- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Global Procurement as a Service Market Size

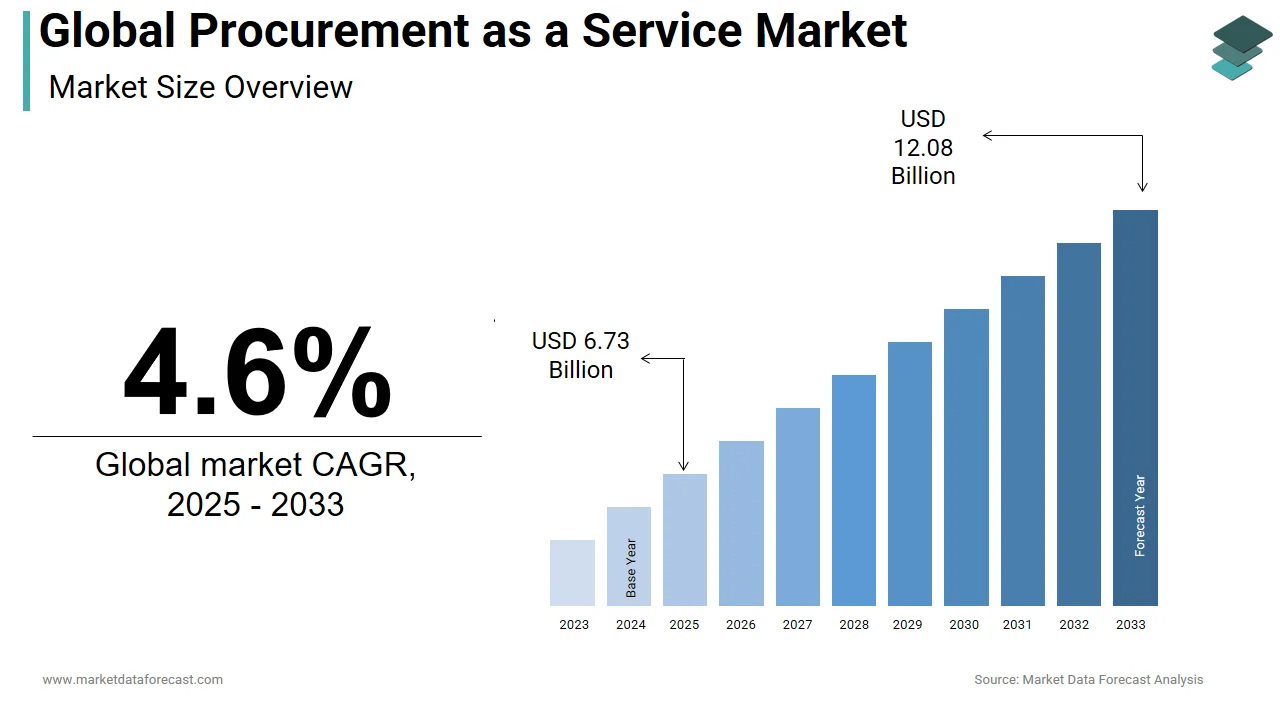

The global procurement as a service market was valued at USD 6.25 billion in 2024. The global market is predicted to reach USD 6.73 billion in 2025 and USD 12.08 billion by 2033, growing at a compound annual growth rate (CAGR) of 7.6% over the foreseen period.

Traditionally, the acquisition has been considered behind the scenes, but its professionals have gradually been recognized in recent years. Although the acquisition integrates platforms, for example, a platform as a service and software as a service, the acquisition as a service platform is currently in its initial phase. The services provided during purchase as a service include KPO, outsourcing of business procedures (BPO), audit and quality control, and supplier management.

Procurement as a Service is an outsourced procurement business model that combines personnel, technology, and experience to manage a part or complement the purchasing functions of the user organization. Technology is helping service providers to examine where their customers are spending money and where they are likely to realize potential savings. Purchase-as-a-service offers help end users select categories for procurement and assign category experts to manage purchases for those categories. These services are technology-based for procurement and sourcing, tracking payments and purchases, and managing tripartite correspondence to ensure that users only pay for what they get. Several suppliers, as a service, make the whole process visible to the companies they work with, usually via reporting portals.

MARKET TRENDS

Strategic sourcing is an essential part of any business, regardless of industry. Strategic sourcing includes analyzing what an organization buys, from whom, at what price, and at what volume. Strategic sourcing involves several activities, including identifying external business expenses, completing the Request for Proposal (RFP) / Request for Quotation (RFQ) process, negotiating prices with suppliers, and implementing contract placements. Strategic sourcing involves finding the balance between the quality of goods and services and their price. Strategic sourcing service providers are experienced in a variety of sourcing activities and offer sourcing as a business services marketplace to streamline your sourcing operations.

Increased global competition and increased consumer demand induce companies to differentiate themselves from their competitors. Manufacturing companies must offer higher quality at lower prices, newer features, and shorter production times, maintaining a market presence and managing costs effectively. As a result, manufacturing companies are gradually adopting outsourcing of supplies and technology solutions that enable them to streamline their manufacturing processes and realize significant savings. This, in turn, allows them to focus on their areas of competence, such as manufacturing, production, and on-time delivery skills. Procurement as a service in manufacturing supports processes such as expense analysis, procurement and category management, supplier management, Procure-to-Pay (P2P) process management, and Source-to-Pay (S2P), as well as supply chain planning and cost management.

MARKET DRIVERS

The global procurement-as-a-service market is expected to experience impressive growth during the forecast period. The growing demand from companies to streamline procurement processes and the positive impact of BPO's evolution on outsourcing are the main drivers of the global procurement-as-a-service market.

MARKET RESTRAINTS

In addition, major technology development initiatives by several major companies are also expected to stimulate demand during the outlook period. However, concerns about data security may slow growth. Despite this limitation, the lucrative opportunities of emerging economies should offer many growth opportunities to actors operating in the procurement-as-a-service market during the foreseen period.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 7.6% |

| Segments Covered | By Component, Organization Size, Vertical, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Proxima (UK), Genpact (US), WNS (India), Capgemini (France), IBM (US), HCL Technologies (India), Infosys (India), Accenture (Ireland), GEP (US), Wipro (India), TCS (India), Aegis (India), Xchanging (UK), Corbus (India), CA Technologies (US) and Others. |

REGIONAL ANALYSIS

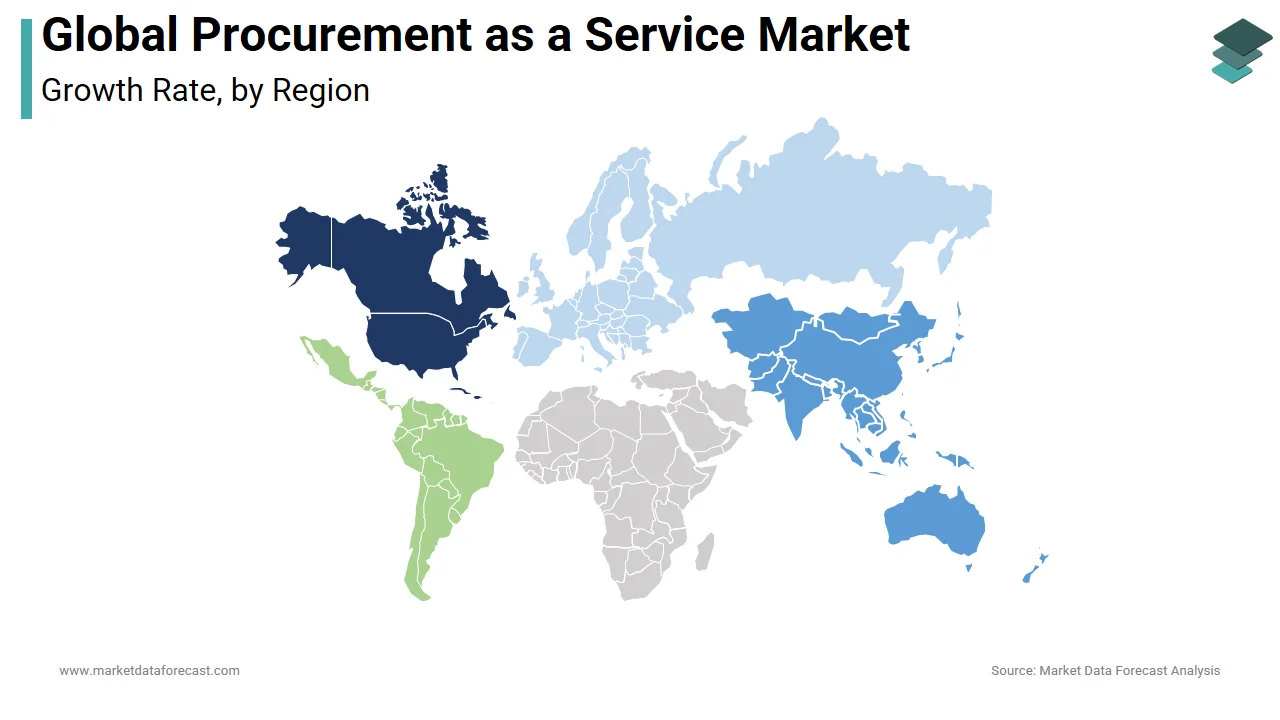

North America had the largest share of the global procurement as a service market in 2024, contributing more than 30% to total revenue. Asia Pacific and Europe ranked second and third, respectively, in the global procurement as a service market in 2019. The Asia Pacific market is foreseen to expand with a CAGR of 7.6% during the forecast period.

KEY MARKET PLAYERS

Product development is a common strategy for companies to expand their product portfolio. Accenture, Infosys Ltd., CAPGEMINI SE, and IBM Corporation are among the market players implementing this strategy to expand the customer base and gain significant market share on a global scale, allowing them to maintain their brand in the market.

The key players operating in the global procurement as a service merchant include Proxima (UK), Genpact (US), WNS (India), Capgemini (France), IBM (US), HCL Technologies (India), Infosys (India), Accenture (Ireland), GEP (US), Wipro (India), TCS (India), Aegis (India), Xchanging (UK), Corbus (India), CA Technologies (US), and so forth.

RECENT MARKET HAPPENINGS

- In January 2019, Accenture launched SynOps, a human-powered engine that leverages data, advanced analytics, and artificial intelligence (AI) to help organizations execute smart operations in key business functions. These functions include finance and accounting, marketing, and acquisitions.

- In November 2018, Accenture acquired Intrigo Systems, a framework integration and consulting service provider for cloud and SAP solutions, working in e-commerce, the store network, and purchasing. The acquisition strengthens Accenture's ability to provide businesses with a purchasing transformation and inventory network.

MARKET SEGMENTATION

This research report on the global procurement as a service market has been segmented and sub-segmented based on the component, organization size, vertical, and region.

By Component

- Strategic Sourcing

- Spend Management

- Category Management

- Process Management

- Contract Management

- Transactions Management

By Vertical

- IT and Telecommunications

- Consumer Goods and Retail

- Manufacturing

- Energy and Public Services

- Healthcare

- Hotels and Tourism

By Organization Size

- SMEs

- large

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa