Global Digital Pathology Market Size, Share, Trends & Growth Forecast Report - Segmented By Type (Human Digital Pathology & Animal Digital Pathology), Product (Scanners, Software, Communication Systems and Storage Systems), Application (Teleconsultation, Disease Diagnosis, Drug Discovery and Training and Education), End Users (Pharmaceutical and Biotechnology, Hospitals and Academic Institutes) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2025 to 2033

Global Digital Pathology Market Size

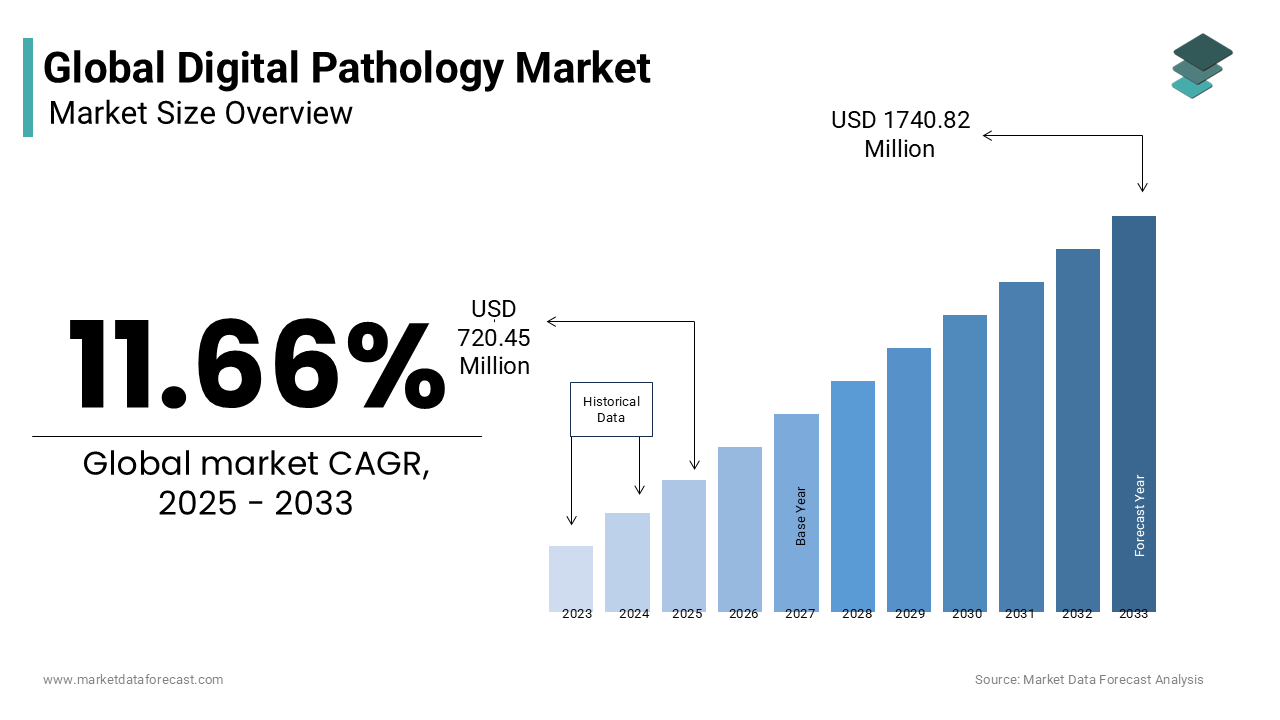

As per our analysis report, the global digital pathology market is projected to value USD 1740.82 million by 2033 from USD 720.40 million in 2025, growing at a CAGR of 11.66% during the forecast period. The size of the digital pathology market was valued at USD 645.17 million in 2024.

Digital pathology is a transformative shift in diagnostic medicine, leveraging high-resolution whole-slide imaging, artificial intelligence, and cloud-based data management to digitize tissue analysis. It enables pathologists to view, analyze, and share histopathological data remotely, improving diagnostic precision and workflow efficiency. As per the College of American Pathologists, over 70% of pathology laboratories in the United States have initiated at least partial digitization of their slide archives as of 2023, signaling a structural evolution in diagnostic infrastructure. The integration of digital pathology into routine clinical workflows has been further accelerated by regulatory endorsements, including the U.S. FDA’s clearance of digital pathology systems for primary diagnosis.

