Global Biopharmaceuticals Market Size, Share, Trends & Growth Forecast Report - Segmented By Product Type (Monoclonal Antibodies (mAb), Erythropoietin, Biotech Vaccines, Recombinant Human (RH) Insulin, Granulocyte colony-stimulating factor (G-CSF), Interferon and Human Growth Hormones (HGH)), Therapeutic Type (Neurology, Infectious diseases, Diabetes, Oncology, Cardiovascular and Other Therapeutic Areas) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2024 to 2033

Global Biopharmaceuticals Market Summary

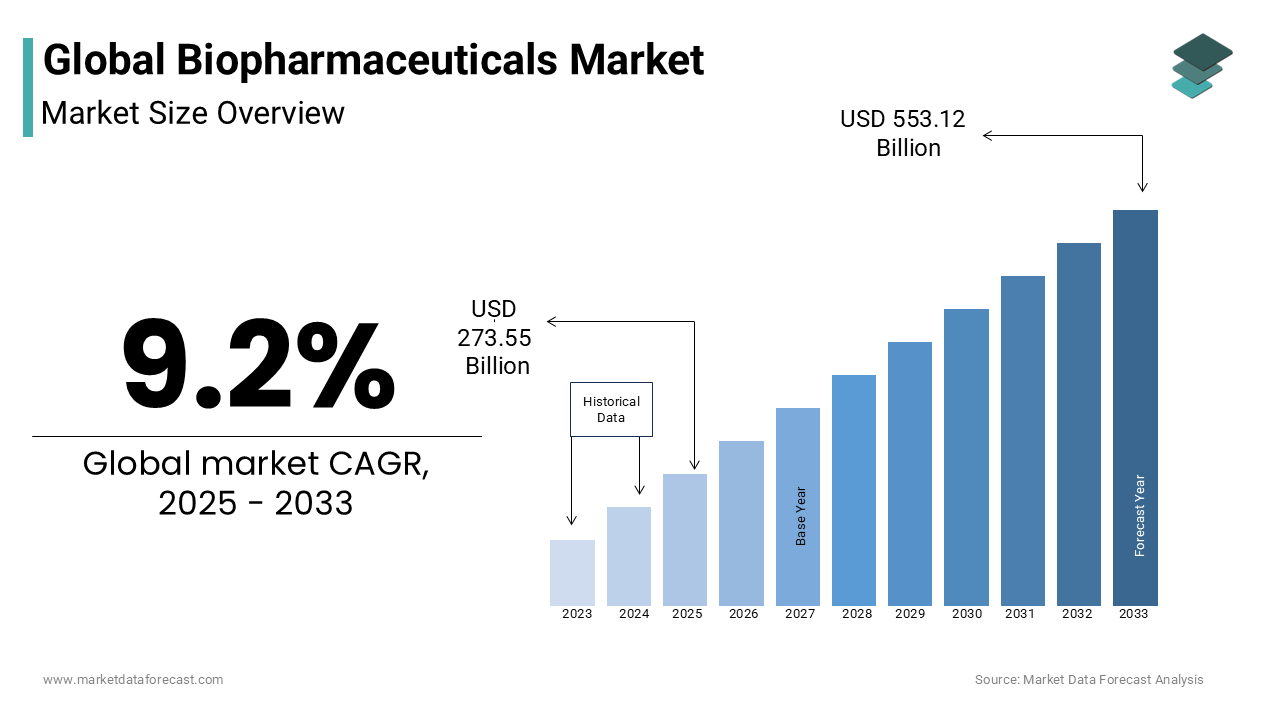

The global biopharmaceuticals market was valued at USD 250.50 billion in 2024 and is projected to reach USD 553.12 billion by 2033, growing at a CAGR of 9.2% from 2025 to 2033. The growth of the global biopharmaceuticals market is driven by the rising prevalence of chronic and infectious diseases, increasing adoption of biologics for targeted therapies, and continuous advancements in biotechnology and drug development. Strong investments in R&D, coupled with the expansion of biosimilars and personalized medicine, are further accelerating market expansion.

Key Market Trends

- Growing adoption of monoclonal antibodies (mAbs) as frontline biologic therapies.

- Rising demand for oncology-focused biopharmaceuticals due to increasing cancer incidence.

- Expanding pipeline of biosimilars to enhance treatment affordability.

- Increasing integration of genomics, proteomics, and AI-driven drug discovery.

