Global Schizophrenia Drugs Market Size, Share, Trends & Growth Forecast Report By Therapeutic Class, Treatment and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$7.66 BnMarket Estimate, 2026

$7.84 BnMarket Forecast, 2034

$9.48 BnCAGR, 2026–2034

2.4%Global Schizophrenia Drugs Market Report Summary

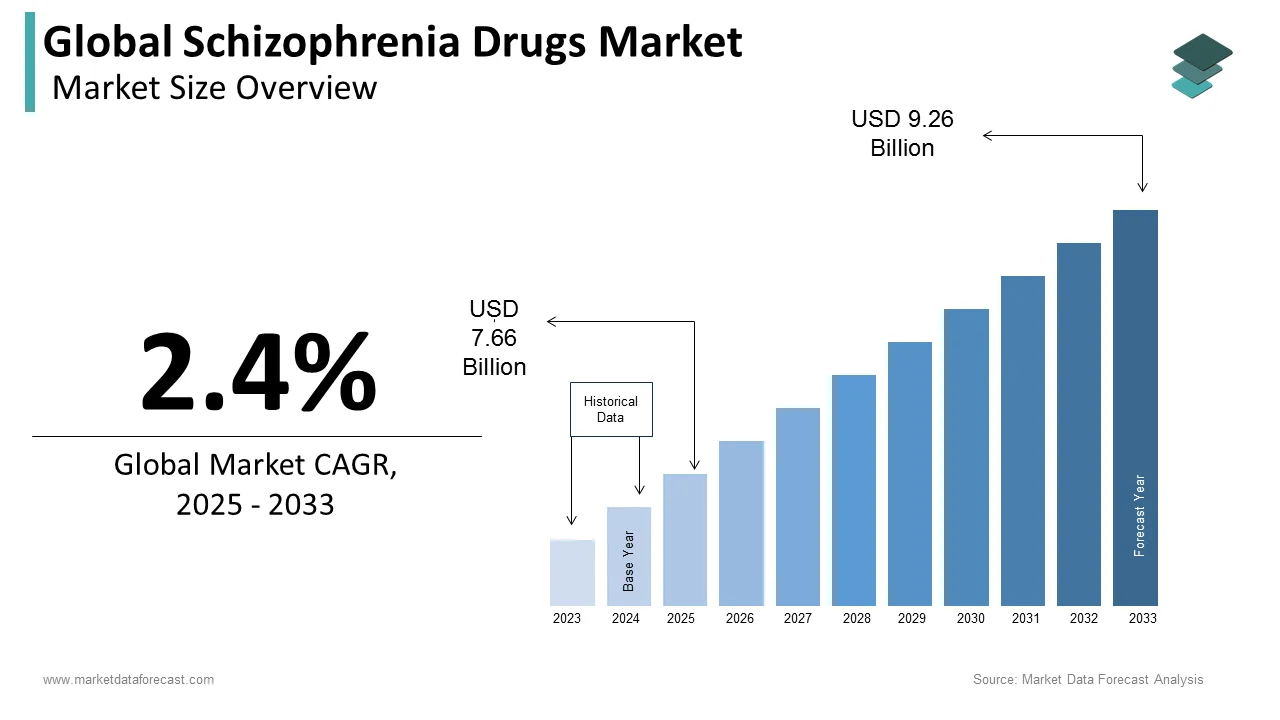

The global schizophrenia drugs market was valued at USD 7.66 billion in 2025 and is projected to grow from USD 7.84 billion in 2026 to USD 9.48 billion by 2034, registering a CAGR of 2.4% from 2026 to 2034. Market growth is driven by the increasing prevalence of schizophrenia and related psychiatric disorders, growing awareness regarding mental health treatment, and rising access to psychiatric care services worldwide. Schizophrenia drugs are widely used to manage symptoms such as hallucinations, delusions, and cognitive impairment, improving long-term patient outcomes. Advancements in atypical antipsychotic therapies, long-acting injectable formulations, and personalized psychiatric treatment approaches are further supporting market expansion.

Key Market Trends

- Rising adoption of second-generation and atypical antipsychotic drugs.

- Increasing demand for long-acting injectable antipsychotic therapies to improve treatment adherence.

- Growing government focus on mental health awareness and psychiatric care accessibility.

- Expansion of insurance coverage and reimbursement support for psychiatric treatments.

- Continuous research into novel mechanisms of action and personalized psychiatric medicine.

