Antibodies Market Report: Global Industry Size, Therapeutic Applications, Growth Trends, and Forecast by Product Type, Technology, End-Use, and Region – 2025 to 2033

Global Antibodies Market Size

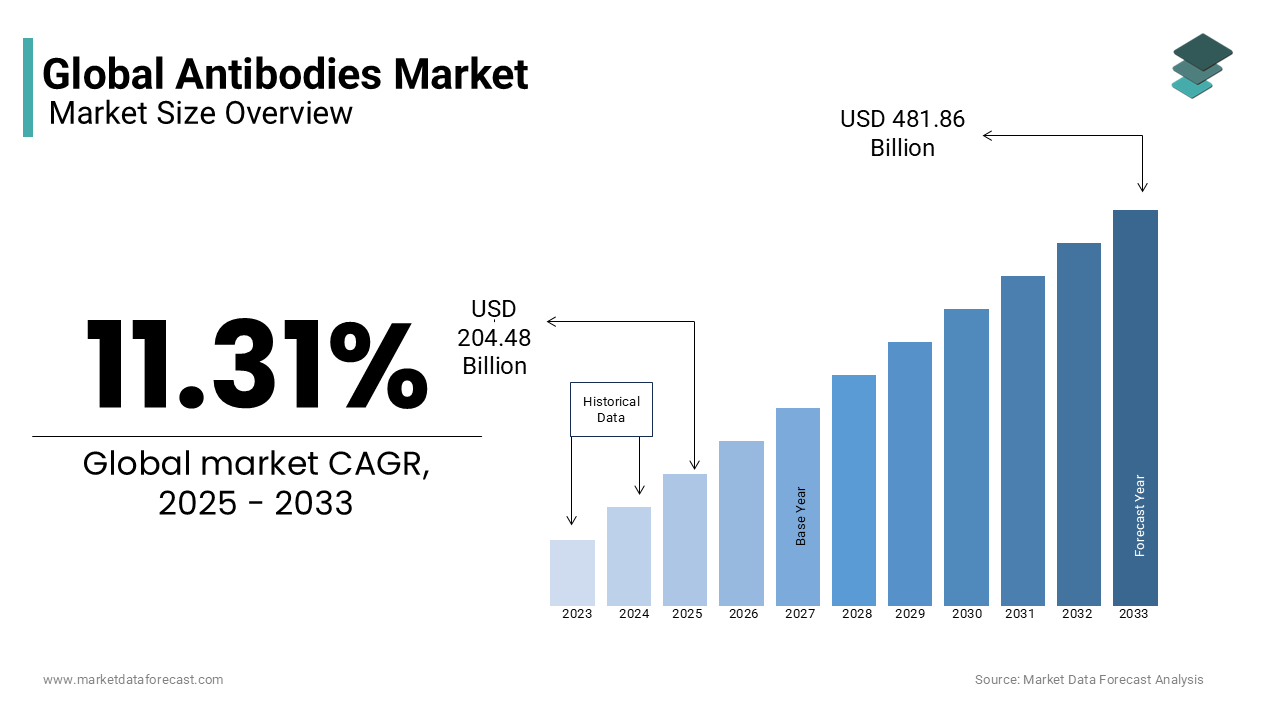

The global antibodies market size was valued at USD 183.7 billion in 2024 and is expected to reach USD 432.90 billion by 2033 from USD 204.48 billion in 2025, growing at a CAGR of 11.31 % during the forecast period.

Antibodies are involved the production and application of monoclonal, polyclonal, and recombinant antibodies used in diagnostics, therapeutics, and research. These highly specific proteins, engineered to bind to target antigens with precision, are foundational in detecting disease biomarkers, modulating immune responses, and enabling targeted drug delivery. Antibodies are integral to the development of immunotherapies, particularly in oncology, autoimmune disorders, and infectious diseases.

The National Institutes of Health emphasizes that antibodies play a pivotal role in vaccine development, as demonstrated during the rapid deployment of SARS-CoV-2 neutralizing antibody therapies and diagnostic assays. Regulatory bodies such as the U.S. Food and Drug Administration and the European Medicines Agency have established robust frameworks for antibody characterization and biosimilar approval, ensuring safety and efficacy. With rising investments in personalized medicine and immuno-oncology, antibodies have evolved from research tools to indispensable agents in modern medicine, driving innovation across clinical and industrial applications.

MARKET DRIVERS

Rising Prevalence of Chronic and Immune-Mediated Diseases

The escalating global burden of chronic illnesses, particularly cancer, autoimmune disorders, and neurodegenerative conditions, has significantly amplified the demand for antibody-based therapeutics. As per the World Health Organization, cancer accounted for nearly 10 million deaths in 2022, with immunotherapies, including checkpoint inhibitors like anti-PD-1 and anti-CTLA-4 antibodies, becoming standard-of-care in melanoma, lung, and renal cancers. Similarly, autoimmune diseases such as rheumatoid arthritis, multiple sclerosis, and inflammatory bowel disease affect a portion of the global population. Monoclonal antibodies like adalimumab and rituximab have revolutionized management by selectively neutralizing inflammatory cytokines or depleting aberrant immune cells. The shift from symptomatic treatment to disease modification is increasingly reliant on antibody specificity, driving pharmaceutical investment and clinical adoption.

Expansion of Diagnostic Applications in Precision Medicine

Antibodies are increasingly central to diagnostic platforms that enable early disease detection, patient stratification, and treatment monitoring in precision medicine. A notable share of clinical decisions are informed by laboratory diagnostics, many of which rely on immunoassays using monoclonal antibodies. Enzyme-linked immunosorbent assays (ELISA), immunohistochemistry (IHC), and flow cytometry depend on high-affinity antibodies to detect biomarkers such as HER2 in breast cancer, PSA in prostate disease, and tau proteins in neurodegeneration. The Centers for Disease Control and Prevention highlights that rapid antigen tests for infectious diseases—including HIV, hepatitis, and SARS-CoV-2—utilize monoclonal antibodies to achieve high specificity and point-of-care usability. In 2022, the FDA authorized several antibody-based diagnostic kits for home and clinical use, reflecting their critical role in public health surveillance. Additionally, liquid biopsy technologies, which analyze circulating tumor cells and cell-free DNA, employ antibody-coated capture systems to isolate rare biomarkers with high sensitivity. Such methods can detect cancer recurrence up to several months earlier than imaging in some cases. With healthcare systems prioritizing early intervention and personalized treatment plans, the integration of antibody-driven diagnostics into routine care is accelerating, creating sustained demand across clinical and research laboratories

MARKET RESTRAINTS

High Development and Manufacturing Costs of Therapeutic Antibodies

The production of monoclonal antibodies remains one of the most expensive processes in biopharmaceutical manufacturing, limiting accessibility and scalability. A major contributor is the complexity of cell-line development, where Chinese hamster ovary (CHO) cells must be genetically engineered and optimized for high-yield, consistent expression. Downstream purification, involving protein A affinity chromatography, accounts for a notable share of total manufacturing costs. Additionally, cold-chain logistics and specialized storage further increase distribution expenses. These financial barriers restrict the entry of smaller biotechs and limit patient access in low- and middle-income countries. Biosimilar development offers some relief, but regulatory hurdles and immunogenicity concerns slow adoption, maintaining high price points across much of the therapeutic antibody landscape.

Risk of Immunogenicity and Adverse Immune Reactions

Despite advances in humanization and engineering, therapeutic antibodies can provoke unwanted immune responses, reducing efficacy and posing safety risks. Fully murine antibodies carry the highest risk, but even chimeric and humanized variants can elicit immune recognition due to glycosylation differences or aggregate formation during storage. Additionally, cytokine release syndrome (CRS), a systemic inflammatory response, has been observed with T-cell-engaging antibodies like blinatumomab, necessitating hospital-based administration and intensive monitoring. These safety concerns increase clinical oversight requirements, limit outpatient use, and deter prescriber confidence, especially in chronic indications requiring long-term therapy.

MARKET OPPORTUNITIES

Advancements in Recombinant and Bispecific Antibody Engineering

Innovations in antibody engineering are unlocking new therapeutic possibilities, particularly through recombinant DNA technology and bispecific antibody platforms. Many bispecific antibodies are in clinical development, targeting solid and hematologic tumors with enhanced specificity and reduced off-target effects. Recombinant techniques, including phage and yeast display, allow for rapid screening of billions of antibody variants, accelerating discovery timelines from years to months. Additionally, fragment-based antibodies (e.g., scFv, Fab, nanobodies) offer improved tissue penetration and faster clearance, beneficial for imaging and targeted delivery. In diagnostics, engineered antibodies with enhanced stability and labeling efficiency are improving the sensitivity of rapid tests and point-of-care devices. With pharmaceutical companies increasingly partnering with biotech startups specializing in antibody design, this technological frontier is poised to redefine treatment paradigms across oncology, neurology, and infectious diseases.

Growth of Biosimilars and Market Expansion in Emerging Economies

The expiration of patents for major monoclonal antibodies has catalyzed the development of biosimilars, offering cost-effective alternatives and expanding access in underserved regions. As per the World Health Organization, biosimilars can reduce treatment costs compared to originator biologics, making therapies more viable for public health systems. In India, the National Biopharma Mission has supported the development of many biosimilar candidates, including trastuzumab and rituximab, to address unmet oncology needs. Also, biosimilar uptake in Latin America and Southeast Asia is growing annually, driven by government procurement and physician education programs. Additionally, local manufacturing initiatives in countries like South Korea and China are reducing import dependency and improving supply resilience. With regulatory harmonization efforts led by the International Council for Harmonisation (ICH), biosimilars are gaining global acceptance, creating a sustainable pathway to democratize access to life-saving antibody therapies.

MARKET CHALLENGES

Complex Regulatory Pathways for Antibody-Based Therapeutics

The approval process for monoclonal antibodies is exceptionally rigorous, requiring extensive preclinical and clinical validation to ensure safety, efficacy, and consistency. As per the U.S. Food and Drug Administration, developers must submit comprehensive data on antibody structure, post-translational modifications, immunogenicity, and batch-to-batch comparability—requirements that are more stringent than for small-molecule drugs. Biosimilars face additional hurdles, requiring head-to-head clinical trials to demonstrate equivalence, despite structural similarity. In emerging markets, inconsistent regulatory frameworks create delays; the World Bank reports that approval timelines for biologics in some African nations exceed seven years due to limited technical capacity. These complexities increase development costs, deter innovation, and delay patient access. Harmonizing global standards and streamlining review processes remain critical challenges for accelerating antibody therapeutics to market.

Cold-Chain and Storage Limitations in Global Distribution

Monoclonal antibodies are highly sensitive to temperature fluctuations, requiring uninterrupted cold-chain logistics from manufacturing to administration. Most therapeutic antibodies must be stored between 2°C and 8°C, with exposure to higher temperatures causing protein denaturation, aggregation, and loss of potency. Even in developed countries, last-mile delivery challenges during power outages or extreme weather can compromise product integrity. Lyophilization (freeze-drying) offers some stability, but reconstitution adds complexity in clinical settings. Innovations in thermostable formulations and alternative delivery methods (e.g., subcutaneous, oral antibodies) are underway, but remain in early stages. Until robust, low-cost cold-chain solutions are widely available, the global scalability of antibody therapies will remain constrained, particularly in areas with the greatest disease burden.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Analysed | By Product Type, Indication, End User, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Analysed | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Abbott Diagnostics, Novartis AG, Pfizer Inc., Thermo Fisher Scientific Inc., Eli Lilly and Company, A.G. Scientific, Inc., Bristol-Myers Squibb, AbbVie Inc., and F. Hoffmann-La Roche Ltd. |

SEGMENTAL ANALYSIS

By Product Type Insights

The monoclonal antibodies segment dominated the antibodies market by accounting for a 66,8% of the total share in 2024. A key driver is the expansion of mAbs in oncology and autoimmune disorders. Additionally, the global cancer burden is rising, with the World Health Organization estimating 19.3 million new cancer cases in 2020, increasing demand for targeted therapies like trastuzumab, rituximab, and pembrolizumab. These drugs offer improved patient outcomes with fewer off-target effects compared to conventional chemotherapy. A further major factor is biopharmaceutical investment and regulatory support. Governments and private investors are heavily funding biologics manufacturing, especially in China and India, where biosimilar production is expanding rapidly.

The antibody-drug conjugates segment is the fastest-growing in the antibodies market by registering a CAGR of 18.7% from 2025 to 2033. This explosive growth stems from their unique mechanism of action, delivering cytotoxic agents directly to diseased cells while sparing healthy tissue. One major growth driver is the rising clinical success and regulatory approvals of ADCs. A further critical factor is the robust pipeline of ADC candidates. Companies like Daiichi Sankyo, AstraZeneca, and Pfizer are leading the development. Additionally, technological advancements in linker and payload systems have improved ADC stability and efficacy. These innovations are broadening ADC applicability beyond oncology into autoimmune and infectious diseases, further fueling market expansion.

By Indication Insights

The cancer segment is the largest indication segment in the antibodies market by capturing a 45.3% of total revenue in 2024. This lead position is due to the growing global cancer burden and the central role of monoclonal antibodies and ADCs in precision oncology. The rising incidence of cancer worldwide is a primary driver. The World Health Organization projects 28.4 million new cancer cases annually by 2040, up from 19.3 million in 2020, with lung, breast, and colorectal cancers leading the surge. In response, antibody-based therapies such as pembrolizumab (Keytruda) and trastuzumab (Herceptin) have become standard-of-care treatments. An additional key factor is the integration of immunotherapy into first-line treatment regimens. Moreover, government and institutional funding for cancer research is accelerating innovation.

The autoimmune diseases segment is the fastest-growing indication in the antibodies market and is projected to grow at a CAGR of 16.3% from 2025 to 2033. This rapid expansion is fueled by increasing prevalence of autoimmune conditions and the success of biologic therapies in managing chronic inflammation. The main driver is the rising global burden of autoimmune disorders.

The clinical effectiveness of monoclonal antibodies like adalimumab (Humira), infliximab (Remicade), and ustekinumab (Stelara) has revolutionized treatment. Additionally, biosimilar entry is expanding access. Since 2023, multiple adalimumab biosimilars have been approved in Europe and Asia, reducing treatment costs. This affordability is increasing patient access in emerging markets like India and Indonesia. Furthermore, pipeline innovation is robust.

By End User Insights

The research institutes segment represented the prominent end-user in the antibodies market by commanding an estimated 42.6% share in 2024. This dominance is driven by the foundational role of antibodies in basic and translational research across academia and biotech. The massive investment in life sciences research is primary factor. The U.S. National Institutes of Health allocated substantial funds in 2023 for biomedical research, much of which involves antibody-based assays for target validation, protein detection, and cellular imaging. Similarly, the European Union’s Horizon Europe program committed significant amount from 2021 to 2027 for health and biotechnology innovation, as stated by the European Commission. An additional critical driver is the expansion of genomics and proteomics initiatives. Additionally, increasing university-industry collaborations are boosting demand. These alliances accelerate antibody validation and commercialization, reinforcing research institutes as the primary consumers of research-grade antibodies.