- Rising collaborations between biotech firms and pharmaceutical giants for innovation.

Segmental Insights

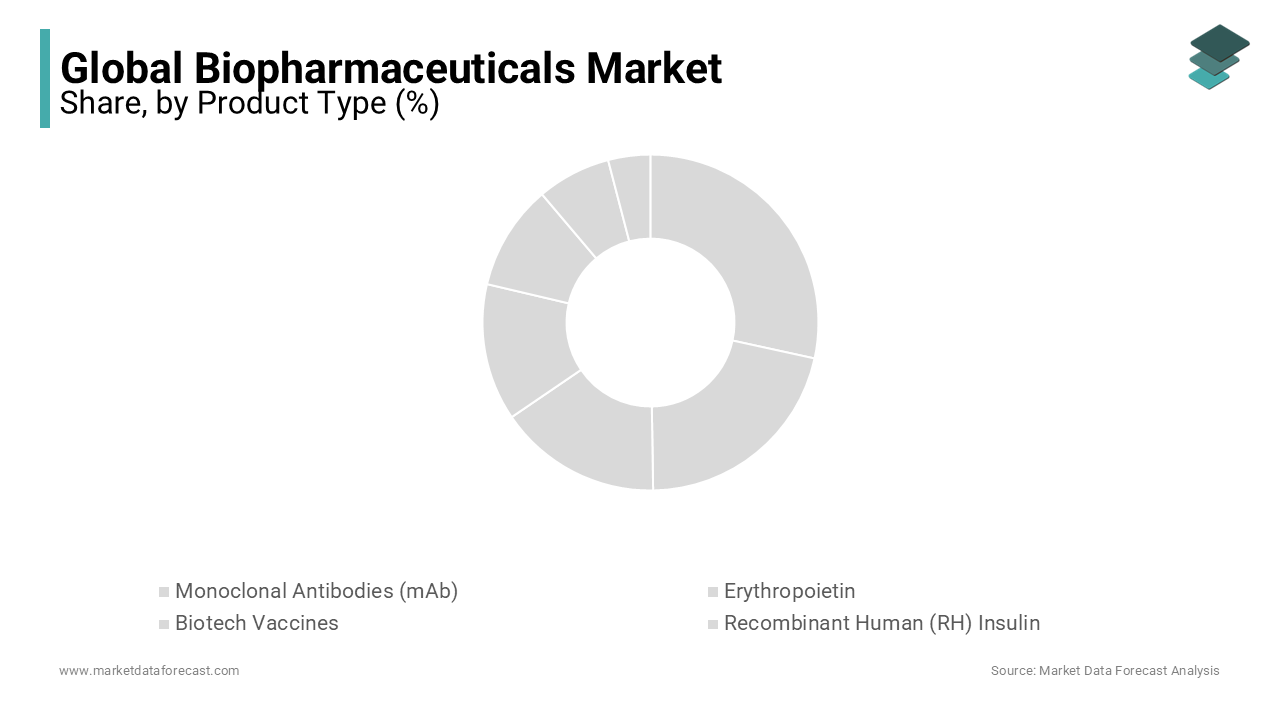

- Based on product type, the monoclonal antibodies (mAbs) segment led the global biopharmaceuticals market with 43.2% share in 2024, supported by their efficacy in autoimmune and cancer treatments.

- Based on therapeutic type, the oncology segment dominated with 48.2% share in 2024, reflecting the growing reliance on biologics for cancer therapy.

Regional Insights

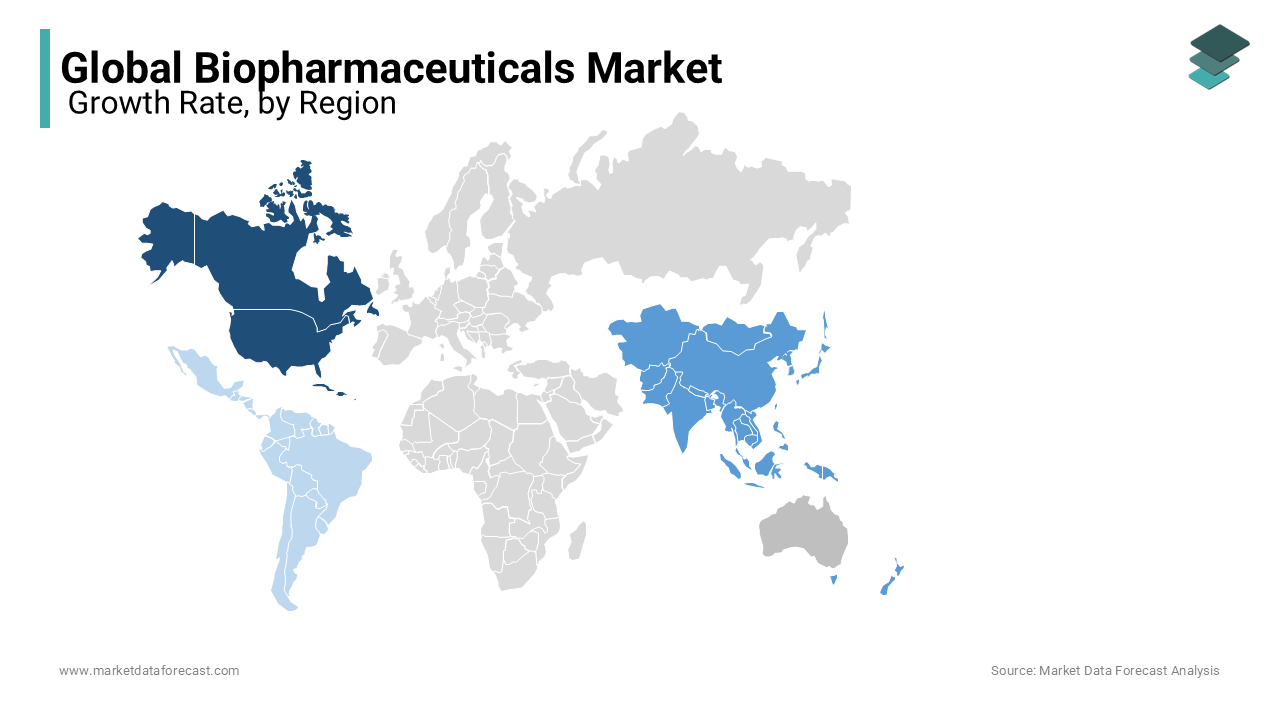

- North America dominated the global biopharmaceuticals market in 2024 with 41.2% share, supported by advanced healthcare infrastructure, high R&D investments, and early adoption of innovative biologics.

- Europe is experiencing steady growth, driven by biosimilar adoption and supportive regulatory frameworks.

- Asia-Pacific is projected to record the fastest CAGR, fueled by increasing healthcare spending, expanding biotech sectors, and rising clinical trial activities.

- Latin America is emerging as a growth market, supported by improved healthcare access and adoption of affordable biosimilars.

- Middle East & Africa are gradually expanding, driven by investments in healthcare modernization and biologics distribution.

Competitive Landscape

Key players in the global biopharmaceuticals market include Merck & Co., Inc., F. Hoffmann-La Roche AG, Eli Lilly and Company, Sanofi, Amgen Inc., AbbVie Inc., Biogen Idec, Bayer AG, Johnson & Johnson Services, Pfizer Inc., and Novartis AG. These companies are focusing on innovative biologic development, biosimilar launches, and strategic alliances to strengthen their global market presence.

Global Biopharmaceuticals Market Size

The global biopharmaceuticals market is anticipated to rise from USD 250.50 billion in 2024 to USD 553.12 billion in 2033, growing at a CAGR of 9.2%.

The biopharmaceuticals are therapeutic agents derived from biological sources, including proteins, nucleic acids, and living cells, produced through advanced biotechnological processes such as recombinant DNA technology, monoclonal antibody engineering, and cell-based cultivation. Unlike traditional small-molecule drugs, biopharmaceuticals are structurally complex, highly specific, and often designed to modulate the immune system or target disease at the molecular level. As per the World Health Organization, over 800 biopharmaceuticals are currently in clinical development, with more than half targeting previously untreatable conditions. The expansion of personalized medicine has further amplified reliance on biopharmaceuticals; for instance, CAR-T cell therapies, which involve genetically modifying a patient’s own immune cells, have demonstrated durable remissions in refractory blood cancers.

MARKET DRIVERS

Rising Prevalence of Chronic and Immune-Mediated Diseases

The escalating global burden of chronic and immune-mediated diseases is driving for the growth of the biopharmaceuticals market. According to the World Health Organization, non-communicable diseases account for 74% of all deaths globally, with cancer alone responsible for nearly 10 million fatalities annually. Biopharmaceuticals such as monoclonal antibodies and immune checkpoint inhibitors have revolutionized cancer treatment. For example, pembrolizumab, an anti-PD-1 therapy, has extended survival in metastatic melanoma patients by over two years in clinical trials, as documented by the U.S. National Cancer Institute. Biologic therapies like adalimumab and infliximab have become standard-of-care due to their ability to selectively inhibit pro-inflammatory cytokines such as TNF-alpha, resulting in significant symptom reduction and disease remission.

Advancements in Genomic Research and Precision Medicine

The rapid evolution of genomic science and its integration into clinical practice has fundamentally reshaped the development and application of biopharmaceuticals, which is additionally fuelling the growth of the biopharmaceuticals market. As per the U.S. National Human Genome Research Institute, the cost of whole-genome sequencing has plummeted from $100 million in 2001 to under $500 in 2024, making genomic profiling accessible for routine diagnostics and treatment planning. This technological democratization has accelerated the discovery of disease-specific biomarkers, allowing biopharmaceutical developers to design agents that selectively target molecular pathways. For instance, trastuzumab, a monoclonal antibody used in HER2-positive breast cancer, improves survival rates by identifying patients whose tumors overexpress the HER2 protein, as confirmed in trials by the European Society for Medical Oncology. The emergence of gene therapies further exemplifies this shift; Zolgensma, a gene-replacement therapy for spinal muscular atrophy, delivers a functional copy of the SMN1 gene via an adeno-associated virus vector, resulting in motor function improvement in 92% of treated infants within one year, according to a longitudinal study by the Children’s Hospital of Philadelphia. Additionally, pharmacogenomic screening is now standard in several countries; in the Netherlands, over 70% of hospitals use genetic testing to guide biologic selection in autoimmune diseases, as reported by the Dutch Pharmacogenetics Working Group.

MARKET RESTRAINTS

High Development Costs and Lengthy Regulatory Pathways

The expansion of the biopharmaceutical market is the exorbitant cost and extended timeline associated with research, clinical validation, and regulatory approval, which is amplifying the growth of the biopharmaceuticals market. The development cycle for biologics typically spans 10 to 15 years, with Phase III trials alone lasting up to five years, as noted by the U.S. Food and Drug Administration. Regulatory scrutiny is particularly rigorous due to the inherent variability of biological systems; for example, biosimilarity assessments require extensive analytical, preclinical, and clinical data to demonstrate equivalence to originator products, delaying market entry for biosimilars. In the European Union, the European Medicines Agency mandates a minimum of two clinical studies to confirm biosimilar efficacy and safety, increasing the development burden. Emerging markets face even greater hurdles; in India, only 12 biologics have received full regulatory approval since 2010, per the Central Drugs Standard Control Organization, due to infrastructure and expertise gaps.

Cold Chain Logistics and Storage Sensitivity of Biologic Products

The structural fragility of biopharmaceuticals with highly specialized storage and distribution systems is posing a significant restraints for the growth of the biopharmaceuticals market. Most biologics, including monoclonal antibodies, vaccines, and cell therapies, are susceptible to denaturation when exposed to temperature fluctuations, requiring uninterrupted cold chain maintenance between 2°C and 8°C, or even -70°C for mRNA-based products, as specified by the World Health Organization. Cell and gene therapies present even greater challenges; autologous CAR-T treatments must be shipped globally while maintaining viability, often relying on cryopreserved transport via specialized couriers. The International Air Transport Association estimates that temperature excursions affect 20% of all biopharmaceutical shipments, increasing waste and costs.

MARKET OPPORTUNITIES

Expansion of Biosimilars in Emerging and Regulated Markets

The growing acceptance and regulatory endorsement of biosimilars present a transformative opportunity to broaden access to high-cost biopharmaceuticals while reducing systemic healthcare expenditures. As per the World Health Organization, biosimilars are rigorously evaluated versions of originator biologics that demonstrate comparable quality, safety, and efficacy, offering cost savings of 20% to 35%, according to the RAND Corporation. In the European Union, where biosimilars have been integrated into clinical practice since 2006, they now account for over 80% of infliximab prescriptions in countries like Germany and Norway, as reported by the European Medicines Agency. This shift has enabled healthcare systems to treat more patients without increasing budgets. In Japan, the government’s Biosimilar Action Plan has driven biosimilar penetration to 45% for filgrastim and 38% for etanercept, significantly lowering public spending on rheumatology and oncology, according to the Pharmaceuticals and Medical Devices Agency. Emerging markets are also embracing biosimilars; India’s National Biopharma Mission supports domestic production, with companies like Biocon launching affordable trastuzumab biosimilars that have expanded breast cancer treatment access to over 100,000 women in rural clinics, as documented by the Indian Council of Medical Research. Regulatory harmonization through initiatives like the ASEAN Common Technical Dossier is accelerating approvals across Southeast Asia.