MARKET DRIVERS

Rising Global Burden of Cancer and Demand for Precision Diagnostics

The escalating global incidence of cancer is a pivotal factor propelling the growth of the Digital Pathology Market. According to the International Agency for Research on Cancer, an estimated 20 million new cancer cases were diagnosed worldwide in 2022. This surge necessitates scalable, accurate, and rapid diagnostic systems capable of handling vast volumes of tissue samples. Digital pathology addresses this demand by enabling concurrent review of slides by multiple specialists, reducing diagnostic turnaround times by up to 40%, as observed in a 2023 study conducted by the European Society of Pathology.

Advancements in Artificial Intelligence and Machine Learning Integration

The integration of digital pathology with artificial intelligence is revolutionizing diagnostic accuracy and operational efficiency, which is also accelerating the growth of the Digital Pathology Market. AI-powered algorithms can detect subtle histological patterns imperceptible to the human eye, significantly augmenting diagnostic confidence. These tools reduce inter-observer variability, a persistent challenge in traditional pathology, where diagnostic discordance rates can reach 15% for certain tumor types, as noted by the Archives of Pathology & Laboratory Medicine. Leading healthcare systems, including the NHS in the UK, have initiated pilot programs integrating AI-driven image analysis for prostate and colorectal cancer screening, reporting a 50% reduction in slide review time.

MARKET RESTRAINTS

High Capital Investment and Infrastructure Requirements

The substantial upfront costs and demanding infrastructural prerequisites are restraining the growth of the Digital Pathology Market. Many institutions in developing regions lack the bandwidth to support seamless image transmission; the International Telecommunication Union reports that only 47% of hospitals in sub-Saharan Africa have access to broadband speeds sufficient for real-time digital pathology workflows. These financial and technical barriers delay implementation in public healthcare systems where budget allocations remain constrained despite growing diagnostic demands.

Regulatory and Standardization Gaps Across Jurisdictions

The stringent regulations in the global interoperability and clinical adoption. While the U.S. FDA has approved several digital pathology platforms for primary diagnosis, equivalent clearances remain limited in regions such as Southeast Asia and Eastern Europe. As per the Global Harmonization Task Force, only 28 of 194 WHO member states had established formal regulatory frameworks for digital pathology systems as of 2023. This lack of harmonization complicates cross-border data sharing and multicenter research collaborations. Additionally, the absence of universal standards for image resolution, file formats, and quality control protocols leads to compatibility issues between vendors.

MARKET OPPORTUNITIES

Expansion of Telepathology in Underserved and Rural Regions

The diagnostic disparities in geographically isolated areas are solely to enhance the growth of the Digital Pathology Market. As per the World Health Organization, over 4.3 billion people globally lack access to essential pathology services, with sub-Saharan Africa and South Asia facing the most acute shortages fewer than 5 pathologists per million population in many countries. Telepathology enables remote consultation by allowing expert pathologists to review digitized slides from distant locations in real time. Similarly, the African Organisation for Research and Training in Cancer reports that telepathology initiatives in Kenya and Uganda have improved diagnostic accuracy by 45% in rural oncology centers.

Integration with Multimodal Data in Precision Medicine Platforms

The fusion of digital pathology with multi-omics and electronic health record (EHR) systems unlocks unprecedented potential in personalized medicine which will additionally propel the growth of the Digital Pathology Market. As per the National Institutes of Health, integrating histopathological imaging with genomic, proteomic, and clinical data enhances predictive modeling for treatment response and disease progression. For instance, the Cancer Genome Atlas project demonstrated that combining AI-analyzed tissue morphology with mutational profiles improved prognostic accuracy in glioblastoma by 38%. Major academic medical centers, including the Mayo Clinic, are deploying integrated digital pathology platforms that synchronize with EHRs by enabling real-time correlation of histological findings with patient histories and therapeutic outcomes.

