infrastructure.

The expansion of telepathology services, especially in rural and underserved areas, has further fueled the need for efficient imaging systems that enable remote diagnosis and expert consultation. Countries like Japan, South Korea, and Australia have been at the forefront of this transition, driven by strong regulatory support and advanced healthcare ecosystems. Meanwhile, emerging economies such as India and China are witnessing a surge in demand due to increasing cancer prevalence and government initiatives aimed at modernizing diagnostic workflows.

MARKET DRIVERS

Increasing Incidence of Chronic Diseases Across APAC

One of the key drivers fueling the growth of the APAC Whole Slide Imaging (WSI) market is the rising incidence of chronic diseases such as cancer, diabetes, and cardiovascular disorders. According to the World Health Organization (WHO), non-communicable diseases (NCDs) account for over 60% of all deaths in the Asia-Pacific region. Globocan reported that in 2022, approximately 9.8 million new cancer cases were diagnosed in Asia, accounting for nearly 50% of the global total. This growing disease burden necessitates more efficient, accurate, and scalable diagnostic tools, which WSI provides by enabling rapid, high-resolution imaging of tissue samples.

In countries like China and India, where patient volumes are exceptionally high, traditional microscopy often leads to diagnostic bottlenecks. The ability of WSI to streamline pathology workflows, reduce manual errors, and facilitate remote consultations makes it an essential tool in managing large caseloads.

Expansion of Telepathology Services in Rural and Remote Areas

Another significant driver of the APAC Whole Slide Imaging (WSI) market is the growing deployment of telepathology services in rural and remote regions. Many APAC countries face disparities in healthcare access, particularly in pathology diagnostics. The digitization of pathology through WSI allows for seamless image transmission to centralized diagnostic hubs or experts located elsewhere, overcoming geographical barriers. For instance, in Australia, where vast distances separate patients from specialists, the Royal College of Pathologists of Australasia reported that telepathology usage increased by 25% in the last two years, largely due to WSI implementation. Moreover, the Philippines Department of Health launched a national telepathology initiative in 2023, which is aiming to integrate WSI into regional hospitals to improve diagnostic efficiency and reduce reliance on overseas testing. In addition to accessibility, WSI supports second-opinion consultations and multi-disciplinary tumor board discussions, enhancing diagnostic accuracy. As per the Japanese Society of Pathology, digital slide sharing among hospitals in Japan increased inter-laboratory diagnostic consistency by over 30%.

MARKET RESTRAINTS

High Initial Investment and Maintenance Costs

A major restraint affecting the growth of the APAC Whole Slide Imaging (WSI) market is the high initial investment required for system acquisition, installation, and ongoing maintenance. Additionally, ancillary costs such as software licenses, cloud storage, and IT infrastructure upgrades add to the financial burden. For example, in Thailand, the Ministry of Public Health reported that only 12% of public hospitals could afford full-scale digital pathology implementations due to budget constraints. Even in more developed markets like South Korea, smaller clinics and independent laboratories struggle to justify the expense without clear short-term returns. Moreover, ongoing maintenance and training expenses pose additional challenges. A study published by the Asian Journal of Pathology indicated that annual maintenance contracts for WSI equipment can range from USD 15,000 to USD 30,000 per unit. As per the Indian Institute of Public Health, many pathology labs in India cited financial limitations as the primary reason for delaying digital transformation.

Regulatory and Reimbursement Challenges

Regulatory complexities and inconsistent reimbursement policies represent another critical challenge impeding the expansion of the APAC Whole Slide Imaging (WSI) market. Unlike the United States and Europe, where WSI systems have received clear regulatory approvals and partial reimbursement coverage, the APAC region lacks a unified framework. As per the Therapeutic Goods Administration (TGA) of Australia, while some WSI devices have been cleared for diagnostic use, there remains ambiguity regarding their inclusion under national insurance schemes. In China, despite the rapid technological advancements, the National Medical Products Administration (NMPA) has yet to establish standardized guidelines for the clinical validation of WSI platforms. India presents another case where regulatory clarity is still evolving. The Central Drugs Standard Control Organization (CDSCO) has not yet classified WSI systems under a definitive regulatory category, leading to procurement hesitancy among hospitals.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence with WSI Platforms

One of the most promising opportunities in the APAC Whole Slide Imaging (WSI) market is the integration of artificial intelligence (AI) to enhance diagnostic accuracy and efficiency. AI-powered image analysis tools are being increasingly adopted to detect anomalies in tissue samples, automate pattern recognition, and assist pathologists in decision-making. In Japan, companies such as Sysmex and Olympus have partnered with AI developers to create intelligent diagnostic modules that can identify cancerous cells with greater precision than manual methods. Clinical trials conducted by the University of Tokyo in 2023 demonstrated that AI-enhanced WSI systems achieved a 96% accuracy rate in detecting prostate cancer, surpassing conventional pathology assessments. India has also seen a surge in AI-based pathology startups. As per NITI Aayog, the Indian government's policy think tank, AI-enabled diagnostic platforms are expected to address the shortage of trained pathologists by automating preliminary screenings. In a pilot program led by the All India Institute of Medical Sciences (AIIMS), AI-assisted WSI reduced diagnosis time by nearly 50% in cervical cancer screening.

Growing Government Initiatives for Digital Health Infrastructure Development

Government-led digital health initiatives across the Asia-Pacific region are creating a conducive environment for the expansion of Whole Slide Imaging (WSI) technologies. Several APAC countries have introduced national programs aimed at modernizing healthcare infrastructure and promoting digital diagnostics. For instance, in 2022, the Indian government launched the Ayushman Bharat Digital Mission (ABDM), which includes provisions for integrating digital pathology into the national health ecosystem. According to the Ministry of Health and Family Welfare, ABDM aims to connect 150,000 health facilities across India by 2025, facilitating seamless exchange of diagnostic data, including digital pathology reports. Australia’s Digital Health Cooperative Research Centre (DH CRC) has also funded several WSI-related projects aimed at enhancing rural pathology services. As per the Australian Institute of Health and Welfare, these initiatives have already led to a 35% increase in digital pathology utilization across regional healthcare centers.

MARKET CHALLENGES

Data Storage and Management Complexity

A significant challenge confronting the APAC Whole Slide Imaging (WSI) market is the complexity associated with data storage, management, and cybersecurity. WSI generates extremely large file sizes, often exceeding several gigabytes per slide, which places substantial demands on storage infrastructure and network bandwidth. According to IDC, a single whole slide image can range from 1 GB to 5 GB in size, and a medium-sized pathology lab processing 100 slides daily would generate around 15 terabytes of data annually. Managing such vast volumes of data requires robust cloud or on-premise storage solutions, which many healthcare providers in the APAC region are not fully equipped to handle.

In developing economies like Indonesia and the Philippines, where IT infrastructure in hospitals is still evolving, the adoption of WSI is hindered by inadequate data center capabilities and unreliable internet connectivity. As per the ASEAN Secretariat, less than 40% of hospitals in Southeast Asia have implemented enterprise-grade data management systems compatible with digital pathology workflows. Even in technologically advanced countries like South Korea, concerns about data security persist. Additionally, compliance with data privacy regulations adds another layer of complexity. In Australia, adherence to the Privacy Act 1988 and the Notifiable Data Breaches (NDB) scheme necessitates stringent encryption and access control measures.

Lack of Skilled Professionals and Training Programs

A critical challenge impeding the growth of the APAC Whole Slide Imaging (WSI) market is the shortage of skilled professionals and the limited availability of structured training programs in digital pathology. The transition from conventional microscopy to digital imaging requires pathologists, laboratory technicians, and IT staff to acquire new competencies in operating WSI systems, interpreting digital images, and integrating them with electronic health records (EHRs). Even in technologically advanced nations like Japan, the adoption of digital pathology is hampered by resistance to change and insufficient training frameworks. The Japanese Society of Pathology promoted that only a handful of residency programs include comprehensive WSI training modules. As per the University of Hong Kong, addressing this skills gap will require collaborative efforts between governments, academic institutions, and industry stakeholders to develop standardized curricula and hands-on training programs.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, End-User and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | China, India, Japan, South Korea, Australia, New Zealand, Thailand, Indonesia, Philippines, Vietnam, Singapore, Rest of APAC. |

| Market Leader Profiled | Philips, Siemens, Positron Corporation, Agfa-Gevaert N.V., CardiArc Ltd., Digirad Corporation |

SEGMENTAL ANALYSIS

By Product Insights

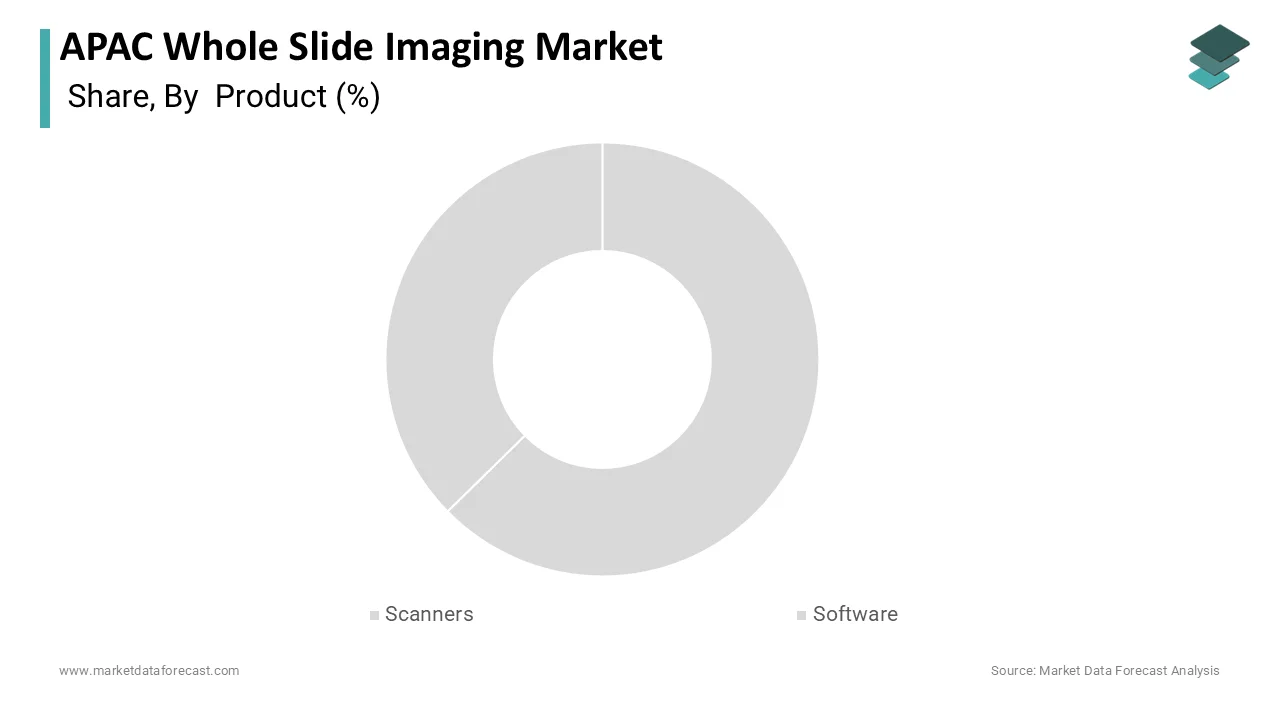

The scanners segment was the largest in the APAC Whole Slide Imaging (WSI) market by accounting for 38.3% of share in 2025 with the high-resolution scanners play in digitizing pathology workflows. One key driver of this segment's growth is the increasing integration of AI-assisted diagnostics with WSI scanners. Additionally, the Japanese Ministry of Health reported that over 65% of tertiary hospitals in Japan have adopted digital pathology scanners as part of their national telepathology initiative. Another factor is the growing need for automation in histopathology labs, especially in countries like China and India where patient volumes are surging.

The software segment is projected to grow with a CAGR of 27.4% during the forecast period due to the rising demand for advanced image analysis tools powered by artificial intelligence and machine learning. Moreover, the integration of WSI software with hospital information systems (HIS) and electronic health records (EHRs) is enhancing data interoperability and workflow efficiency. A report by Deloitte indicated that 70% of Australian pathology labs using integrated WSI software experienced a reduction in turnaround time for diagnostic reports.

By Application Insights

The cancer diagnostics application segment held 42.3% of the APAC Whole Slide Imaging (WSI) market share in 2025due to the rising incidence of various cancers across the region, particularly in densely populated countries like China and India. In China, the National Cancer Center reported that annual cancer diagnoses exceeded 4 million in 2023, prompting widespread adoption of digital pathology for faster and more accurate diagnostics. Similarly, in India, the Indian Council of Medical Research (ICMR) noted a 12% increase in cancer cases between 2020 and 2023, reinforcing the urgency for scalable diagnostic solutions. The integration of WSI with AI-powered analytics has further enhanced early detection capabilities. Clinical trials conducted by the University of Tokyo found that AI-enhanced WSI achieved a 96% accuracy rate in identifying malignant cells, significantly improving diagnostic reliability.

The telepathology segment is lucratively to grow with a projected CAGR of 28.7% in the next coming years. This rapid growth is primarily fueled by the expansion of digital health infrastructure and the increasing demand for remote diagnostic services in underserved regions. Furthermore, the adoption of cloud-based WSI platforms is enabling seamless image sharing and collaborative diagnosis across borders.

By End-User Insights

The hospitals and clinics segment was accounted in holding 45.3% of the APAC Whole Slide Imaging (WSI) market share in 2025 with the rising burden of chronic diseases and the increasing adoption of digital pathology in diagnostic workflows. In China, the National Health Commission reported that more than 40% of tertiary hospitals had implemented digital pathology systems by 2023, supported by government incentives under the "Healthy China 2030" initiative. Similarly, in India, the Ministry of Health and Family Welfare observed a 35% increase in WSI adoption among large private hospitals between 2021 and 2023, driven by the need for faster and more accurate diagnostics. The integration of WSI with hospital information systems (HIS) has also improved workflow efficiency. Additionally, the expansion of telepathology services in rural and semi-urban areas is strengthening the role of hospitals in driving WSI adoption.

The academic and research institutes segment is likely to grow with a CAGR of 29.3% during the forecast period. According to the University Grants Committee of Hong Kong, digital pathology is now a core component of postgraduate pathology training, with over 80% of residency programs incorporating WSI-based case studies. In Japan, the University of Tokyo reported a 40% increase in WSI usage for biomedical research between 2021 and 2023, particularly in oncology and regenerative medicine. Government funding for research infrastructure is also playing a crucial role. The Australian Research Council (ARC) allocated AUD 15 million in 2023 for digital pathology projects aimed at advancing AI-based diagnostics. Meanwhile, in South Korea, the National Research Foundation (NRF) reported a 22% rise in WSI-related research publications between 2022 and 2023, indicating strong academic engagement.

COUNTRY LEVEL ANALYSIS

China was the largest contributor by holding 30.1% of the Whole Slide Imaging (WSI) market share in 2025due to the robust healthcare modernization efforts and increasing investments in digital pathology infrastructure. Additionally, the growing prevalence of cancer has accelerated the deployment of WSI for diagnostic applications. The National Cancer Center of China reported that annual cancer diagnoses exceeded 4 million in 2023, necessitating scalable and efficient diagnostic tools. Furthermore, the integration of artificial intelligence (AI) with WSI platforms has enhanced early detection capabilities. Clinical trials conducted by Peking Union Medical College Hospital showed that AI-assisted WSI improved breast cancer detection accuracy by 15% compared to traditional microscopy.

Japan was positioned second with 18.6% of the APAC Whole Slide Imaging (WSI) market share in 2025with its highly developed healthcare infrastructure and strong regulatory support for digital diagnostics. The aging population in Japan is a key driver of WSI adoption, as it increases the burden of chronic diseases such as cancer and cardiovascular disorders. Moreover, Japan’s emphasis on telepathology and multi-center collaborations has further expanded WSI usage. The Japanese Society of Pathology noted that digital slide sharing among hospitals increased inter-laboratory diagnostic consistency by over 30%.

India Whole Slide Imaging (WSI) market growth is likely to be driven by the rising cancer incidence, expanding healthcare infrastructure, and government-led digital health initiatives. According to the Indian Council of Medical Research (ICMR), cancer cases in India are projected to rise by 12% by 2025, which is reinforcing the need for scalable and accurate diagnostic tools. The launch of the Ayushman Bharat Digital Mission (ABDM) in 2022 has played a pivotal role in integrating digital pathology into the national health ecosystem. Private sector participation has also surged, with companies like Tata 1mg and Thyrocare investing heavily in digital pathology labs. As per NITI Aayog, AI-enabled diagnostic platforms are expected to address the shortage of trained pathologists by automating preliminary screenings.

Australia Whole Slide Imaging (WSI) market growth is driven by it’s well-developed healthcare system, robust regulatory framework, and increasing investments in telepathology services. Australia's focus on precision medicine and AI-assisted diagnostics has further propelled WSI adoption. The country's regulatory environment is also conducive to WSI adoption, with the Therapeutic Goods Administration (TGA) approving several WSI scanners for clinical use. As per the Office of the Chief Health Scientist, digital pathology is now recognized as a standard diagnostic tool in public health institutions.

South Korea Whole Slide Imaging (WSI) market growth is attributed to its advanced healthcare infrastructure, government-backed digital health initiatives, and increasing adoption of AI-integrated diagnostic systems. The National Cancer Center of South Korea reported that cancer diagnoses exceeded 200,000 cases annually, necessitating scalable imaging solutions. Clinical evaluations conducted at Seoul National University Hospital found that AI-assisted WSI improved gastric cancer detection accuracy by 20% compared to manual methods. The government’s “Korean New Deal” initiative includes substantial funding for digital healthcare transformation, with WSI being a key component. As per the Korea Health Industry Development Institute (KHIDI), investments in digital pathology infrastructure have grown by 16% annually since 2020.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Philips, Siemens, Positron Corporation, Agfa-Gevaert N.V., CardiArc Ltd., Digirad Corporation, Gamma Medica Inc., GE Healthcare, Hologic Inc., Leica Microsystems GmbH, Nikon Corporation, Visiopharm, 3Dhistech, Hamamatsu Photonics KK, and Indica Labs are a few of the companies playing a key role in the APAC whole slide imaging market profiled in this report.

The competition in the APAC Whole Slide Imaging (WSI) market is intensifying as key players strive to capture a larger share of the growing digital pathology ecosystem. With increasing demand for precision diagnostics and remote pathology services, companies are investing heavily in product innovation, strategic collaborations, and regional expansion. The market features a mix of established medical device manufacturers and emerging technology-driven firms, all vying to offer superior imaging solutions that integrate seamlessly with clinical workflows. A significant portion of the competition revolves around technological differentiation, particularly in AI-enabled image analysis and cloud-based storage systems. Additionally, vendors are focusing on building strong distribution networks and forming alliances with academic and research institutions to drive adoption. As healthcare institutions across the APAC region continue to modernize their diagnostic capabilities, the competitive environment remains dynamic, with continuous advancements shaping market dynamics and influencing vendor strategies.

Top Players in the Market

One of the leading players in the APAC Whole Slide Imaging (WSI) market is Leica Biosystems, a global provider of integrated pathology solutions. The company has a strong presence in the region, particularly in Japan, South Korea, and Australia, where it supplies high-resolution digital scanners and advanced image management systems. Leica’s commitment to innovation and its focus on integrating artificial intelligence with WSI platforms have positioned it as a key player in the digital pathology space. Its collaboration with academic institutions and healthcare providers supports the development of more accurate and efficient diagnostic workflows.

Another major contributor to the market is Olympus Corporation, known for its cutting-edge imaging technologies and end-to-end digital pathology solutions. Olympus has been instrumental in advancing telepathology services across the APAC region by offering scalable WSI systems tailored for both large hospitals and research centers. The company's emphasis on product reliability, user-friendly interfaces, and seamless integration with laboratory information systems has made its solutions highly sought after in clinical and academic settings.

Hamamatsu Photonics is also a dominant force in the WSI market, particularly in Japan and China. Renowned for its high-speed, high-resolution slide scanners, Hamamatsu has played a pivotal role in enabling digital transformation in pathology labs. The company actively collaborates with AI developers and healthcare institutions to enhance diagnostic accuracy and efficiency.

Top Strategies Used by Key Market Participants

A primary strategy adopted by leading players in the APAC Whole Slide Imaging (WSI) market is technology integration and innovation with artificial intelligence and cloud-based platforms. Companies are focusing on enhancing their imaging software to offer automated diagnostics, which improves accuracy and reduces manual workload. This approach not only enhances clinical outcomes but also strengthens competitive positioning in a rapidly evolving market.

Another key strategy is strategic partnerships and collaborations with academic institutions, healthcare providers, and AI developers. These alliances help companies gain insights into clinical needs, refine their products, and accelerate adoption across hospitals and research facilities. Collaborations also support data standardization and regulatory alignment, which is making digital pathology more accessible and acceptable in routine diagnostics.

The expansion into emerging markets is a critical growth driver. Major players are increasing their regional presence through localized distribution networks, training programs, and direct sales initiatives. The companies are strengthening their foothold in the APAC WSI market by targeting countries with rising disease burdens and improving healthcare infrastructure.

RECENT HAPPENINGS IN THE MARKET

In January 2024, Leica Biosystems launched an AI-powered digital pathology platform in collaboration with a Japanese research institute, aiming to improve cancer diagnostics through enhanced image analysis and faster reporting.

In March 2024, Olympus Corporation expanded its regional footprint by establishing a new digital pathology service center in Singapore, offering training, technical support, and consultation to hospitals adopting WSI technology.

In June 2024, Hamamatsu Photonics partnered with an Indian health-tech startup to develop localized digital pathology solutions tailored for rural healthcare settings, enhancing accessibility and affordability across underserved regions.

In September 2024, Philips Healthcare , a major player in digital diagnostics, introduced a cloud-based WSI system in China, designed to streamline data sharing and support multi-center pathology collaboration among hospitals.

In November 2024, Sysmex Corporation entered into a strategic alliance with a South Korean university hospital to co-develop AI-driven tools for early-stage cancer detection using whole slide imaging, reinforcing its commitment to innovation in diagnostic technologies.

MARKET SEGMENTATION

This research report on the apac whole slide imaging market has been segmented and sub-segmented into the following categories.

By Product

- Scanners

- Software

By Application

- Telepathology

- Cancer

By End-User

- Academic and Research Institutes

- Hospitals and Clinics

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC