Global Stem Cell Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Allogeneic and Autologous), Application, End-User and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2024 to 2033

Global Stem Cell Market Size

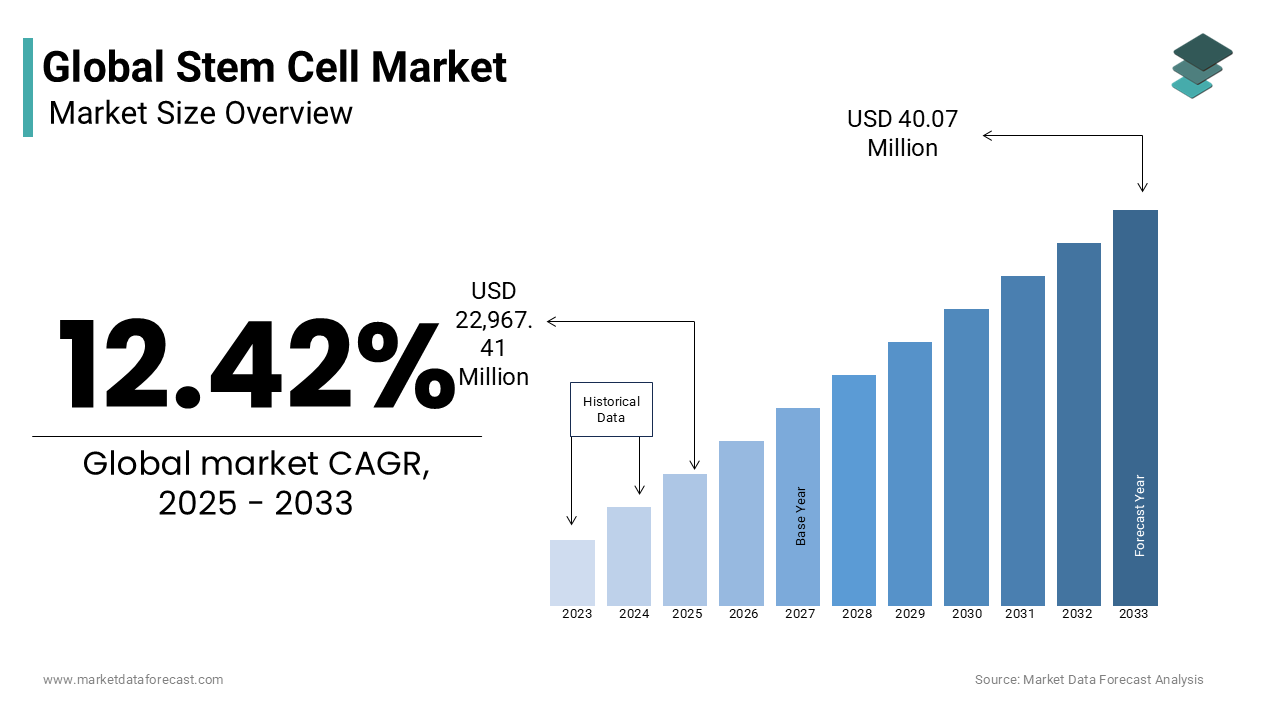

The global stem cell market size was valued at USD 20,430 million in 2024 and is anticipated to reach USD 22,967.41 million in 2025 from USD 58,595.02 million by 2033, growing at a CAGR of 12.42% during the forecast period from 2025 to 2033.

Stem Cells are pivotal in regenerative medicine, disease modeling, and drug discovery, offering transformative potential for conditions with limited therapeutic options. Regulatory advancements, such as Japan’s conditional approval pathway for regenerative products, have accelerated translational research, positioning stem cell science at the forefront of next-generation medical innovation.

MARKET DRIVERS

Advancement in Induced Pluripotent Stem Cell (iPSC) Technology is a principal driver of the stem cell market, enabling the reprogramming of somatic cells into a pluripotent state without the ethical controversies associated with embryonic sources. Japanese groups (including RIKEN) have conducted small early-phase iPSC-derived retinal cell trials with promising functional outcomes in a handful of patients; results have been incremental and reported in staged trial publications. Dozens of iPSC-based programs are underway or planned across indications (ophthalmology, neurology, cardiology, etc.) The technology also facilitates patient-specific disease modelling. Large research consortia (including groups at Broad and other institutes) have created iPSC panels numbering in the low thousands to support disease modeling and screening. Because iPSCs circumvent immune rejection and support personalized therapy development, they are increasingly integrated into precision medicine frameworks, driving both academic and commercial investment.

Rising Prevalence of Chronic and Degenerative Diseases is fueling demand for regenerative therapies, positioning stem cells as a critical frontier in long-term disease management. As per the World Health Organization, non-communicable diseases accounted for 74% of global deaths in 2023, with cardiovascular conditions, diabetes, and neurological disorders representing the most burdensome categories. These trends underscore the inadequacy of conventional treatments in halting disease progression. Stem cell-based interventions, such as MSC infusions for myocardial regeneration and neural stem cell grafts for spinal injury repair, are being explored as disease-modifying solutions. Some early clinical studies have reported modest improvements in ejection fraction (single-digit to low-double digits) in selected cohorts; results are heterogeneous and require larger confirmatory trials.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Ethical Constraints significantly impede the commercialization and clinical translation of stem cell therapies. The U.S. Food and Drug Administration requires rigorous preclinical data, phased clinical trials, and manufacturing compliance under Current Good Tissue Practice (cGTP) standards, which can extend approval timelines beyond a decade. In the European Union, the Advanced Therapy Medicinal Products (ATMP) regulation imposes complex authorization pathways, delaying market access. Additionally, ethical debates persist around the use of embryonic stem cells. These regulatory and moral complexities deter investment and limit the scalability of promising therapies.

Limited Long-Term Safety and Efficacy Data remain a critical restraint, particularly concerning tumorigenicity and immune responses post-transplantation. Without robust post-market surveillance and standardized outcome metrics, skepticism persists among clinicians and payers, slowing adoption even for therapies demonstrating short-term promise.

MARKET OPPORTUNITIES

Integration of Stem Cells with Organoid and 3D Bioprinting Technologies presents a transformative opportunity for disease modeling and tissue engineering. Researchers at the Hubrecht Institute have developed intestinal, cerebral, and hepatic organoids from patient-derived iPSCs, enabling realistic simulation of disease progression and drug response. Like many organoid-based studies were published, with applications ranging from cystic fibrosis treatment prediction to cancer immunotherapy testing. The Wake Forest Institute for Regenerative Medicine successfully implanted lab-grown bladder tissues in pediatric patients using autologous stem cells, demonstrating clinical feasibility. 3D bioprinting platforms, such as those developed by CELLINK, now enable precise deposition of stem cell-laden bioinks to construct vascularized tissues. These advancements reduce reliance on animal models and accelerate therapeutic development, positioning stem cells as foundational tools in next-generation biomedical engineering.

Expansion of Public and Private Biobanking Infrastructure is creating scalable repositories for stem cell preservation and research access. Also, the United Kingdom’s NHS Blood and Transplant service stored 20,000–25,000 cord blood units for hematopoietic stem cell transplantation, while Japan’s Center for iPS Cell Research and Application (CiRA) maintained a bank of 75-100 clinical-grade iPSC lines. Private banks report an annual increase in client enrollment, driven by parental awareness of future therapeutic potential. These biobanks support allogeneic therapy development by providing HLA-typed, quality-controlled cells.

MARKET CHALLENGES

Tumorigenic Risk and Uncontrolled Differentiation remain persistent challenges in stem cell therapy deployment. Pluripotent stem cells, particularly embryonic and iPSCs, possess inherent potential to form teratomas if residual undifferentiated cells persist post-transplantation. The U.S. National Cancer Institute emphasizes that incomplete differentiation protocols and genetic instability during cell culture amplify oncogenic risks. Additionally, heterogeneity in cell populations can lead to unpredictable tissue integration; researchers at Stanford University observed aberrant electrical signaling in iPSC-derived cardiomyocyte grafts implanted in primate hearts. These biological uncertainties necessitate advanced purification techniques and real-time in vivo monitoring, complicating clinical protocols and raising safety thresholds for regulatory approval.

High Costs and Limited Reimbursement Mechanisms hinder widespread clinical adoption of stem cell therapies. Autologous stem cell treatments, such as those for orthopedic regeneration or autoimmune conditions, often exceed $50,000 per procedure, placing them beyond the reach of most patients. In the United States, Medicare does not reimburse for most regenerative procedures outside clinical trials, as per the Centers for Medicare & Medicaid Services. The manufacturing complexity, requiring sterile facilities, skilled personnel, and personalized logistics, contributes to high pricing.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Treatment Mode, Cell Type, Technology Segment, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Athersys, StemCells, Inc., Cryo Cell International, Geron Corporation, Mesoblast Ltd., Aastrom Biosciences, Inc., Celgene Corporation, Invitrogen, and Cytori Therapeutics Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The autologous stem cell therapy segment held the largest share of the global stem cell market of 55.2% in 2024. This dominance is primarily driven by its inherent biological compatibility and reduced risk of immune rejection. Since autologous therapies utilize a patient’s own cells, typically harvested from bone marrow, adipose tissue, or peripheral blood, there is no need for donor matching or long-term immunosuppression. Besides, the rise of point-of-care applications in orthopedics and dermatology has accelerated adoption; the American Academy of Orthopaedic Surgeons notes that more than 50,000 autologous mesenchymal stem cell injections were performed in the U.S. in 2023 for osteoarthritis and tendon injuries. The procedural safety and regulatory favorability further reinforce its position as the preferred modality in regenerative interventions.

