Global Release Agents Market Size, Share, Trends & Growth Forecast Report – Segmented By Composition (Emulsifiers, Antioxidants, Vegetable Oils, Wax & Wax Esters), Application (Bakery & Confectionery, Meat, And Processed Food), Type (Fluid, Solid, And Others), And Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2026 To 2034)

Market Size, 2025

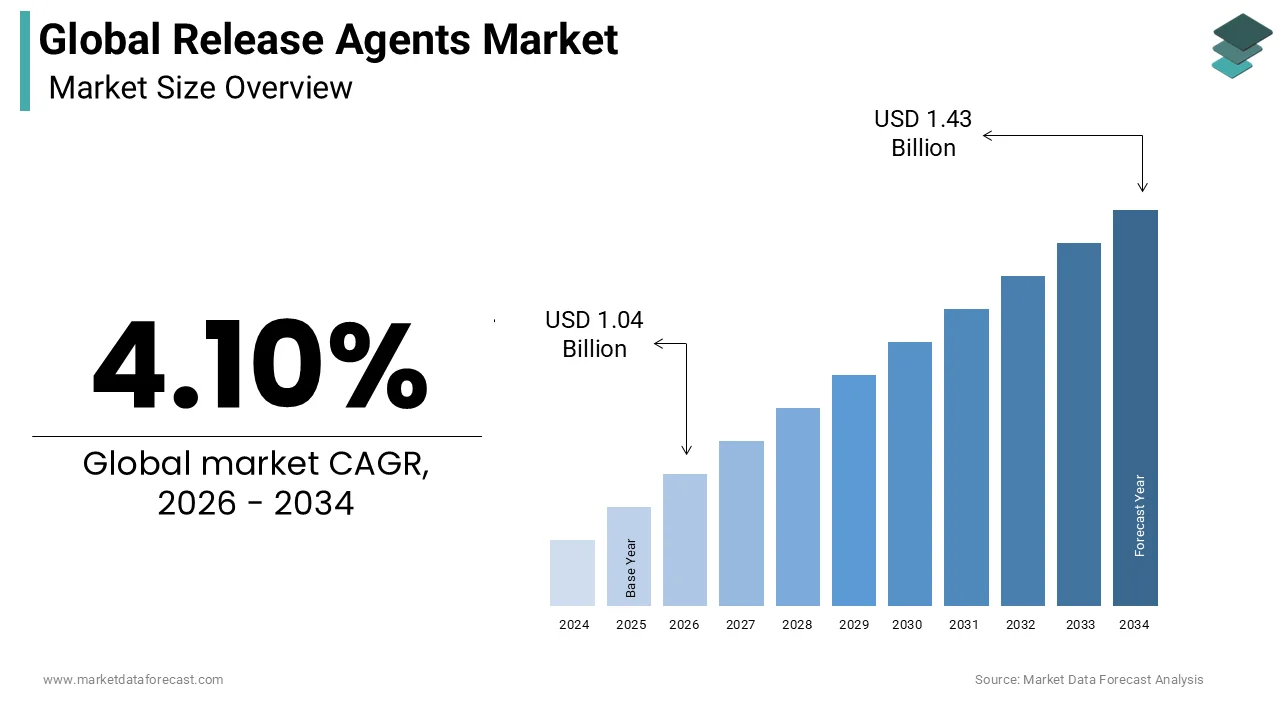

$1.01 BnMarket Estimate, 2026

$1.04 BnMarket Forecast, 2034

$1.43 BnCAGR, 2026–2034

4.1%Global Release Agents Market Size

The global release agents market size was calculated to be USD 1.00 billion in 2025 and is anticipated to be worth USD 1.43 billion by 2034 from USD 1.04 billion in 2026, growing at a CAGR of 4.10% during the forecast period.