The diagnostic laboratories segment is the fastest-growing end-user and is expected to grow at a CAGR of 15.8% from 2025 to 2033. This surge is driven by the integration of antibody-based assays into routine clinical diagnostics and the expansion of precision medicine. The rising demand for early and accurate disease detection is a key factor. Early diagnosis improves survival rates in cancers like cervical and colorectal, leading to widespread adoption of immunohistochemistry (IHC) and ELISA tests in labs. A further driver is the growth of centralized and reference labs. In India, Dr. Lal PathLabs and Metropolis Healthcare processed large number of tests, many involving antibody-based diagnostics for cancer biomarkers and infectious diseases, according to the companies’ annual reports. Furthermore, regulatory approvals for companion diagnostics are accelerating adoption. The FDA has approved several antibody-based companion diagnostics, including PD-L1 IHC tests for immunotherapy eligibility. These tools are now standard in oncology workflows, increasing lab dependency on high-quality antibodies.

By Application Insights

The medical application segment led the antibodies market by holding a 50.7% of the share in 2024. This dominance reflects the direct use of therapeutic antibodies in patient care across hospitals and clinics. The widespread clinical use of monoclonal antibodies in chronic disease management is a major driver. As of 2023, over 100 monoclonal antibodies are approved for medical use, treating conditions ranging from cancer to asthma, as listed by the U.S. FDA. Drugs like dupilumab (Dupixent) for atopic dermatitis and evolocumab (Repatha) for hypercholesterolemia are increasingly prescribed, with Dupixent generating substantial in sales. An additional factor is the shift from small molecules to biologics in treatment guidelines. Additionally, payer coverage and reimbursement policies are supporting adoption.

The experimental application segment is growing at the fastest rate, with a CAGR of 17.2% from 2025 to 2033. This growth is driven by the expanding use of antibodies in preclinical research, drug discovery, and novel therapeutic development. The rise in R&D spending by biotech and pharmaceutical firms is a key factor. Companies like Regeneron and Genentech use experimental antibodies in high-throughput screening to identify new drug candidates. A further driver is the adoption of advanced technologies like CRISPR and single-cell sequencing, which rely on antibodies for cell sorting and protein detection. Furthermore, academic and government grants are funding exploratory research. These efforts are generating demand for custom and novel antibodies, fueling market growth.

REGIONAL ANALYSIS

North America Antibodies Market Insights

North America led the global antibodies market with a 40.4% share in 2024. The region’s dominance is anchored in its advanced healthcare infrastructure, high R&D expenditure, and strong regulatory framework. The U.S. is the primary contributor, hosting a significant share of global biotech companies, including leaders like Amgen, Regeneron, and AbbVie. In 2023, the U.S. biopharmaceutical sector invested notably in R&D, the highest globally. This innovation ecosystem has led to the approval of over 70 monoclonal antibodies, many developed domestically. A further key factor is Medicare and private insurance coverage for biologics. Additionally, academic excellence and public funding drive discovery.

Europe Antibodies Market Insights

Europe holds a significant share. The region’s strength lies in its integrated healthcare systems, robust biosimilar adoption, and pan-European research networks. Countries like Germany, the UK, and Switzerland are hubs for antibody innovation. Roche (Switzerland) and AstraZeneca (UK) are among the top mAb developers. The European Medicines Agency has approved several monoclonal antibodies, and biosimilars now account for a significant share of mAb prescriptions in Germany and Norway, reducing costs and increasing access. Moreover, Horizon Europe funds cross-border antibody research.

Asia-Pacific Antibodies Market Insights

Asia-Pacific is the fastest-growing region. This growth is fueled by rising healthcare spending, expanding biomanufacturing, and government support.

China is the regional leader, investing in billions in biopharma, aiming to produce many innovative biologics. India is emerging as a biosimilar powerhouse. Japan maintains high adoption of advanced therapies, with a large number of patients receiving mAbs annually, supported by universal health coverage.

Latin America Antibodies Market Insights

Latin America accounts for notable share of the global antibodies market. The region is seeing increased access to biologics through public health programs. Brazil’s Unified Health System (SUS) provides free access to rituximab and trastuzumab, treating a significant number of cancer patients annually. In 2023, the country approved biosimilars, improving affordability. Mexico’s IMSS and ISSSTE programs have expanded coverage for adalimumab and infliximab, with usage increasing year-on-year.However, high costs and regulatory delays remain barriers.

Middle East and Africa Antibodies Market Insights

The Middle East and Africa is at nascent but growing stage, with growth concentrated in the Gulf states. Saudi Arabia and the UAE are investing heavily in biopharma infrastructure under Vision 2030 and UAE Centennial 2071. Saudi Arabia launched the National Center for Biotechnology, allocating funds for biologic development, including monoclonal antibodies for cancer and diabetes. However, limited manufacturing and cold-chain logistics constrain access.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Notable companies profiled in the report leading the global antibodies market are Abbott Diagnostics, Novartis AG, Pfizer Inc., Thermo Fisher Scientific Inc., Eli Lilly and Company, A.G. Scientific, Inc., Bristol-Myers Squibb, AbbVie Inc., and F. Hoffmann-La Roche Ltd.

The competition in the antibodies market is intense and multifaceted, driven by a convergence of pharmaceutical giants, specialized biotech firms, and emerging biosimilar developers. Innovation is the primary battleground, with companies striving to develop next-generation antibodies that offer greater specificity, reduced immunogenicity, and enhanced delivery mechanisms. Differentiation arises not only in therapeutic efficacy but also in engineering advancements such as bispecific antibodies, antibody-drug conjugates, and humanized formats. Market leaders leverage their established pipelines and global distribution networks, while smaller players focus on niche indications and novel targets to gain footholds. Regulatory expertise, speed of clinical development, and lifecycle management of blockbuster drugs further define competitive dynamics. The entry of biosimilars has intensified price competition in mature markets, prompting originators to shift toward new indications and improved formulations. Geopolitical factors, including regional manufacturing incentives and intellectual property frameworks, also influence strategic positioning. Overall, the market is characterized by rapid technological evolution, high barriers to entry, and a constant race to translate scientific breakthroughs into clinical and commercial success.

Top Players in the Antibodies Market

Roche (Genentech)

Roche, through its subsidiary Genentech, stands as a pioneer in the development of monoclonal antibodies, having introduced some of the most impactful biologic therapies in oncology and immunology. The company’s expertise in antibody engineering and targeted therapeutics has set industry benchmarks. Roche's commitment to innovation is reflected in its robust pipeline and deep integration of research with clinical application. Its global distribution network and long-standing reputation for quality ensure widespread adoption of its antibody products across hospitals, research centers, and diagnostic labs, making it a cornerstone of the biologics landscape.

Johnson & Johnson (Janssen Biotech)

Janssen Biotech, a division of Johnson & Johnson, has been instrumental in advancing antibody-based treatments for autoimmune diseases, oncology, and infectious diseases. Known for its patient-centric approach, the company has developed highly effective monoclonal antibodies that address unmet medical needs. Janssen combines strong R&D capabilities with a vast commercial infrastructure, enabling rapid translation of scientific discoveries into accessible therapies. Its collaborations with academic institutions and biotech firms further amplify its influence, positioning it as a key architect in shaping the global antibodies ecosystem.

AbbVie

AbbVie has emerged as a dominant force in the antibodies market through its flagship product Humira and a growing portfolio of immunology-focused biologics. The company has mastered the lifecycle management of antibody therapies, maintaining leadership even amid biosimilar competition. AbbVie’s strategic focus on inflammatory diseases has led to the development of next-generation antibodies with improved efficacy and dosing convenience. Its global reach, combined with a culture of scientific excellence and strategic partnerships, allows AbbVie to continuously innovate and sustain its influence across therapeutic areas.

Top Strategies Used by Key Market Participants

One major strategy is therapeutic area specialization, where companies focus on high-impact domains such as oncology, autoimmune disorders, or rare diseases to build deep expertise and capture niche markets. This enables them to develop highly targeted antibodies with strong clinical differentiation. Another key approach is strategic partnerships and licensing agreements, allowing firms to co-develop antibody candidates, share R&D risks, and expand into new geographies through local alliances. Additionally, vertical integration and in-house manufacturing expansion is widely adopted, ensuring supply chain control, reducing production costs, and accelerating time-to-market for both research-grade and therapeutic antibodies.