Integration of Artificial Intelligence in Biopharmaceutical Discovery and Development

The integration of artificial intelligence (AI) into biopharmaceutical R&D is unlocking unprecedented efficiencies in drug discovery, target identification, and clinical trial design, which is significantly hindering the growth of the biopharmaceuticals market. As per the Nature Biotechnology journal, AI-driven platforms can analyze petabytes of genomic, proteomic, and clinical data to predict protein structures and disease pathways with remarkable accuracy; DeepMind’s AlphaFold has successfully predicted over 200 million protein structures, including many previously unknown, revolutionizing target validation. Companies like Insilico Medicine have leveraged generative AI to design novel biologic candidates, reducing preclinical discovery from years to months. In 2023, the company advanced an AI-generated fibrosis drug into Phase II trials—the first of its kind—demonstrating the viability of machine-driven innovation. AI also enhances clinical development; according to the U.S. Food and Drug Administration, machine learning models are now used to identify optimal patient cohorts, improving trial enrollment efficiency by 30% in oncology studies. In China, the National Medical Products Administration has approved AI-assisted platforms for biomarker discovery, accelerating biologic development for rare diseases. Furthermore, AI optimizes manufacturing processes by predicting yield variability and detecting contamination risks in bioreactors, as implemented by Novartis in its continuous bioprocessing units.

MARKET CHALLENGES

Immunogenicity and Unintended Immune Responses to Biologic Therapies

The biopharmaceutical domain is the risk of immunogenicity where the patient’s immune system recognizes a therapeutic protein as foreign, triggering neutralizing antibodies that diminish efficacy or induce adverse reactions. As per the U.S. Food and Drug Administration, up to 80% of patients treated with certain recombinant enzymes develop anti-drug antibodies, which compromise treatment outcomes in conditions like hemophilia and lysosomal storage disorders. For instance, approximately 30% of hemophilia A patients treated with recombinant factor VIII develop inhibitors, rendering the therapy ineffective and increasing bleeding risks, according to the World Federation of Hemophilia. Immunogenicity is influenced by multiple factors, including protein aggregation, post-translational modifications such as glycosylation, and route of administration.

Ethical and Regulatory Ambiguity in Gene and Cell Therapies

The rapid advancement of gene and cell-based biopharmaceuticals has outpaced the development of cohesive ethical and regulatory frameworks, creating uncertainty in clinical deployment and patient access. As per the Nuffield Council on Bioethics, therapies involving germline editing or heritable genetic modifications raise profound ethical questions about consent, equity, and long-term societal impact, which is prompting calls for international governance. While somatic cell therapies like CAR-T are approved in multiple jurisdictions, regulatory divergence persists; in the United States, the FDA requires long-term follow-up for up to 15 years to monitor delayed adverse events, whereas regulatory oversight in some Asian countries remains less stringent, as noted by the International Council for Harmonisation. Additionally, the autologous nature of many cell therapies introduces logistical and ethical complexities; patient-derived cells are manipulated ex vivo, raising issues around ownership, data privacy, and informed consent.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| Segments Covered | By Product Type, Therapeutic Type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Merck & Co., Inc., F. Hoffmann- La Roche AG, Eli Lilly and Company, Inc., Sanofi, Amgen Inc., AbbVie Inc., Biogen Idec, Bayer AG, Johnson & Johnson Services, Pfizer, Inc. and Novartis AG. |

SEGMENTAL ANALYSIS

By Product Type Insights

The monoclonal antibodies (mAbs) segment was the largest and held 43.2% of the biopharmaceuticals market share in 2024. The therapeutic success of mAbs stems from their ability to precisely target disease-associated antigens without broadly suppressing physiological functions. According to the American Society of Clinical Oncology, eight of the top ten best-selling oncology drugs in 2023 were monoclonal antibodies, including trastuzumab for HER2-positive breast cancer and rituximab for non-Hodgkin’s lymphoma, both of which have significantly improved survival rates in their respective indications. The U.S. Food and Drug Administration approved 22 new mAbs in 2023 alone, reflecting sustained innovation and regulatory confidence in this class. Furthermore, the development of bispecific antibodies and antibody-drug conjugates (ADCs) has enhanced potency and reduced off-target effects. A 2023 clinical trial by Memorial Sloan Kettering demonstrated that the ADC trastuzumab deruxtecan reduced tumor size by 73% in metastatic breast cancer patients with low HER2 expression, a previously untreatable subgroup.

The biotech vaccines segment is expected to register a CAGR of 16.8% from 2025 to 2033, with the global pivot toward preventive medicine and the proven success of mRNA and recombinant vector platforms during the pandemic. As per the World Health Organization, over 13 billion doses of biotech-based COVID-19 vaccines were administered globally by the end of 2023, establishing a robust infrastructure for future vaccine deployment. BioNTech has since advanced 15 mRNA candidates into clinical trials, including vaccines for tuberculosis, malaria, and personalized cancer immunotherapies, as documented in its 2023 pipeline report. Additionally, recombinant protein vaccines are gaining traction; Novavax’s protein-based COVID-19 vaccine received approval in 45 countries by 2024, according to the European Medicines Agency, offering an alternative for individuals averse to nucleic acid platforms. Investment in pandemic preparedness is further accelerating growth; the Coalition for Epidemic Preparedness Innovations has committed $3.5 billion through 2029 to develop vaccines for Disease X and other priority pathogens.

By Therapeutic Type Insights

The oncology segment was the largest and held 48.2% of the biopharmaceuticals market share in 2024 with the escalating global cancer burden and the central role of biologics in modern cancer treatment. According to the International Agency for Research on Cancer, 20 million new cancer cases were diagnosed worldwide in 2023, with projections indicating a rise to 30 million by 2040 due to aging populations and lifestyle changes. Biopharmaceuticals have become indispensable in oncology, particularly monoclonal antibodies, immune checkpoint inhibitors, and CAR-T cell therapies, which offer targeted mechanisms with fewer systemic side effects than chemotherapy. The U.S. National Cancer Institute reports that immune checkpoint inhibitors have improved five-year survival rates in metastatic melanoma from 10% to over 50%, transforming once-fatal diagnoses into manageable conditions.

The neurology segment is swiftly emerging with a CAGR of 15.2% from 2025 to 2033, with the breakthroughs in targeting neurodegenerative and neuroinflammatory diseases—conditions long considered untreatable. According to the World Health Organization, over 55 million people globally live with dementia, a number expected to reach 139 million by 2050 by creating urgent demand for disease-modifying therapies. Gene therapy is also advancing; Roche’s hemophilia A gene therapy, valoctocogene roxaparvovec, achieved sustained factor VIII expression in 80% of patients, reducing bleeding episodes by 98%, as per the U.S. Food and Drug Administration’s 2023 review. Regulatory incentives, such as the U.S. FDA’s Fast Track and Breakthrough Therapy designations, are expediting development, with over 300 biologics in clinical trials for neurological disorders as of 2024, according to the Michael J. Fox Foundation.

REGIONAL ANALYSIS

North America was the top performer of the global biopharmaceuticals market by capturing a 41.2% of share in 2024. The U.S. Food and Drug Administration’s Center for Biologics Evaluation and Research (CBER) approved 56 novel biologics in 2023, the highest globally, including groundbreaking gene therapies and bispecific antibodies. Companies like Amgen, Regeneron, and Genentech continue to lead in monoclonal antibody development, with Humira alone generating $20 billion in annual sales before biosimilar competition. The presence of integrated payer systems enables rapid reimbursement; Medicare and private insurers cover over 90% of FDA-approved biologics, ensuring patient access. Additionally, the U.S. hosts the largest concentration of biotech startups, with over 2,500 firms in the San Francisco Bay Area and Boston-Cambridge corridor, per the Biotechnology Innovation Organization.

Europe was positioned second by capturing 28.1% of the biopharmaceuticals market share in 2024. The European Medicines Agency (EMA) maintains a rigorous yet predictable approval pathway, authorizing 34 new biologics in 2023, including advanced therapies like allogeneic CAR-T and recombinant enzymes for rare diseases. Countries like Germany, Switzerland, and the UK are home to leading biopharmaceutical firms such as Roche, Novartis, and AstraZeneca, which collectively invest over €25 billion annually in R&D, according to the European Federation of Pharmaceutical Industries and Associations. The EU’s Innovative Health Initiative supports cross-border collaboration, accelerating clinical development. Biosimilar adoption is particularly advanced; in Norway, biosimilars account for over 90% of infliximab prescriptions, reducing treatment costs and expanding access. The EU Orphan Medicines Regulation has incentivized development for rare diseases, resulting in over 200 authorized orphan biologics as of 2024, per the EMA.