The allogeneic stem cell therapy segment is the fastest-growing and is projected to expand at a CAGR of 13.6% in the coming years. Its rapid growth is due to the scalability and off-the-shelf availability of donor-derived cell banks, enabling immediate treatment access without patient-specific manufacturing delays. The Japanese Ministry of Health, Labour and Welfare approved Temcell, an allogeneic MSC therapy for graft-versus-host disease, under a conditional licensing system that allows commercialization after early-phase trials, significantly shortening time-to-market. As per the World Marrow Donor Association, over 35,000 allogeneic transplants were performed globally in 2023, with cord blood units increasingly used due to their immunological flexibility. Furthermore, advancements in HLA-matching algorithms and cryopreservation have improved engraftment success rates. Institutions like the Fred Hutchinson Cancer Center have demonstrated that haploidentical transplants now achieve survival rates exceeding 70%, making allogeneic therapies viable even with partial donor matches.

By Application Insights

The musculoskeletal disorders segment represented the largest application by capturing 32.7% of the market in 2023, as documented by Statista. This position is underpinned by the high global burden of degenerative joint diseases and sports-related injuries. Stem cell therapies, particularly those using mesenchymal stem cells (MSCs), are increasingly deployed to regenerate cartilage, reduce inflammation, and delay joint replacement surgery. A 2023 multicenter trial published in The Lancet Rheumatology showed that intra-articular MSC injections improved knee function scores over months compared to placebo. These clinical outcomes have positioned stem cells as a critical alternative in managing chronic musculoskeletal deterioration.

The Cardiovascular Diseases segment is the fastest-growing application and is projected to grow at a CAGR of 14.2% from 2025 to 2033. This surge is fueled by the urgent need for regenerative solutions in ischemic heart disease, where conventional treatments fail to restore lost myocardial tissue. The World Health Organization identifies cardiovascular diseases as the leading cause of death globally, responsible for 17.9 million deaths annually. Stem cell-based cardiac repair aims to regenerate damaged myocardium using progenitor cells or MSCs. In a 2023 trial led by the Cardiovascular Cell Therapy Research Network and funded by the NIH, patients receiving CD34+ stem cell infusions after myocardial infarction exhibited a 15% improvement in left ventricular ejection fraction within six months. Additionally, Japan’s approval of HeartSheet, a myoblast sheet derived from autologous cells, has validated the feasibility of cardiac tissue engineering. Hence, the momentum toward functional cardiac regeneration is accelerating.

By End User Insights

The Hospitals segment dominated the end-user landscape by representing 63.6% of the stem cell market in 2023, according to Euromonitor International. This preeminence is rooted in their infrastructure for complex, high-acuity procedures such as hematopoietic stem cell transplantation (HSCT) and surgical integration of regenerative therapies. Major academic medical centers, including Mayo Clinic and Johns Hopkins, operate dedicated cell processing laboratories compliant with FDA and AABB standards, ensuring sterility and traceability. Additionally, hospitals are primary sites for clinical trials. Their access to multidisciplinary teams, advanced imaging, and critical care support makes hospitals the natural hub for both established and experimental stem cell interventions.

The clinics segment, particularly specialized regenerative and outpatient medical centers, is the fastest-growing end-user and is expanding at a CAGR of 12.8% from 2025 to 2033. This growth is driven by the proliferation of minimally invasive, same-day stem cell procedures for orthopedic, aesthetic, and neurodegenerative conditions. In countries like Germany and South Korea, medical spas and wellness clinics have integrated stem cell facials and joint rejuvenation into premium service portfolios. However, regulatory scrutiny remains high, underscoring the need for standardized oversight amid rapid expansion.

REGIONAL ANALYSIS

North America occupied the foremost position in the global stem cell market by commanding a 39.6% share in 2024. The region’s position is anchored in robust biomedical research funding, advanced healthcare infrastructure, and a high concentration of clinical trials. The United States, in particular, hosts over 40% of all registered stem cell studies globally, according to the U.S. National Library of Medicine. Canada complements this ecosystem with public cord blood banking and provincial healthcare integration of approved stem cell treatments. With strong intellectual property frameworks and venture capital inflows exceeding $2.3 billion into regenerative startups in 2023, as per PitchBook, North America remains the epicenter of innovation and clinical translation.

Europe holds a notable market share, with Germany, the UK, and Sweden leading in research and clinical deployment. The region benefits from coordinated regulatory oversight through the European Medicines Agency (EMA), which has approved seven advanced therapy medicinal products (ATMPs) based on stem cells as of 2024. The UK’s Medicines and Healthcare products Regulatory Agency (MHRA) has pioneered adaptive licensing pathways, enabling early access to stem cell treatments for rare diseases. Additionally, public healthcare systems in Scandinavia and Germany increasingly reimburse approved cell therapies, enhancing patient access and market stability.

Asia Pacific is a key player in the market, which is propelled by aggressive government investment and progressive regulatory models. China has launched over 600 stem cell clinical trials, second only to the U.S., with the Chinese Academy of Sciences spearheading research in organoid and iPSC technologies. India is emerging as a clinical trial hub due to lower operational costs and a large patient pool. With aging populations in South Korea and Australia driving demand for regenerative solutions, the region is rapidly evolving into a key player in both innovation and commercialization.

Latin America accounts for a notable share of the global market, with Brazil and Mexico emerging as regional leaders. Brazil’s National Health Surveillance Agency (ANVISA) permits the use of autologous stem cells for certain conditions under regulated protocols, fostering a growing network of accredited clinics. Public research institutions like the University of São Paulo are conducting pioneering work in Parkinson’s disease and diabetes using iPSCs. However, regulatory fragmentation and unlicensed clinics offering unproven treatments remain challenges. Despite this, increasing medical tourism, particularly from the U.S. and Europe, drawn by lower costs and accessible therapies, is fueling market expansion. Collaborations with U.S. and European research centers are enhancing technical capabilities and data standardization across the region.

Middle East and Africa collectively hold a decent portion of the market, with Israel and the United Arab Emirates driving regional advancement. Israel’s Ministry of Health supports stem cell research through the Israel Innovation Authority, including pancreatic islet cell development for diabetes. The Weizmann Institute and Hadassah Medical Center are leaders in neural and cardiac regeneration studies. In the UAE, Dubai Healthcare City has established a regulatory framework for regenerative therapies, attracting international clinics and research partnerships. South Africa, despite limited funding, maintains a strong academic presence; the University of Cape Town leads clinical trials in HIV-associated neurocognitive disorders using MSCs. According to the African Academy of Sciences, only 12 stem cell trials were active across sub-Saharan Africa in 2023, constrained by infrastructure gaps. However, rising investment in biotechnology hubs and cross-continental collaborations signal nascent but growing potential.

COMPETITIVE LANDSCAPE

The competition in the Stem Cell Market is characterized by a convergence of biotech innovators, pharmaceutical giants, and specialized regenerative medicine firms vying for dominance in a high-stakes, science-intensive domain. While large corporations leverage financial resources and global distribution, smaller firms differentiate through niche technological expertise and first-mover advantages in novel indications. Geopolitical variations in regulation create both opportunities and fragmentation, with Japan and the U.S. leading in approvals while other regions lag. Intellectual property control over cell lines and differentiation protocols is a key battleground. The scarcity of skilled personnel and GMP facilities further intensifies competition for talent and infrastructure. As clinical validation grows, the market is shifting from experimental offerings to evidence-based therapies, demanding rigorous science, regulatory acumen, and sustainable commercial models to achieve long-term leadership.

KEY MARKET PLAYERS

Some of the notable companies that are profiled in the global stem cell market are

- Athersys

- StemCells, Inc.

- Cryo Cell International

- Geron Corporation

- Mesoblast Ltd

- Aastrom Biosciences, Inc.

- Celgene Corporation

- Invitrogen

- Cytori Therapeutics Inc.

Top Players in the Stem Cell Market

Mesoblast Limited has solidified its presence in the Asia Pacific stem cell landscape through pioneering work in allogeneic mesenchymal precursor cell (MPC) therapies. The Australian biotech firm has advanced its remestemcel-L candidate for pediatric graft-versus-host disease and inflammatory conditions, gaining conditional approval pathways in Japan and New Zealand. The company also partnered with Singapore’s Agency for Science, Technology, and Research to evaluate MPCs in diabetic kidney disease, leveraging regional clinical networks. By aligning with Asia Pacific’s progressive regulatory frameworks and emphasizing off-the-shelf applicability, Mesoblast has positioned itself as a leader in scalable, immune-modulatory cell therapies tailored to regional healthcare demands.

Celgene Corporation (a Bristol-Myers Squibb company) has played a transformative role in advancing hematopoietic stem cell transplantation through its oncology-focused regenerative portfolio. In the Asia Pacific region, Celgene has supported the integration of stem cell-based treatments for multiple myeloma and lymphoma by collaborating with hospitals in South Korea, Australia, and India to standardize high-dose chemotherapy and autologous transplant protocols. Its drug Revlimid, often used in conjunction with stem cell transplants, has become a cornerstone in post-transplant maintenance therapy. By combining pharmacological innovation with cell therapy support, Celgene has strengthened the clinical ecosystem necessary for advanced regenerative oncology across diverse healthcare settings.

Fujifilm Cellular Dynamics, Inc. (formerly CDI) has emerged as a critical enabler of induced pluripotent stem cell (iPSC) research in the Asia Pacific by supplying high-quality, clinical-grade human cells for drug discovery and disease modeling. The company, a subsidiary of Fujifilm, leverages Japan’s leadership in iPSC science to provide standardized cardiomyocytes, neurons, and hepatocytes to pharmaceutical and academic institutions across Japan, China, and Singapore. Additionally, the company introduced a GMP-compliant cell banking service in Osaka, catering to regional biotechs requiring regulatory-compliant materials. By focusing on upstream innovation and infrastructure support, Fujifilm is accelerating the translation of stem cell science into therapeutic development across the region.

Top Strategies Used by Key Market Participants

Key players in the Stem Cell Market are deploying strategic vertical integration, regulatory pathway optimization, international partnerships, technology licensing, and investment in GMP-compliant manufacturing to consolidate their positions. Companies are prioritizing allogeneic “off-the-shelf” platforms to overcome scalability challenges, while leveraging real-world evidence to support reimbursement. Collaborations with academic institutions and government agencies are accelerating clinical validation, particularly in cardiovascular and neurological applications. Expansion into the Asia Pacific is driven by favorable regulatory sandboxes and growing clinical trial infrastructure. Additionally, firms are enhancing supply chain resilience through regional biobanking and cryopreservation networks. Digital tracking, blockchain-enabled chain of identity, and AI-driven cell characterization are being adopted to ensure safety, traceability, and regulatory compliance across complex cell therapy workflows.

RECENT MARKET HAPPENINGS

- In February 2023, Mesoblast partnered with Nipro Corporation in Japan to enhance the distribution and cryopreservation of its allogeneic stem cell therapies, ensuring a stable supply across the Asia Pacific in the Stem Cell Market.

- In May 2023, Fujifilm Cellular Dynamics launched a GMP-compliant iPSC banking facility in Osaka, Japan, to support regional drug developers with clinical-grade human cells in the Stem Cell Market.

- In August 2023, Celgene collaborated with the Asian Society for Blood and Marrow Transplantation to standardize autologous stem cell transplant protocols across South Korea and India in the Stem Cell Market.

- In January 2024, Lonza initiated a new contract manufacturing agreement with a Chinese biotech firm to produce allogeneic MSC therapies for cardiovascular indications in the Stem Cell Market.

- In March 2024, Vericel expanded its European distribution network for MACI, a stem cell-based cartilage repair product, through a partnership with a German orthopedic solutions provider in the Stem Cell Market.

MARKET SEGMENTATION

This research report on the global stem cell market has been segmented and sub-segmented based on the following categories.

By Type

- Autologous stem cell therapy

- Allogeneic stem cell therapy

By Application

- Musculoskeletal disorders

- Cardiovascular diseases

By End User

- Hospitals

- Clinics

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

Who are the major players are in the global stem cell market?

As per our report, the global stem cell market size is predicted to be worth USD 58,595.02 million by 2033.

What is the growth rate of the stem cell market?

For the coming period of 2025 to 2033, the global stem cell market is expected to grow at a CAGR of 12.42%

Which segment by treatment mode is expected to play leading role in stem cell market?

Athersys, StemCells, Inc., Cryo Cell International, Geron Corporation, Mesoblast Ltd., Aastrom Biosciences, Inc., Celgene Corporation, Invitrogen, and Cytori Therapeutics Inc. are some of the notable companies in the global stem cell market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com