RECENT MARKET DEVELOPMENTS

- In January 2023, Roche launched a new research hub in Singapore focused on antibody discovery for Asian-prevalent cancers, aiming to enhance regional innovation and accelerate clinical development.

- In June 2023, AbbVie entered a global collaboration with a biotech startup to co-develop novel bispecific antibodies for autoimmune diseases, expanding its pipeline beyond existing therapies.

- In September 2023, Johnson & Johnson expanded its manufacturing facility in Ireland to increase production capacity for monoclonal antibodies, ensuring supply stability for key markets.

- In February 2024, AstraZeneca acquired a U.S.-based antibody engineering company to strengthen its expertise in next-generation ADC platforms and solidify its oncology pipeline.

- In May 2024, Amgen partnered with a Japanese pharmaceutical firm to jointly commercialize a new immunology-focused monoclonal antibody in the Asia-Pacific region, enhancing market access and regional presence.

MARKET SEGMENTATION

This research report on the global antibodies market has been segmented based on the product type, indication, end-user, application, and region.

By Product Type

- Monoclonal Antibodies

- Murine

- Chimeric

- Humanized

- Human

- Polyclonal Antibodies

- Type I

- Type II

- Type III

- Type IV

- Type V

- Type VI

- Type VII

- Type VIII

- Antibody drug complexes

- Immunogen Technology

- Seattle Genetics Technology

- Immunomedics Technology

By Indication

- Cancer

- Autoimmune Diseases

- Infectious Diseases

- Cardiovascular Diseases

- CNS Disorders

- Others (Inflammatory, Microbial Diseases, & Others)

By End User

- Hospitals/Clinics

- Research Institute

- Diagnostics laboratories

By Application

- Medical

- Experimental

- Western blot

- ELISA

- Radioimmune Assays

- Immunofluorescence

- Others (Immunohistochemistry, Immunoprecipitation, & Immunocytochemistry)

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What is the current size of the global antibodies market?

As per our research report, the global Antibodies Market size is projected to be USD 481.86 billion by 2033.

What are the key factors driving growth in the antibodies market?

The market is fueled by the rising prevalence of chronic and rare diseases, advances in monoclonal antibody technologies, expansion of research and diagnostics, and government funding for biologic R&D.

What are the major segments in the antibodies market?

The market is segmented by By Product Type (Monoclonal Antibodies, Polyclonal Antibodies and Anti-body Drug Complexes), Indication (Cancer, Autoimmune Diseases, Infectious Diseases, Cardiovascular Diseases, CNS Disorders and Others), End User, Application and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa).

Which regions are leading the global antibodies market?

North America holds the largest market share due to strong biotech infrastructure and FDA approvals. Europe follows, with Asia-Pacific rapidly expanding due to growing pharmaceutical investments in China and India.

Who are the key players in the antibodies market?

Major players include Roche, AbbVie, Amgen, Johnson & Johnson, Merck & Co., and emerging biotech firms developing next-gen antibody formats and biosimilars.

What is the projected CAGR of the antibodies market from 2025 to 2033?

The global Antibodies Market is estimated to grow at a CAGR of 11.31% from 2025 to 2033.

How are monoclonal antibodies shaping the future of the market?

Monoclonal antibodies dominate the market, especially in oncology and autoimmune treatment. They are also being explored in antibody-drug conjugates (ADCs), bispecifics, and immunotherapies.

What are the key challenges in the antibodies market?

Major challenges include high production costs, regulatory complexities for biologics, competition from biosimilars, and limited cold chain infrastructure in emerging markets.

How is the rise of biosimilars impacting the antibodies market?

Biosimilars are increasing access to antibody therapies by offering lower-cost alternatives to original biologics, especially in Europe and Asia, while also intensifying price competition for branded therapies.

What trends will define the antibodies market over the next decade?

Key trends include AI-driven antibody discovery, growth of antibody-drug conjugates (ADCs), expansion of diagnostic antibodies, and increased M&A activity among biotech startups and pharma giants.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com