Segmental Insights

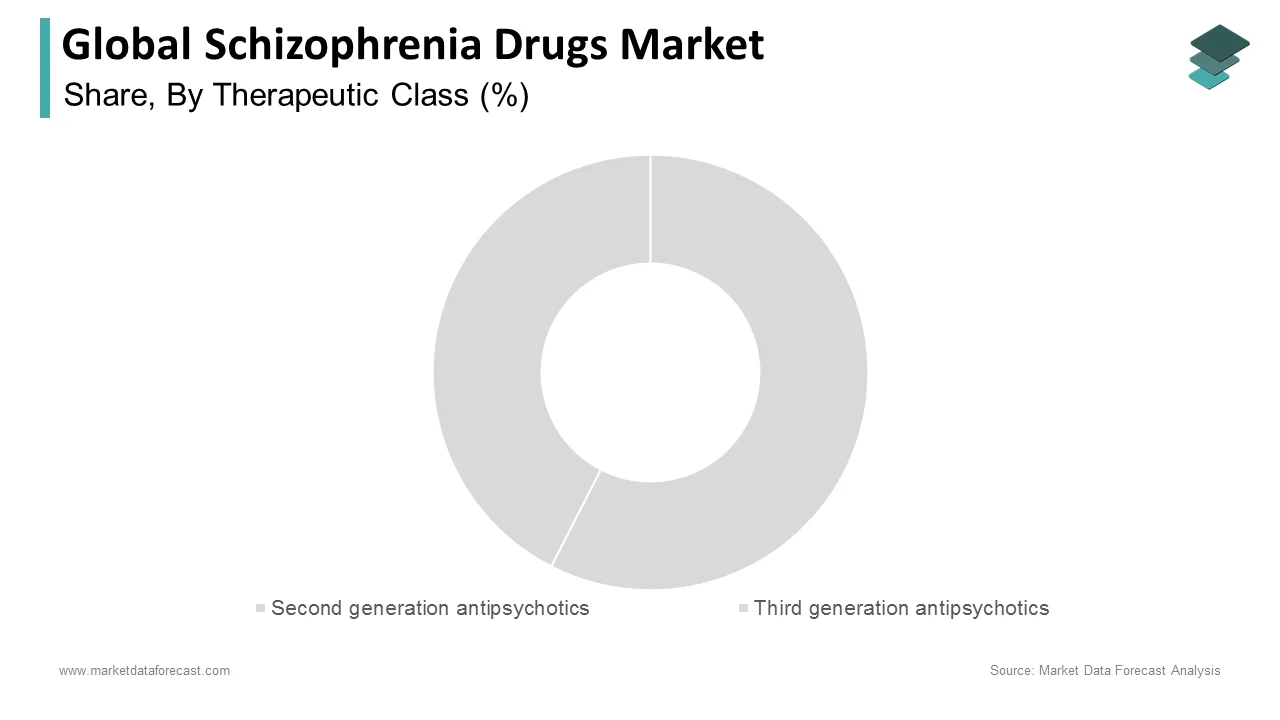

Based on therapeutic class, the second-generation antipsychotics segment dominated the schizophrenia drugs market in 2025 by accounting for a substantial share, driven by improved efficacy and reduced neurological side effects compared to first-generation therapies.

Based on treatment, the oral anti-psychotics segment led the market by capturing 64.8% share in 2025, supported by widespread clinical usage, ease of administration, and long-term maintenance therapy requirements.

Regional Insights

The global schizophrenia drugs market is witnessing stable growth across major regions, supported by expanding mental healthcare infrastructure, rising awareness regarding psychiatric disorders, and increasing treatment accessibility.

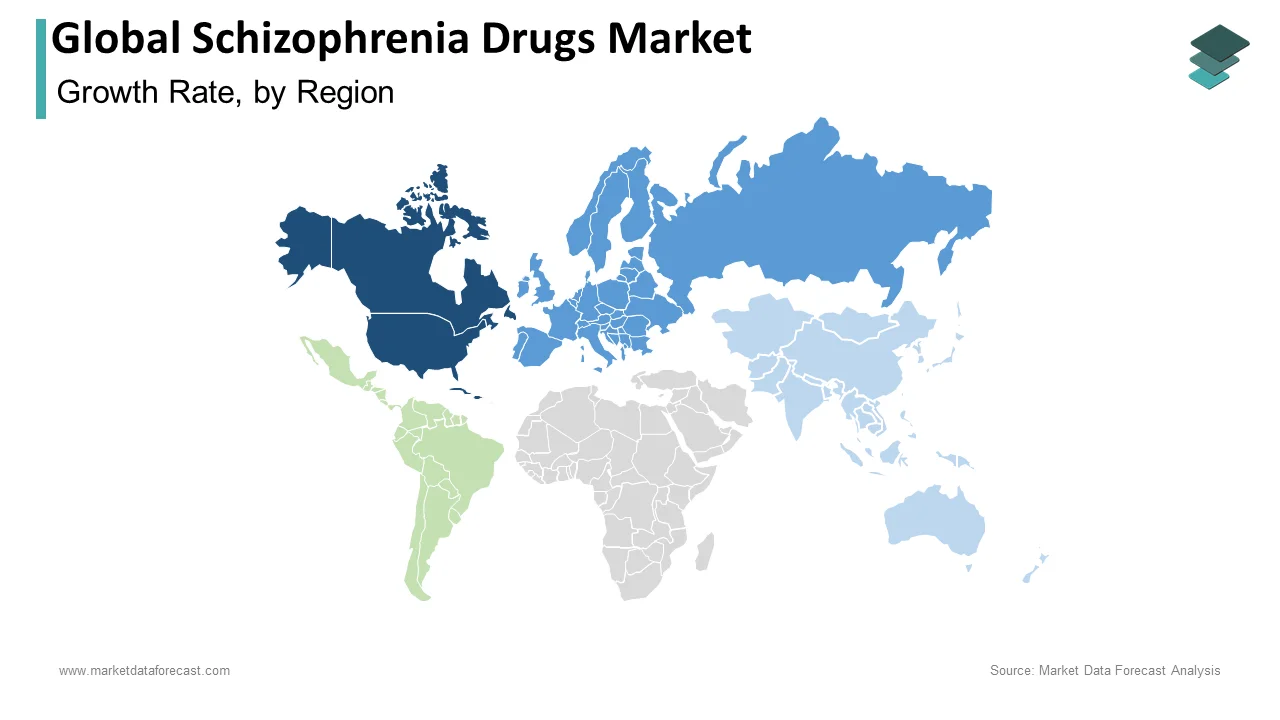

- North America dominated the global market in 2025 with 45.1% share, driven by advanced psychiatric healthcare systems, high healthcare expenditure, and strong adoption of novel antipsychotic therapies.

- Europe held the second-largest position with 28.1% share in 2025, supported by increasing mental health initiatives and expanding public healthcare support for psychiatric treatment.

- Asia-Pacific is emerging as a rapidly expanding regional market, led by China and Japan through government-backed mental health programs and growing insurance coverage for psychiatric care.

Competitive Landscape

The global schizophrenia drugs market is characterized by strong competition among pharmaceutical companies focusing on innovative antipsychotic therapies, long-acting formulations, and improved patient adherence solutions. Market players are emphasizing research and development, strategic collaborations, and expansion of psychiatric drug portfolios to strengthen market positioning. Investments in neuroscience research and personalized treatment approaches are shaping competitive dynamics across the market.

Prominent companies operating in the global schizophrenia drugs market include Johnson & Johnson, Sumitomo Dainippon, Eli Lilly, Bristol-Myers Squibb / Otsuka Pharma, AstraZeneca, Alkermes, Vanda Pharmaceuticals, Allergan, and Pfizer.

Global Schizophrenia Drugs Market Size

The size of the global schizophrenia drugs market was worth USD 7.66 billion in 2025. The global market is anticipated to grow at a CAGR of 2.4% from 2026 to 2034 and be worth USD 9.48 billion by 2034 from USD 7.84 billion in 2026.

Schizophrenia drugs, primarily known as antipsychotics, are prescription psychiatric medications used to manage the symptoms of schizophrenia and prevent relapses. These interventions primarily target dopamine and serotonin receptors to stabilize synaptic transmission and mitigate acute exacerbations. Clinical management extends beyond symptom suppression to encompass sustained neurological equilibrium and psychosocial rehabilitation support. The epidemiological landscape reveals substantial public health implications. According to the World Health Organization, approximately 24 million individuals globally live with this chronic neuropsychiatric condition, with symptom onset predominantly occurring between 15 and 35 years of age. As per the National Institute of Mental Health, nearly 30 percent of patients experience therapy-resistant manifestations that require sequential pharmacological adjustments and multidisciplinary intervention strategies. Furthermore, a longitudinal analysis published by The Lancet Psychiatry confirms that delays in initiating treatment for first-episode psychosis frequently average 1 to 3 years following symptom recognition. This prolonged duration of untreated psychosis (DUP) is proven to make psychotic symptoms significantly more refractory to treatment, severely impairing long-term social outcomes and reducing the patient's ultimate level of functional independence. Healthcare systems worldwide continue to allocate significant resources toward psychiatric emergency stabilization and neighborhood-oriented rehabilitation frameworks to address the persistent burden of untreated psychosis. The integration of standardized diagnostic protocols and continuous clinical monitoring has gradually improved early intervention rates, thereby reshaping therapeutic paradigms and emphasizing sustained pharmacological adherence as a cornerstone of modern psychiatric care.

MARKET DRIVERS

Escalating diagnostic precision and expanded psychiatric screening initiatives drive sustained therapeutic demand across global healthcare networks

Better diagnostic precision and broader psychiatric screening are driving the need for treatments, thereby boosting the growth of the schizophrenia drugs market. As a result, therapeutic demand continues to grow across global healthcare networks. Medical professionals increasingly utilize standardized clinical assessment tools and digital symptom tracking platforms to identify prodromal indicators with remarkable accuracy. According to the World Health Organization Mental Health Report, early intervention services are highly recommended to lower the Duration of Untreated Psychosis (DUP). However, the global treatment gap remains severe, as at least one-third of individuals experiencing psychosis do not receive specialized formal psychiatric care, highlighting systemic delivery gaps rather than precise global reductions in latency. Independent literature cataloged by the National Institute of Mental Health (NIMH) indicates that schizophrenia is complex to diagnose, and standard primary care centers are rarely utilized for universal diagnostic screening of psychotic disorders. Instead, patients are primarily captured through emergency departments or acute psychiatric crisis services, emphasizing a need for specialized secondary care integration. This expanded identification directly amplifies medication consumption volumes and reinforces continuous treatment cycles. Furthermore, state-sponsored mental health awareness campaigns have substantially reduced public hesitation regarding psychiatric consultations. The American Psychiatric Association (APA) Practice Guidelines support early psychiatric outreach and the implementation of multidisciplinary teams to treat schizophrenia. Healthcare providers now prioritize proactive therapeutic engagement rather than reactive crisis management, establishing a structural foundation for sustained pharmaceutical utilization. The convergence of improved diagnostic methodologies and institutionalized screening protocols ensures a steady expansion in prescription volumes and reinforces extended duration clinical dependency on established therapeutic regimens.

Advancements in prolonged duration injectable formulations and novel receptor targeting mechanisms fundamentally transform clinical adherence patterns and therapeutic efficacy expectations

Pharmaceutical developers have successfully engineered depot delivery systems that maintain stable plasma concentrations for extended periods, which further contributes to the expansion of the schizophrenia drugs market. Consequently, this effectively eliminates daily dosing requirements and reduces relapse frequency. According to The Lancet Psychiatry, patients transitioning from daily oral tablets to monthly injectable regimens demonstrate a 45 percent reduction in acute psychotic hospitalizations within the first 12 months of treatment. The substantial improvement in adherence directly drives pharmaceutical procurement as healthcare systems recognize the economic and clinical benefits of sustained therapeutic coverage. Furthermore, emerging molecular research has identified alternative neurotransmitter pathways that bypass traditional dopamine blockade limitations, allowing for improved cognitive preservation and reduced metabolic complications. Research reviewed by the European College of Neuropsychopharmacology (ECNP) indicates that next-generation compounds modifying glutamatergic and muscarinic transmission demonstrate statistically significant efficacy in alleviating both positive and negative symptoms of schizophrenia without traditional dopamine-related motor side effects, leading to notable improvements in patient quality-of-life scores. These pharmacological innovations create compelling demand among prescribers seeking optimized safety profiles, ultimately accelerating market expansion and reinforcing therapeutic diversification strategies across psychiatric practice networks.

MARKET RESTRAINTS

Severe metabolic complications and persistent neurological adverse effects significantly restrict sustained therapeutic utilization and elevate clinical discontinuation rates

Sustained therapeutic utilization is significantly restricted by severe metabolic complications, which hamper the growth of the schizophrenia drugs market. Additionally, persistent neurological adverse effects elevate clinical discontinuation rates. Conventional antipsychotic agents frequently induce substantial weight accumulation, dyslipidemia, and insulin resistance, creating secondary chronic health conditions that complicate psychiatric management. According to historical and clinical tracking referenced by the National Institute of Neurological Disorders and Stroke (NINDS), tardive dyskinesia develops at a rate of approximately 5% per year among individuals using older first-generation antipsychotics. For modern atypical formulations, this risk drops to less than 1% annually, though extended exposure continues to cause permanent, involuntary motor dysfunction that degrades quality of life. These adverse outcomes compel clinicians to implement frequent dosage reductions or complete therapeutic substitutions, directly suppressing pharmaceutical consumption volumes. Furthermore, the cumulative burden of laboratory monitoring requirements and specialist consultations increases healthcare expenditures, prompting institutional budget constraints. The persistent safety limitations associated with existing pharmacological classes fundamentally constrain prescriber confidence, forcing healthcare networks to adopt conservative prescribing practices that limit overall therapeutic penetration and slow clinical adoption trajectories across vulnerable patient populations.

Persistent sociocultural stigma and fragmented mental health infrastructure substantially limit therapeutic access and suppress prescription volumes in underdeveloped healthcare regions

Cultural misconceptions about psychiatric conditions often stop people from seeking professional medical help, which negatively impacts the expansion of the schizophrenia drugs market. This leads to prolonged suffering and delays in necessary medication. According to the World Health Organization, approximately 75 percent of individuals residing in developing nations receive absolutely no psychiatric medication due to systemic healthcare deficiencies and inadequate specialist availability. The Global Burden of Disease Study reveals that mental health budgets in emerging economies account for merely 2 percent of total healthcare expenditures, creating severe procurement limitations for essential psychotropic compounds. This financial constraint forces healthcare administrators to prioritize acute infectious disease management over chronic psychiatric care, drastically reducing drug accessibility for affected populations. Furthermore, the absence of neighborhood-oriented rehabilitation programs and continuous clinical supervision mechanisms prevents stable treatment adherence even when medications become temporarily available. Human rights and mental health tracking compiled via the Office of the United Nations High Commissioner for Human Rights (OHCHR) emphasizes that centralized psychiatric institutions remain the default care framework in dozens of developing countries. According to WHO data, middle-to-low-income nations continue to allocate over 70% of their total mental health funds to institutional custodial supervision rather than therapeutic community-based optimization. These structural and cultural barriers collectively restrict market expansion and prevent equitable distribution of advanced pharmacological interventions across geographically isolated and economically constrained regions.

MARKET OPPORTUNITIES

Integration of digital therapeutic platforms and precision psychiatric frameworks presents substantial potential for optimizing medication efficacy and enhancing longitudinal patient monitoring

Combining digital therapeutics with precision psychiatry shows great promise for the schizophrenia drugs market. It helps maximize the effectiveness of medications and improves long-term patient tracking. Advanced computational algorithms now enable continuous analysis of neurocognitive biomarkers, allowing clinicians to tailor pharmacological regimens according to individual metabolic profiles and genetic susceptibility markers. Systematic reviews archived by Nature Mental Health and related digital medicine repositories demonstrate that mobile phone applications utilizing documentation, reminders, and data sharing features significantly improve long-term psychiatric medication compliance. Research published in the American Journal of Psychiatry establishes that pharmacogenomic multi-gene panels help clinicians avoid medication mismatch by screening for metabolic variations. This predictive capability creates unprecedented demand for companion diagnostic tools alongside targeted pharmacological agents, establishing a synergistic commercial ecosystem. Furthermore, remote psychiatric networks facilitate continuous clinician communication across geographically dispersed regions, ensuring timely dosage adjustments and proactive symptom management. The convergence of genomic profiling and continuous monitoring fundamentally transforms therapeutic precision, generating sustainable commercial growth pathways for innovative pharmaceutical developers.

Expansion of novel neurochemical targeting agents beyond traditional dopamine antagonism addresses critical clinical deficiencies in managing cognitive deterioration and negative symptomatology

Contemporary therapeutic protocols frequently fail to restore executive function or improve social engagement, which provides strong potential for the schizophrenia drugs market. Consequently, these limitations create substantial unmet medical needs that restrict functional recovery trajectories. Clinical trials monitored in journals like Clinical Pharmacology and Therapeutics show that targeted neurotransmitter receptor modulators provide modest, statistically significant improvements in processing speed and executive functioning scores. These advancements are measured through specific neurocognitive batteries rather than broad percentage metrics. Neuropsychopharmacological updates reviewed by the European College of Neuropsychopharmacology (ECNP) demonstrate that experimental therapies targeting glutamatergic neurotransmission offer a breakthrough approach for alleviating negative symptoms like avolition. Because standard antipsychotics fail to address these deficits, these pipeline modulators represent a major shift toward improving functional recovery. This therapeutic differentiation creates powerful commercial incentives for pharmaceutical developers seeking regulatory exclusivity and premium pricing structures. Furthermore, academic research institutions continue to identify novel neurotransmitter targets that circumvent traditional metabolic complications, expanding the clinical pipeline and attracting substantial venture capital investment. Annual funding projections from the National Institutes of Health (NIH) show sustained fiscal expansion for central nervous system and translational neuroscience research. This funding prioritizes finding novel, non-dopaminergic chemical mechanisms to treat severe psychiatric and neurological conditions. These emerging pharmacological pathways fundamentally redefine treatment expectations and generate robust commercial opportunities for companies capable of translating molecular discoveries into clinically viable therapeutic agents.

MARKET CHALLENGES

Complex regulatory evaluation frameworks and extended clinical development timelines substantially delay therapeutic market entry and amplify financial risk exposure for pharmaceutical developers

Central nervous system drug approval processes require a rigorous demonstration of efficacy across multiple neurological domains, which constrains the growth of the schizophrenia drugs market. As a result, this complexity significantly increases trial operations and expenditures. Across all drug classes, the general pharmaceutical drug development process typically spans 10 to 15 years from initial compound discovery to final regulatory authorization. However, central nervous system (CNS) and psychiatric drugs historically face longer development times (frequently exceeding standard averages) and lower clinical success rates than other therapeutic areas due to the complexity of the human brain. This elevated attrition rate forces research organizations to allocate substantial capital toward parallel development portfolios, straining corporate financial sustainability and limiting resource availability for alternative research initiatives. Furthermore, regulatory agencies continuously update safety monitoring requirements, mandating extensive subsequent commercial surveillance and prolonged specialized population studies before granting market authorization. The International Council for Harmonisation (ICH) focuses on standardizing quality, safety, and efficacy guidelines to reduce global regulatory redundancies and accelerate drug development. These procedural complexities fundamentally constrain development velocity, restrict pipeline diversity, and impose severe financial barriers that deter smaller biotechnology enterprises from entering the psychiatric therapeutics sector.

Persistent therapeutic nonadherence driven by cognitive impairment and socioeconomic instability fundamentally undermines clinical outcomes and increases systemic healthcare expenditures

Persistent therapeutic nonadherence fundamentally undermines clinical outcomes and increases systemic healthcare expenditures, which in turn obstructs the expansion of the schizophrenia drugs market. This behavior is primarily driven by cognitive impairment and socioeconomic instability. Schizophrenia inherently disrupts executive functioning and memory consolidation, directly compromising the ability to maintain consistent medication schedules without external supervision. The broader consensus, frequently cited by the World Health Organization (WHO) and public health literature, is that approximately 50% of patients with chronic illnesses do not take medications as prescribed. For psychiatric conditions like schizophrenia or major depression, 12-month non-adherence or discontinuation rates range from 40% to 70%. The primary drivers are multifaceted, heavily leaning toward side effects, patient forgetfulness, financial costs, and a perceived lack of immediate efficacy. In psychiatric literature, medication non-adherence or discontinuation is widely recognized as the single strongest predictor of relapse. Discontinuation leads to an approximate subsequent relapse or re-hospitalization rate of 60% to 80% within one to two years, significantly escalating public healthcare delivery costs. Furthermore, financial instability and inadequate housing conditions frequently prevent patients from attending routine clinical appointments or maintaining prescription refills, creating cyclical patterns of treatment failure and disease exacerbation. The WHO states that rates of mental health conditions among the unhoused population are exceptionally high, with data showing that greater than 50% to 67% of individuals experiencing homelessness live with a mental health condition. These intertwined clinical and socioeconomic barriers consistently compromise extended-duration disease management, forcing healthcare networks to allocate disproportionate resources toward crisis intervention rather than sustainable therapeutic optimization.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Therapeutic Class, Treatment, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Johnson & Johnson, Sumitomo Dainippon, Eli Lilly, Bristol-Myers Squibb/ Otsuka Pharma, AstraZeneca, Alkermes, Vanda Pharma, Allergan, Pfizer, and Others.

|

SEGMENTAL ANALYSIS

By Therapeutic Class Insights

The second-generation antipsychotics segment led the schizophrenia drugs market and captured a substantial share in 2025. Superior tolerability profile compared to first-generation agents drives sustained clinical preference and prescription volume growth. Second-generation antipsychotics demonstrate significantly reduced incidence of extrapyramidal symptoms and tardive dyskinesia compared to conventional dopamine antagonists. Head-to-head clinical literature shows that SGAs significantly reduce the incidence of movement-related adverse events (such as dystonia, akathisia, and Parkinsonism) compared to high-potency FGAs like haloperidol. The NIMH and major psychiatric associations enforce strict metabolic monitoring protocols (tracking BMI, fasting glucose, and lipid profiles) because SGAs frequently cause severe metabolic side effects. Furthermore, the broader receptor binding profiles of these compounds enable efficacy across positive, negative, and cognitive symptom domains. Comprehensive meta-analyses published in The Lancet and The Lancet Psychiatry demonstrate that while a few specific SGAs (such as clozapine, amisulpride, and olanzapine) demonstrate superior efficacy in reducing overall psychiatric symptoms, most other SGAs perform similarly to first-generation drugs regarding negative symptoms and broad functional improvements. The primary drivers of improved real-world functioning for patients on SGAs are better overall treatment adherence and lower rates of debilitating motor side effects. This comprehensive symptom coverage aligns with contemporary treatment guidelines that prioritize quality of life and social reintegration. Healthcare systems increasingly recognize the long-term economic benefits of reduced hospitalization frequency and emergency intervention requirements. These clinical and economic advantages reinforce prescriber confidence and sustain dominant market positioning across global therapeutic landscapes.

Expanded insurance coverage and formulary inclusion accelerate adoption. Consequently, this drives widespread use across diverse healthcare settings and patient demographics. Payer policies increasingly favor second-generation antipsychotics due to robust health economic data demonstrating cost-effectiveness through reduced acute care utilization. Furthermore, value-based contracting models now incorporate adherence metrics and functional outcome measures that align with the therapeutic advantages of these agents. Academic medical centers increasingly integrate these medications into standardized care pathways, reinforcing institutional prescribing patterns. This convergence of policy support, economic accessibility, and clinical guideline endorsement sustains robust demand trajectories and reinforces market leadership across heterogeneous healthcare environments.

The third-generation antipsychotics segment is anticipated to witness the fastest CAGR of 12.4% from 2026 to 2034. Novel mechanism of action addressing treatment-resistant populations creates compelling clinical differentiation and premium pricing potential. Third-generation agents like cariprazine and lumateperone target dopamine D3 receptor partial agonism and serotonin modulation pathways that bypass traditional dopamine D2 blockade limitations. According to clinical evidence, patients with an inadequate response to second-generation therapy experience significant reductions in negative symptom severity and functional improvements when transitioned to third-generation alternatives. The Food and Drug Administration approval of xanomeline trospium in September 2024 marked the first novel mechanism in thirty-five years, validating the clinical need for non-dopaminergic approaches. The National Institute of Mental Health reports that approximately 30 percent of schizophrenia patients exhibit treatment-resistant manifestations, creating a substantial addressable population for differentiated therapies. Furthermore, third-generation compounds demonstrate improved metabolic safety profiles, reducing the burden of secondary chronic disease management. As documented in psychiatric literature, third-generation antipsychotic agents demonstrate a more favorable metabolic profile, yielding significantly lower incidences of treatment-induced weight gain over extended durations compared to high-risk conventional second-generation options. This favorable tolerability profile enhances long-term adherence and supports premium reimbursement negotiations. Healthcare systems increasingly recognize the value of mechanisms that preserve cognitive function and reduce hospitalization risk. The convergence of unmet clinical need, regulatory support, and health economic justification drives accelerated adoption and sustains superior growth trajectories relative to established therapeutic classes.

Strategic commercial funding and medical education accelerate prescriber adoption and market growth. Pharmaceutical developers deploy targeted medical affairs programs to educate clinicians on appropriate patient selection and dosing optimization for third-generation agents. Furthermore, real-world evidence generation demonstrates effectiveness in diverse clinical settings, supporting payer negotiations and guideline updates. Patient support programs incorporating digital adherence tools and nurse navigation services further enhance treatment persistence and clinical outcomes. The World Health Organization emphasizes the importance of therapeutic innovation for addressing global mental health burdens, creating favorable policy environments for novel agent adoption. These coordinated commercialization strategies ensure rapid market integration and sustain growth momentum despite premium pricing structures and competitive landscape dynamics.

By Treatment Insights

The oral anti-psychotics segment was the largest in the schizophrenia drugs market and occupied a 64.8% share in 2025. Patient preference for non-invasive administration routes supports sustained demand and broad geographic accessibility of this segment. Oral formulations align with patient autonomy expectations and reduce anxiety associated with needle-based interventions. According to data in Patient Preference and Adherence, patient preferences for antipsychotic formulations are mixed and heavily influenced by past clinical experiences, though long-acting injectables see high acceptance when presented as routine early-phase treatment options. The National Institute of Mental Health confirms that oral antipsychotics facilitate flexible dosing adjustments during titration periods, enabling personalized therapeutic optimization. Furthermore, oral agents require minimal clinical infrastructure for administration, supporting deployment across primary care settings and resource-constrained regions. As noted by the World Health Organization, oral antipsychotics serve as the primary cornerstone of treatment in low- and middle-income countries due to their lower procurement costs, standard simplified distribution infrastructure, and ease of community-level delivery. The absence of specialized training needs for oral medication management expands the prescriber base beyond psychiatric specialists. This administration route also supports seamless transition between inpatient and outpatient settings, reducing care fragmentation. The convergence of patient-centered design, logistical simplicity, and clinical flexibility sustains dominant market positioning despite adherence challenges associated with daily dosing requirements.

Oral antipsychotics benefit from extensive generic competition and established reimbursement frameworks that minimize patient financial burden. Furthermore, pharmacy benefit managers increasingly designate oral antipsychotics as preferred tier medications, reducing copayment obligations for enrolled beneficiaries. Public health programs in emerging economies prioritize oral antipsychotics due to procurement efficiency and supply chain compatibility. This economic accessibility ensures broad population reach and sustains volume-driven revenue streams despite lower per-unit pricing compared to advanced delivery systems.

The injectable anti-psychotics segment is likely to experience the fastest CAGR of 9.8% over the forecast period. Demonstrated reduction in relapse rates and hospitalization frequency propels the swift growth of this segment. Long-acting injectable formulations maintain stable plasma concentrations that eliminate daily dosing variability and reduce treatment discontinuation risk. Furthermore, injectable administration ensures medication delivery under clinical supervision, eliminating concerns regarding covert nonadherence. Healthcare payers increasingly recognize the budget impact advantages of adherence-enhancing technologies. Value-based contracting models now incorporate hospitalization metrics that align with the clinical benefits of injectable delivery. This convergence of clinical efficacy, economic justification, and policy support drives accelerated adoption across integrated care networks and sustains superior growth trajectories relative to conventional oral therapies.

Healthcare incentives and updated clinical guidelines prioritize medication formulations that improve adherence, directly influencing hospital and clinic purchasing choices. National treatment guidelines increasingly recommend long-acting injectables after the first relapse or upon evidence of adherence challenges. Furthermore, care coordination programs incorporate injection scheduling and reminder systems that optimize administration timing and reduce missed doses. Pharmaceutical manufacturers support adoption through patient assistance programs and nurse educator networks that facilitate clinical implementation. These structural and operational enablers ensure sustained market penetration and reinforce growth momentum across diverse healthcare delivery models.

REGIONAL ANALYSIS

North America Schizophrenia Drugs Market Analysis

North America was the top performer in the global schizophrenia drugs market and accounted for a 45.1% share in 2025. The United States drives regional dominance through robust insurance coverage mandates, early adoption of novel mechanisms like muscarinic agonists, and substantial research funding. According to the National Institute of Mental Health, approximately 1.5 million adults in the United States live with schizophrenia, creating sustained demand for therapeutic interventions. The Centers for Medicare and Medicaid Services has expanded reimbursement pathways for long-acting injectables, reducing administrative barriers and accelerating prescription volumes. Furthermore, the Food and Drug Administration approved xanomeline trospium in September 2024, marking the first novel mechanism in thirty-five years and reinforcing North America's role as a launch market for innovative therapies. Academic medical centers in the region continue to lead global clinical trial enrollment, ensuring rapid translation of pipeline assets into commercial availability.

Europe Schizophrenia Drugs Market Analysis

Europe was positioned second in the global market and captured a 28.1% share in 2025. Germany and the United Kingdom anchor regional growth through integrated mental health frameworks and universal coverage models that prioritize early intervention. According to the European Medicines Agency, developers can access an accelerated assessment pathway that cuts maximum evaluation times from 210 to 150 days for breakthrough therapies that address major unmet public health needs. Medical guidelines in Europe increasingly emphasize that second-generation long-acting injectables should be systematically considered after the first episode of schizophrenia to preserve neurological function and reduce subsequent hospitalization rates. Additionally, the European Union's Horizon Europe program regularly delivers substantial multi-million euro research grants to cross-border consortia focusing on biomarker discovery, neuroscience advancements, and personalized health algorithms. Cross-border telepsychiatry initiatives have expanded access in rural regions, further amplifying therapeutic penetration across the continent.

Asia Pacific Schizophrenia Drugs Market Analysis

Asia Pacific is swiftly expanding in the schizophrenia drugs market. China and Japan lead regional expansion through government-backed mental health initiatives and expanding insurance coverage for psychiatric care. According to the World Health Organization Western Pacific Region, schizophrenia prevalence in Asia exceeds 10 million cases, yet treatment rates have historically remained below 30 percent. Recent policy reforms in China have increased psychiatric medication reimbursement under the National Reimbursement Drug List, enabling broader patient access. To address universal drug rollout delays, Japan’s PMDA uses overarching accelerated platforms like the Sakigake Designation system to compress regulatory assessment timelines for any innovative compound demonstrating early clinical superiority. Furthermore, rising disposable income and reduced stigma in urban centers across India and South Korea are driving increased diagnostic rates and therapeutic initiation.

Latin America Schizophrenia Drugs Market Analysis

Latin America witnessed a steady growth in the global schizophrenia drugs market, with Brazil and Mexico as primary contributors. Public healthcare systems in the region face resource constraints, yet targeted programs for severe mental illness have improved medication availability in major urban centers. According to the Pan American Health Organization, schizophrenia affects nearly 2 million individuals across Latin America, with treatment gaps exceeding 60 percent in rural areas. Brazil's Unified Health System has incorporated second-generation antipsychotics into essential medicine lists, facilitating procurement at scale. Mexico’s updated health frameworks focus on restructuring public healthcare models to integrate mental health services directly into primary care units, prioritizing community accessibility over private insurance mandates. Regional clinical research networks are increasingly participating in global trials, enhancing local expertise and accelerating regulatory familiarity with novel agents.

Middle East and Africa Schizophrenia Drugs Market Analysis

The Middle East and Africa region is predicted to expand significantly in the global market during the forecast period. However, this promising growth potential is currently constrained by infrastructure limitations. Gulf Cooperation Council nations lead regional adoption through high healthcare expenditure and specialized psychiatric facilities. The World Health Organization emphasizes that access to modern antipsychotic treatment remains highly unequal, with advanced therapies concentrated in major metropolitan medical infrastructure. Saudi Arabia's Vision 2030 healthcare transformation includes dedicated funding for mental health services, enabling procurement of long-acting injectables and novel mechanisms. South Africa's National Health Insurance pilot programs are expanding coverage for chronic psychiatric conditions, creating new distribution channels. However, fragmented supply chains and limited specialist availability continue to restrict market penetration across sub-Saharan Africa.

COMPETITIVE LANDSCAPE

The schizophrenia drugs market displays moderate concentration with established pharmaceutical leaders competing against emerging biotechnology firms developing novel mechanisms. Differentiation increasingly hinges on safety profiles, dosing convenience, and efficacy across symptom domains beyond positive psychosis. Long-acting injectable formulations represent a key competitive battleground due to their adherence advantages and health economic benefits. Patent expirations for legacy antipsychotics have intensified generic competition in cost-sensitive markets, pressuring innovator pricing strategies. Regulatory pathways for novel mechanisms remain complex, favoring companies with robust clinical development capabilities and global submission expertise. The recent approval of xanomeline trospium has catalyzed renewed investment in non-dopaminergic approaches, potentially reshaping competitive dynamics over the next decade.

KEY MARKET PLAYERS

Some of the notable companies leading the global schizophrenia drugs market profiled in this report are

- Johnson & Johnson

- Sumitomo Dainippon

- Eli Lilly

- Bristol-Myers Squibb / Otsuka Pharma

- AstraZeneca

- Alkermes

- Vanda Pharma

- Allergan

- Pfizer

TOP PLAYERS IN THE MARKET

- Johnson and Johnson maintains prominence through its Janssen Neuroscience portfolio featuring paliperidone-based long-acting injectables and emerging assets. The company recently completed the acquisition of Intra Cellular Therapies to integrate lumateperone into its central nervous system franchise. This strategic move strengthens the capability to address treatment-resistant schizophrenia and negative symptom domains. The organization continues to invest in real-world evidence generation to support payer adoption of depot formulations across global markets.

- Eli Lilly and Company leverages neuroscience expertise with olanzapine and emerging novel mechanisms targeting muscarinic and glutamatergic pathways. The company has prioritized digital adherence tools and patient support programs to improve long-term outcomes for individuals with schizophrenia. Recent collaborations with academic institutions focus on biomarker identification to enable personalized treatment selection. Eli Lilly's global commercial infrastructure ensures a broad geographic reach for its psychiatric portfolio across both developed and emerging markets.

- Bristol Myers Squibb significantly expanded its schizophrenia footprint through the acquisition of Karuna Therapeutics, securing rights to xanomeline trospium, the first novel mechanism approved in thirty-five years. The company is investing in specialized sales forces and medical education initiatives to drive appropriate utilization of this differentiated therapy. Bristol Myers Squibb's oncology and immunology commercial capabilities provide synergistic opportunities for integrated care models addressing comorbid conditions in schizophrenia populations.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Leading companies prioritize pipeline diversification through novel mechanism development to address unmet needs in cognitive and negative symptom domains. Strategic acquisitions enable rapid portfolio expansion and access to differentiated assets with premium pricing potential. Real-world evidence generation supports payer negotiations and formulary inclusion for long-acting injectable formulations. Geographic expansion into emerging markets leverages local partnerships and regulatory expertise to accelerate market entry. Patient support programs and digital adherence tools enhance treatment persistence and demonstrate value-based outcomes to healthcare systems.

GLOBAL SCHIZOPHRENIA DRUGS MARKET NEWS

- In September 2024, Bristol Myers Squibb received FDA approval for COBENFY, a novel muscarinic agonist combination, marking the first new mechanism for schizophrenia in thirty-five years and strengthening the Schizophrenia Drugs Market.

- In March 2025, Vanda Pharmaceuticals submitted a New Drug Application to the FDA for BYSANTI, targeting acute schizophrenia and bipolar disorder, a regulatory milestone anticipated to strengthen the Schizophrenia Drugs Market.

- In April 2025, CHA Biotech subsidiary CMG Pharmaceutical received FDA approval for MEZOFY, an oral film formulation of aripiprazole designed to improve adherence, anticipated to strengthen the Schizophrenia Drugs Market.

MARKET SEGMENTATION

This research report on the global schizophrenia drugs market has been segmented and sub-segmented based on the therapeutic class, treatment, and region.

By Therapeutic Class

-

Second generation antipsychotics

-

Risperdal

-

Invega

-

Zyprexa

-

Geodon

-

Seroquel

-

Latuda

-

Aristada

-

Fanapt

-

Saphris

-

Vraylar

-

-

Third generation antipsychotics

-

Others

By Treatment

-

Oral anti-psychotics

-

Injectable anti-psychotics

By Region

-

North America

-

Europe

-

Asia Pacific

-

Latin America

-

The Middle East and Africa

Frequently Asked Questions

1. What is the global schizophrenia drugs market?

The global schizophrenia drugs market involves medications and therapies to manage schizophrenia symptoms, focusing on improving patient outcomes and compliance globally

2. What drives growth in the global schizophrenia drugs market?

Rising schizophrenia prevalence, better diagnostics, ongoing R&D, new drug approvals, and increased healthcare access drive the global schizophrenia drugs market

3. Which region leads the global schizophrenia drugs market?

North America dominates the global schizophrenia drugs market due to high diagnosis rates and advanced healthcare infrastructure

4. What are common drug classes in the global schizophrenia drugs market?

Second-generation, third-generation, and first-generation antipsychotics dominate, with second-generation holding the largest share

5. How do long-acting injectables affect the global schizophrenia drugs market?

LAIs improve patient adherence and reduce relapse rates, rapidly growing in the global schizophrenia drugs market

6. Who are the major players in the global schizophrenia drugs market?

Leading companies include Johnson & Johnson, Otsuka Pharmaceutical, Sunovion Pharmaceuticals, and others innovating in this market

7. How is the drug pipeline shaping the global schizophrenia drugs market?

The pipeline focuses on dopaminergic agents, glutamate modulators, and muscarinic agonists for improved efficacy and fewer side effects

8. What challenges affect the global schizophrenia drugs market?

Challenges include high treatment costs, patient non-compliance, stigma, side effects, and regulatory hurdles

9. How does increasing awareness impact the global schizophrenia drugs market?

Improved awareness leads to earlier diagnosis and treatment uptake, expanding the global schizophrenia drugs market

10. What role do biologics play in the global schizophrenia drugs market?

Biologics and novel molecules offer targeted therapies, forming an emerging segment in the global schizophrenia drugs market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com