Asia-Pacific biopharmaceuticals market is expected to experience substantial growth opportunities during the forecast period. China stands as the regional leader, propelled by aggressive government investment in life sciences under its “Made in China 2025” and “Healthy China 2030” initiatives. The National Medical Products Administration approved 28 novel biologics in 2023, including domestic monoclonal antibodies and CAR-T therapies, as reported by the China Pharmaceutical Enterprise Development Association. India is emerging as a biosimilar powerhouse, where Biocon and Dr. Reddy’s have launched affordable versions of trastuzumab and insulin glargine by improving access for millions.

Latin America biopharmaceuticals market is likely to have a prominent growth opportunity during the forecast period. Brazil leads the region by leveraging its large population and established pharmaceutical infrastructure to expand biologic access. Public programs like “Farmácia Popular” subsidize biologic treatments for diabetes and rheumatoid arthritis, reaching over 10 million patients. Mexico has strengthened its regulatory framework, aligning with ICH guidelines to attract foreign investment. Argentina has developed domestic biologic production through companies like mAbxience, reducing import dependence.

Middle East and Africa biopharmaceuticals market is having steady opportunities throughout the forecast period. The UAE has established Dubai Science Park to attract biotech firms, hosting over 120 life sciences companies by 2024, according to the Dubai Health Authority. In South Africa, the Council for Scientific and Industrial Research is developing biosimilars for HIV and cancer, addressing high disease burdens; the country has the largest HIV-positive population globally, with 8.5 million people affected, as reported by UNAIDS. Egypt has launched a national biotechnology strategy, focusing on insulin and vaccine production.

KEY PLAYERS AND COMPETITIVE LANDSCAPE

A list of crucial competitors dominating the global Biopharmaceuticals market profiled in this report is Merck & Co., Inc., F. Hoffmann- La Roche AG, Eli Lilly and Company, Inc., Sanofi, Amgen Inc., AbbVie Inc., Biogen Idec, Bayer AG, Johnson & Johnson Services, Pfizer, Inc. and Novartis AG.

The competitive dynamics of the biopharmaceuticals market are defined by a convergence of scientific ambition, regulatory complexity, and global health imperatives. Established multinational corporations leverage decades of R&D expertise, robust pipelines, and global distribution networks to maintain leadership, while nimble biotech firms disrupt the landscape with novel modalities and platform technologies. The race to develop first-in-class therapies, particularly in oncology, neurology, and rare diseases fuels intense rivalry, with differentiation increasingly dependent on molecular specificity, clinical outcomes, and speed of innovation. Intellectual property remains a battleground, as patent cliffs for blockbuster biologics open doors for biosimilar competition, prompting originators to extend lifecycle through next-generation formulations and combination therapies. Geopolitical factors, including trade policies and local manufacturing mandates, further shape competitive positioning. Companies are no longer competing solely on efficacy but on accessibility, sustainability, and integration into healthcare systems. The rise of personalized medicine demands adaptive clinical development and companion diagnostics, raising the bar for technological sophistication. Trust, regulatory compliance, and ethical stewardship have become strategic assets, especially in gene and cell therapies.

Top Players in the Biopharmaceuticals Market

Roche stands as a pioneering force in the biopharmaceutical sector, renowned for its groundbreaking innovations in oncology and immunology. The company has redefined cancer treatment through monoclonal antibodies such as rituximab, trastuzumab, and atezolizumab, which target specific molecular pathways with high precision. Roche’s commitment to personalized medicine is evident in its integrated diagnostics-therapeutics model, where companion diagnostics guide treatment selection, enhancing clinical efficacy. Its investment in neuroscience and rare diseases has led to the development of transformative therapies, including those for spinal muscular atrophy and Alzheimer’s disease.

