Global Solar Photovoltaic (PV) Market Size, Share, Trends, & Growth Forecast Report – Segmented By Component (Modules, Inverters), Material (Silicon, Compounds), Installation Type (Ground Mounted, BIVP), Application (Residential, Commercial & Industrial, Utilities) and Region - Industry Forecast of 2024 to 2033.

Global Solar Photovoltaic (PV) Market Size

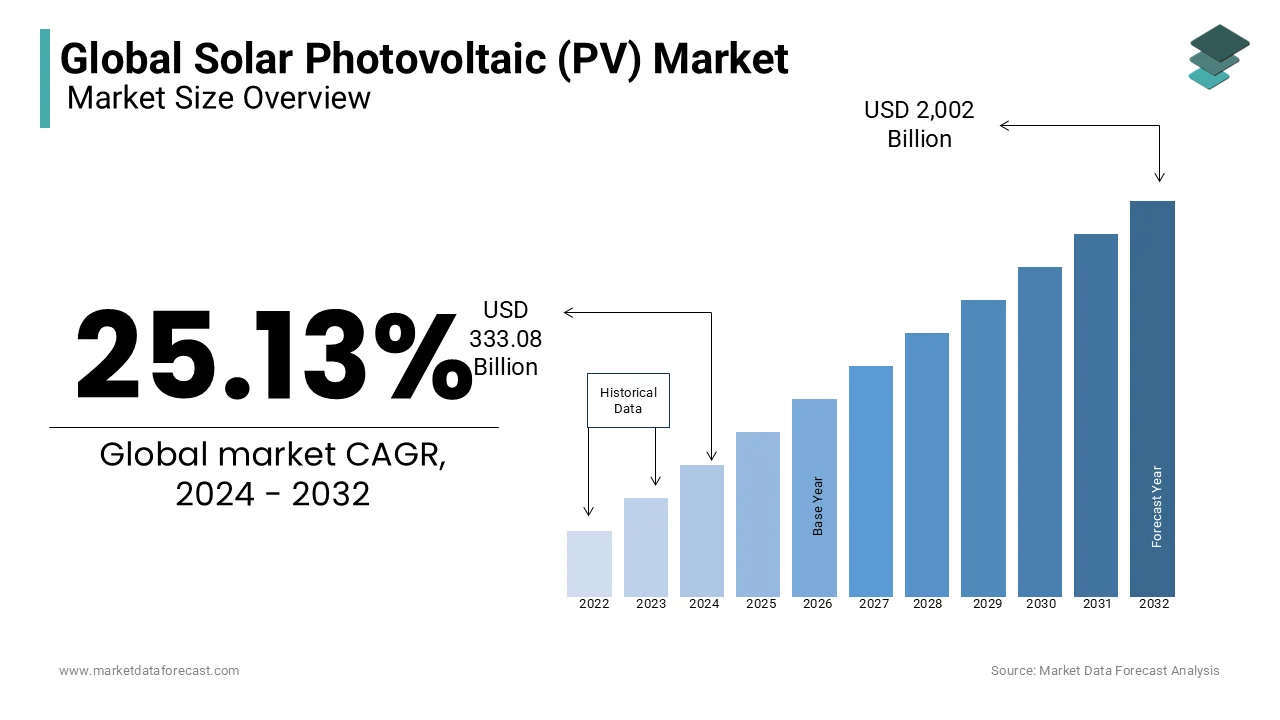

The Global Solar Photovoltaic (PV) Market is estimated to grow from USD 333.08 billion in 2024 to USD 2504.95 billion in 2033, representing a CAGR of 25.13%.

Solar photovoltaic is the deployment and manufacture of systems that convert sunlight into electricity through semiconductor technology. This sector is evolving rapidly: as per the International Renewable Energy Agency, the worldwide installed solar capacity surpassed 1,100 GW in 2022, with solar projected to contribute over half of global electricity by 2050 according to IRENA. Meanwhile, in Europe alone, solar PV capacity rose from 164 GW in 2021 to nearly 260 GW by 2023 by supplying over 9% of the EU’s electricity in 2023 as per SolarPower Europe.

MARKET DRIVERS

Acceleration of Global Deployment and Policy Backing

The expansion of infrastructure with supportive policy frameworks is driving the growth of the solar photovoltaic market. Europe’s solar capacity leapt from 164 GW in 2021 to 259.99 GW by 2023, with solar providing 9.1% of electricity generation in the EU in 2023, with the impact of favorable regulation and subsidies as per SolarPower Europe. Additionally, projections from the US NREL study suggest solar’s share of US electricity could rise from 3% in 2020 to 40% by 2035, if annual installations ramp up to 30 GW_AC annually between 2021 and 2025, then further to 60 GW_AC from 2025 to 2030, with the important role of policy-driven large-scale uptake.

Technological Gains and Cost Declines

Technological innovation with cost effectiveness and performance is also expected to expand the growth of the solar photovoltaic market. According to the IEA, the carbon intensity of solar manufacturing has halved since 2011, although overall emissions rose due to expanded production, underscoring efficiency improvements. In thin-film PV, perovskite technologies have achieved lab efficiencies of 26.7%, while CdTe and CIGS reached 23.1% and 23.6% respectively, as recently reviewed in academic literature. These advancements are delivering higher power yields and reducing material use, which are pivotal to lowering levelized costs and expanding applications across flexible and integrated solutions.

MARKET RESTRAINTS

Supply Glut and Market Instability

The unfolding supply overhang in China is significantly hindering the growth of the solar photovoltaic market. China’s polysilicon production now stands at roughly 3.23 million tons, nearly double the expected demand by prompting a proposed ¥50 billion restructuring fund aimed at curbing overcapacity. This glut has forced shutdowns of solar enterprises and widespread layoffs, pointing to fragile market dynamics. Excessive supply risks destabilizing prices, undermining margins, and dissuading investment, particularly if capacity remains decoupled from actual installation demand with a supply-side restraint that could throttle sustainable market growth.

Policy Uncertainty and Investment Slowdown

The policy shifts and dwindling subsidies are beginning to dampen solar configurations is to hamper the growth of the solar photovoltaic market. In the US, solar capacity additions are forecast to drop from 48.6 GW in 2025 to 43.5 GW by 2030, driven by tariff pressure and potential cuts to clean energy tax credits, according to SEIA and Wood Mackenzie. Similarly, China’s elimination of guaranteed pricing for renewables has triggered a slowdown in second-half 2025 installations, despite record performance in H1 with 212 GW added, which is signaling growing investor caution.

MARKET OPPORTUNITIES

Expanding Residential Rooftop Adoption

Residential PV represents a vast and growing segment that is creating new opportunities for the growth of the solar photovoltaic market. In India, rooftop solar installations are expected to more than double to 4 million by March 2026, under the PM Surya Ghar Muft Bijli Yojana, which promotes free electricity and aggregated utility models by signifying durable grassroots expansion. These installations not only reduce grid dependence but also democratize energy generation.

Rebalancing Overcapacity to Support Global Demand

China’s production overcapacity, while currently a burden, shall pose new opportunities for the growth of the solar photovoltaic market in the next coming years. Analysts note that global solar installations surged 32% in 2024, but supply far outpaces demand, particularly in China. This surplus could be mobilized to meet burgeoning global deployment needs in developing nations are helping to triple renewable generation by 2030.

MARKET CHALLENGES

Grid Constraints and Infrastructure Bottlenecks

Grid readiness in accommodating rapid PV deployment is likely to degrade the growth of the solar photovoltaic market. For instance, in Australia, despite achieving 40.6 GW of PV capacity by March 2025, representing nearly 20% of national electricity, project pipelines are jeopardized by transmission delays, approval lags, and workforce shortages, according to the Clean Energy Council. Without commensurate upgrades in infrastructure and permitting processes, solar additions risk stalling. These operational lags can deflate project financing, hinder timely delivery, and raise costs—challenging the pace of solar integration into the broader electricity system.

Pollution-Induced Performance Losses

Air pollution poses a non-obvious but meaningful threat to PV efficiency, which also hinders the growth of the solar photovoltaic market. In Delhi, urban haze reduced silicon panel insolation by approximately 11.5% (±1.5%), equating to losses of 200 kWh/m² annually, according to empirical research. Extrapolating globally, economic losses due to pollution-related PV underperformance could amount to billions of dollars each year. Fine particulates reduce light transmission, dampen output, and undermine revenue projections. In polluted regions, deployment strategies must factor in such forgone yield by challenging the assumption that solar output is uniformly predictable and underscoring the need for environmental mitigation to preserve PV ROI.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2023 |

| Forecast Period | 2024 to 2033 |

| CAGR | 25.13% |

| Segments Covered | By Component, Material, Installation Type, Application, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Trina Solar Ltd, Kaneka Corporation, Kyocera Corporation, Panasonic Corporation, Sharp Corporation Ltd, BP Solar International, Bloo Solar Inc., 1366 Technologies Inc., 3GSolar Photovoltaics Ltd., Canadian Solar Inc., JA Solar, First Solar Inc., Jinko Solar Holding Company Ltd, Yingli Green Energy Holding Co. Ltd, Renesola, Sun Power Corporation, Solar World AG, Mitsubishi Electric Corporation, and Others. |

SEGMENTAL ANALYSIS

By Component Insights

The silicon-based solar modules segment accounted in holding a significant share of the solar photovoltaic market in 2024. With the mass deployment in utility, residential, and commercial-scale projects. Modules form the core visible surface of PV systems, thus benefiting directly from economies of scale which drive cost-per-watt down. Industrial expansion in Asia alone has slashed manufacturing costs, reinforcing market control.

The inverters segment is likely to grow with a prominent CAGR in the coming years due to the soaring demand for smart, grid-interactive systems in residential and utility applications, as well as the rising complexity of power conversion needs in hybrid and storage-integrated setups. Inverter innovation in efficiency, digital integration, and two-way grid functionality is thus fueling rapid growth.

By Material Insights

The silicon reigns segment held the dominant share of the solar photovoltaic market in 2024. According to the International Technology Roadmap for PV (ITRPV) in 2024, nearly 98% of PV production derived from silicon wafer–based technology, with n-type wafers comprising about 70% of output. Silicon's superiority is underpinned by its proven reliability, high conversion efficiency, and well-established manufacturing infrastructure. Its abundance, falling costs due to economies of scale, and solid performance make silicon the foundational material across residential, commercial, and utility PV installations.

The while silicon segment is anticipated to hit the highest CAGR in the coming years with the growing demand for the systems that integrate seamlessly into building fabrics by offering both structural and energy-generation roles. Innovations in compound materials such as perovskites with efficiencies now exceeding 18% also contribute to compound segment acceleration by enabling lightweight, flexible, and architecturally adaptive solutions.

By Installation Type Insights

The ground-mounted installations segment accounted in holding a dominant share of the solar photovoltaic market in 2024. These systems benefit from economies of scale large-scale arrays configured for optimal solar capture and versatile site usage, including repurposed land or rural areas.

The Building-integrated photovoltaics (BIPV) segment is expected to growing at a significant CAGR of 20.9% during the forecast period, owing to the rising demand for energy-harvesting architectural finishes, especially in regions prioritizing sustainability and design coherence.

REGIONAL ANALYSIS

Asia Pacific Solar Photovoltaic (PV) Market Insights

Asia Pacific was the top performer of the solar photovoltaic market with 55.4% of the share in 2024 from surging demand in China, accounting for nearly half of cumulative global installations, and robust policy frameworks.

Europe Solar Photovoltaic (PV) Market Insights

Europe was positioned second with a significant share of the solar photovoltaic market in 2024. In Q1 2025, Europe's solar generation rose 32% year-on-year to 68 TWh, with Germany alone achieving 11% of its power from solar and Poland skyrocketing solar output by 677% since 2020 Reuters. The region’s green energy policies, climate-aligned targets, and public support mechanisms are actively driving adoption at scale.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the global solar photovoltaic (PV) market include Trina Solar Ltd, Kaneka Corporation, Kyocera Corporation, Panasonic Corporation, Sharp Corporation Ltd, BP Solar International, Bloo Solar Inc., 1366 Technologies Inc., 3GSolar Photovoltaics Ltd., Canadian Solar Inc., JA Solar, First Solar Inc., Jinko Solar Holding Company Ltd, Yingli Green Energy Holding Co. Ltd, Renesola, Sun Power Corporation, Solar World AG, Mitsubishi Electric Corporation, and Others.

The solar photovoltaic industry is characterized by intense rivalry among a concentrated group of vertically integrated manufacturers and system providers. Leaders continuously vie for efficiency supremacy through advancements in module technology, from PERC to TOPCon and bifacial innovations. Market competition also spans regional expansion—firms race to establish localized manufacturing footprints to capitalize on incentives and mitigate tariffs. There is growing convergence between module makers and energy systems developers as competitive advantage now hinges on offering integrated PV-plus-storage solutions.

Top Players in the Solar Photovoltaic Market

Jinko Solar

Jinko Solar is a Chinese PV heavyweight, has been intensifying its presence across the Asia-Pacific. The firm recently expanded production capabilities via a joint venture in Malaysia and other ASEAN regions, leveraging regional incentives to boost module output. Additionally, it has been deploying innovative bifacial and PERC technologies to cater to the evolving requirements of utility-scale and distributed installations.

JA Solar Technology Co.

JA Solar has reinforced its footing in the Asia-Pacific photovoltaic arena through targeted capacity expansions and technology adoption. The company introduced high-efficiency, low-light tolerant modules compatible with tropical and monsoon climates. It also scaled operations by increasing wafer and cell manufacturing footprints in key Asian industrial hubs. These moves strengthen delivery pipelines and local responsiveness by ensuring that JA Solar remains deeply interconnected with Asia-Pacific demand cycles and regional energy policies.

Trina Solar

Trina Solar continues to escalate its influence in Asia-Pacific via R&D-led differentiation and strategic partnerships. Recently, the firm launched a collaborative initiative with regional EPC developers to pilot smart PV systems with embedded energy management. It has also rolled out high-density module lines and energy storage hybrids in India and China to complement rooftop and utility projects.

Top Strategies Used by Key Market Participants

Key players in the solar PV market have deployed a strategic playbook rooted in vertical integration, geographical diversification, technological advancement, and localization of supply chains. Most firms particularly Chinese majors have moved downstream into cell and module fabrication to capture greater value. Others are establishing manufacturing in regions like Southeast Asia and India to optimize logistics and tariff exposure. Investments in next-gen module technologies like TOPCon, bifacial, and smart modules enhance their competitive edge.

RECENT MARKET HAPPENINGS

- In June 2024, Jinko Solar inaugurated a high-capacity production line in Malaysia, bolstering its regional supply resilience and lowering logistic costs.

- In March 2023, JA Solar commenced operations of a new wafer-and-cell manufacturing hub in Southeast Asia to localise production and shield against trade barriers.

- In January 2024, Trina Solar launched a smart integrated PV solution pilot project with engineering partners in India, shifting toward system-level offerings.

- In April 2024, Jinko Solar signed a strategic partnership with a regional utility in Indonesia to develop bifacial module deployments tailored to tropical climates.

- In May 2023, Trina Solar entered into a collaborative R&D agreement focused on energy management-integrated modules with a leading Asian EPC firm.

MARKET SEGMENTATION

This global solar photovoltaic (PV) market research report has been segmented and sub-segmented based on component, material, installation type, application, and region.

By Component

- Modules

- Inverters

By Material

- Silicon

- Compounds

By Type

- Ground-mounted

- BIPV

By Application

- Residential

- Commercial & Industrial

- Utilities

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the Solar Photovoltaic (PV) Market growth rate during the projection period?

The Global Solar Photovoltaic (PV) Market is expected to grow with a CAGR of 25.13% between 2024 and 2033.

What can be the total Solar Photovoltaic (PV) Market value?

The Global Solar Photovoltaic (PV) Market size is expected to reach a revised size of USD 2504.95 billion by 2033.

Name any three Solar Photovoltaic (PV) Market key players?

Kyocera Corporation, Panasonic Corporation, and Sharp Corporation Ltd are the three Solar Photovoltaic (PV) Market key players.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com