MARKET CHALLENGES

Data Privacy, Security, and Ethical Concerns in Digital Slide Management

The digitization of sensitive histopathological data introduces cybersecurity and ethical challenges which hamper the growth of the Digital Pathology Market. These systems generate vast repositories of personally identifiable health information, making them prime targets for cyberattacks. According to the U.S. Department of Health and Human Services, healthcare data breaches affected over 49 million individuals in 2023, with ransomware attacks on hospital networks increasing by 87% compared to the previous year. However, a 2023 audit by the Ponemon Institute revealed that 62% of pathology departments lack dedicated cybersecurity protocols for digital slide archives. Furthermore, ethical dilemmas arise regarding patient consent for AI training on anonymized slides, as complete de-identification remains technically challenging.

Workforce Resistance and Skill Gaps in Digital Transition

The transition to digital pathology faces resistance from pathologists accustomed to conventional microscopy, which is also hampering the growth of the Digital Pathology Market. A 2023 survey by the Association for Molecular Pathology found that 44% of practicing pathologists in North America expressed concerns about eye strain, reduced tactile feedback, and diminished diagnostic confidence when using digital platforms. This skill gap delays adoption and limits effective utilization of advanced analytics. In Europe, the European Society of Pathology notes that fewer than 30% of pathologists have received certification in digital diagnostics, despite growing institutional investments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Product, Application, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Perkin Elmer, Inc., Definiens AG, Sectra AB, Koninklijke Philips N.V., G.E. Healthcare, InspirataCo.o, Ventana Medical Systems, Inc., Leica Biosystems, 3D-Histech Ltd, Hamamatsu Photonics and K.K., Digipath Co. |

SEGMENTAL ANALYSIS

By Type Insights

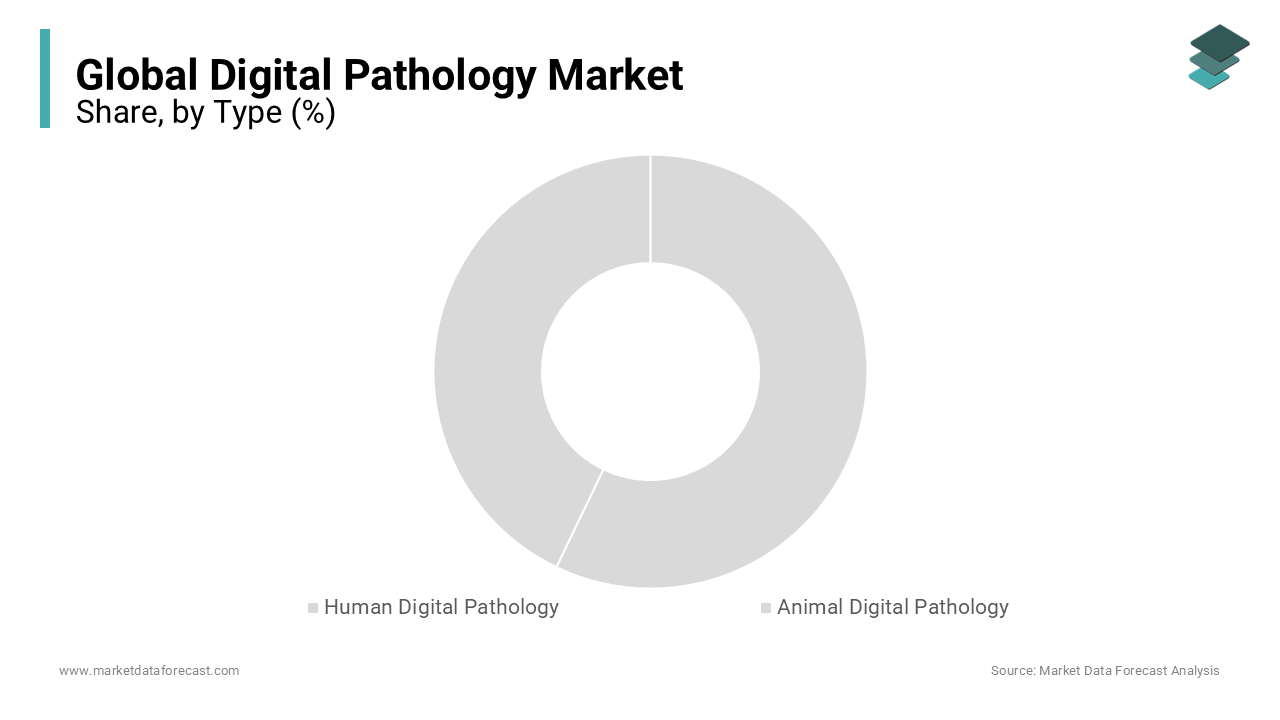

The human digital pathology segment was accounted in holding a significant share of the Digital Pathology Market with the escalating demand for cancer diagnostics and the integration of digital workflows in clinical medicine. This has prompted healthcare institutions to adopt digital pathology for primary diagnosis, second opinions, and tumor board reviews. Furthermore, regulatory advancements have accelerated adoption; the U.S. Food and Drug Administration granted full approval for whole-slide imaging in primary diagnosis in 2017, a milestone that catalyzed large-scale implementation across North American and European hospitals.

The animal digital pathology is projected to grow at a CAGR of 12.8% from 2025 to 2033 with the increasing reliance on veterinary clinical trials and comparative oncology research. Additionally, pharmaceutical companies are leveraging animal models in preclinical drug testing, where digital pathology enables high-throughput histopathological analysis. The One Health initiative emphasizes the interconnection between human, animal, and environmental health, which has further incentivized investment in veterinary digital diagnostics.

By Product Insights

The software segment held 38.2% ofthe Digital Pathology Market share in 2024 with the growing dependency on advanced image analysis algorithms and workflow management tools. Pathologists increasingly rely on software for AI-powered detection of malignancies, quantitative morphometry, and case prioritization. For instance, AI-based prostate cancer detection software developed by PathAI demonstrated a 94% sensitivity rate in multicenter validation studies, as published in The Lancet Digital Health in 2023.

The storage systems segment is anticipated to register a CAGR of 14.3% during the forecast period with the exponential growth in digital slide data generation. Cloud-based storage adoption in pathology has grown by 68% since 2020, as reported by the Cloud Security Alliance, due to its cost-efficiency and disaster recovery capabilities. Furthermore, hybrid storage models combining on-premise servers with off-site cloud backups are becoming standard in academic medical centers, ensuring uninterrupted access while meeting data sovereignty laws in regions like the EU under GDPR.

By Application Insights

The disease diagnosis segment was the largest and held 46.7% of the global digital pathology market share in 2024 with the clinical imperative to improve diagnostic accuracy and turnaround times in high-volume specialties such as oncology and nephropathology. Digital pathology enables concurrent multi-pathologist review, reducing diagnostic discrepancies. Additionally, the integration of digital pathology into primary diagnosis has gained regulatory legitimacy, with the FDA approving Philips IntelliSite Pathology Solution for full diagnostic use. Hospitals implementing digital diagnosis platforms report a 35% improvement in case throughput, as documented by the Mayo Clinic’s Department of Laboratory Medicine and Pathology.

The drug discovery segment is swiftly emerging with an expected CAGR of 15.1% throughout the forecast period with the increasing use of digital pathology in preclinical and translational research. Pharmaceutical companies are incorporating quantitative histopathology into toxicology and efficacy assessments by enabling precise measurement of drug effects on tissue architecture.

By End User Insights

The hospitals segment was the largest by capturing 52.4% of the digital pathology market share in 2024 with the integration of digital pathology into routine diagnostic workflows, particularly in oncology and surgical pathology departments. Large tertiary care centers are investing in enterprise-wide digital systems to streamline operations and support multidisciplinary tumor boards. Additionally, hospital mergers and the rise of integrated delivery networks are driving standardization across pathology departments, necessitating interoperable digital platforms.

The pharmaceutical and biotechnology sector is projected to grow with an expected CAGR of 14.9% in the coming years with the expanding role of digital pathology in clinical trial design and biomarker development. Biopharma firms are increasingly reliant on high-content tissue imaging to assess drug mechanisms and patient stratification. VENTANA DP 600 scanner, for example, is used across 80% of its global immuno-oncology trials to standardize slide evaluation, as stated in the company’s 2023 R&D report. Additionally, digital pathology enables centralized review of biopsy samples from multicenter trials, reducing inter-site variability.

REGIONAL ANALYSIS

North America Digital Pathology Market Insights

North America was the largest contributor in the global digital pathology market by holding 41.3% of share in 2024. The U.S. FDA’s 2017 approval of the first whole-slide imaging system for primary diagnosis has driven the rapid adoption of the implementation across academic and community hospitals. Additionally, high healthcare expenditure enables substantial investment in cutting-edge diagnostic technologies. The presence of leading technology vendors such as GE Healthcare, Leica Biosystems, and Proscia further strengthens the ecosystem, which is fostering innovation and clinical validation.