Amgen has been instrumental in advancing the science of protein-based therapeutics, establishing itself as a leader in cardiovascular and oncology biologics. The company pioneered the development of erythropoiesis-stimulating agents and granulocyte colony-stimulating factors, addressing unmet needs in anemia and chemotherapy-induced neutropenia. Amgen’s expertise in large-molecule engineering has enabled the creation of targeted therapies, including PCSK9 inhibitors that significantly lower LDL cholesterol in high-risk patients. The company emphasizes sustainable innovation through robust pipeline development and strategic collaborations with academic and clinical institutions.

Johnson & Johnson (Janssen Biotech) plays a transformative role in the biopharmaceutical landscape through its diversified portfolio in immunology, oncology, and infectious diseases. Janssen has developed highly effective monoclonal antibodies for psoriasis, Crohn’s disease, and multiple myeloma, significantly improving quality of life for patients with chronic inflammatory and hematologic disorders. The company demonstrated global leadership during the pandemic by deploying a recombinant vector-based vaccine at unprecedented speed.

Top Strategies Used by Key Market Participants

A primary strategy among leading biopharmaceutical companies is vertical integration of research, manufacturing, and commercialization to ensure control over product quality, supply chain resilience, and time-to-market efficiency. Firms can rapidly scale production, respond to regulatory demands, and protect intellectual property by maintaining in-house capabilities across the development lifecycle. This integrated model also supports innovation continuity, enabling seamless transition from preclinical discovery to clinical deployment.

Another pivotal approach is the pursuit of strategic alliances with academic institutions, biotech startups, and contract development and manufacturing organizations (CDMOs). These collaborations allow large players to access novel platforms, such as gene editing and AI-driven drug design, while mitigating R&D risks. Partnerships also facilitate entry into emerging therapeutic areas and accelerate clinical validation through shared expertise and infrastructure.

A third key strategy is geographic diversification and localization of production to meet regional regulatory requirements and improve market access. Companies are establishing regional manufacturing hubs and tailoring clinical trials to local patient populations, enhancing relevance and acceptance of therapies. This localization strengthens relationships with health authorities and supports equitable distribution, particularly in high-growth emerging markets.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Roche announced the expansion of its biologics manufacturing facility in Singapore by enhancing capacity for monoclonal antibody production to meet growing demand in the Asia-Pacific region and reinforcing its regional supply chain resilience.

- In May 2024, Amgen entered into a strategic collaboration with a leading gene-editing biotech firm to co-develop next-generation CAR-T therapies for solid tumors, which is aiming to overcome current limitations in tumor infiltration and persistence.

- In January 2024, Johnson & Johnson initiated a global Phase III trial for its investigational bispecific antibody in early Alzheimer’s disease by marking a significant advancement in its neuroscience pipeline and positioning the therapy for potential first-mover advantage.

- In March 2024, Novartis launched a digital therapeutics platform integrated with its cell therapy delivery system, which is enabling real-time patient monitoring and remote clinical support for CAR-T recipients, thereby improving post-treatment care standards.

- In June 2024, AstraZeneca inaugurated a new biologics research center in Cambridge, UK, focused on AI-driven target discovery and antibody engineering, strengthening its innovation pipeline in oncology and respiratory diseases.

MAEKET SEGMENTATION

This research report on the global biopharmaceuticals market is segmented and sub-segmented into the following categories and analyzed market size and forecast for each segment are analyzed.

By Product Type

- Monoclonal Antibodies (mAb)

- Erythropoietin

- Biotech Vaccines

- Recombinant Human (RH) Insulin

- Granulocyte colony-stimulating factor (G-CSF)

- Interferon

- Human Growth Hormones (HGH)

By Therapeutic Type

- Neurology

- Infectious diseases

- Diabetes

- Oncology

- Cardiovascular

- Other Therapeutic Areas

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is driving the growth of the biopharmaceuticals market?

The market is driven by rising prevalence of chronic diseases, advancements in biotechnology, increasing demand for personalized medicine, and growing investments in R&D by pharmaceutical companies.

Which segment by product led the biopharmaceuticals market in 2024?

The monoclonal antibodies segment led the global biopharmaceuticals market in 2024.

Which region dominated the market for biopharmaceuticals worldwide in 2024?

Geographically, the North American region dominated the biopharmaceuticals market worldwide in 2024.

What challenges does the biopharmaceutical industry face?

Challenges include high development and production costs, complex regulatory approval processes, patent expiration, and supply chain issues.

What is the expected future outlook for the biopharmaceuticals market?

The market is expected to witness robust growth due to increasing adoption of biologics, innovations in gene and cell therapy, and expansion into emerging markets.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com