Global Pink Himalayan Salt Market Research Report – Segmented By Type (Iodized And Unionized), Application (Food & Beverages, Salt Lamps, Bath Salts, Gourmet Salts And Others), Distribution Channel (Supermarket And Hypermarket, Specialty Stores, Online And Others), And Region(North America, Europe, Asia-Pacific, Latin America, Middle East And Africa) - Global Industry Analysis, Size, Share, Trends & Growth Forecast 2026 to 2034

Market Size, 2025

$13.25 BnMarket Estimate, 2026

$13.82 BnMarket Forecast, 2034

$19.35 BnCAGR, 2026–2034

4.3%Global Pink Himalayan Salt Market Summary

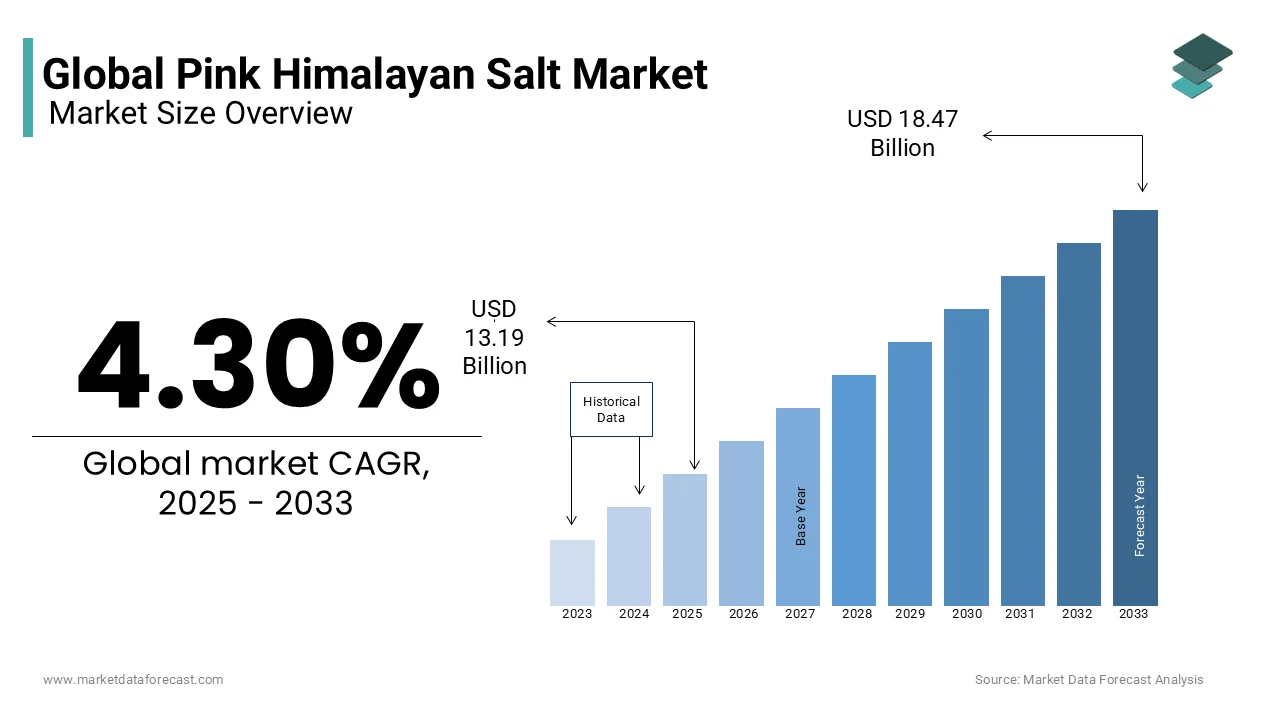

The global pink Himalayan salt market size was valued at USD 13.25 billion in 2025 and is projected to increase from USD 13.82 billion in 2026 to USD 19.35 billion by 2034, registering a steady CAGR of 4.30% during the forecast period. Market expansion is driven by rising demand for natural, mineral-rich salts, increasing adoption in gourmet and functional foods, and the growing popularity of clean-label and chemical-free ingredients. The expanding use of pink Himalayan salt in wellness therapies, personal care formulations, and premium culinary applications is further boosting global demand.

Key Market Trends

- Rising consumer shift toward natural and unprocessed salts due to perceived health benefits and trace mineral content.

- Expanding applications of Himalayan salt in gourmet cooking, artisanal foods, and specialty seasoning blends.

- Growing use of pink Himalayan salt in spa, wellness, bath salts, lamps, and therapeutic products.

- Increasing retail penetration across supermarkets, specialty stores, and online channels, improving product accessibility.

- Strong traction for premium and branded Himalayan salt products, driven by clean-label and sustainable sourcing trends.

Segmental Insights

- Based on type, the uniodized segment dominated the global pink Himalayan salt market in 2025, driven by its natural composition, purity, and rising preference among health-conscious consumers seeking additive-free salt options.

- Based on application, the food & beverages segment accounted for 42.1% of total global consumption in 2025, supported by the growing usage of pink Himalayan salt in cooking, seasoning, packaged foods, and functional nutrition products.

- Based on distribution channel, supermarkets and hypermarkets led the distribution landscape with a 43.6% share in 2025, owing to wide product availability, diverse brand offerings, and strong consumer footfall in retail chains.

Regional Insights

The global market demonstrates strong regional demand, with North America holding a leading position due to widespread consumer adoption of natural salts and premium food ingredients.

- North America dominated the market with 37.4% of global demand in 2025, supported by robust retail presence, rising health-awareness trends, and increased use of Himalayan salt in culinary and wellness products.

Competitive Landscape

The global pink Himalayan salt market is moderately consolidated, with key players focusing on product purity, sustainable sourcing, and expanding their distribution networks. Companies are investing in premium packaging, wellness-oriented product lines, and private-label partnerships to strengthen market presence.

Major players operating in the market include McCormick & Company Inc., K+S AG, BJ's Wholesale Club Holdings Inc., Frontier Co-Op, Kainos Capital (Olde Thompson LLP), Premier Foods plc, HSK Ward Proprietary Limited (McKenzies Foods), and Natierra Superfood

Global Pink Himalayan Salt Market Size

The global pink himalayan salt market size was valued at USD 13.25 Billion in 2025. The global market size is expected to reach USD 19.35 billion by 2034 from USD 13.82 billion in 2026. The market is promising CAGR for the predicted period is 4.30%.

Pink Himalayan Salt is renowned for its distinctive pink hue derived from trace minerals such as iron oxide. Unlike conventional table salt, this unrefined salt is marketed for its purported health benefits, minimal environmental processing, and culinary appeal. As per the Geological Survey of Pakistan, the Khewra mine alone holds estimated reserves of over 220 million tons, with annual extraction averaging 385,000 tons, underscoring its geological significance. The salt’s mineral composition includes up to 98% sodium chloride and traces of magnesium, calcium, and potassium, as per the Pakistan Council of Scientific and Industrial Research. Increasing consumer preference for natural food additives has elevated its use in gourmet kitchens and wellness circles, with Pink Himalayan Salt is exported worldwide.

MARKET DRIVERS

Consumer preference for “natural” and clean-label products is rising in developed markets, which benefits specialty salts like Himalayan salt, is a pivotal driver of the Pink Himalayan Salt Market. Health-conscious consumers are increasingly avoiding refined salts containing anti-caking agents and opting for alternatives perceived as purer and nutritionally superior. This shift is reinforced by growing distrust in synthetic food additives. Moreover, the clean-label movement, championed by major retailers like Whole Foods Market, has integrated Pink Himalayan Salt into certified natural product lines, further legitimizing its market presence. The trend is amplified by social media influencers and wellness advocates who emphasize its aesthetic and holistic appeal.

The expanding application of Pink Himalayan Salt in non-culinary wellness and lifestyle sectors, particularly in spa therapies, salt rooms, and home décor, is another significant driver. The global rise of halotherapy, controlled inhalation of dry salt aerosol, is fueling demand for high-purity salt blocks and granules. Additionally, salt lamps and carved salt tiles have gained traction in interior design, with Salt lamps and carved salt décor have gained traction online. This diversification beyond the kitchen amplifies market resilience.

MARKET RESTRAINTS

The environmental degradation and labor challenges associated with unregulated mining practices in the Khewra region is one major restraint in the Pink Himalayan Salt Market. Despite its vast reserves, the mine operates under outdated infrastructure. Miners often work in poorly ventilated tunnels with limited safety gear, leading to frequent accidents. Furthermore, inefficient mining techniques have led to structural instability, with the Geological Survey of Pakistan has raised general concerns over mining safety. These conditions not only raise ethical sourcing concerns among Western importers but also limit production scalability, discouraging long-term investment from international distributors seeking sustainable supply chains.

The prevalence of counterfeit and adulterated Pink Himalayan Salt in global markets, undermining consumer trust and brand integrity, is another critical restraint. Investigations revealed that counterfeit and adulterated Himalayan salt is a known issue. This proliferation of imitation products stems from the high profit margins and low regulatory oversight in transnational supply chains. Authentic salt from Khewra is distinguishable by its unique crystalline structure and mineral signature, yet portable spectrometers used for verification remain rare in customs inspections. Also, the absence of a globally harmonized certification system enables fraudulent labeling, deterring premium buyers and complicating market differentiation.

MARKET OPPORTUNITIES

The integration of blockchain technology for supply chain transparency, enabling traceability from mine to consumer, is an emerging opportunity. With increasing demand for ethical sourcing, blockchain traceability has been piloted in the food and natural products sector. Also, 73% of global consumers in 2023 expressed willingness to pay a premium for products with verifiable provenance, particularly in the organic and natural goods sector. By embedding QR codes on packaging linked to immutable mining logs, firms can demonstrate compliance with labor and environmental standards. Pakistan has ICT-focused initiatives, aiming to reduce fraud and enhance export credibility. This technological leap could position genuine suppliers as leaders in the ethical mineral trade, capturing value in high-margin markets.

The development of value-added Pink Himalayan Salt derivatives for functional foods and nutraceuticals is another promising opportunity. With rising interest in electrolyte balance and mineral supplementation, manufacturers are incorporating micronized Himalayan salt into hydration tablets, sports beverages, and dietary supplements. Companies such as Ultima Replenisher and LMNT have already launched products featuring Pink Himalayan Salt as a key ingredient, citing its natural electrolyte profile. Himalayan salt contains bioavailable forms of magnesium and potassium, albeit in trace amounts, which may support claims of improved hydration. This pivot toward science-backed functional applications could elevate the salt from a culinary novelty to a legitimate health ingredient.

MARKET CHALLENGES

The lack of standardized regulatory definitions for “natural” and “mineral-rich” claims, leading to inconsistent labeling and consumer confusion, is a significant challenge facing the Pink Himalayan Salt Market. While the U.S. Department of Agriculture does not regulate the term “natural” for salt products, the European Union’s Food Information to Consumers Regulation allows broad interpretations, enabling misleading marketing. Also, a notable share of surveyed consumers believed Pink Himalayan Salt contained significantly more essential minerals than table salt, a perception not supported by nutritional science. The Mayo Clinic emphasizes that the trace mineral content, while present, is too minimal to confer measurable health benefits. This misinformation risks regulatory scrutiny and potential backlash from health authorities, complicating brand positioning and inviting corrective advertising mandates.

The vulnerability of the supply chain to geopolitical and infrastructural instability in Pakistan’s Punjab Province, is another pressing challenge. The Khewra mine, located near the city of Jhelum, relies on a fragile transportation network that is frequently disrupted by monsoon-related landslides and road degradation. Besides, regional energy shortages have hampered processing facilities. These disruptions delay shipments and increase logistics costs, making it difficult for exporters to meet contractual obligations. U.S. importers have reported delays in shipments of Pakistani salt due to supply chain disruptions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.30% |

| Segments Covered | By Type, Application, Distribution Channel And Region. |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Lemonconcentrate S.L.U., Florida Chemical Company (acquired by ADM), Banner Chemicals Limited, Citrus Oleo, Sucorrico, Belize Ltd., Spectrum Chemical, Citrosuco, Firmenich SA, Tropfruit Nordeste S.A. |

SEGMENTAL ANALYSIS

By Type Insights

The uniodized segment dominated the Pink Himalayan Salt Market by capturing a substantial share of total value in 2025. This dominance is due to the core consumer perception that uniodized Himalayan salt retains its natural mineral integrity. Unlike iodized variants, which are often associated with industrial processing, uniodized salt is marketed as a pure, unrefined alternative. The preference is reinforced by wellness communities and functional nutritionists who argue that dietary iodine is sufficiently obtained from seafood and dairy, making added iodine unnecessary and potentially excessive.

The iodized segment is projected to grow at the fastest CAGR of 7.8% from 2026 to 2034. This accelerated growth is primarily driven by public health initiatives in developing economies where iodine deficiency remains a persistent concern. As per the World Health Organization, nearly 2 billion people globally live in iodine-deficient regions, with South Asia and Sub-Saharan Africa bearing the highest burden. In response, governments in countries like Pakistan and Nepal have begun exploring fortified versions of locally produced salts, including iodized Pink Himalayan Salt, to improve compliance with national nutrition programs. This convergence of cultural preference and public health strategy is creating a niche but expanding market.

By Application Insights

The Food & Beverages segment commanded the largest share of the global Pink Himalayan Salt Market at 42.1% of total consumption by volume in 2025. This lead position is anchored in the rising demand for natural flavor enhancers in both home cooking and commercial food production. Gourmet chefs and artisanal food brands increasingly use the salt for its subtle mineral complexity and visual appeal. Also, sales of premium condiments in the U.S. surged. Additionally, the clean-label movement has prompted major food manufacturers like Nestlé and General Mills to reformulate processed products with natural salts.

The Bath Salts segment is expanding at the fastest CAGR of 9.3% during the forecast period. This surge is fueled by the integration of Pink Himalayan Salt into at-home spa routines and therapeutic regimens. The salt’s rich magnesium and sulfate content is believed to support transdermal mineral absorption, a concept gaining traction in dermatological wellness. Brands such as Dr. Teal’s and Bath & Body Works have introduced Himalayan salt-infused bath crystals, contributing to a year-on-year sales increase in the premium bath category.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the leading distribution channel for Pink Himalayan Salt by holding a 43.6% share of global sales in 2025. This dominance is largely due to the integration of the product into mainstream grocery aisles, particularly in developed markets where retailers have expanded their natural and organic sections. Major chains like Walmart, Kroger, and Tesco now feature Pink Himalayan Salt alongside conventional salts, increasing consumer accessibility. Besides, private-label offerings from retailers such as Amazon Basics and Kirkland Signature have enhanced affordability and shelf presence.

The online distribution channel is experiencing the most rapid growth, with a projected CAGR of 12.6% in the coming years. This acceleration is driven by the rise of direct-to-consumer (DTC) branding and the global reach of digital marketplaces. Consumers increasingly seek detailed product provenance, usage guides, and customer reviews—elements that online platforms provide more comprehensively than physical stores. In the U.S., e-commerce sales of health and wellness products grew, with specialty salts forming a notable segment. Besides, social media-driven campaigns by brands have boosted online visibility, with Instagram and TikTok contributing to an increase in digital conversion rates.

REGIONAL ANALYSIS

North America Pink Himalayan Salt Market Insights

North America spearheaded the Pink Himalayan Salt Market by accounting for 37.4% of global demand in 2025. The region’s lead position is underpinned by a deeply entrenched health and wellness culture, particularly in the United States, where functional foods and clean-label products dominate consumer preferences. The rise of paleo, keto, and whole-food diets has further amplified demand, with nutritionists frequently recommending Pink Himalayan Salt as a less processed alternative. Additionally, the U.S. Department of Agriculture’s Organic Trade Association reported that sales of certified organic pantry staples grew, reflecting a broader shift toward mindful consumption that positions Himalayan salt as a staple in health-conscious households.

Europe Pink Himalayan Salt Market Insights

Europe is also a major player in the market. The region’s strong regulatory emphasis on food transparency and sustainability has created a favorable environment for premium mineral salts. Countries like Germany, France, and the United Kingdom have seen a surge in demand for ethically sourced and traceable food products. According to the European Commission’s 2023 Consumer Trends Report, a notable share of EU citizens consider product origin a critical factor in purchasing decisions. This has led major retailers such as Carrefour and EDEKA to partner with certified suppliers from Pakistan’s Khewra mine. Moreover, the proliferation of halotherapy centers across Central Europe has increased institutional demand for high-purity salt, reinforcing both culinary and therapeutic applications in the regional market.

Asia Pacific Pink Himalayan Salt Market Insights

Asia Pacific accounts for a significant share of the global market, with growth concentrated in urban centers of India, Japan, and Australia. Although the salt is mined in Pakistan, domestic consumption in South Asia remains relatively low due to affordability and traditional preferences for iodized table salt. However, rising disposable incomes and exposure to global wellness trends are shifting consumer behavior. Australia’s complementary medicine sector has also embraced Himalayan salt.

Latin America Pink Himalayan Salt Market Insights

Latin America holds a modest market share but exhibits growing momentum, particularly in Brazil and Mexico. The region’s expansion is fueled by increasing health awareness and the influence of North American dietary trends. Additionally, the rise of boutique wellness retreats in Mexico’s Yucatán Peninsula has driven demand for Himalayan salt in spa treatments and architectural installations. Also, gourmet salt usage in high-end restaurants grew annually over the past three years, indicating a cultural shift toward premiumization.

Middle East and Africa Pink Himalayan Salt Market Insights

The Middle East and Africa collectively account for small share of the global market, with the United Arab Emirates and South Africa serving as key entry points. In the UAE, the Ministry of Climate Change and Environment has promoted sustainable food choices. In South Africa, the Health Professions Council has observed a growing interest in holistic therapies, with salt lamps and bath salts becoming common in urban wellness centers.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the prominent players in the global pink Himalayan salt market are

-

McCormick & Company Inc

-

K+S AG

-

BJ's Wholesale Club Holdings Inc

-

Frontier Co-Op

-

Kainos Capital (Olde Thompson LLP)

-

Premier Foods plc

-

HSK Ward Proprietary Limited (McKenzies Foods)

-

Natierra Superfood

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the Pink Himalayan Salt Market are deploying vertical integration, digital traceability, and product diversification to consolidate their positions. Companies are securing mining rights or exclusive supply agreements to ensure raw material control and reduce dependency on third-party vendors. Brand differentiation is achieved through blockchain-based authenticity verification, addressing widespread counterfeiting concerns. Firms are expanding into value-added formats such as bath salts, electrolyte blends, and flavored gourmet variants to capture niche wellness segments. Strategic e-commerce investments, including region-specific online platforms and social media marketing, are enhancing consumer reach. Partnerships with wellness centers, gourmet retailers, and functional food manufacturers are enabling cross-sector penetration. Sustainability messaging, including eco-friendly packaging and ethical labor claims, is increasingly used to appeal to environmentally conscious consumers in developed markets across North America, Europe, and Asia Pacific.

COMPETITON OVERVIEW

Competition in the Pink Himalayan Salt Market is intensifying as both established mineral suppliers and wellness-focused brands vie for consumer trust and market share. The absence of standardized certifications allows for widespread product variation, enabling smaller players to compete on authenticity and storytelling. Larger firms leverage supply chain control, technological innovation, and international distribution networks to maintain advantage. Differentiation increasingly hinges on provenance verification, packaging transparency, and alignment with health trends such as clean eating and holistic wellness. Price competition remains limited due to the premium positioning of the product, but brand credibility is paramount. Companies are investing in scientific validation of health claims and expanding into adjacent wellness categories to reduce reliance on culinary sales alone, creating a dynamic and fragmented competitive landscape shaped by both geological origin and marketing ingenuity.

TOP PLAYERS IN THE MARKET

- Himalayan Gourmet Salt Co., based in Lahore, Pakistan, is a vertically integrated producer with direct access to Khewra Mine blocks, enabling stringent quality control and consistent supply. The company has significantly expanded its footprint in the Asia Pacific region by establishing distribution partnerships with organic food retailers in Australia and Japan. This innovation was introduced in response to rising demand for transparency in New Zealand and South Korea. The company also collaborated with wellness centers in Thailand and Bali to supply bulk salt for spa therapies, diversifying beyond culinary applications and reinforcing its presence in the premium lifestyle segment across Southeast Asia.

- The Spice House, a U.S.-based specialty seasoning importer with growing influence in Asia Pacific, sources premium-grade Pink Himalayan Salt for gourmet and culinary markets. It has strengthened its position in the region by partnering with high-end supermarkets such as City’Super in Hong Kong and Marukai in Japan. It also launched educational campaigns through digital platforms to inform Asian consumers about the differences between refined and natural salts. By emphasizing product purity and culinary versatility, The Spice House has positioned itself as a trusted premium brand, particularly among expatriate communities and urban health-conscious consumers in major metropolitan areas across the region.

- SaltWorks Inc., headquartered in Washington, is a global leader in specialty salt distribution and has deepened its engagement in the Asia Pacific market through e-commerce expansion and strategic alliances. The company launched a dedicated Asia-Pacific portal in early 2023, offering localized shipping and multilingual support to enhance customer experience in markets like Taiwan and the Philippines. It introduced a line of infused Pink Himalayan Salts, flavored with organic herbs and citrus, tailored to regional palates. Additionally, SaltWorks partnered with wellness influencers in Indonesia and Vietnam to promote salt lamps and bath products. These digital-first initiatives have enabled rapid market penetration, particularly in urban wellness circles, while its commitment to sustainable packaging aligns with evolving environmental standards across countries such as Japan and Australia.

RECENT HAPPENINGS IN THE MARKET

- In March 2022, Himalayan Gourmet Salt Co. launched a blockchain-traceable packaging system for its premium salt line, enabling consumers in Japan and Australia to verify the origin and purity of each batch through a QR code, enhancing trust and combating counterfeit products in the Asia Pacific market.

- In August 2022, The Spice House introduced a range of micronized Pink Himalayan Salt blends tailored for the functional snack sector, partnering with health food manufacturers in Singapore to incorporate the mineral salt into plant-based protein bars and electrolyte-enhanced crackers.

- In January 2023, SaltWorks Inc. launched a dedicated e-commerce platform for the Asia Pacific region, featuring localized payment options, multilingual customer support, and fast shipping to Taiwan, the Philippines, and South Korea, significantly improving market accessibility and consumer engagement.

- In June 2023, Himalayan Gourmet Salt Co. partnered with luxury wellness resorts in Bali and Phuket to supply bulk Pink Himalayan Salt for halotherapy rooms and spa treatments, expanding its application beyond food into the high-growth therapeutic wellness segment.

- In November 2023, The Spice House initiated an educational digital campaign across Hong Kong and Malaysia, using influencer collaborations and scientific content to highlight the differences between refined table salt and natural mineral salts, strengthening brand authority in urban health-conscious communities.

MARKET SEGMENTATION

This research report on the global pink Himalayan salt market has been segmented and sub-segmented based on type, application, distribution channel, and region.

By Type

- Iodized

- Unionized

By Application

- Food & Beverages

- Salt Lamps

- Bath Salts

- Gourmet Salts

- Others

By Distribution Channel

- Supermarket and Hypermarket

- Specialty Stores

- Online

- Others

By Region

- North America

- Europe

- Asia – Pacific

- Middle East and Africa

- Latin America

Frequently Asked Questions

1. What is pink Himalayan salt?

Pink Himalayan salt is a natural rock salt mined from the Khewra Salt Mine in Pakistan, known for its pink color due to trace minerals.

2. Why is pink Himalayan salt popular worldwide?

It is marketed as a healthier alternative to table salt, with minerals, unique flavor, and wellness benefits.

3. What factors are driving the growth of the global pink Himalayan salt market?

Rising health consciousness, demand for natural food products, and increased use in wellness, spa, and beauty industries.

4. Which region dominates the global pink Himalayan salt market?

North America and Europe are the largest consumers, while Asia-Pacific is emerging as a fast-growing market.

5. What are the main applications of pink Himalayan salt?

It is used in food seasoning, cooking, decorative lamps, spa treatments, detox baths, and therapeutic practices.

6. What distribution channels are most common for pink Himalayan salt?

Supermarkets, specialty stores, health food stores, and online platforms are major sales channels.

7. What challenges does the pink Himalayan salt market face?

High cost, counterfeit products, and competition from sea salt and other mineral salts.

8. Who are the key players in the global pink Himalayan salt market?

Key companies include SaltWorks Inc., The Spice Lab, HimalaSalt, Frontier Co-op, and Khewra Salt Mines.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com