Release agents are specialized chemical substances applied to molds, dies, or surfaces to prevent adhesion of materials during manufacturing processes such as injection molding, die casting, and composite fabrication. These agents ensure smooth demolding, reduce surface defects, and extend the lifespan of production equipment by minimizing wear and contamination. Depending on the application, release agents can be water-based, solvent-based, silicone-based, or formulated with synthetic oils, each offering specific performance benefits in terms of thermal resistance, film formation, and residue control. Additionally, environmental regulations are influencing formulation choices, pushing manufacturers toward eco-friendly and biodegradable options. As per the European Chemicals Agency (ECHA), regulatory scrutiny on volatile organic compounds (VOCs) has led to a shift from solvent-based to water-based and low-VOC alternatives across key markets in Europe and North America. Moreover, the growing use of automated spraying systems and robotic mold cleaning technologies is enhancing the efficiency of release agent application, further driving their adoption in precision manufacturing environments.

MARKET DRIVERS

Growth in Automotive and Aerospace Manufacturing

A significant driver of the release agents market is the sustained expansion of the automotive and aerospace industries, both of which rely heavily on complex molding and casting techniques. The demand for lightweight, high-strength components in electric vehicles (EVs) and next-generation aircraft has intensified the use of advanced composite materials, which is necessitating effective release solutions to maintain production efficiency and part quality. Similarly, the aerospace sector is witnessing rising demand for carbon fiber-reinforced polymer (CFRP) components due to their superior strength-to-weight ratio. Manufacturers such as Airbus and Tesla have adopted automated mold lubrication systems using silicone and semi-permanent release agents to improve repeatability and reduce maintenance downtime.

Rising Demand for Molded Plastics in Consumer Goods and Packaging

Another key driver fueling the release agents market is the growing reliance on plastic molding processes in the production of consumer goods and packaging materials. Injection molding remains the preferred method for manufacturing items such as containers, caps, toys, medical devices, and household appliances, all of which require efficient mold release to ensure consistent output and aesthetic finish. As per PlasticsEurope, global plastics production exceeded 400 million metric tons in 2023, with packaging accounting for nearly 40% of total plastic consumption worldwide. The increasing use of thin-wall and multi-cavity molds in food packaging and disposable products has heightened the necessity for release agents that facilitate rapid demolding without compromising hygiene standards. In addition, the rise of custom-shaped and textured plastic components in premium consumer electronics and personal care products has driven demand for release agents that offer clean separation, minimal residue, and compatibility with high-gloss finishes. Companies like Procter & Gamble and Unilever have integrated advanced mold release systems into their packaging supply chains to enhance productivity and reduce rework. Furthermore, the shift toward sustainable packaging has prompted the development of bio-based polymers such as PLA and PHA, which often present unique release challenges due to their different thermal behaviors.

MARKET RESTRAINTS

Regulatory Restrictions on Certain Chemical Formulations

One of the primary restraints affecting the release agents market is the increasing regulatory scrutiny surrounding certain chemical ingredients used in traditional formulations. Governments and environmental agencies globally are imposing restrictions on substances classified as volatile organic compounds (VOCs), persistent organic pollutants (POPs), and potential endocrine disruptors, compelling manufacturers to reformulate their products. For instance, the European Union’s REACH regulation mandates comprehensive safety assessments for chemicals used in industrial applications. Similarly, the U.S. Environmental Protection Agency (EPA) has introduced stricter emission standards under the Clean Air Act, targeting VOC content in industrial coatings and release agents. According to the American Coatings Association, compliance with these regulations has resulted in increased R&D expenditures for formulators, who must develop alternative compositions that meet performance requirements while adhering to legal thresholds. These regulatory pressures not only increase production costs but also delay product approvals and market entry timelines, especially for small and mid-sized players lacking the resources to invest in continuous reformulation efforts.

High Cost of Specialty Release Agents

Another significant challenge impeding the widespread adoption of release agents is the relatively high cost associated with specialty formulations designed for high-temperature applications, food contact compliance, and ultra-low residue performance. Compared to conventional release agents, these advanced products often incorporate engineered polymers, functional silicones, or hybrid wax systems that deliver superior performance but come at a premium price.

The average cost of semi-permanent silicone-based release agents is approximately two to three times higher than standard water-based alternatives. Despite their longer durability and reduced application frequency, many manufacturers in price-sensitive regions opt for lower-cost options to manage operational expenses. This pricing disparity is especially evident in emerging economies where cost optimization is a priority over process efficiency. Additionally, the transition to environmentally compliant formulations often involves additional processing steps, such as filtration and disposal of residual waste, which further increases overall costs.

MARKET OPPORTUNITIES

Development of Bio-Based and Sustainable Release Agents

A major opportunity emerging in the release agents market is the development and commercialization of bio-based and sustainable formulations designed to align with global environmental goals and regulatory mandates. Several multinational companies, including BASF and Croda International, have launched bio-derived release agents specifically tailored for food-grade and pharmaceutical applications. Moreover, the adoption of circular economy principles is encouraging the use of biodegradable and non-toxic formulations in sectors such as food packaging and medical device manufacturing. In response, research institutions and chemical manufacturers are investing in green chemistry innovations to enhance the performance characteristics of bio-based release agents. Collaborative initiatives, such as those supported by the Biobased Industries Consortium, aim to bridge the gap between eco-friendliness and industrial effectiveness, which is positioning sustainable release agents as a high-growth segment within the broader market.

Integration with Smart Manufacturing and Industry 4.0 Technologies

The integration of release agents with smart manufacturing and Industry 4.0 technologies presents a transformative opportunity for the market by enabling real-time monitoring, predictive maintenance, and optimized application processes. According to Deloitte Insights, over 60% of leading automotive and aerospace firms are investing in IoT-enabled mold management systems that track release agent coverage, temperature fluctuations, and cycle times to ensure consistent demolding performance. These systems leverage data analytics to adjust release agent dosages dynamically, minimizing excess use and extending mold longevity. Additionally, robotic spray systems equipped with AI-driven sensors are gaining popularity in high-volume production environments. As reported by McKinsey & Company, companies implementing automated release agent application systems have seen up to a 25% reduction in production downtime and improved part quality due to uniform coating distribution. Startups and technology providers are also entering the space with cloud-connected platforms that allow remote monitoring and troubleshooting of release agent performance. This convergence of chemical formulation and digital intelligence is reshaping the value proposition of release agents, transforming them from consumables into integral components of smart factory ecosystems.

MARKET CHALLENGES

Compatibility Issues with New Materials and Processes

One of the most pressing challenges facing the release agents market is ensuring compatibility with new materials and advanced manufacturing processes. As industries adopt novel composites, high-performance polymers, and additive manufacturing techniques, traditional release agents often fail to provide adequate demolding properties without compromising surface finish or material integrity.

For example, in the automotive and aerospace sectors, the increasing use of carbon fiber-reinforced polymers (CFRPs) and thermoplastic olefins (TPOs) has introduced unique release challenges due to their high resin content and sensitivity to surface contamination. Similarly, the emergence of multi-material injection molding and co-injection techniques requires release agents that can perform consistently across diverse substrates without causing interfacial issues.

Volatility in Raw Material Prices and Supply Chain Disruptions

Another significant challenge impacting the release agents market is the volatility in raw material prices and ongoing disruptions in global supply chains. The production of release agents relies on a variety of base oils, emulsifiers, polymers, and specialty additives, many of which are sourced from petroleum-based feedstocks or agricultural commodities subject to price fluctuations. According to the U.S. Energy Information Administration (EIA), crude oil prices experienced sharp swings in 2023, peaking above USD 90 per barrel before dropping below USD 75 , directly affecting the cost of mineral oils and synthetic esters used in release agent formulations. Supply chain bottlenecks, including container shortages, port congestion, and labor strikes, have further exacerbated production delays and inventory shortages.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.10% |

| Segments Covered | By Composition and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | ADM Company, AAK AB, Cargill, DowDuPont, Avatar Corporation, Par-Way Tryson Company, Associated British Foods PLC, Mallet & Company, Lecico GmbH, Lallemand and Others. |

SEGMENTAL ANALYSIS

By Composition Insights

The emulsifiers segment was accounted in holding 35.4% of the release agents market share in 2025. One key driver behind the widespread use of emulsifiers is their compatibility with food-grade release agents , particularly in bakery, confectionery, and meat processing industries. As per the U.S. Food and Drug Administration (FDA), over 80% of edible release agents approved for industrial use contain emulsifiers such as lecithin, mono- and diglycerides, and polysorbates to ensure safe and consistent performance. Additionally, emulsifiers are essential in enhancing the stability of silicone-in-water emulsions , which are widely used in injection molding and composite manufacturing. These formulations provide a controlled release effect while reducing residue buildup on molds, making them ideal for high-volume production settings. The growing adoption of water-based release agents , driven by environmental regulations and worker safety concerns, has further boosted demand for emulsifiers.

The vegetable oils segment is likely to grow with an expected a CAGR of 7.8% from 2026 to 2034. A major contributing factor is the increasing regulatory push for eco-friendly lubricants , particularly in Europe and North America. The European Union’s Renewable Energy Directive (RED) encourages the use of plant-based materials in industrial processes, prompting manufacturers to adopt vegetable oil-based release agents that are biodegradable and non-toxic. Moreover, soybean, rapeseed, and sunflower oils have gained traction due to their natural lubricity and compatibility with food contact surfaces. In addition, advancements in epoxidation and esterification technologies have improved the oxidative stability and thermal resistance of vegetable oils, enabling their use in high-temperature molding operations. Companies like BASF and Cargill have launched modified vegetable oil-based release agents tailored for rubber, plastic, and composite manufacturing, aligning with corporate sustainability goals and consumer preferences for cleaner production methods.

LEADING PLAYERS IN THE RELEASE AGENTS MARKET

BASF SE

BASF is a global leader in specialty chemicals and plays a pivotal role in the release agents market by offering high-performance formulations tailored for industrial, food processing, and composite manufacturing applications. The company focuses on developing innovative, sustainable solutions that enhance mold release efficiency while complying with environmental regulations. BASF's strong R&D capabilities allow it to create customized release agents that meet the evolving needs of automotive, plastics, and food industries.

Croda International Plc

Croda is a leading supplier of high-performance functional fluids and release agent ingredients derived from sustainable sources. The company specializes in bio-based release agents used in food processing, pharmaceuticals, and personal care manufacturing. Croda’s commitment to green chemistry aligns with growing industry demand for environmentally responsible products. Its portfolio includes emulsifiers, wax esters, and lubricants designed to ensure clean separation without compromising product quality.

Clariant AG

Clariant is a major contributor to the release agents market through its broad range of additives and specialty chemicals engineered for industrial demolding applications. The company provides silicone-based, water-based, and wax-modified release agents suited for rubber, thermoplastics, and composite molding. Clariant emphasizes sustainability by integrating renewable feedstocks into its formulations while maintaining superior performance standards. Its focus on technical support and application-specific customization helps clients optimize production efficiency and reduce maintenance downtime.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the most prevalent strategies among leading players in the release agents market is product innovation focused on sustainability. Companies are investing heavily in research and development to formulate bio-based, low-VOC, and recyclable release agents that align with tightening environmental regulations and corporate sustainability goals.

Another key approach is strategic partnerships and collaborations with end-use industries. By working closely with automotive, food processing, and composite manufacturing firms, release agent suppliers can better understand specific performance requirements and co-develop tailored solutions that enhance productivity and compliance.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the global release agents market include ADM Company, AAK AB, Cargill, DowDuPont, Avatar Corporation, Par-Way Tryson Company, Associated British Foods PLC, Mallet & Company, Lecico GmbH, Lallemand and Others.

The competition in the release agents market is marked by a dynamic interplay between established multinational chemical companies and specialized regional formulators striving to maintain relevance amid shifting industry demands. As industries increasingly prioritize sustainability, process efficiency, and regulatory compliance, release agent manufacturers are under pressure to innovate rapidly and offer differentiated product portfolios. Large players leverage their extensive R&D capabilities, global supply chains, and brand recognition to maintain dominance, particularly in regulated markets such as North America and Europe. Meanwhile, smaller and mid-sized companies are capitalizing on niche applications, custom formulations, and localized service models to carve out competitive advantages. The market is witnessing heightened rivalry as companies compete not only on product performance but also on environmental credentials, cost-effectiveness, and technical support.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, BASF launched a new line of bio-based release agents designed specifically for food contact applications. This initiative was aimed at supporting manufacturers in complying with food safety regulations while reducing reliance on petroleum-based formulations.

- In August 2023, Croda International expanded its production capacity in Southeast Asia to meet rising demand for plant-derived release agent ingredients. The expansion targeted growing markets in plastic and rubber molding, where sustainable solutions are gaining traction.

- In March 2025, Clariant introduced a high-performance silicone emulsion tailored for aerospace composite manufacturing. This product was developed to enhance mold release efficiency in high-temperature applications while minimizing residue buildup.

- In October 2025, Lubrizol Corporation acquired a specialty release agent business from a European manufacturer. This acquisition was intended to strengthen Lubrizol’s position in the industrial demolding sector and expand its presence in the European market.

- In December 2025, Michelman launched an advanced water-based release agent with enhanced film-forming properties for use in multi-cavity injection molds. This innovation was designed to improve cycle times and surface finish consistency in high-volume production environments.

DETAILED SEGMENTATION OF THE GLOBAL RELEASE AGENTS MARKET INCLUDED IN THIS REPORT

This research report on the global release agents market has been segmented and sub-segmented based on composition, and region.

By Composition

- Emulsifiers

- Antioxidants

- Vegetable Oils

- Wax & Wax Esters

By Region

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What factors are driving the growth of the Release Agents Market?

Increasing industrial production, growing demand for processed foods, expanding automotive and construction industries, and advancements in high-performance release agent formulations are key growth drivers.

2. Which type of release agent holds the largest market share?

Water-based release agents hold the largest market share due to their environmental benefits, low VOC emissions, and compliance with stringent regulations.

3. Which application segment dominates the market?

The food processing segment dominates the market owing to the extensive use of release agents in bakery, confectionery, and processed food manufacturing.

4. What are the main types of release agents available?

Release agents are available as water-based, solvent-based, silicone-based, and vegetable oil-based formulations, depending on the application.

5. What challenges does the Release Agents Market face?

Challenges include fluctuating raw material prices, stringent environmental regulations, and the need to develop sustainable and non-toxic formulations.

6. How is sustainability influencing the market?

Manufacturers are focusing on bio-based, biodegradable, and water-based release agents to reduce environmental impact and meet regulatory requirements.

7. Which distribution channels are commonly used?

Direct sales, industrial distributors, specialty chemical suppliers, and online business-to-business (B2B) platforms are the primary distribution channels.

8. What opportunities exist in the Release Agents Market?

Growing demand for eco-friendly products, increasing adoption in composite manufacturing, and expanding industrial automation present significant growth opportunities.

9. Who are the key players in the Release Agents Market?

Major companies include Henkel, Chem-Trend, McGee Industries, Croda International, and Münzing Chemie.

10. What is the future outlook for the Release Agents Market?

The market is expected to grow steadily, driven by increasing industrial production, rising demand for sustainable release solutions, technological advancements, and expanding applications across food, automotive, and manufacturing industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com