Europe Digital Pathology Market Insights

Europe was positioned second by occupying 28.7% of the Digital Pathology Market share in 2024, with strong academic research networks and cross-border collaborations in digital diagnostics. Countries like Germany, the UK, and the Netherlands have implemented national digitization strategies. The UK’s National Health Service Digital reported that 45% of pathology departments had adopted digital systems for secondary consultation by 2023. Regulatory alignment under the EU In Vitro Diagnostic Regulation (IVDR) has standardized device approvals, facilitating vendor entry and clinical integration. Moreover, the European Society of Pathology’s Digital Pathology Task Force has developed guidelines adopted in 18 countries, promoting best practices.

Asia Pacific Digital Pathology Market Insights

The Asia Pacific digital pathology market growth is anticipated to grow with rapid technological adoption and expanding healthcare access. Countries such as Japan, South Korea, and Australia lead in infrastructure development, with Japan’s Ministry of Health, Labour and Welfare approving multiple digital pathology systems for clinical use since 2020. In India, the government’s National Digital Health Mission has incentivized the digitization of medical records, including pathology reports, with over 150 hospitals participating in pilot imaging programs.

Latin America Digital Pathology Market Insights

Latin America digital pathology market is anticipated to grow lucratively in the coming years. Brazil and Mexico are at the forefront, driven by public-private partnerships and oncology-focused healthcare reforms. Brazil’s Ministry of Health launched a national telepathology initiative in 2022, connecting 30 regional hospitals with centralized pathology hubs, resulting in a 40% improvement in diagnostic turnaround for cervical and breast cancer, as documented by the Oswaldo Cruz Foundation. However, economic volatility and uneven healthcare funding constrain large-scale deployment.

Middle East & Africa Digital Pathology Market Insights

The Middle East and Africa Digital Pathology Market is anticipated to grow in the coming years. Gulf Cooperation Council (GCC) countries such as the UAE and Saudi Arabia are investing heavily in smart healthcare infrastructure. The UAE’s Ministry of Health and Prevention allocated $1.2 billion for digital health transformation between 2021 and 2025, including digital pathology integration in major hospitals.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Perkin Elmer, Inc., Definiens AG, Sectra AB, Koninklijke Philips N.V., G.E. Healthcare, Inspirata Co., Ventana Medical Systems, Inc., Leica Biosystems, 3D-Histech Ltd, Hamamatsu Photonics and K.K., and Digipath Co. are some of the major companies in the global digital pathology market.

The competition in the digital pathology market is intensifying as global technology providers and diagnostic firms race to capture emerging opportunities in precision medicine and telepathology. The landscape is characterized by rapid innovation, with companies differentiating through AI integration, scanner speed, and software intelligence rather than hardware alone. Established medical device manufacturers are competing with agile digital health startups that offer specialized AI algorithms and cloud-based platforms. Regulatory milestones, such as FDA and CE-IVD clearances, serve as key differentiators, influencing adoption in clinical settings. While Western markets remain mature, the Asia Pacific region is becoming a strategic battleground, with vendors tailoring solutions to diverse healthcare infrastructures.

Top Players in the Digital Pathology Market

Roche Diagnostics

Roche Diagnostics has emerged as a pivotal force in the digital pathology landscape across the Asia Pacific region, where it has intensified its focus on integrated diagnostic ecosystems. The company’s VENTANA DP 200 scanner and UNICORN software platform have been adopted in major cancer centers in Japan, South Korea, and Australia, enabling seamless slide digitization and AI-driven analysis. In 2023, Roche collaborated with the National Cancer Center Singapore to validate digital workflows for immunotherapy biomarker assessment, reinforcing its role in precision oncology. The company also launched a cloud-based image management system in India, tailored to support telepathology in decentralized hospitals.

Philips Healthcare

Philips Healthcare has established a robust footprint in the Asia Pacific digital pathology market through strategic partnerships and localized innovation. Its IntelliSite Pathology Solution, one of the first FDA-cleared end-to-end digital pathology platforms, is now operational in leading hospitals in Australia, Japan, and Malaysia. The company further strengthened its presence by launching a regional AI research hub in Singapore, focusing on developing algorithms for gastric and liver cancer detection prevalent in Asian populations. Philips has also collaborated with India’s Apollo Hospitals to scale digital pathology across multiple urban and semi-urban centers.

Canon Medical Systems

Canon Medical Systems has strategically expanded its influence in the Asia Pacific digital pathology market by leveraging its expertise in medical imaging and AI. Its DR. EX platform integrates whole-slide imaging with advanced analytics, gaining traction in academic and research institutions across Japan and South Korea. The company also initiated a collaboration with Australia’s Peter MacCallum Cancer Centre to develop AI models for early detection of colorectal cancer. Canon’s focus on speed, image fidelity, and seamless integration with existing PACS systems has positioned it as a preferred partner for institutions modernizing pathology workflows. Its continued investment in local R&D and regulatory approvals elevates its commitment to long-term growth in the region’s evolving digital diagnostics space.

Top Strategies Used by the Key Market Participants

Key players in the digital pathology market are deploying multifaceted strategies to consolidate their positions and drive innovation. Strategic partnerships with academic medical centers and biopharma firms enable real-world validation of digital platforms. Companies are heavily investing in artificial intelligence to enhance image analysis accuracy and automate diagnostic workflows. Product launches featuring high-throughput scanners and cloud-native software are accelerating digital transformation in pathology departments. Mergers and acquisitions are being leveraged to expand technological capabilities, particularly in AI and data analytics. Geographical expansion, especially in emerging markets across the Asia Pacific and Latin America, is supported by localized regulatory submissions and training initiatives. Additionally, vendors are focusing on interoperability with existing hospital IT systems by ensuring smooth integration into clinical ecosystems. These strategies collectively enhance scalability, regulatory compliance, and clinical utility, reinforcing competitive advantage.

RECENT MARKET HAPPENINGS

- In February 2024, F. Hoffman-La Roche Ltd announced a partnership with PathAI to develop artificial intelligence (AI) digital pathology algorithms for Roche’s Tissue Diagnostics business.

- In October 2023, Pramana and Gestalt announced the availability of an integrated AI-powered platform and digital pathology solutions, combining digital pathology, AI, image analysis, and DICOM into a streamlined, single, comprehensive offering.

- In October 2023, F. Hoffman-La Roche Ltd. announced its partnership with Ibex and Amazon Web Services to enhance the adoption of AI-enabled digital pathology solutions, which help diagnose breast and prostate cancer.

- In August 2023, PathAI announced the commercial launch of its product “AISight Digital Pathology Image Management System.”

- In 2023, Leica Biosystems announced the launch of its new digital pathology platform, the Aperio VERSA. The Aperio VERSA is a comprehensive digital pathology platform that offers a wide range of features, including whole-slide imaging, image analysis, and telepathology.

- In 2023, Roche Diagnostics launched its new digital pathology software, the NAVIFY Digital Pathology Platform. This cloud-based platform offers many features, including whole-slide imaging, image analysis, and telepathology.

- In 2022, Hamamatsu Photonics announced the launch of its new digital pathology scanner, the NanoZoomer S60. This high-speed scanner can scan whole slides in 15 seconds.

MARKET SEGMENTATION

This research report on the global digital pathology market has been segmented and sub-segmented based on type, product, application, end-user, and region.

By Type

- Human Digital Pathology

- Animal Digital Pathology

By Product

- Scanners

- Software

- Communication Systems

- Storage Systems

By Application

- Teleconsultation

- Disease Diagnosis

- Drug Discovery

- Training and Education

By End Users

- Pharmaceutical and Biotechnology

- Hospitals

- Academic Institutes

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

Who are the major players in the digital pathology market?

Perkin Elmer, Inc., Definiens AG, Sectra AB, Koninklijke Philips N.V., GE Healthcare, Inspirata Co., Ventana Medical Systems, Inc., Leica Biosystems, 3D-Histech Ltd, Hamamatsu Photonics and K.K., and Digipath Co. are a few of the companies playing a leading role in the global digital pathology market.

Does this report include the impact of COVID-19 on the digital pathology market?

Yes, we have included the impact of COVID-19 on the global digital pathology market in this report.

Which region will lead the digital pathology market in the future?

The global digital pathology market size is estimated to grow by USD 1740.82 million by 2033.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com