Global Rare Earth Elements Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Lanthanum, Cerium, Neodymium, Praseodymium, Samarium, Europium, Others), Application and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2025 to 2033

Rare Earth Elements Market Summary

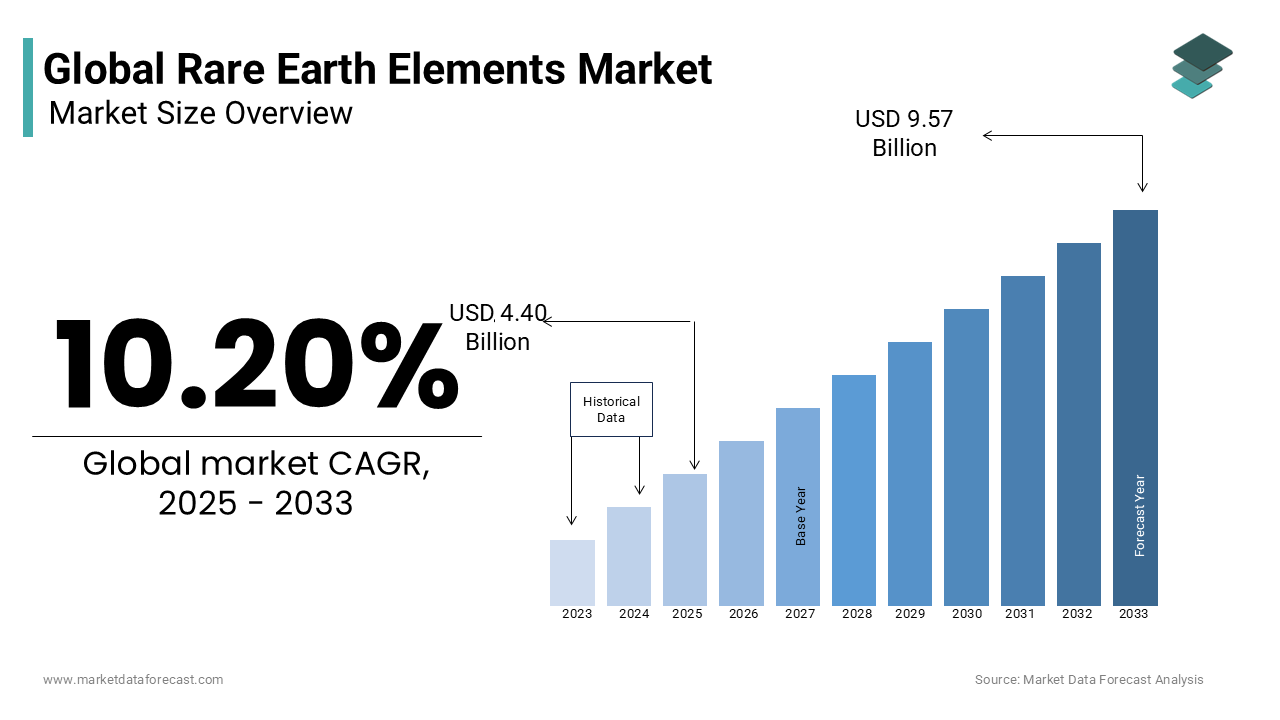

The global rare earth elements market was valued at USD 3.99 billion in 2024, is projected to reach USD 4.40 billion in 2025 and USD 9.57 billion by 2033, expanding at a CAGR of 10.20% from 2025 to 2033. The growth of the rare earth elements market is driven by rising demand for renewable energy technologies, rapid adoption of electric vehicles (EVs), expansion in consumer electronics, and increasing defense applications where high-performance magnets and alloys are critical.

Key Market Trends

- Rising adoption of neodymium-based magnets in EV motors and wind turbines.

- Increasing focus on supply chain diversification outside of China.

- Strong demand for miniaturized electronics and advanced consumer devices.

- Government-backed strategic reserves and recycling initiatives to ensure supply security.

- Ongoing R&D for sustainable mining and rare earth recycling technologies.

Segmental Insights

- Based on type, the neodymium segment dominated the rare earth elements market in 2024, holding 32.1% of the global share, driven by its extensive use in permanent magnets.

- Based on application, the magnets segment was the largest, capturing 41.3% share in 2024, supported by strong demand from clean energy, EVs, and advanced electronics.

Regional Insights

Asia-Pacific was the top performer in the global rare earth elements market in 2024, accounting for a significant share, with China maintaining dominance across mining, refining, and export supply chains. Australia and India are increasing production capacities, while North America is strengthening domestic processing and recycling capabilities to reduce dependency on imports. Europe is focusing on sustainable sourcing and circular economy models, supporting long-term demand.

Competitive Landscape

The global rare earth elements market is moderately consolidated, with China retaining a dominant position in global supply. Companies are investing in new mines, advanced separation technologies, and partnerships with EV and electronics manufacturers to secure long-term contracts.

Key players in the market include:

- China Northern Rare Earth (Group) High-Tech Co., Ltd.

- Lynas Rare Earths Ltd

- MP Materials Corp.

- Iluka Resources Ltd

- Arafura Resources Ltd

- Avalon Advanced Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

- Hitachi Metals Ltd

- Indian Rare Earth Limited (IREL)

Global Rare Earth Elements Market Size

The global rare earth elements market was valued at USD 3.99 billion in 2024, is estimated to reach USD 4.40 billion in 2025, and is projected to reach USD 9.57 billion by 2033, growing at a CAGR of 10.20% from 2025 to 2033.

Rare earth elements (REEs) comprise a group of 17 chemically similar metallic elements, including the 15 lanthanides, scandium, and yttrium by enabling high-performance technologies due to their unique magnetic, luminescent, and electrochemical properties. These elements are indispensable in modern applications such as permanent magnets, electric vehicle (EV) motors, wind turbine generators, and defense systems. According to the U.S. Geological Survey, neodymium and praseodymium are now essential in over 90% of high-strength permanent magnets used in advanced propulsion systems.

MARKET DRIVERS

Expansion of Electric Vehicle Production and Permanent Magnet Demand

The shift toward electric mobility, which are vital for manufacturing high-efficiency neodymium-iron-boron (NdFeB) magnets used in EV traction motors is accelerating the growth of rope market. According to the International Council on Clean Transportation, over 14 million battery electric and plug-in hybrid vehicles were produced globally in 2023, each requiring between 1 and 3 kilograms of rare earth oxides for motor assembly. Tesla’s Model S and Model 3, along with most premium EVs from BMW, Nissan, and Rivian, rely on REE-based motors for superior power density and thermal stability. The European Automobile Manufacturers Association confirms that 85% of new electric drivetrains in Europe incorporate rare earth magnets.

Deployment of Offshore and Direct-Drive Wind Turbines

The rapid scaling of wind energy, particularly offshore installations utilizing direct-drive generators, is significantly increasing the growth of rare earth elements market. Unlike geared turbines, direct-drive systems eliminate mechanical gearboxes and instead use large permanent magnets made from neodymium and dysprosium by enhancing reliability and reducing maintenance in remote marine environments. As per the Global Wind Energy Council, over 12 gigawatts of offshore wind capacity were commissioned in 2023, with 70% of new turbines employing direct-drive technology. Siemens Gamesa and GE Renewable Energy have both standardized REE-based generators in their offshore platforms, with GE’s Haliade-X model alone consuming over 2,600 kilograms of neodymium per unit.

MARKET RESTRAINTS

Geopolitical Concentration of Mining and Processing Infrastructure

The rare earth supply chain is heavily concentrated in China, which controls over 60% of global mining output and an estimated 85% of refining capacity. The Pentagon’s 2023 Critical Minerals Assessment identified dysprosium and terbium as having the highest supply risk due to single-source dependency. In 2022, China imposed export controls on gallium and germanium, raising concerns that similar restrictions could extend to rare earths. The European Commission has classified REEs as critical raw materials with a high supply risk, noting that no European facility currently possesses full-scale separation capability for mixed rare earth concentrates. This geopolitical imbalance limits strategic autonomy and complicates long-term procurement planning for industries reliant on uninterrupted REE access.

Environmental and Regulatory Hurdles in Mining and Refining Operations

The rare earth extraction and processing generate substantial environmental impacts, including radioactive waste, acid leaching, and water contamination, which have led to stringent regulatory barriers in many countries. According to the Canadian Environmental Assessment Agency, a single rare earth processing plant can produce up to 2,000 tons of low-level radioactive waste annually, requiring secure long-term storage. In Australia, Lynas Rare Earths’ processing facility in Malaysia has faced repeated regulatory scrutiny and public opposition over radiological safety, delaying expansion plans. These environmental complexities increase project timelines, capital costs, and social license challenges, which is deterring investment in new non-Chinese supply chains.

MARKET OPPORTUNITIES

Development of Urban Mining and End-of-Life Recycling Infrastructure

Urban mining is the recovery of rare earths from end-of-life electronics, EV motors, and industrial equipment to diversify supply and reduce environmental impact, which is escalating the growth of rope market. According to the United Nations Institute for Training and Research, less than 1% of rare earths are currently recycled globally, indicating vast untapped potential. According to European Environment Agency, over 10 million tons of electronic waste were generated in the EU in 2023, containing recoverable neodymium and dysprosium from hard drives and motors. Companies like Hydromet in Estonia and Noveon Magnetics in the U.S. have developed hydrometallurgical and direct recycling processes that recover over 95% of rare earths from shredded magnets.

Advancements in Substitute-Free and Reduced-REE Magnet Technologies

Innovation in magnet design is creating opportunities to reduce or eliminate rare earth content without sacrificing performance, which is likely to escalate the growth of rope market. According to Oak Ridge National Laboratory, FeN magnets could theoretically achieve energy products exceeding 100 MGOe, surpassing conventional NdFeB magnets. Meanwhile, Toyota has commercialized a reduced-dysprosium magnet for hybrid vehicles, cutting usage by 50% through grain boundary diffusion technology. As per the International Electrotechnical Commission, over 30% of new industrial motors launched in 2023 featured low- or zero-REE designs, which is indicating a structural shift in material engineering.

MARKET CHALLENGES

High Capital Intensity and Long Development Timelines for Non-Chinese Projects

Establishing rare earth mining and processing facilities outside China requires substantial capital investment and extended development periods, which is a challenging factor for the growth of rope market. The Mountain Pass expansion project in the U.S. required over $400 million in investment and took eight years to resume partial operations after bankruptcy. In Greenland, the Kvanefjeld project was delayed indefinitely in 2021 due to political and environmental opposition, despite holding one of the world’s largest undeveloped REE deposits.

Complex Separation and Purification Processes Due to Chemical Similarity

The technical difficulty of separating individual rare earth elements due to their nearly identical ionic radii and chemical behavior is also to degrade the growth of rope market. Extracting high-purity oxides (99.99% or higher) requires hundreds of solvent extraction stages, consuming vast amounts of chemicals and energy. According to the U.S. Department of Energy, producing one ton of separated neodymium generates approximately 75 cubic meters of wastewater and 1.4 tons of radioactive thorium byproduct. These inefficiencies increase production costs and environmental liabilities. While membrane separation and ionic liquid technologies are under development, they remain in pilot phases.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Application and Region. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

| Key Market Players | China Northern Rare Earth (Group) High-Tech Co., Ltd., Lynas Rare Earths Ltd, MP Materials Corp., Iluka Resources Ltd, Arafura Resources Ltd, Avalon Advanced Materials Inc., Shin-Etsu Chemical Co., Ltd., Hitachi Metals Ltd, and Indian Rare Earth Limited (IREL). |

SEGMENTAL ANALYSIS

By Type Insights

The neodymium segment was accounted in holding 32.1% of the global rare earth elements market share in 2024 with its indispensable role in the production of high-performance permanent magnets used in electric vehicle (EV) motors, wind turbine generators, and precision industrial equipment. According to the International Energy Agency, over 90% of modern EV traction motors utilize neodymium-iron-boron (NdFeB) magnets due to their unmatched energy density and thermal stability. The integration into consumer electronics and robotics is additionally to enhance the growth of segment. Apple Inc. disclosed in its 2023 Environmental Progress Report that every iPhone vibration motor and iPad speaker contains neodymium-based magnets, with over 230 million iPhones sold annually.

The praseodymium segment is expected to grow with a CAGR of 9.6% from 2025 to 2033 with its increasing use in high-strength permanent magnets. Automakers such as BMW and Tesla are adopting NdPr (neodymium-praseodymium) magnets to enhance motor efficiency and durability in performance models and long-range vehicles. As per Global Wind Energy Council, offshore wind turbines, which require enhanced magnet stability, use NdPr ratios as high as 3:1. Additionally, the U.S. Department of Defense has initiated programs to secure praseodymium supplies for next-generation radar and sonar systems with its strategic importance.

By Application Insights

The magnets application segment dominated the rare earth elements market with 41.3% of share in 2024 with the irreplaceable role of neodymium, praseodymium, and dysprosium in manufacturing NdFeB permanent magnets, which deliver superior magnetic strength, compact size, and energy efficiency. According to the European Automobile Manufacturers Association, over 85% of new EV models launched in 2023 featured permanent magnet synchronous motors (PMSMs), each requiring 1–3 kilograms of rare earth oxides. As per the International Federation of Robotics, over 500,000 industrial robots were installed globally in 2023, nearly all incorporating rare earth magnets in their joint actuators and servo drives.

The batteries segment is projected to grow at a CAGR of 11.4% from 2025 to 2033 with the use of lanthanum and cerium in nickel-metal hydride (NiMH) batteries, which remain critical in hybrid electric vehicles (HEVs) and aerospace systems despite the rise of lithium-ion technology. Moreover, emerging solid-state battery research is exploring cerium-doped electrolytes to enhance ionic conductivity and thermal stability. Researchers at the Massachusetts Institute of Technology have demonstrated that cerium oxide nanoparticles improve dendrite suppression in lithium-metal cells, increasing cycle life by up to 40%.

REGIONAL ANALYSIS

Asia Pacific Rare Earth Elements Market Analysis

Asia-Pacific was the top performer of the global rare earth elements market by capturing a significant share in 2024. China dominated the regional landscape, producing over 70% of the world’s rare earths and controlling nearly 90% of refining capacity, according to the Chinese Society of Rare Earths. China’s dominance extends to downstream applications, with the country manufacturing 75% of the world’s permanent magnets, as confirmed by the Ministry of Industry and Information Technology. Japan and South Korea, while lacking domestic mining, are major consumers, relying on secure supply agreements with China for EV and electronics manufacturing.

North America Rare Earth Elements Market Analysis

North America rare earth production and 18% of refined consumption, as documented by the U.S. Department of the Interior. The United States maintains a strategic foothold through the Mountain Pass mine in California, the only operational rare earth mine in the Western Hemisphere, which produced 43,000 metric tons of concentrate in 2023. The U.S. Department of Defense has funded six rare earth magnet recycling and refining projects since 2021 under the Defense Production Act, aiming to establish a secure supply chain for defense systems.

Europe Rare Earth Elements Market Analysis

Europe rare earth elements market growth is likely to have a significant CAGR during the forecast period. The region is highly dependent on imports from China, for magnets used in wind turbines, EVs, and aerospace. The European Raw Materials Alliance aims to produce 20% of the EU’s annual rare earth demand by 2030 through urban mining and secondary recovery. According to the Fraunhofer Institute, end-of-life recycling could supply up to 30% of Europe’s neodymium needs by 2035. Sweden’s Per Geijer deposit in the Norra Kärr area contains one of the largest europium and yttrium resources in Europe, with test drilling confirming 110,000 tons of rare earth oxides.

Middle East & Africa Rare Earth Elements Market Analysis

The Middle East and Africa rare earth elements market growth is attributed to grow with significant potential in Southern and East Africa. Burundi’s Gakara project, operated by Rainbow Rare Earths, has achieved commercial production with grades exceeding 40% total rare earth oxides, among the highest globally. Namibia’s Lofdal project is being developed for its high dysprosium and terbium content, critical for high-temperature magnets. According to the International Renewable Energy Agency, African nations are increasingly linking rare earth development to green industrialization, with Namibia and Botswana exploring processing zones to add value before export.

Latin America Rare Earth Elements Market Analysis

Latin America rare earth market growth is likely to grow with Brazil and Argentina leading exploration efforts. Brazil possesses one of the world’s largest niobium deposits at Araxá, which co-occurs with rare earths, enabling integrated extraction. The Brazilian Nuclear Energy Commission reports that monazite sands along the southeastern coast contain over 1.8 million tons of rare earth oxides, though development has been slow due to environmental regulations. Argentina’s Salar de Olaroz hosts lithium-rich brines with recoverable cerium and lanthanum with Lithium Americas exploring co-extraction methods.

COMPETITIVE LANDSCAPE

The rare earth elements market features a highly asymmetric competitive landscape, dominated by China’s integrated control over mining, refining, and magnet production, while non-Chinese players strive to establish resilient alternatives. Competition is less about price and more about supply security, technological capability, and regulatory compliance. Global players face the dual challenge of replicating China’s decades-long infrastructure buildup while adhering to stricter environmental and social governance standards. The race is intensifying in downstream segments, particularly in magnet and recycling technologies, where innovation determines strategic relevance. Governments are actively intervening through subsidies and defense contracts to support domestic champions.

Key Market Participants

A few of the major companies in the global rare earth elements market include

- China Northern Rare Earth (Group) High-Tech Co., Ltd.

- Lynas Rare Earths Ltd

- MP Materials Corp.

- Iluka Resources Ltd

- Arafura Resources Ltd

- Avalon Advanced Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

- Hitachi Metals Ltd

- Indian Rare Earth Limited (IREL)

- Top Players in the Rare Earth Elements Market

- China Northern Rare Earth (Group) High-Tech Co., Ltd.

Top Players in the Rare Earth Elements Market

China Northern Rare Earth, headquartered in Baotou, Inner Mongolia, is a pivotal force in the Asia-Pacific rare earth sector, operating the world’s largest rare earth production and processing complex integrated with the Bayan Obo mine. The company dominates the supply of light rare earths, particularly neodymium and praseodymium, which are essential for magnet manufacturing. In 2023, it expanded its separation capacity by 20,000 metric tons annually to meet rising demand from EV and wind turbine producers.

Lynas Rare Earths Ltd

Lynas Rare Earths has emerged as the most significant rare earth producer outside China, with its flagship Mt. Weld mine in Western Australia supplying high-grade concentrate to its processing facility in Malaysia. The company plays a critical role in diversifying global supply, particularly for neodymium and praseodymium used in clean energy technologies. In 2022, Lynas secured a $120 million U.S. Department of Defense grant to build a magnet manufacturing facility in Texas, marking a strategic expansion into downstream production. In Asia-Pacific, it strengthened its position by finalizing a rare earth separation plant in Kalgoorlie, Australia, set to begin operations in 2025, which will reduce reliance on Malaysian refining.

Iluka Resources Limited

Iluka Resources has strategically pivoted from mineral sands to become a key contender in the Asia-Pacific rare earth value chain, focusing on the development of the Eneabba Rare Earths Refinery in Western Australia. The project, launched in 2023, aims to produce high-purity separated rare earth oxides, including neodymium, praseodymium, and dysprosium, from monazite feedstock sourced from its own operations and third parties. This initiative positions Iluka as the first fully integrated rare earth refiner in Australia, reducing regional dependency on Chinese processing. The company has entered into offtake discussions with European and Japanese manufacturers seeking alternative supply chains. Additionally, Iluka is advancing its Dubbo Zirconia Project to co-produce rare earths from zircon processing residues.

Top Strategies Used by Key Market Participants

Key players in the rare earth elements market are deploying vertical integration, geopolitical diversification, and technological innovation to consolidate their positions. Companies are expanding from mining into separation and magnet manufacturing to capture higher value and ensure downstream control. Strategic partnerships with governments and defense agencies are securing funding for non-Chinese supply chains, as seen in U.S. and Australian initiatives. Investment in recycling technologies is accelerating to recover rare earths from end-of-life electronics and industrial motors, reducing primary extraction dependence. Firms are also advancing solvent-free and low-waste separation methods to meet environmental standards.

MARKET SEGMENTATION

The research report on the Rare Earth Elements Market has been segmented and sub-segmented based on categories.

By Type

- Lanthanum

- Cerium

- Neodymium

- Praseodymium

- Samarium

- Europium

- Others

By Application

- Magnets

- Metallurgy

- Batteries

- Polishing Agent

- Glass and Ceramics

- Catalyst

- Phosphors

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What are rare earth elements?

Rare earth elements (REEs) are a group of 17 chemical elements, including lanthanides, scandium, and yttrium, used in high-tech applications such as electronics, renewable energy, and defense.

Who are the leading players in the rare earth elements market?

Key players include Lynas Corporation Ltd., China Northern Rare Earth Group, MP Materials, Arafura Resources, Iluka Resources, Alkane Resources Ltd., China Minmetals Rare Earth Co., Ltd., and Rare Element Resources.

What factors are driving the growth of the rare earth elements market?

Growth is driven by increasing demand for electric vehicles, renewable energy technologies, consumer electronics, and government initiatives supporting strategic minerals.

What are the challenges in the rare earth elements market?

Challenges include environmental concerns in mining, supply chain dependency on a few countries (especially China), and high production costs.

What is the future outlook of the rare earth elements market?

The market is expected to grow steadily due to rising adoption of electric vehicles, renewable energy technologies, and advanced electronics, with efforts to diversify the supply chain globally.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com